ADC - Agree Realty: 4.4% Monthly Dividends With A Superior Business Model

2023-07-31 09:55:42 ET

Summary

- Agree Realty is a top-tier retail REIT with a well-diversified portfolio of large tenants like Walmart and Dollar General.

- The company's conservative capital structure, strong balance sheet, and focus on ground leases contribute to its growth and stability.

- With a 4.4% dividend yield and promising acquisition pipeline, ADC presents a favorable investment opportunity. Valuation at 16.6x forward FFO reflects its faster growth potential.

Introduction

It's time to talk about a REIT. In this case, a relatively small one with a top-tier portfolio and a healthy balance sheet similar to some of its bigger peers, except that it comes with higher growth rates. That company is Agree Realty ( ADC ) , a company named after Richard Agree, who founded this company in 1971.

Since then, it has become a highly followed name with characteristics that make it a superior retail REIT. It also comes with a well-covered monthly dividend with a yield exceeding 4%.

In this article, we'll dive into these qualities as I'm looking to expand my REIT watchlist.

So, let's get to it!

What Makes Agree Realty To Great

I am a picky investor. Despite covering countless tickers, I only own 22 stocks in my dividend growth portfolio. I prefer to go big into a few names instead of buying so many that I may as well buy 2-3 ETFs instead.

I'm even pickier when it comes to REITs, as I am not yet looking to sacrifice a high (potential) total return to get a higher yield.

However, there are some fantastic REITs on the market. Agree Realty is one of them.

With a market cap of $6 billion, Agree is one of the smallest retail-focused REITs. But that's OK. After all, smaller REITs tend to be in a better position to grow, which could enhance the total return picture.

Over the past ten years, ADC shares have outperformed their much larger peers, Realty Income ( O ) and NNN REIT ( NNN ), by a wide margin. It beat the real estate ETF ( VNQ ) by roughly 100 points. Its performance has been in line with the S&P 500. Please note that I like both O and NNN. I'm not making the case that they need to be sold. They both have their benefits, including slightly higher yields.

