AEM - Agnico Eagle: Too Cheap To Ignore

2023-10-04 11:06:29 ET

Summary

- Agnico Eagle Mines is down sharply from its highs, and is a case of the proverbial baby being thrown out with the bathwater.

- This is because the company offers low-capex growth, industry-leading margins, and diversification in top-tier jurisdictions, yet trades at a significant discount to its historical multiple.

- In this update, we'll look at its relatively low capex growth opportunities, its valuation after this sharp correction, and why AEM stock is a premier pick for gold exposure.

It's been a rough stretch for the Gold Miners Index ( GDX ), with the sector finding itself down ~30% from its May highs despite a relatively mild 12% decline in the gold price. This is even more disappointing considering that the index is down nearly 50% from its Q3 2020 highs in a period where the gold price is relatively flat, which might be causing many investors to scratch their heads.

Unfortunately, it's not this simple, and while the gold price has held its ground above $1,800/oz outside of brief excursions below this level, margins have been pinched severely, impacted by rising labor, fuel, and consumables costs. The result has been a more than 35% decline in margins sector-wide from peak levels in Q3 2020, and up to 70% declines in margins for more leveraged producers.

Fortunately, Agnico Eagle Mines Limited (AEM) is not in the latter camp. For starters, it benefits from a higher employee/contractor ratio. Second, it is one of the few producers to hedge fuel prices, meaning it's less sensitive to rises in fuel prices like we saw in Q3 that will impact margins for some producers. Third, it added one of the world's largest gold mines and two of the world's highest-grade mines at an attractive price with Detour Lake, Fosterville, and Macassa, helping it to maintain its industry-leading margins in this period of inflationary pressures. And since then, the company has been working to ensure it can maintain sub $1,100/oz all-in sustaining costs with the company putting the pieces in place to set Malartic up to be a 900,000 ounce per annum operation post-2030, and potentially add an incremental 250,000 ounces at Detour Lake as well.

Hence, I think this is a case of a sector leader being thrown out with the bathwater, which doesn't happen every week. This provides an opportunity to add exposure to AEM.

Kittila Operations - Company Website

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q3 Outlook

Beginning with the Q3 outlook, most producers should benefit from higher production as the bulk of the sector has back-ended weighted production. While Agnico Eagle is slightly different with a similar Q3 vs. Q2 2023, 2024 should be a much better year, with full ownership of Canadian Malartic set to push production up over 4% to 3.5+ million ounces per year. And while some companies will struggle with the rise in energy prices in Q3 with a flat to down gold price, Agnico Eagle has done a phenomenal job hedging ~64% of its diesel exposure for the remainder of 2023 at a price of $0.69/liter, more than 25% below its cost guidance assumption of $0.93/liter.

Hence, I am surprised that AEM has slid at a similar rate to its peer group given that it's more insulated from the negative setup of rising energy prices and lower gold prices that most producers will face in Q3, with a more pronounced impact in Q4 as the metal has slid below $1,900/oz.

