EPRT - Agree Realty: The Monthly Payer Is Absolutely Cheap But Relatively Expensive

2023-09-14 10:00:00 ET

Summary

- Agree Realty is an investment grade rated REIT with a diverse portfolio of 2,004 properties across the US.

- The company's leases are primarily "net lease" agreements, where tenants are responsible for operating costs.

- The REIT has not performed well over the last year, and we explain why we are still not long.

Agree Realty Corporation ( ADC ) is a investment grade rated REIT. At the end of Q2-2023, it had a portfolio of 2,004 properties, spanning close to 42 million square feet of gross leasable area or GLA. ADC has a presence in almost all of the US states, and its diversification within the retail sphere is impressive.

Investor Presentation

Going further deeper, ADC does not get more than 6.5% in annualized base rent from any single tenant and its top 20 list has several familiar names, Walmart Inc. ( WMT ), Best Buy Co., Inc ( BBY ) and CVS Health Corporation ( CVS ).

Investor Presentation

Almost all of its leases are of the "net lease" kind. That is, besides the rent, the tenant is also responsible for the operating costs of the property they occupy, such as repairs and maintenance, property taxes, insurance, trash removal, etc. In essence, only the major capital expenditures fall in ADC's lap. Besides this, ADC also has contractually built in rent escalators tied to CPI or fixed amounts. At times, there are additional increases written into the agreements, that are based on gross sales levels.