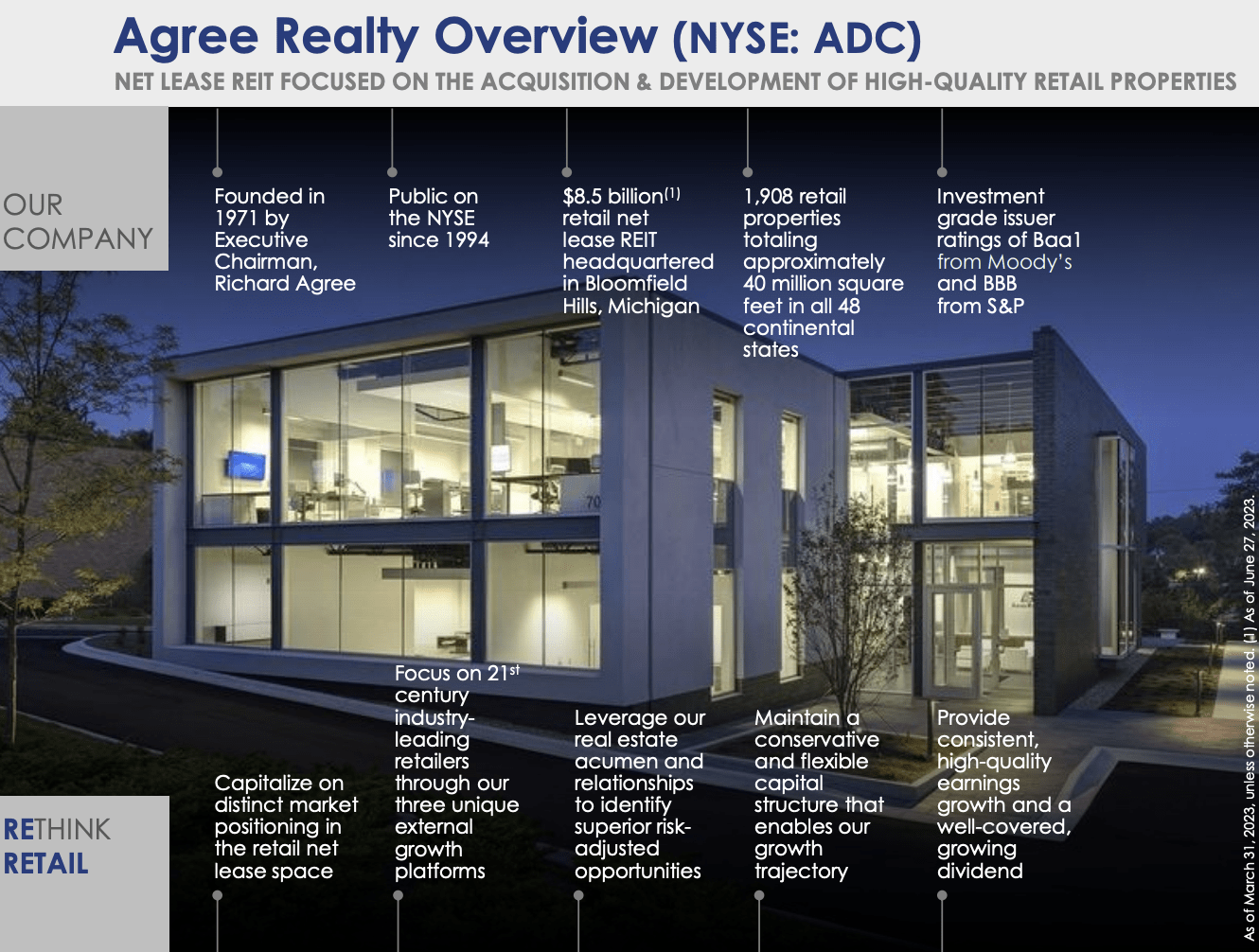

As we can see in the overview below, ADC was founded in 1971. It went public a year before my birth and has turned into a well-diversified triple-net-lease giant focused on maintaining a conservative capital structure that provides both growth and satisfying shareholder distribution growth.

{kind=link}

Agree Realty Corporation

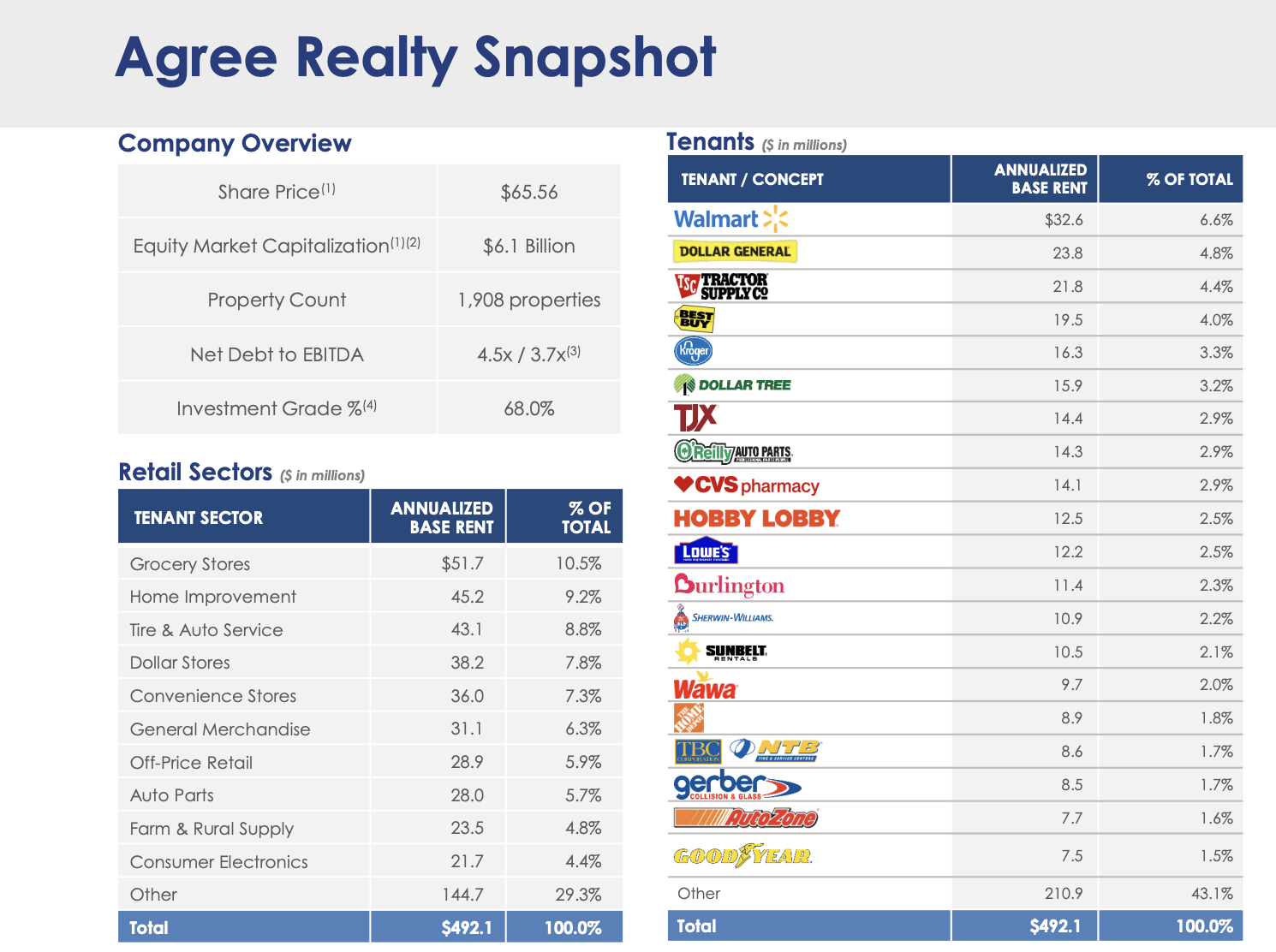

Looking at the company's tenants, we see that it's not messing around. Its top tenants include some of the biggest corporations in the US, like Walmart ( WMT ), Dollar General ( DG ), Tractor Supply ( TSCO ), Best Buy ( BBY ), and Kroger ( KR ).