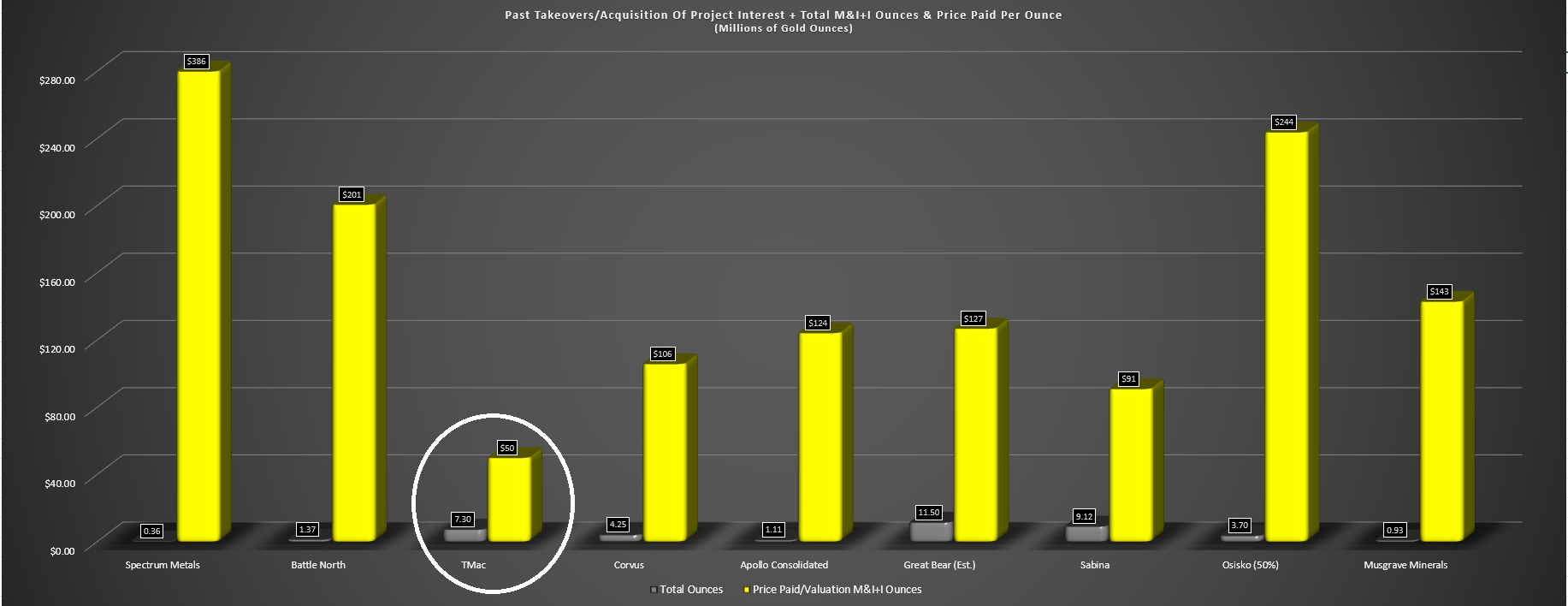

Past Takeover Prices On Per Ounce Value vs. AEM/TMac Acquisition - Company Filings, Author's Chart & Estimates

