API - Agora: Path To Profitability Remains Challenging

2023-03-20 12:42:49 ET

Summary

- Although long-term trends in the CPaaS market are encouraging, the market is highly competitive, and Agora faces risks from operating in the Chinese market.

- The company's accelerated share buyback execution could offer some protection against downsides before it expires in 2024.

- With API’s major clients tightly controlling costs and a challenging demand environment, I expect limited chances of upward re-rating of the company’s multiple in the near term.

- The stock is trading at a deeply discounted multiple, but I remain on the sidelines for now.

Thesis

There is limited visibility into the path to profitability for Agora, Inc. (API) with the uncertainty surrounding its business continuing. The company faces the prospects of negative revenue growth in 2023, and with no major catalysts expected in the next few months until the company's next results, the key factors to watch will be the macro developments and company's buyback activity. Although I remain positive on the prospects of CPaaS industry and API's leading technology capabilities, I remain on the sidelines for now until macro headwinds subside.

Post Q4 Outlook

Agora's fourth quarter results were largely in-line with slow revenue growth and reduced losses due to optimization of headcount. The company is still struggling to identify new revenue sources, but the market may give it some recognition if it meets its commitment to achieving non-GAAP breakeven by the end of 2023. Due to limited visibility into Agora's long-term growth outlook and normalized margin, it is challenging to determine its stock valuation. However, the company's accelerated share buyback execution could offer some protection against downsides before it expires in 2024.

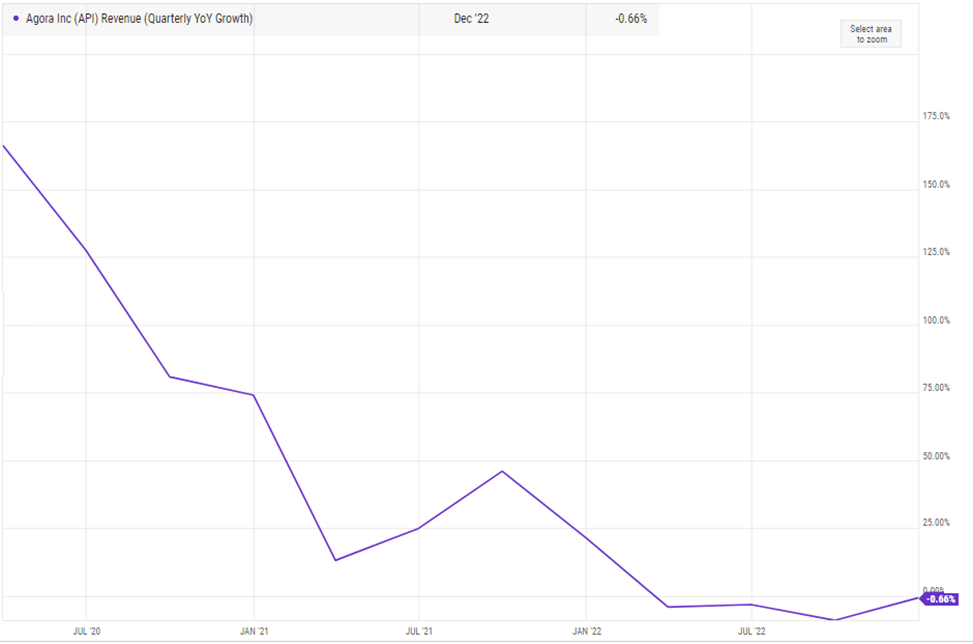

Struggling With A Weak Demand Environment

Agora is facing two main challenges when it comes to demand. Firstly, their larger clients are tightly controlling costs and are reducing their consumption volume while also pushing for lower fee rates. This has resulted in strict cost control measures being implemented by these clients. Secondly, start-ups, who are struggling to raise funds, are not generating much demand either. As a result, I expect negative revenue growth in the near-term due to slow demand and the sale of Easemob's customer engagement business. This particular business segment has accounted for a low-to-mid single-digit of Agora's total revenue in the past two years. The combination of these factors has created a challenging environment for Agora to operate in, and it remains to be seen how the company will address these issues going forward.

