NNN - Agree Realty And NNN REIT Q3: Solid Earnings Shows Why Both SWANs Are Great Buys Right Now

2023-11-06 11:00:00 ET

Summary

- NNN REIT beat analysts' estimates on FFO and raised guidance, showing resilience in the current macro environment.

- NNN has fallen nearly 9% in the past year but recently experienced a price jump after the FED meeting.

- Agree Realty also beat estimates and raised acquisition guidance, with a strong portfolio and attractive growth prospects.

- I suspect REIT prices will begin to rebound as we are getting closer to the end of the rate hike cycle.

- With recession talks all but dead, I expect high-quality REITs like Agree Realty and NNN REIT to continue posting strong growth in the coming quarters.

Introduction

It's no secret that over the past year, REITs have been beaten up, or should I say beaten down. Many are trading near pandemic prices and now offer dividend investors great bargains, and some nice upside if you plan on holding for the long term. I mean why invest if you don't plan on holding for at least a few years? I know everyone is different but when I purchase shares of a company, I purchase them with a plan to hold forever, unless something fundamentally changes or a better investment is available. The reason is I try to pick high-quality stocks, not just ones that offer high yields.

I don't knock those who only look for high-yielders, but I try not to focus on yield, but instead on quality. I can't say that I haven't been there before though. I've definitely chased high yields in the past. But every so often, an opportunity comes along to pick up quality stocks at a good price, or on sale like now. In this article, I get into why these two REITs are currently a bargain.

#1 NNN REIT (NNN)

NNN REIT recently reported Q3 earnings and beat analysts' estimates on FFO by $0.01. FFO came in at $0.81, an increase of $0.01 from Q1 & Q2, and $0.02 from Q2 '22. This may not seem like a lot but as I always say, some growth is better than no growth at all, even if it's by a penny or two. Those who know anything about NNN, or REITs for that matter should know that these are generally not fast-growing investments. If you're looking for those, then you should consider other stocks in different sectors.

Considering the current macro environment where many companies are facing headwinds, NNN not only beat estimates but managed to raise guidance as well. Management now expects full-year core FFO per share of $3.19-$3.23, compared to the prior $3.17-$3.22. So, as macroeconomic headwinds continue to challenge businesses, especially REITs, NNN raised guidance. This is a testament to the quality of the company this REIT is, and I expect them to continue to deliver for the foreseeable future.

The REIT did fall short on revenue consensus by $2 million, coming in at $205.1 million, but this is up from Q2 by over 1%. Additionally, they managed to increase revenue by nearly 6% from $193.5 million year-over-year. Again not eye-popping numbers, but for a REIT right now, those are solid. Like we say in the military: Slow is smooth, smooth is fast.

As you can see below, NNN has fallen nearly 9% in the last year and was recently trading below $35, where it hit a new 52-week low. NNN was already one of my larger positions but I couldn't help but take advantage while many investors were rotating into T-bills. Sure, I could get nearly 6% on a safer, fixed-rate investment but I decided to take advantage and lower my cost basis. The REIT traded around $35 for a while before recently jumping to nearly $39 at the time of writing.

One reason for the recent price jump is the FED meeting held on November 1st. Jerome Powell, in my opinion, eased some concerns investors had. For one, they decided to hold rates steady for the second time, something they haven't done since the start of rate hikes last year. This seemed to boost investor sentiment and gave some more hope that we're getting closer to the end of the rate hike cycle. He also addressed concerns of a looming recession, stating one is all but cancelled.

I've stated before that when rates begin to come to a close, and/or cut, REITs & BDCs will reverse in price. Many REITs will begin to rise while some BDCs will fall in price. This is not to say BDCs are not quality investments. But those who know, BDCs thrive in high-interest environments, and when there are cuts, investor sentiment will shift as well. I hold some BDCs and still plan to hold those same ones when rates begin to reverse.

In this chart, you can see NNN last traded around these prices in 2017 & 2018 before trading near $60, right before the pandemic. Again, that was in the low-interest rate environment. Some say that we will never see that again and they could be right. I don't try to predict what the FED will do, but I do think rates will begin to decline sometime next year.