{kind=link}

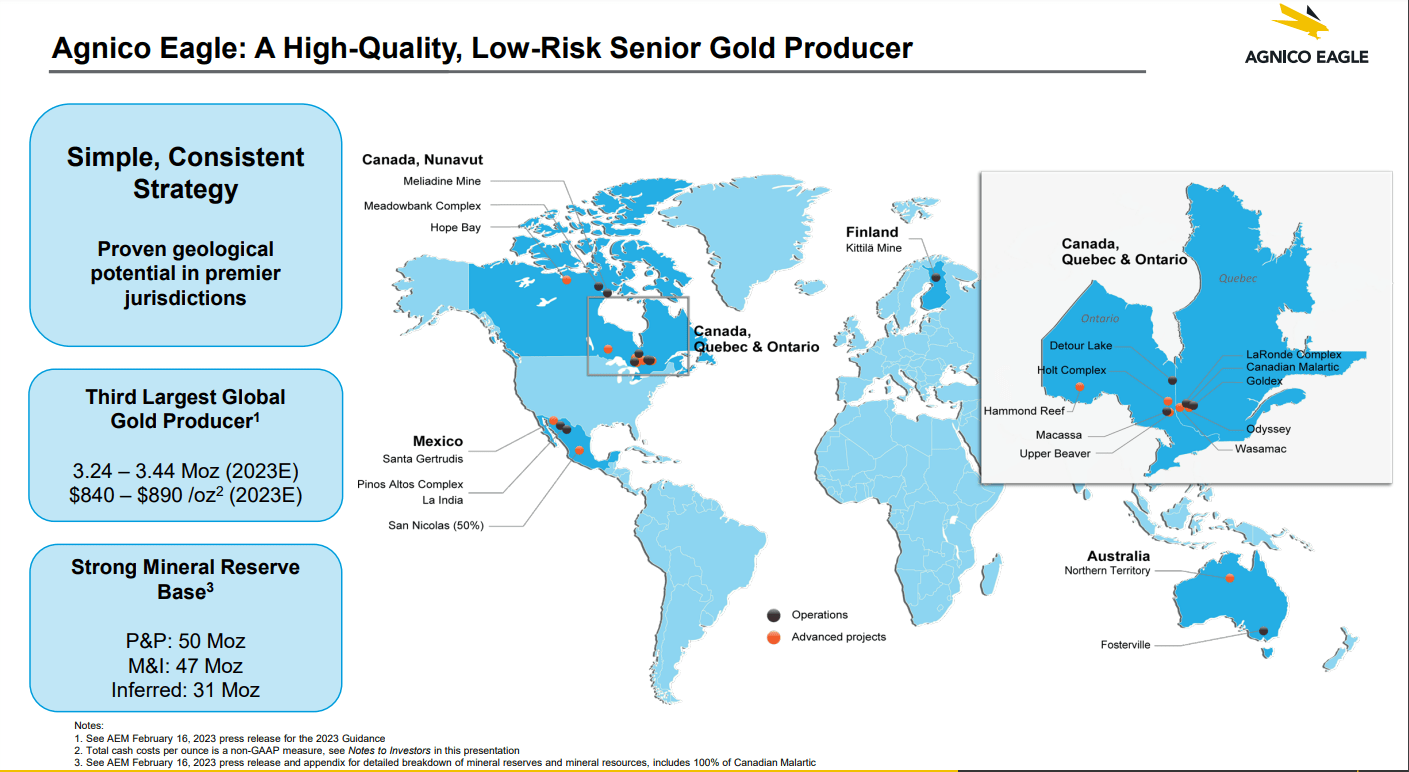

However, while many investors focus on the short term, I think the bigger picture is far more important, and this is where Agnico Eagle excels and doesn't get nearly enough credit. For starters, the company continues to increase its exploration budget at Hope Bay, an asset that it picked up for a song at ~$50/oz on total resource ounces with significant sunk capital, and an operation that ultimately be the next Meliadine for the company, capable of producing upwards of 350,000 ounces per annum in a jurisdiction where it already operates and has a competitive advantage (labor, contractor, supplier network). Meanwhile, the opportunity in the Abitibi Region is just as significant, yet the market doesn't seem to giving the company any credit for these opportunities with the stock continuing to trade well below its all-time highs despite being a more diversified producer, a high-margin producer, and one with material organic/low-capex growth opportunities in Tier-1 jurisdictions with the best pipeline it's ever had in its history.