{kind=link}

Management Focused On Cost Reduction But Path To Profitability Remains Challenging

Agora has taken aggressive cost control measures since the third quarter of 2022, resulting in a significant reduction in total headcount from approximately 1,300 in 2021 to around 1,000 presently. This optimization could reduce approximately 20% of total operating expenses in 2023. However, the increasing macroeconomic challenges are negatively affecting client demand both domestically and overseas, overshadowing the growth outlook for Agora in 2023.

Long-Term Trends Remain Encouraging

Agora delivers industry-leading performance in terms of latency and communication quality. The use of real-time video and voice for online interactions has become increasingly popular, especially due to the pandemic, and is utilized for social, educational, entertainment, gaming, and enterprise purposes. To incorporate real-time engagement features into their applications, developers are turning to third-party platforms that offer such infrastructure services, as it is difficult and expensive to build these features on their own. IDC forecasts the worldwide CPaaS (Communication PaaS) market to grow from $5.9 billion in 2020 to $21.7 billion in 2025.

Valuation

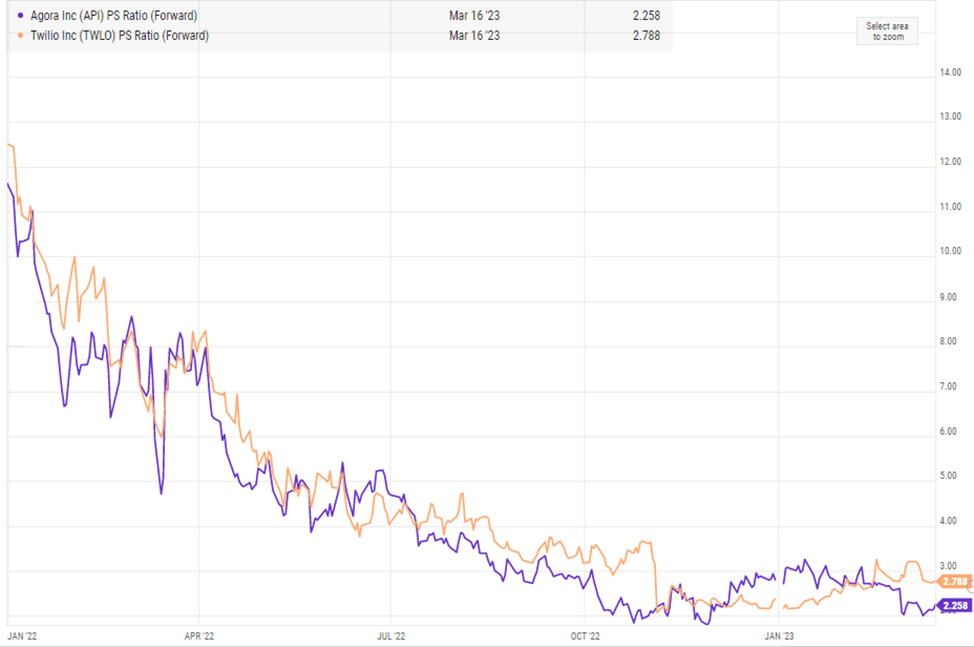

Agora operates in a niche segment of the CPaaS space, which is highly competitive, with Twilio being the dominant player in terms of revenue. Other vendors, such as Vonage and Daily.co, also competes in this market, which has seen a consistent influx of new entrants due to its strong growth potential. I believe it's appropriate to apply a lower multiple to Agora compared to Twilio; considering Agora's smaller business size and the complexity of operating in the Chinese market, applying a discount to Agora would be appropriate. The stock is currently trading at a deep discount to its historical average; however, that is true for most stocks in the industry. I currently don't have a price target on the stock and will remain on the sidelines until the macro-headwinds start to subside.

{kind=link}

Final Thoughts

Agora's Q4 results were affected by macro headwinds as demand slowed down, resulting in negative revenue growth. With the company's major clients tightly controlling costs and a challenging demand environment, I expect limited chances of upward re-rating of the company's multiple in the near term. Agora has focused on cost reduction, but the path to profitability remains unclear as of yet. Although long-term trends in the CPaaS market are encouraging, the market is highly competitive, and the company faces risks from operating in the Chinese market. The stock is trading at a deeply discounted multiple, but I remain on the sidelines for now.

For further details see:

Agora: Path To Profitability Remains Challenging