ADC - Agree Realty: Safety And Income For Your Portfolio

2023-05-15 20:51:16 ET

Summary

- ADC is amongst the safest net lease REITs out there and enjoys a number of competitive advantages.

- Between a high percentage of investment grade tenants, a unique ground lease strategy and a fortress balance sheet, this company offers the stability every portfolio needs.

- At the same time, the stock has a solid growing dividend and is trading at a reasonable level at which it has only traded a couple of times in history.

Dear readers/followers,

My bullish stance towards net lease REITs is well documented here on Seeking Alpha as I've covered a number of them including Realty Income ( O ), Essential Properties Trust ( EPRT ), NNN REIT ( NNN ), EPR Properties ( EPR ) and Broadstone Net Lease ( BNL ). Today I want to cover one of the safest and arguably best positioned REITs for a potential economic slowdown - Agree Realty Corporation ( ADC ).

Why Agree Realty?

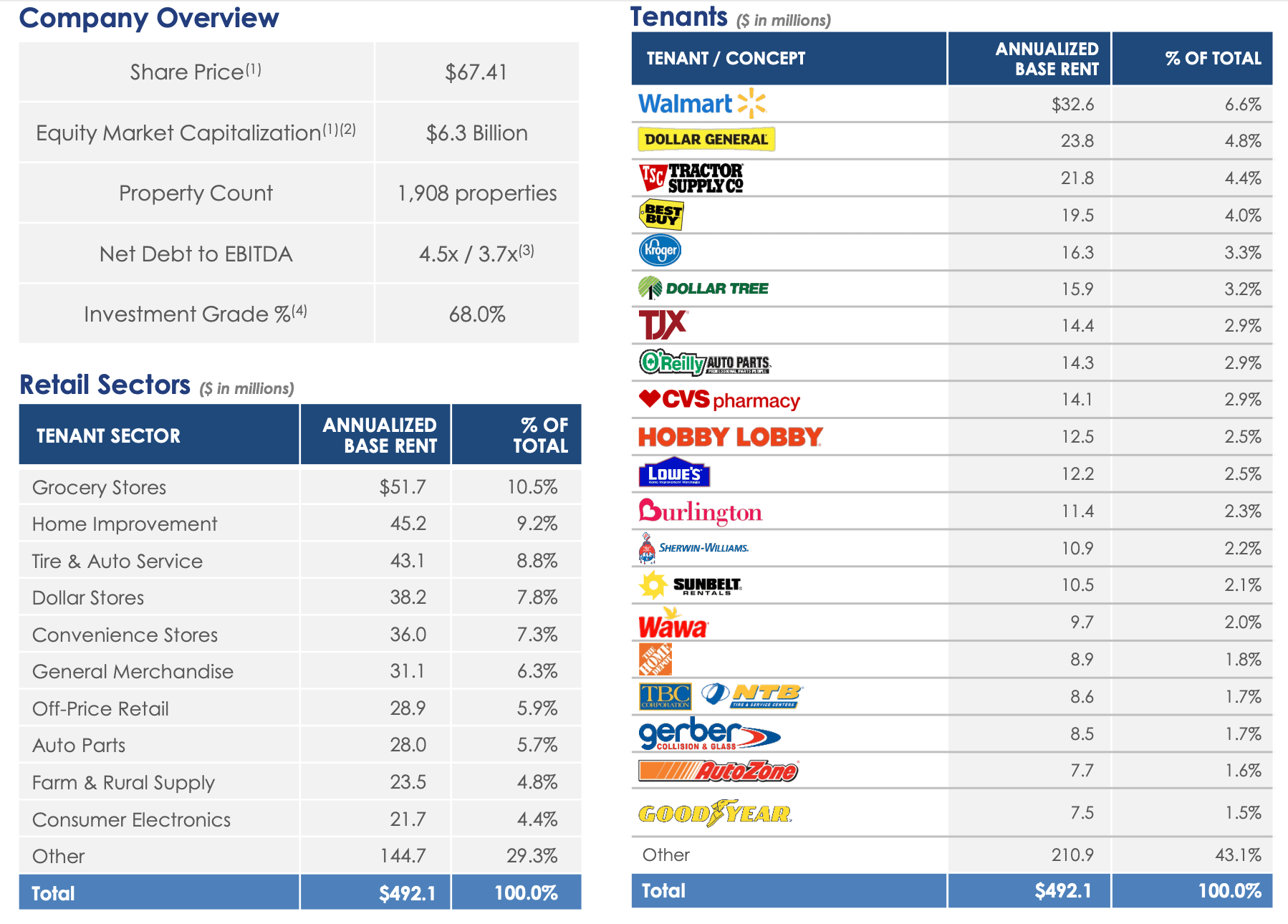

To get started, let's talk about what makes this net lease different. First off, its their tenants . While most of the net lease REITs I've covered to date focus on small single-tenant properties with an average asset size of $2-5 Million (think a fast food restaurant or a car wash), ADC focuses on big box stores of some of the biggest and most well-known retailers, such as Home Depot ( HD ) or Walmart ( WMT ). This means that the company has one of the highest percentages of investment grade tenants out there at 68%. With such strong tenants the likelihood of them not being able to afford rent in minimal.

Not only are their tenants some of the biggest retailers, but they also operate in sectors that are fairly resistant to an economic slowdown as well as e-commerce. In terms of the tenant sector, grocery stores take the lead at 10.5% ABR, followed by home improvement at 9.2% and auto at 8.8%. As you can see the REIT is extremely well diversified in terms of sectors. When looking at individual tenants, Walmart being their largest tenant accounts for 6.6% of ABR and is followed by very well known companies like Dollar General ( DG ), Tractor Supply ( TSCO ) and Best Buy ( BBY ). I like the tenant mix a lot for its safety, so much so that I think that if you were to describe the safest net lease portfolio, this is would be it. A staggering occupancy of 99.7% also helps and it's worth noting that less than 10% of leases expire before 2026.

{kind=link}

ADC actually goes a step further in terms of safety by getting involved in ground leases . This is another major point which really differentiates them from competition. Ground leases are much safer, because the tenant pays for the building that it builds on the land. If he cannot continue to pay rent for the land, the landlord (ADC in this case) keeps the building. This gives tenants an extra incentive to make sure that they honor the lease contract in full. In total about 12% of ABR comes from ground leases and 87% of this from investment grade tenants.