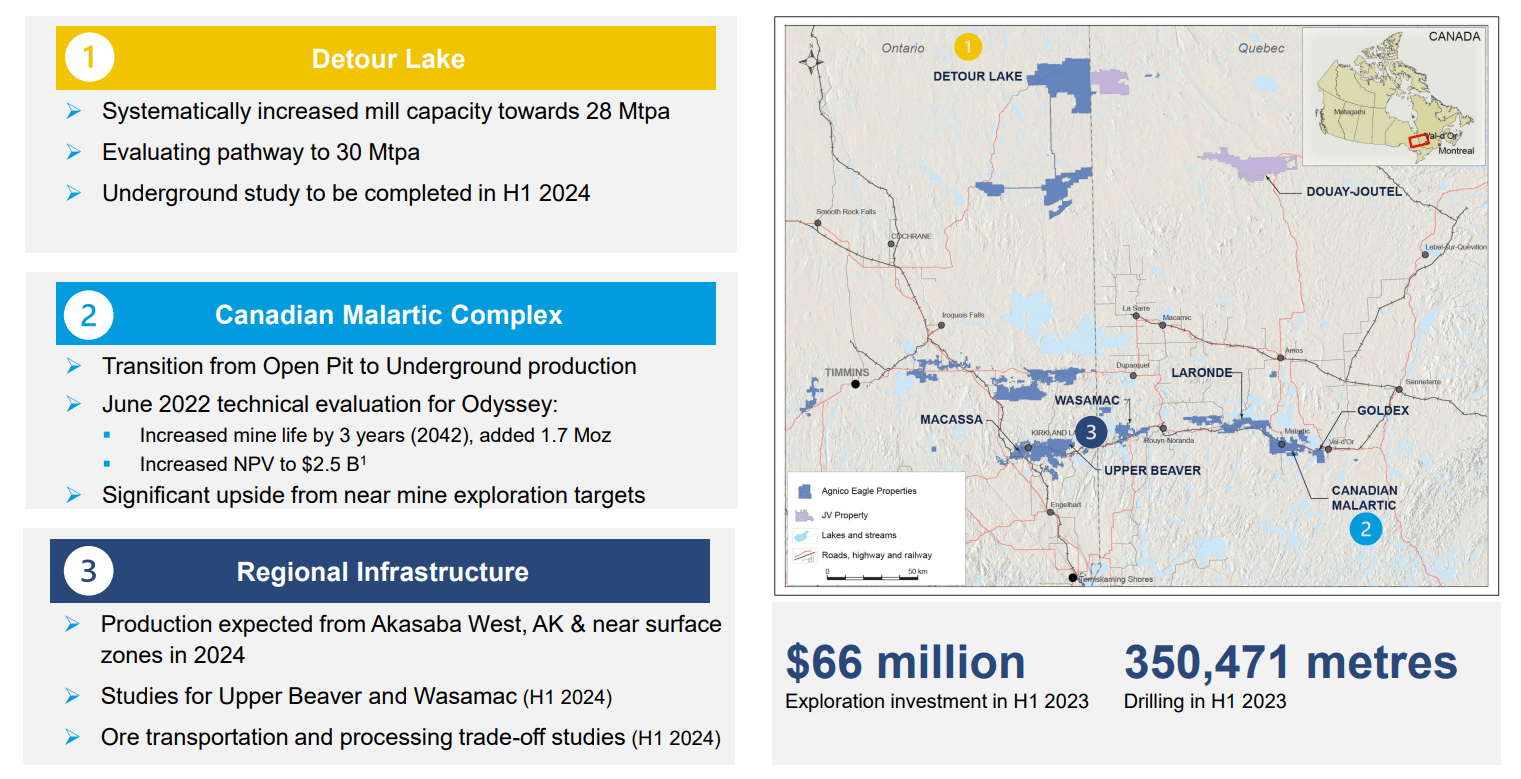

The Opportunity In The Abitibi Region

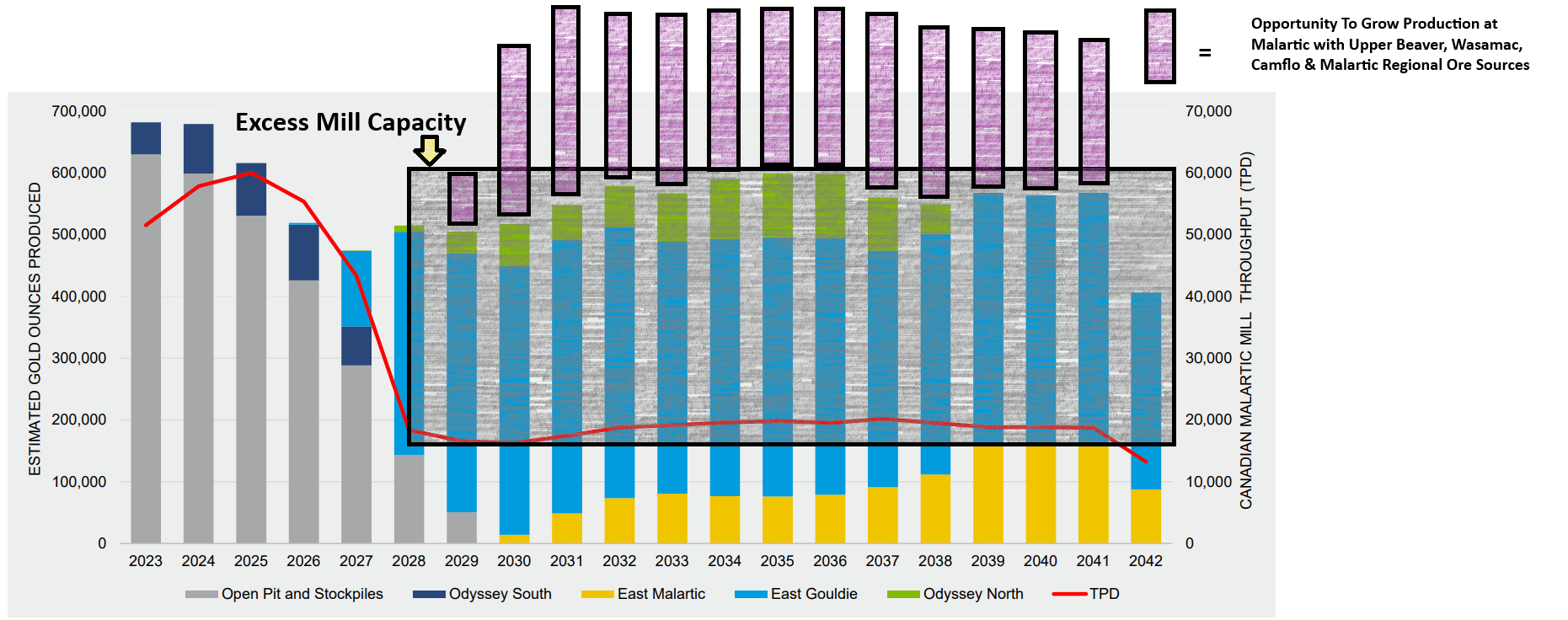

Outside of a potential opportunity to increase production to ~1.0 million ounces per annum through further throughput increases and underground potential at Detour Lake, the opportunity to the south running from Macassa west of the Ontario/Quebec border to Canadian Malartic is massive. This is because the company's recent acquisition of Yamana's Canadian operations (50% Canadian Malartic and Wasamac) has given the company full control of the massive Canadian Malartic [CM] Mill (60,000 tonnes per day) and another spoke for a future regional milling strategy, on top of a growing resource base in the Kirkland Lake Camp (ex-Macassa). With the mill full over the past decade processing lower-grade Malartic ore, the opportunity wasn't there to take advantage of this excess capacity. However, these acquisitions have lined up with the Malartic Mill getting ready to throttle down to ~20,000 tonnes per day, as the dominant ore source is Odyssey Underground, once open-pit and stockpile inventory is exhausted in 2028.

Abitibi Region Production & Opportunity - Company Presentation

{kind=link}

As noted by the company in previous releases, the company is looking at potentially hauling ore from these million ounce orphaned deposits (Wasamac, Upper Beaver) to take advantage of 40,000 tonnes of excess daily capacity at the CM Mill at the end of this decade. Assuming 5,000 tonnes per day from each operation, Wasamac could support ~140,000 ounces per year of incremental production at ~2.6 grams per tonne of gold over 12 years based on its current reserve inventory, and Upper Beaver could support ~260,000 ounces over five years at an average grade of 5.0 grams per tonne of gold.