The total portfolio covers more than 1,900 properties.

While having large tenants comes with the risks related to somewhat subdued pricing power, I think it's worth it, as I do not want to own a company that is exposed to the risks faced by smaller retail stores. As much as I love smaller (often family-owned) stores, they cannot compete with the big guys, and their competitive advantage isn't getting any better.

{kind=link}

Agree Realty Corporation

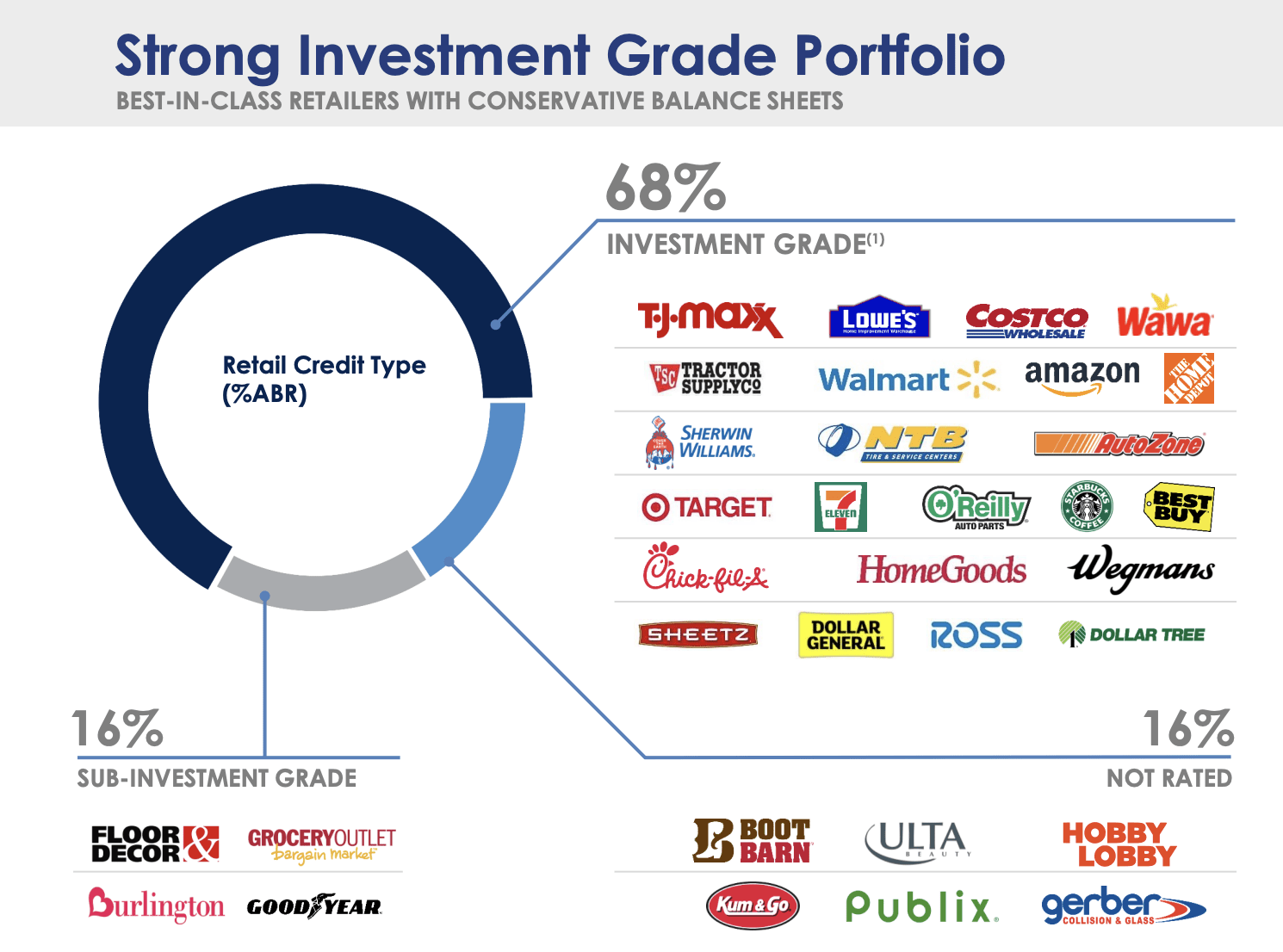

Not only is a big part of the company's tenant portfolio anti-cyclical or semi-cyclical, but 68% of the company's rent comes from investment-grade companies. 16% of its tenants are sub-investment grade. While this comes with higher risks, the companies that are in this category are not likely to fail anytime soon. Meaning it will take a lot for these companies to go under, let alone all of them at the same time.

16% of its tenants are not rated. This includes private companies like Publix, which can withstand even the most severe recessions.

{kind=link}

Agree Realty Corporation

At the end of the first quarter, 99.7% of the portfolio was leased, with a weighted average remaining lease term of roughly 8.8 years.