Growing Portfolio

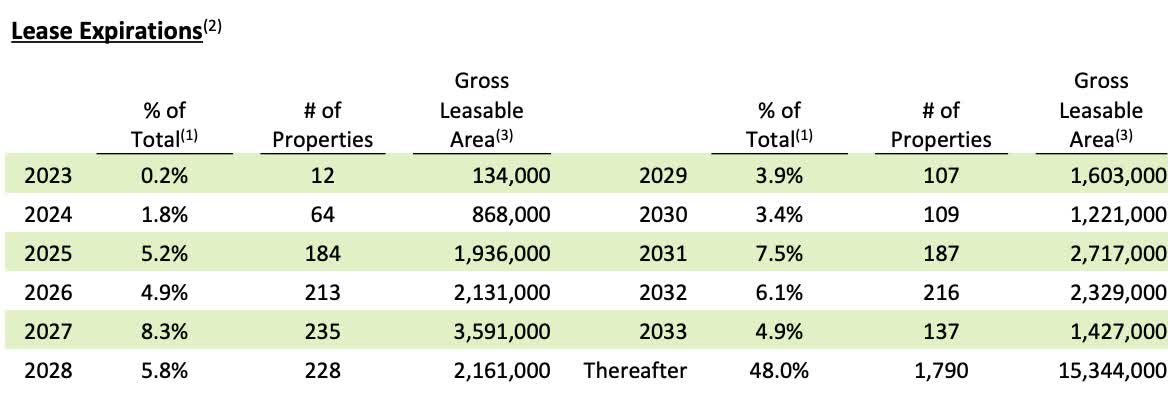

NNN also continued to grow its portfolio during the quarter. The REIT made $212.5 million in property investments, including 46 additional properties for an initial cash cap rate of 7.4%. They also sold 12 properties for $49 million, generating $20 million in capital gains on sales at a 6.0% cap rate. YTD they've sold a total of 26 properties, producing over $40 million in proceeds at a cap rate of 5.8%. At quarter end the portfolio stood at 3,511 properties in 49 states. Furthermore, NNN's portfolio was 99.2% occupied and had no sizable lease expirations until 2025, with 5.25%, or 184 property leases expiring. Even then this isn't a very large amount. NNN's leases have a weighted average lease term of 10.1 years.

{kind=link}

Their dividend track record also speaks for itself. 34 years of dividend increases, what's not to like? This is one you want to hold. One is because it's trading at a bargain right now, and also because according to Morgan Stanley, the market will continue to be volatile in the coming months and dividends could cushion some of the capital losses. They recommended dividend stocks with long track records of consistent dividend growth. Sounds like NNN fits the bill to me. With a forward P/AFFO ratio below its 5-year average and the sector median of 12.65x, NNN is still a strong buy even with the recent price surge.

#2 Agree Realty (ADC)

Agree Realty also recently reported its Q3 earnings at the end of last month and they continue to shine through all the economic uncertainty as well. Despite the higher rates, which means higher costs for borrowing and REIT prices declining to new 52-week lows, Agree Realty stood strong. Like NNN, they also beat analysts' estimates by a penny, with FFO coming in at $1.00 a share. This was an increase of $0.02 from the 1st & 2nd quarters, and a $0.03 year-over-year Revenue of $136.81 million also beating estimates by nearly $2 million, and increased by almost 5.5% from Q2. Year-over-year this increased nearly 25% from $110 million.