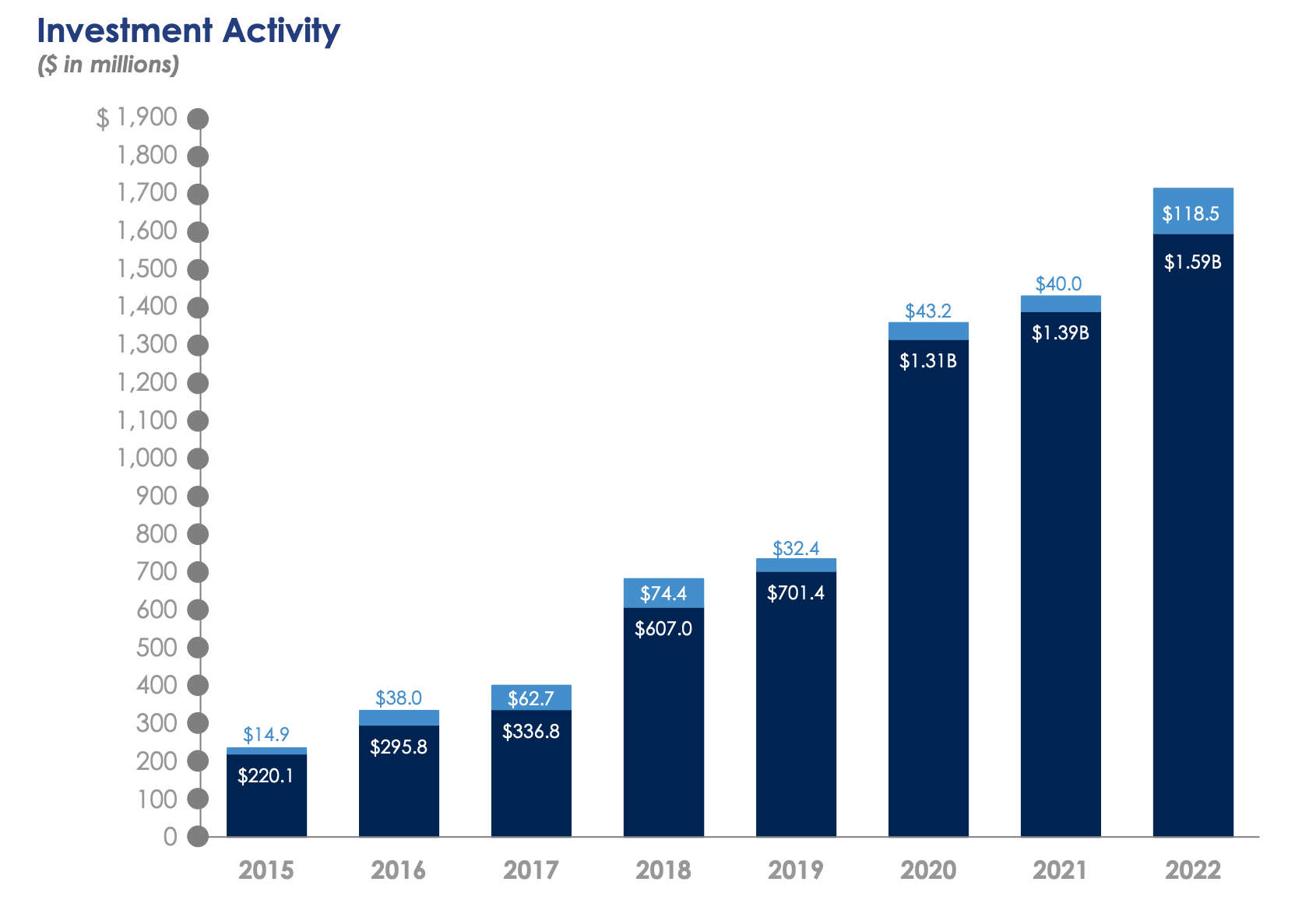

Agree Realty has grown their portfolio primarily by acquisitions, but they do have a small development division. In Q1 2023 they acquired 66 properties and two land plots for ground lease for $320 Million and increased their acquisition guidance for the full year from $1 Billion to $1.2 Billion. Management also noted that they already have an additional $100 Million under LOIs. I like the fact that the company is going shopping now that cap rates have increased a lot, because these will prove to be tremendous purchases in the long term. In particular, their Q1 acquisitions averaged a cap rate of 6.7% on really outstanding lease terms - 75% of tenants investment grade and a 13 year average lease term. In terms of development, 5 new projects were commenced in Q1 while construction continued on 21 projects with an anticipated cost totaling $85 Million.

{kind=link}

Solid same-store performance as well as new acquisitions in Q1 have resulted in a modest 0.6% core FFO increase to $0.98 per share. For the full year, analysts are expecting a 2% YoY increase, followed by 5% in 2023 and 2024. Nothing spectacular, but this is a safety play, not necessarily a growth play.