The company also very successfully engages in ground leases .

A ground lease is an agreement in which a tenant is permitted to develop a piece of property during the lease period , after which the land and all improvements are turned over to the property owner.

A ground lease indicates that improvements will be owned by the property owner unless an exception is created and stipulates that all relevant taxes incurred during the lease period will be paid by the tenant. Because a ground lease allows the landlord to assume all improvements once the lease term expires, the landlord may sell the property at a higher rate . Ground leases are also often called land leases, as landlords lease out the land only.

This is what Joey Agree said during the 1Q23 earnings call when asked if he could elaborate a bit on ground leases:

[...] I think people are becoming generally speaking, more aware of the embedded value in the ground lease space . We were very fortunate to take advantage of it for a while, but we continue to find those select opportunities, whether they be blended extends, but a really interesting one in California this quarter with a former seller, but we'll continue to source those opportunities.

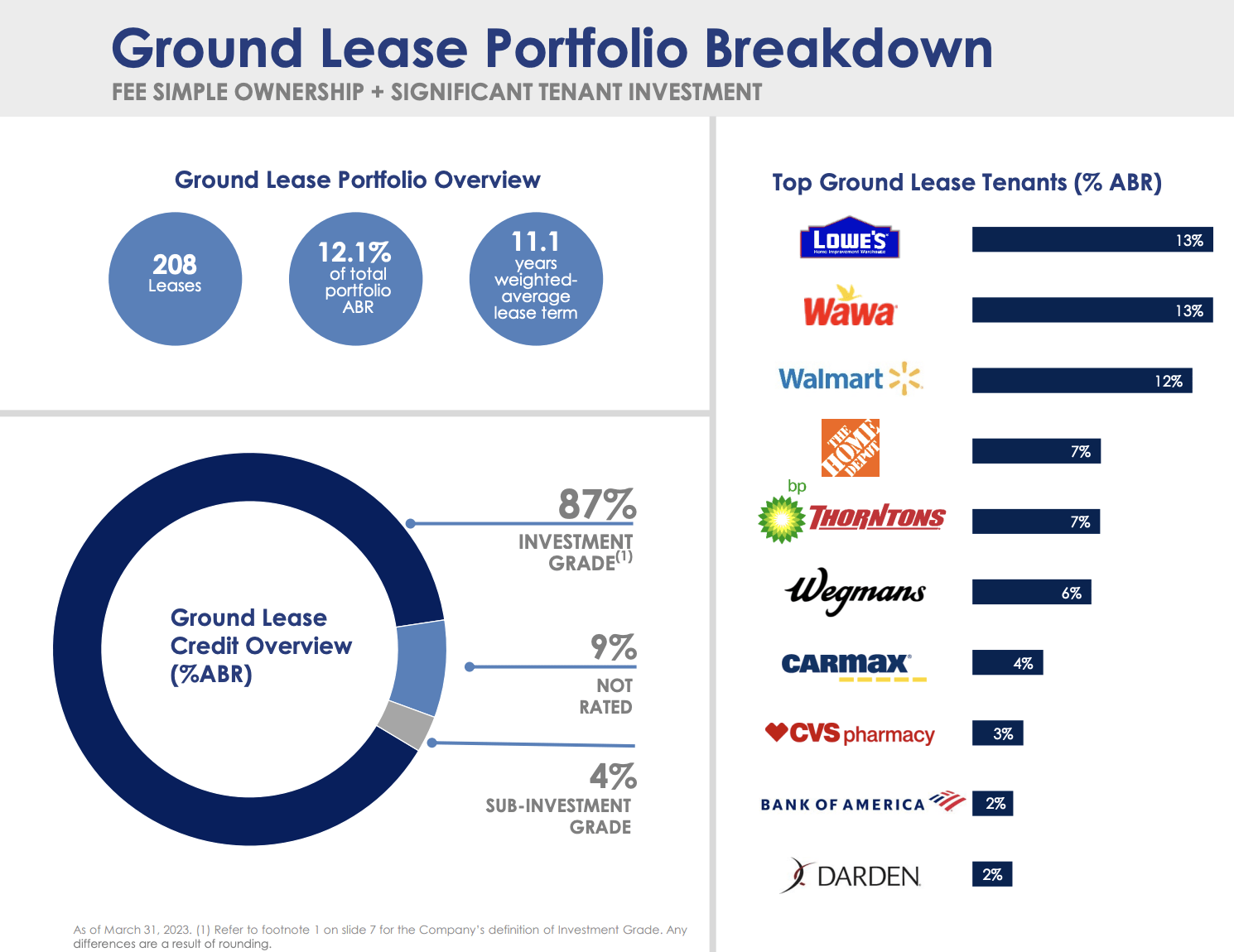

As of 1Q23, the company had 208 ground leases, consisting of 12.1% of its average base rent with an 11.1 average weighted lease term. 87% of ground lease tenants are investment-grade tenants.