Like NNN, they also raised guidance, and acquisition guidance. They now expect this to be at $1.3 billion for the year. Also, the REIT managed to increase its exposure to investment-grade tenants to an all-time high of nearly 69%. They invested nearly double NNN's amount in property count with $411 million in 98 new properties, bringing the portfolio to 2,084 properties in 49 states. So, while some companies have been searching for growth opportunities, ADC has been busy! In Q2 of this year, they managed to pass the 2,000 milestone in properties and continued to acquire additional ones in the 3rd quarter. These properties were acquired at a weighted-average cap rate of 6.9%, slightly below NNN's 7.4%. Occupancy stood at 99.7% at the end of the quarter, one of the highest ratings in the entire sector, and slightly above NNN's 99.2%

One thing that makes ADC my absolute favorite REIT are the ground leases. During the quarter they acquired an additional 7 ground leases bringing their total to 217. So, as you can see this REIT is one of the best, if not the best in the sector. And investors should take advantage of the share price decline.

As you can see ADC's price has declined like NNN as well, offering a great bargain right now. And like I previously mentioned, I think the sentiment will start to shift soon, especially with the FED calling the recession all but cancelled. Like NNN, ADC's price was trading around $54-$55 dollars before getting a recent boost. It also hit a new 52-week low of $52.69, but has since rebounded to above $58 where it trades at the time of writing.

In 2017-2020 right before the pandemic ADC was trending upwards and to the right like NNN right before the pandemic as well. Right now the REIT is trading well below its 5-year forward P/AFFO ratio of almost 20x, so investors are getting a massive bargain if you ask me.

Furthermore, ADC expects to deliver 3% AFFO growth over the next year. This accounts for a conservative credit loss amount, inflationary growth in G&A over 5%, and any outstanding borrowings on the revolver. No acquisitions, no new capital, or anything. With a 5% yield and expected 3% AFFO growth, investors get 8% growth to sit and do nothing. You can't ask for much better than that. Besides maybe the 2.9% dividend increase that the company rewarded shareholders with for the second time this year. ADC doesn't sport the dividend track record like its peer NNN, but 11 years of uninterrupted increases are not too shabby either.