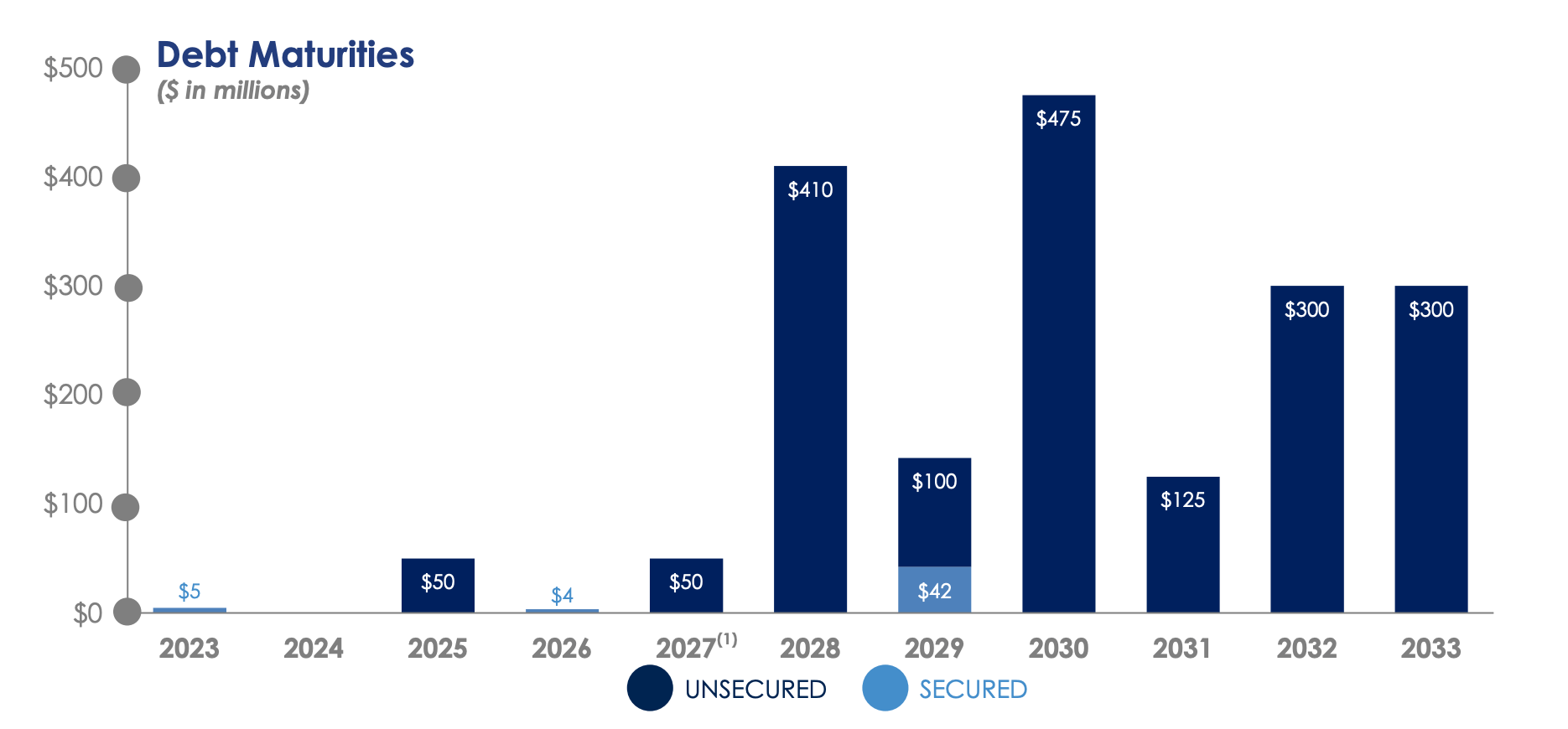

Once again, the safety theme is reflected in their balance sheet as well. They have a BBB rating, a healthy net debt to EBITDA of 4.5x (3.7x including unsettled forward equity) and a great maturity schedule which gives them all the flexibility they need until 2028. In terms of liquidity, they have $1.2 Billion available on their revolver plus outstanding forward equity - enough to hit their acquisition targets. Agree says they have a fortress balance sheet and I agree!

{kind=link}

Before diving into valuation let's look at the dividend which plays a major role for most investors. Management announced a $0.243 per share for April which translates to a yield of 4.4%, slightly below what you can get from other net lease REITs. The payout ratio for the first quarter stood at 73% which was below the low end of the targeted range of 75-85% of AFFO. This leaves ample room to raise the dividend in the future which is something the company has a history of doing (10-year CAGR of 6%). Given the low payout ratio, the dividend can easily increase by 5-6% a year going forward.

So there you have it. A portfolio of some of the strongest tenants in the net lease space, a unique differentiator in a form of ground lease, low lease expirations and a fortress balance sheet with a growing well covered dividend. But can we reasonably expect to beat a broader index and still benefit from this level of safety? Let's see.