{kind=link}

Agree Realty Corporation

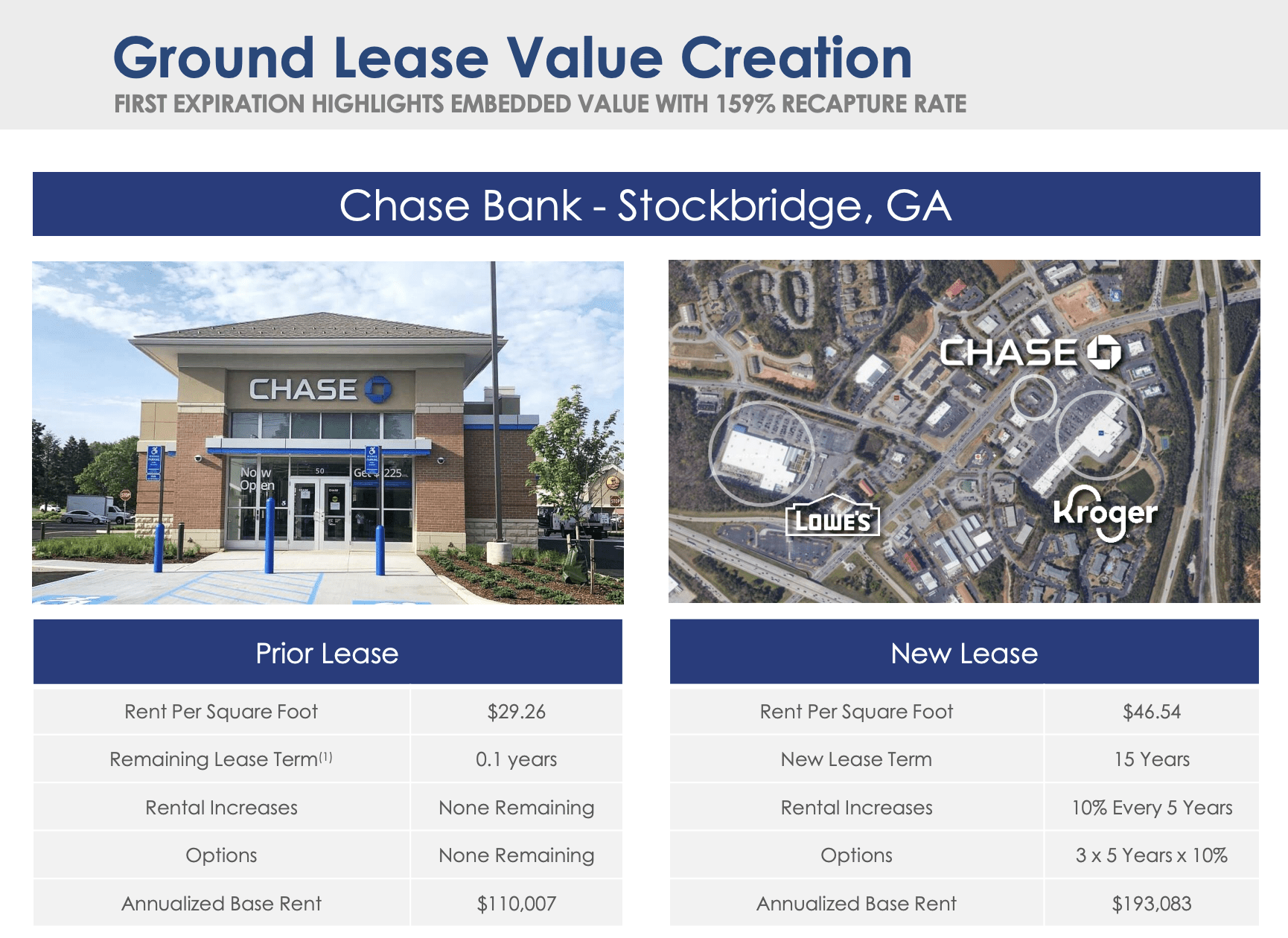

In its most recent investor presentation, the company elaborated on its success in adding value through new ground leased. For example, in Stockbridge, California, the company has engaged in a new 15-year ground lease, boosting rent per SF to $46.54. Even better, the new deal comes with a 10% rent increase every five years, which is roughly 2.1% per year.

{kind=link}

Agree Realty Corporation

On a side note, these deals show that companies like Agree Realty are better off in low-rate/inflation environments, as it allows them to maintain a balance sheet with lower interest costs and benefit more from gross rent hikes.