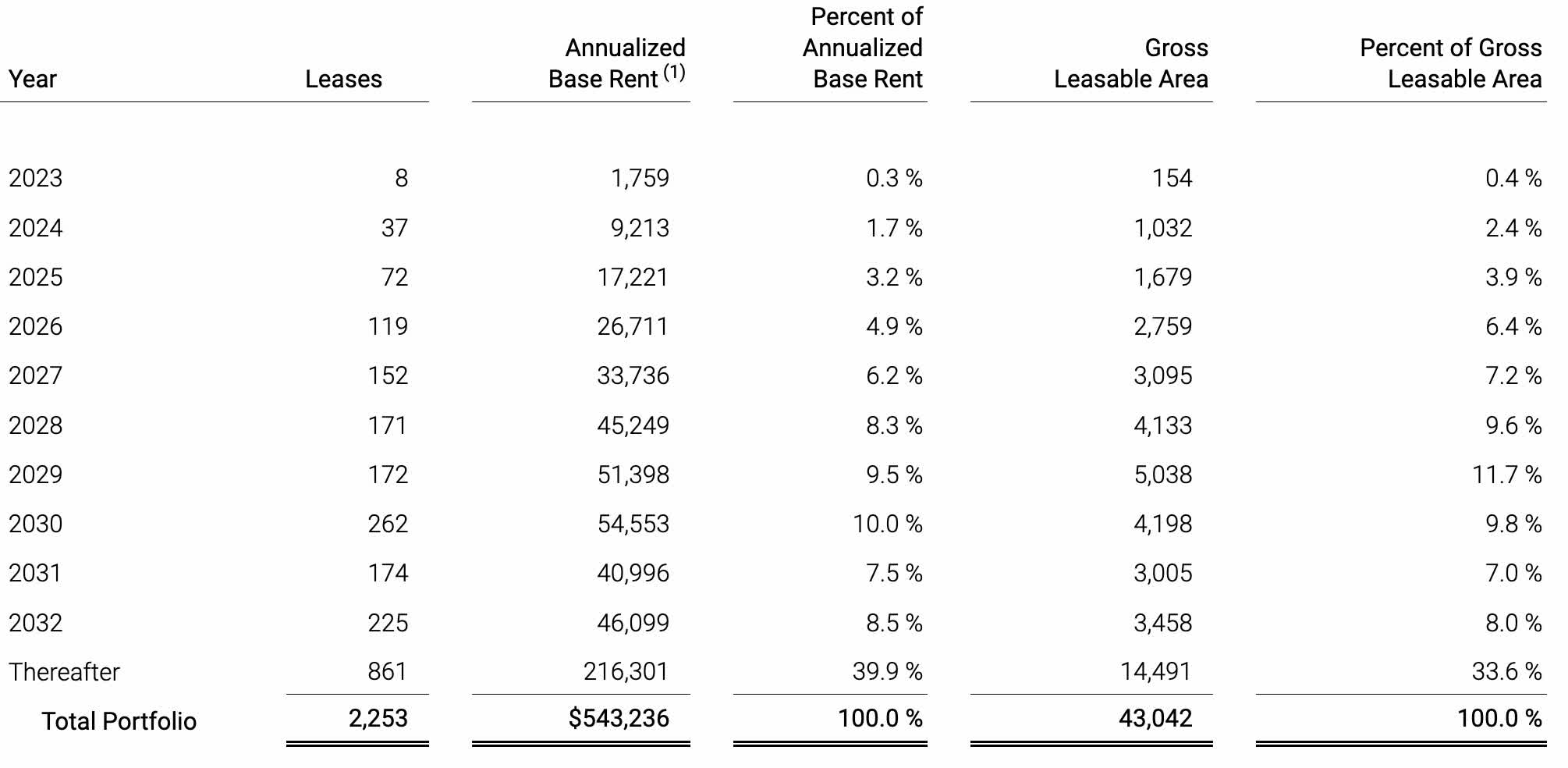

Additionally, they have only eight leases that are expiring through the rest of the year. As you can see, ADC lease expirations are also well-structured like its peer NNN with only a small amount maturing in the next few years. Another thing to note is the company received an upgrade to its rating of B to BBB from MSCI, a leader in ESG indices. This was driven by improvements in the company's governance and business ethics & practices. Of course, this wasn't an upgrade in their credit rating, but it still shows the company is a solid business.

{kind=link}

Risks To Consider

Although the recent FED meeting seemed to boost investor's confidence, we are not out of the woods yet, especially for REITs. Inflation is still an ongoing battle for the economy and they did leave the door open for more rate hikes down the line. If rates continue to climb, this will make it harder for REITs as the costs remain elevated. Furthermore, this will make it harder for them to grow externally. Another risk to NNN specifically is the company has $350 million worth of debt due next year that they will likely have to refinance at a higher rate.

ADC's fortress balance sheet is the best in the sector in my opinion. They have no significant amount of debt maturing until 2028. REITs also face the risk of lower occupancy in the current macro environment. As tenants become stressed, REITs could have to deal with lower occupancies, which will in turn affect rental revenues. That's why tenant concentration and credit ratings are important. A big difference between NNN & ADC is that ADC focuses on IG tenants while NNN does not. Both have their pros and cons. But for the first time in four consecutive quarters, NNN witnessed its occupancy rating drop slightly from the 2nd quarter's rating of 99.4%. This is still above their historical average of 98.2%. They also managed to grow properties from 3,449 to 3,511 in the same period.

Conclusion

Agree Realty & NNN REIT are two of the best REITs in the sector, and both have been unfairly punished related to negative sentiment in the market with the rapid rise in interest rates. As I suspect we are closer to the end of the rate hike cycle, with the FED essentially declaring recession talks basically dead, I foresee REIT prices will begin to surge, starting with these two. Even in the challenging environment 2023 has presented for the sector, both REITS have continued to thrive, increasing FFO & revenues while growing their portfolios at attractive spreads. They also have well-laddered debt maturities making them less susceptible to the higher for longer environment. As the FED continues to monitor inflation, at the first sign of a rate cut, these two REITs will offer some nice capital appreciation as they both trade well below the P/AFFO ratios.

For further details see:

Agree Realty And NNN REIT Q3: Solid Earnings Shows Why Both SWANs Are Great Buys Right Now