The result is ~400,000 ounces of incremental production by utilizing just one-fourth of the excess capacity that will be available at the CM Mill post-2028. And while five years of contribution might not seem like much based on its ~8.0 million tonne reserve base, I am confident that the team can successfully convert resources to support a 12+ million tonne reserve base or a ~7-year mine life at 5.0+ grams per tonne of gold.

Notably, this does not include regional opportunities like Camflo which could take advantage of a portion of the other 30,000 tonnes per day of excess capacity to lift production closer to 1.0 million ounces per annum in peak years potentially.

Canadian Malartic Production Profile with Odyssey + Upside Potential - Company Presentation, Author's Notes & Drawings

{kind=link}

Outside of the obvious benefit from a cash flow standpoint from turning a ~550,000 ounce operation into a 900,000+ ounce operation, this growth is highly attractive because it's relatively low capex and easier to permit. The reason is that Upper Beaver and Wasamac would have smaller footprints than previously envisioned if these trade-off studies prove lucrative (delivering ore by rail from these two deposits), with no need for a stand-alone processing facility which cuts out a significant portion of required capex to build these assets. In addition, this production is coming from within Agnico Eagle's backyard, making it low-risk growth and it will also benefit from its position as a partner and employer of choice in the region. So, while other producers have major growth opportunities in their pipelines like block caves, super pits, and forays into new regions with massive copper-gold projects, I see AEM's growth as lower-capex and with less technical and jurisdictional, making this opportunity superior.