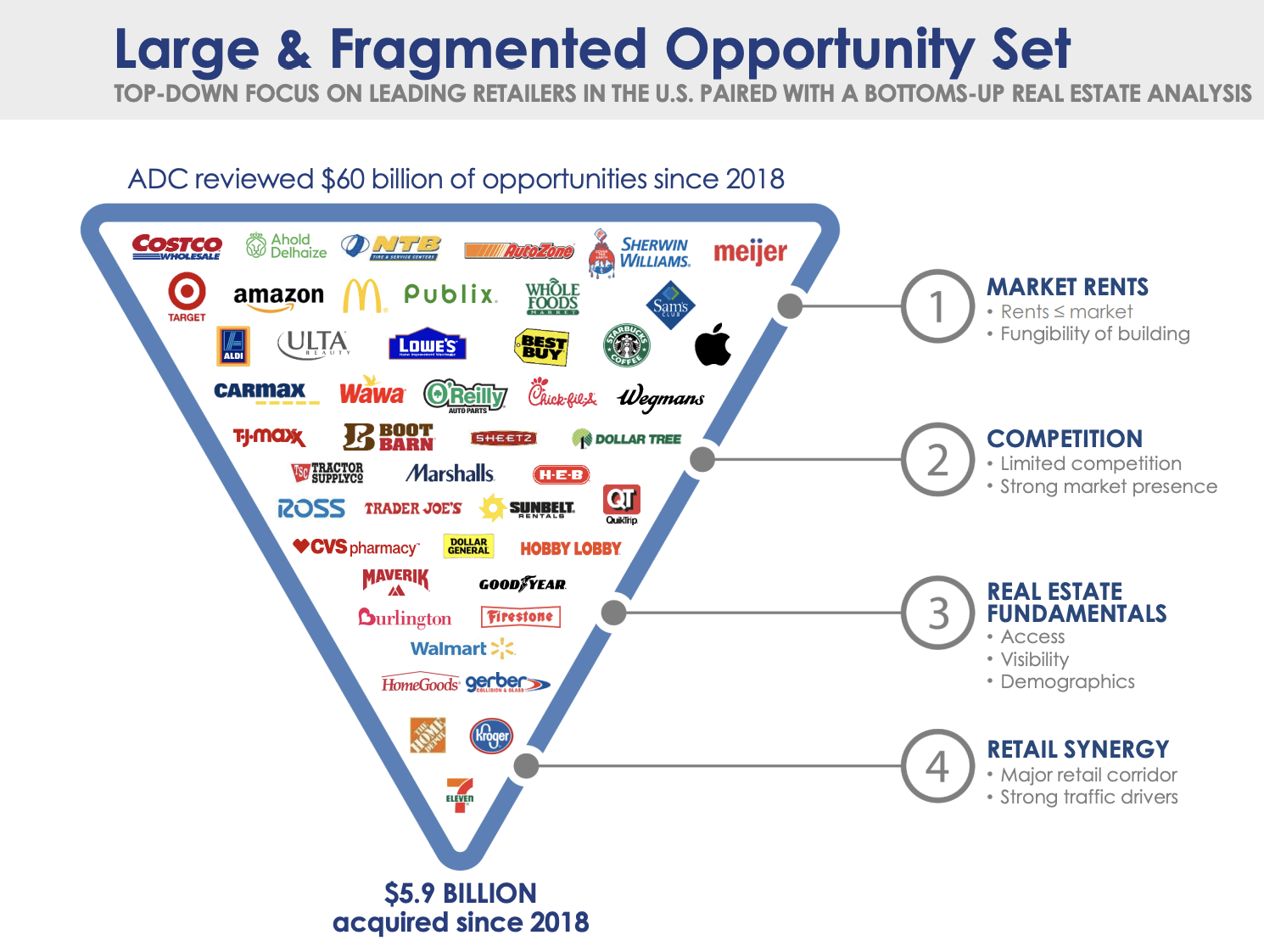

Having said all of this, ADC is very picky when it comes to investing in growth. Since 2018, the company has reviewed $60 billion in potential deals, resulting in $5.9 billion in acquired growth.