Valuation

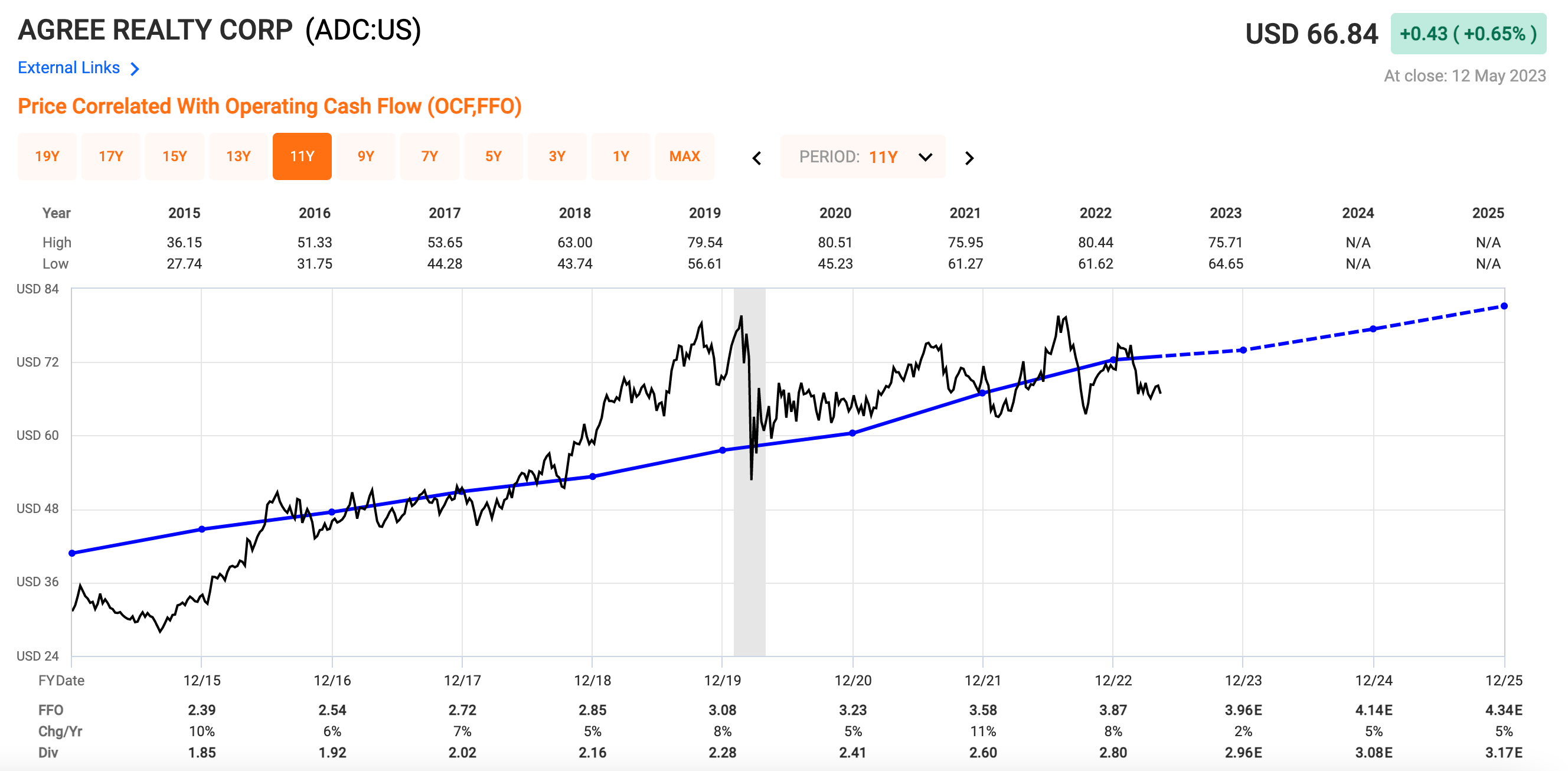

Quality never comes cheap. The stock has largely been range bound since 2019 and now sits near the bottom of the range. With about $126 Million in quarterly revenues the stock currently trades at an AFFO yield of about 6% which is below the cap rate they were able to achieve on their recent acquisitions of 6.7%. However, as most management teams are now saying that they feel that cap rates have more or less peaked, I'm quite happy to buy ADC's portfolio at a 6% yield. That's a 250 bps spread to 10-year treasury yields which I feel more than compensates for the limited risk given their high proportion of investment grade tenants.

Currently ADC trades at 17x FFO which is about as low as it has traded with the exception of several short-lived crashes. The valuation is reasonable and leaves some (though not a lot) of upside from here. In particular, over the medium-term I can see ADC closing part of the gap to its longer term average and reaching an exit multiple of 18.5x, which yields a price target of $80 per share.

{kind=link}

With that, I expect ADC to return:

- 4.4% in dividends (growing at 5% per year)

- 3% on average from FFO growth

- 3% from multiple expansion (if 18.5x FFO is reached within 3 years)

- solid total expected annual return of 10.4%

One shouldn't expect to double their money in a stock like ADC, but every portfolio needs some stability and that's really where ADC shines. I'm a buyer at these prices and rate the company as a " BUY " here at $66.80 per share.

For further details see:

Agree Realty: Safety And Income For Your Portfolio