Let's take a look at the valuation and see whether the market has clued into the opportunity to add ~600,000 ounces within the Abitibi region by the end of the decade (Detour: +300,000 ounces, Upper Beaver/Wasamac: +380,000 ounces, AK/Upper Canada: + 30,000 ounces, offset by lower production at Odyssey vs. Malartic during transition to underground), and up to 350,000 ounces per annum in Nunavut with Hope Bay.

Valuation

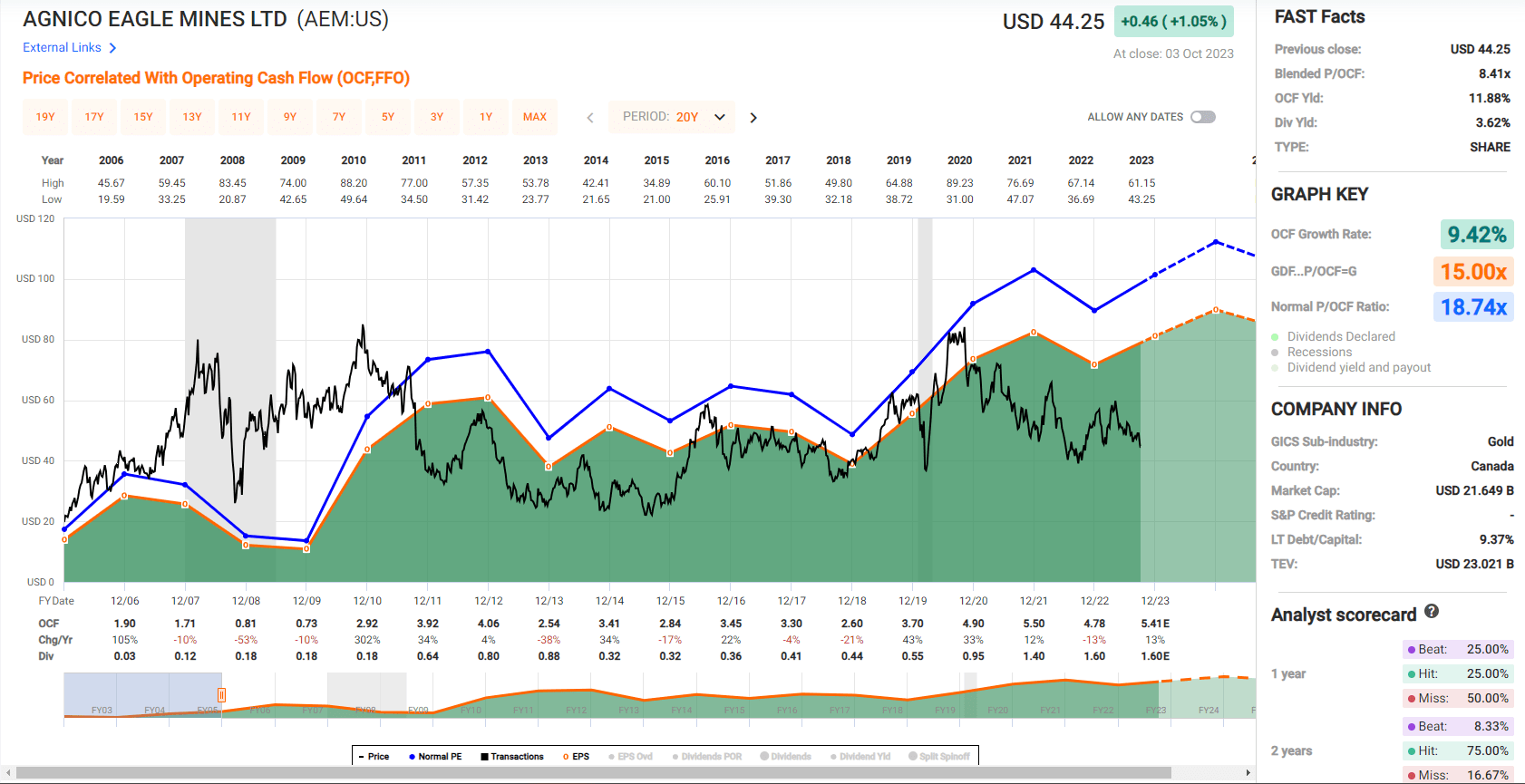

Based on ~495 million shares and a share price of $44.00, Agnico Eagle trades at a market cap of ~$21.8 billion and an enterprise value of ~$23.3 billion. This makes Agnico Eagle one of the top-5 largest capitalization companies in the sector, and has left the stock trading at just ~7.7x FY2024 cash flow per share estimates of $5.70, a massive discount to its historical multiple of ~18.7x cash flow and a ~40% discount to its 10-year average cash flow multiple of ~13.0x cash flow. Given that Agnico Eagle obviously has a lower growth rate than it did in the 2000-2015 period when it brought multiple new mines online (LaRonde Expansion, Lapa, Goldex, Kittila, Meadowbank, Pinos Altos, La India), I don't think it reasonable to expect it to trade at 20.0x to 40.0x cash flows near its peaks like it did in this high growth period when gold was in a secular bull market. However, even if we apply a more conservative multiple of 11.5x cash flow, I see a fair value for AEM of $65.60 - pointing to a 40% upside from current levels or a ~45% return on a total return basis.

Agnico Eagle Mines - Historical Cash Flow Multiple - FASTGraphs.com

{kind=link}

It's important to note that this fair value estimate assumes no upside in the gold price above $1,900/oz. In addition, this fair value assumes that the multiple compression we've seen sector wide persists, given that as recently as Q4 2020 Agnico Eagle traded as high as 18.0x cash flow (a 50% premium to the conservative multiple I've used to derive fair value).