{kind=link}

Agree Realty Corporation

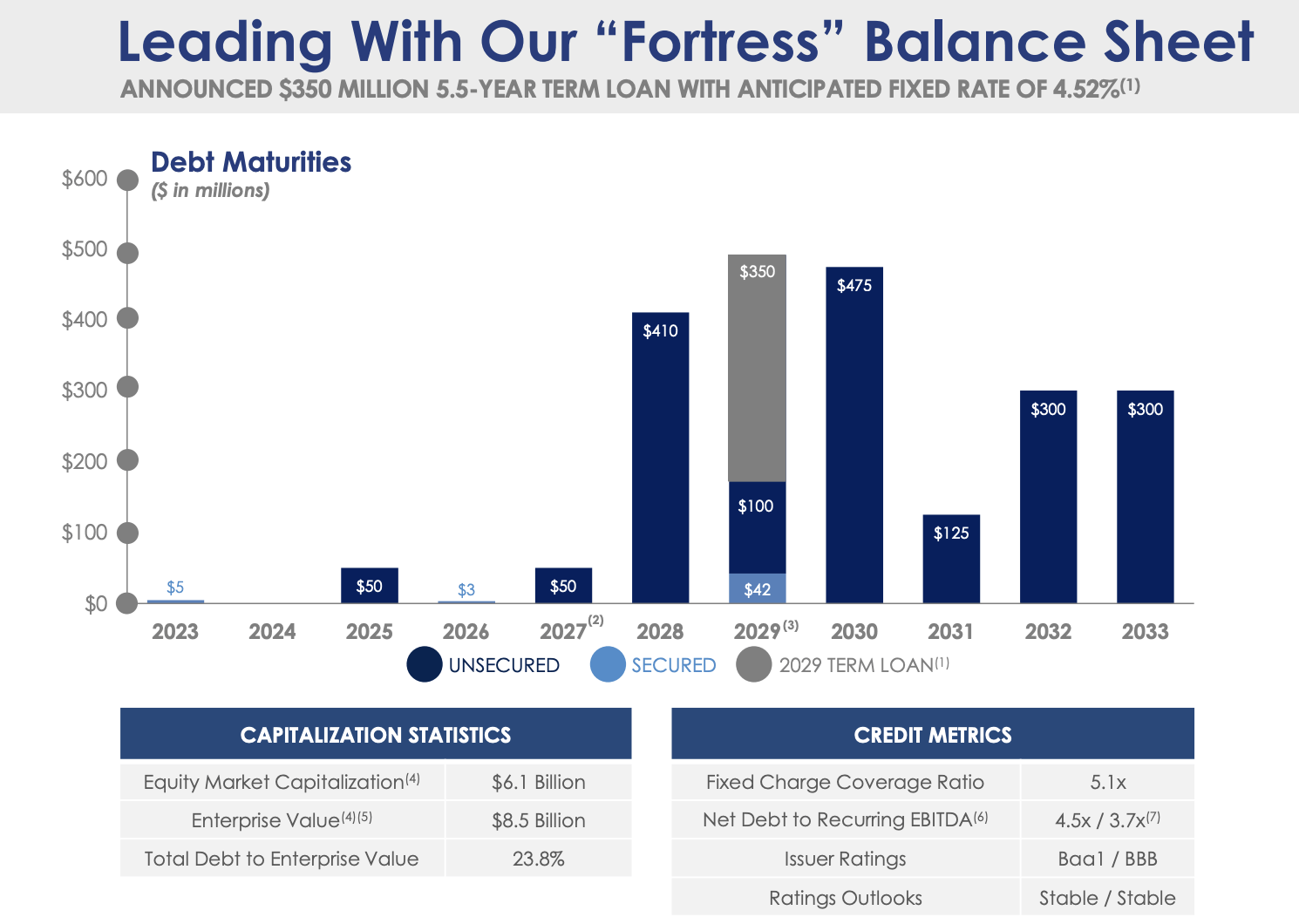

Before I continue to talk about growth, it needs to be said that ADC has a top-tier balance sheet. The company has a net leverage ratio of 4.5x EBITDA, which is one of the lowest numbers I've encountered in a very long time (in the REIT space).

Furthermore, this net debt ratio is 3.7x EBITDA when adjusted for forward equity offerings. Essentially, the company is lowering net financial debt by diluting the shareholder.

The Company occasionally sells shares of common stock through forward sale agreements to enable the Company to set the price of such shares upon pricing the offering (subject to certain adjustments) while delaying the issuance of such shares and the receipt of the net proceeds by the Company.

So far, shareholder dilution hasn't stopped the stock from outperforming, as proceeds are invested in value-adding projects.

Having said that, the company has a 5.1x fixed-charge coverage ratio and a BBB credit rating.

Also, the company has no meaningful maturities until 2028, which is a huge blessing in this elevated-rate environment.

{kind=link}

Agree Realty Corporation

Based on this context, and going back to the company's growth strategy, during the 1Q23 earnings call, Joey Agree highlighted the lack of competition among both public and private buyers, which has provided ADC with increased access to attractive risk-adjusted opportunities. In other words, while elevated rates aren't great for REITs, they do benefit financially stable companies that can outbid competitors with less favorable access to funding.

According to the company, its pipeline shows promising signs with narrowing bid-ask spreads and seller fatigue. The company has been able to quickly close attractive propositions with a dynamic pipeline featuring various future opportunities.

At the end of April alone, the company executed letters of intent to acquire over $100 million worth of high-quality assets at attractive cap rates.

In 1Q23, ADC's acquisition volume for the year has been raised from at least $1 billion to at least $1.2 billion due to increased visibility into the pipeline.

The weighted average cap rate for the acquisitions was 6.7%, which is a 30 basis point expansion relative to the fourth quarter of 2022 and 50 basis points higher than the full year of 2022.

Furthermore, a significant portion of these acquisitions (75%) are leased to investment-grade retailers, with a weighted average lease term of over 13 years, which is impressive and marking a 5-year high.

The ADC Dividend

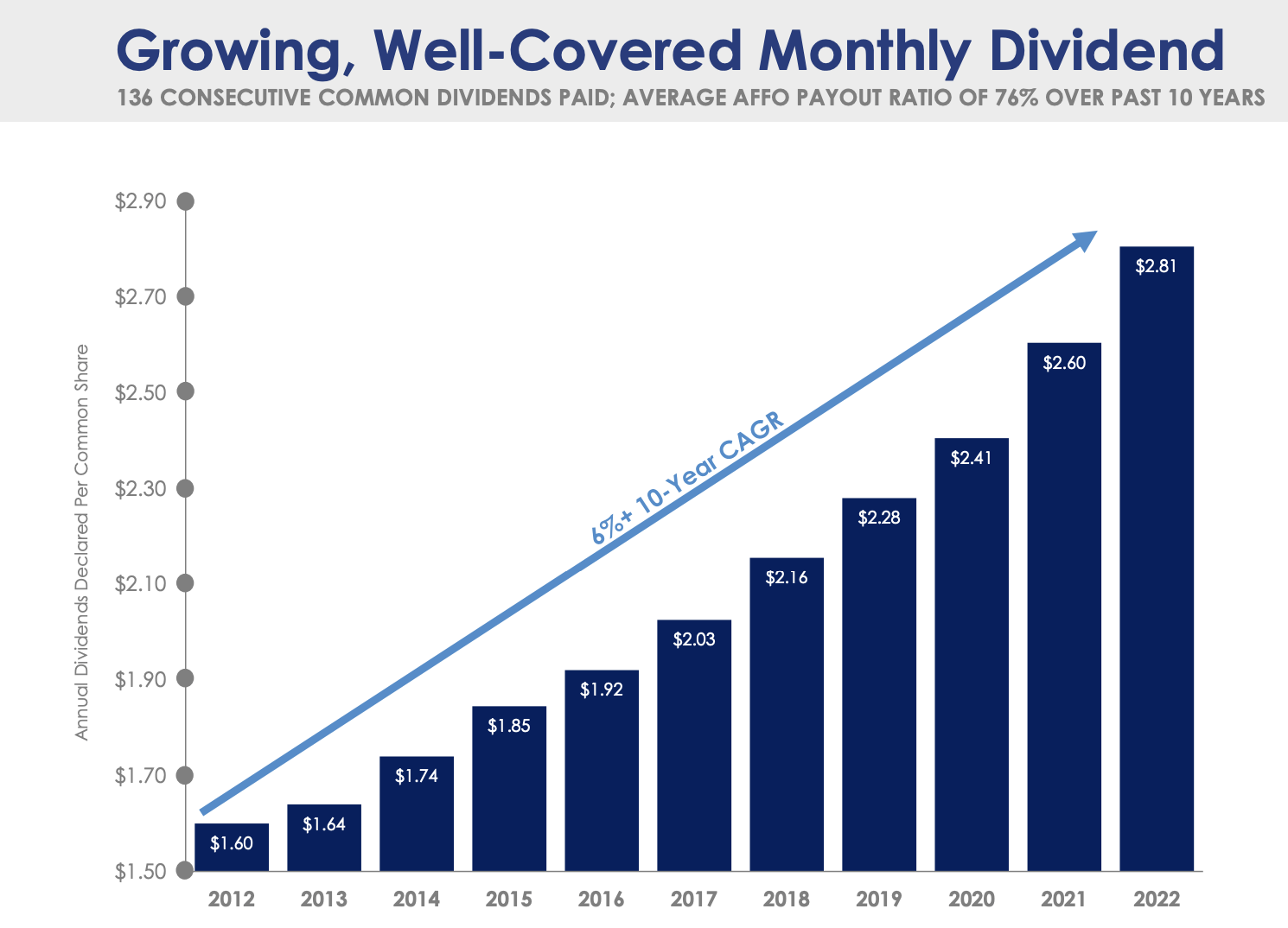

ADC pays a $0.243 per share monthly dividend. This translates to a 4.4% yield.

The company has never cut its dividend and hiked its dividend by 6% per year over the past ten years.

{kind=link}

Agree Realty Corporation

The dividend is protected by a 74% payout ratio.

Valuation

Agree Realty is trading at 16.6x forward funds from operations. The sector median is 13.0x.

This premium is warranted because Agree is growing faster.

- Over the past five years, it has grown its adjusted funds from operations by 7.2% per year, beating the sector median by more than 530 basis points per year.

Furthermore, this valuation is close to the longer-term median.

The current consensus price target is $76, which is 15% above the current price.

I agree with the consensus price target.

However, I cannot make the case that ADC is a must-buy at these levels. The stock has lost momentum again, as it seems that interest rates may remain elevated longer than expected, which has been my thesis for a while.

Rising oil (and gasoline) prices aren't helping either.

Hence, I believe that ADC is a great buy at $60.

Waiting for $60 comes with the risk of not buying it because the stock might take off. However, given the risk tolerance of most portfolios that I advise, that's a risk I'm willing to take.

My rating is bullish to reflect the valuation and long-term potential of this stock.

Takeaway

Agree Realty is a top-tier retail REIT that offers investors an attractive combination of growth potential and stable income.

With a well-diversified portfolio of high-quality tenants, including major corporations like Walmart, Dollar General, and Best Buy, the company is positioned for long-term success with subdued risks.

Furthermore, ADC's focus on ground leases and its careful approach to growth has resulted in a solid balance sheet and a track record of outperformance compared to larger peers in the REIT space, which I expect to continue.

For further details see:

Agree Realty: 4.4% Monthly Dividends With A Superior Business Model