Finally, it assumes that Agnico Eagle does not buy back shares to boost its per share metrics, which would not surprise me given the opportunity to scoop up shares at a discount ahead in this period of malaise for the sector. In fact, the company has historically taken advantage of buying back shares at similar levels, repurchasing ~1.7 million shares at a weighted average price of $44.70 last year, and an additional 100,000 shares at $47.75 in Q1. In summary, this 18-month price target could end up proving conservative.

Diversification & Tier-1 Jurisdiction Production Profile - Company Presentation

{kind=link}

However, for a long-term outlook, I think this is a business capable of generating upwards of $7.50 per share in cash flow and trading at a cash flow multiple of 12-16 as it has historically commanded a premium to its peer group because of its capital discipline, superior jurisdictional profile and industry-leading margins. So, using the high end of this range for multiples where it should trade in a more favorable gold price environment, this is a stock that could easily trade above $100.00 per share over the next three years while providing diversification and sleep-well-at-night exposure to the gold price. This is important because there is no shortage of headaches for investors in this sector, from serial share dilution to sloppy M&A and issues at mine sites. However, AEM has proven to be disciplined and outperforms from a margin standpoint because of its focus on high-quality and above-average grade assets in its backyard (less reliance on contractors), meaning it passes Warren Buffett's #1 rule of "don't lose money."

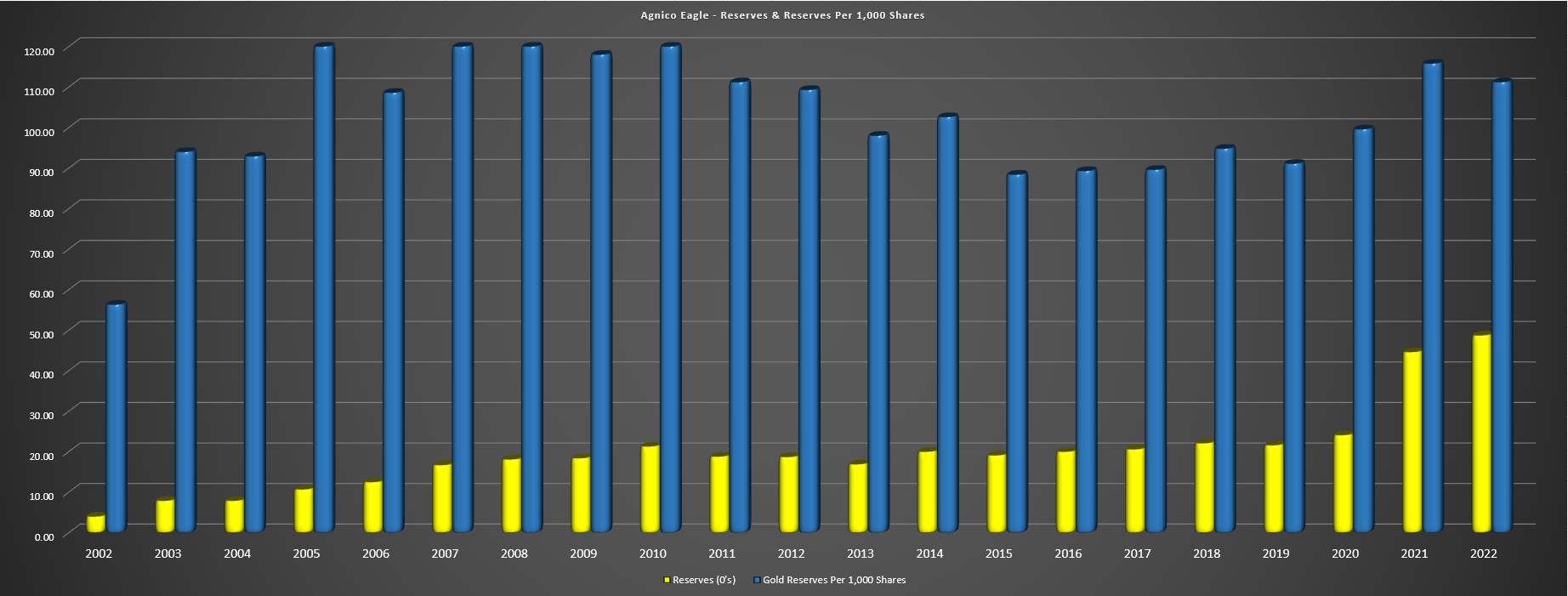

Finally, I'd be remiss not to point out that while there are several growth stories in this sector, there are few growth stories on a per share basis. And as I've highlighted before, reserve growth is important, but far more important is reserve growth per share . This is because reserve growth that comes at the expense of significant share dilution means that investors are getting exposure to fewer ounces of gold per share held and the result is one is actually seeing their exposure to precious metals diluted by owning a given producer. The result? An investor is not getting their desired leverage to the gold price if reserves and or production per share are declining. Obviously, this isn't ideal, since it makes little sense to own a more volatile and riskier producer of a commodity (vs. the metal itself) if it is not offering the leverage that one should get for taking on this added risk.

Agnico Eagle - Reserves Per Share - Company Filings, Author's Chart

{kind=link}

As the chart above highlights, Agnico Eagle has done a phenomenal job of growing reserves per share, benefiting from success at the drill bit at Zone 20 North and LZ5 at LaRonde, Amaruq at Meadowbank, and several others, in addition to well-timed counter-cyclical M&A (Meliadine, Kittila, Meadowbank, Pinos Altos, Canadian Malartic 50%) at a discount to fair value. And it's important to note that the above chart doesn't do Agnico Eagle given that it's sitting on a 15+ million ounce resource at Odyssey that the company is working to convert into reserves. In addition, it does not include Wasamac, a ~1.9 million ounce reserve base at grades above its average reserve grade. Finally, while Hope Bay carries ~3.4 million ounces of reserves in inventory, this figure looks set to grow as well, given continued exploration success. Hence, I expect this trend of reserve growth, production and dividend growth to continue, and investors can take solace that the busy M&A period is likely over after key pieces were added to the portfolio over the past 2 years.

Summary

Agnico Eagle continues to be the premier pick in the gold producer space for investors looking for a sleep-well-at-night miner that can continue to grow, and while Franco-Nevada ( FNV ) is certainly another option, investors have to pay a steep multiple in the latter case given the stock's outperformance over the past decade. For this reason, I see AEM as the far more attractive option, trading at a ~40% discount to its 10-year average cash flow multiple vs. an 8% discount for FNV. And while FNV may look at bolt-on M&A to keep pace with its peers from a growth standpoint because of how difficult it is to grow from its current size, Agnico Eagle's period of M&A that has weighed on the share price is in the rearview mirror. Therefore, I see AEM as the best way to get exposure to the gold price currently, especially for risk-averse investors, and I see this pullback below $44.00 as a gift.

For further details see:

Agnico Eagle: Too Cheap To Ignore