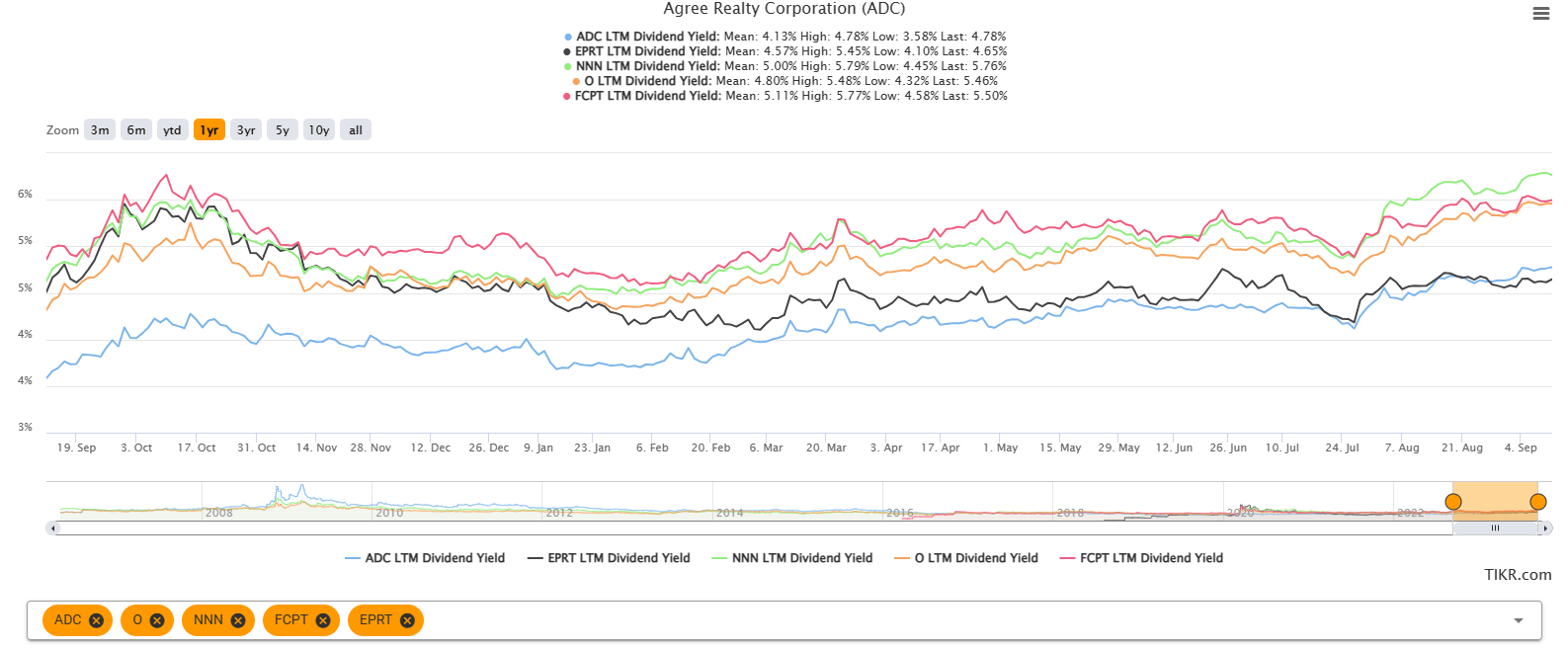

At June 30, 99.7% of its portfolio was occupied and had a remaining weighted average lease term or WALT of 8.6 years. This less impressive compared to what we have discussed so far for this REIT. At the same timepoint, its competitors like Realty Income Corporation ( O ) and NNN REIT, Inc ( NNN ) had a higher WALT of 9.6 years and 10.2 years , respectively. Essential Properties Realty Trust, Inc. ( EPRT ), a fan favorite, surpassed them all with a WALT of 14 years at June 30, 2023. ADC's WALT is more comparable to a net lease REIT that we recently covered , Four Corners Property Trust Inc ( FCPT ).

ADC has been at the forefront of most of the pack in the last 5 years, in terms of the total return that it earned its investors.

In recent times however, the market seems to have a change of mind and we can see that in its 3 year total return.

We can also see that from the drubbing it received over the last one year.

While multiple contraction had a hand to play in this underperformance, the fact that it had the lowest starting yield amongst the five, did not help.

{kind=link}

We take a look at the most recent financial results and explain our outlook for this REIT.

Q2-2023

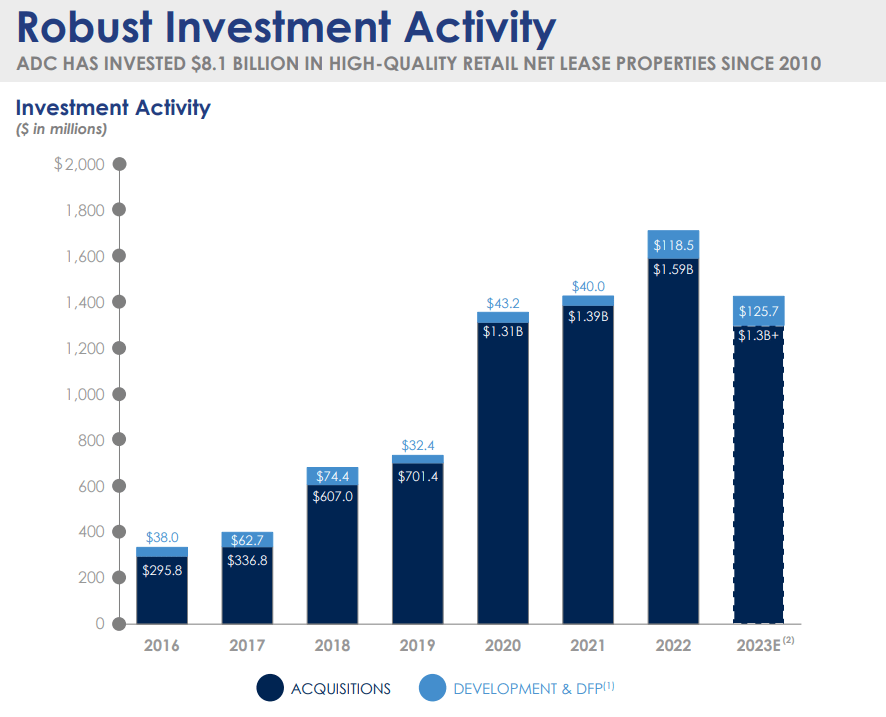

The portfolio grew by close to 400 properties in the one year since June 30, 2023. This drove the rental income higher by 24% year over year.

{kind=link}

Rental income did not make this journey alone. The costs associated with owning additional properties also reflected the same upward trajectory. As noted by the increase in the property count above and the graph below, ADC has ongoing investment projects.

{kind=link}

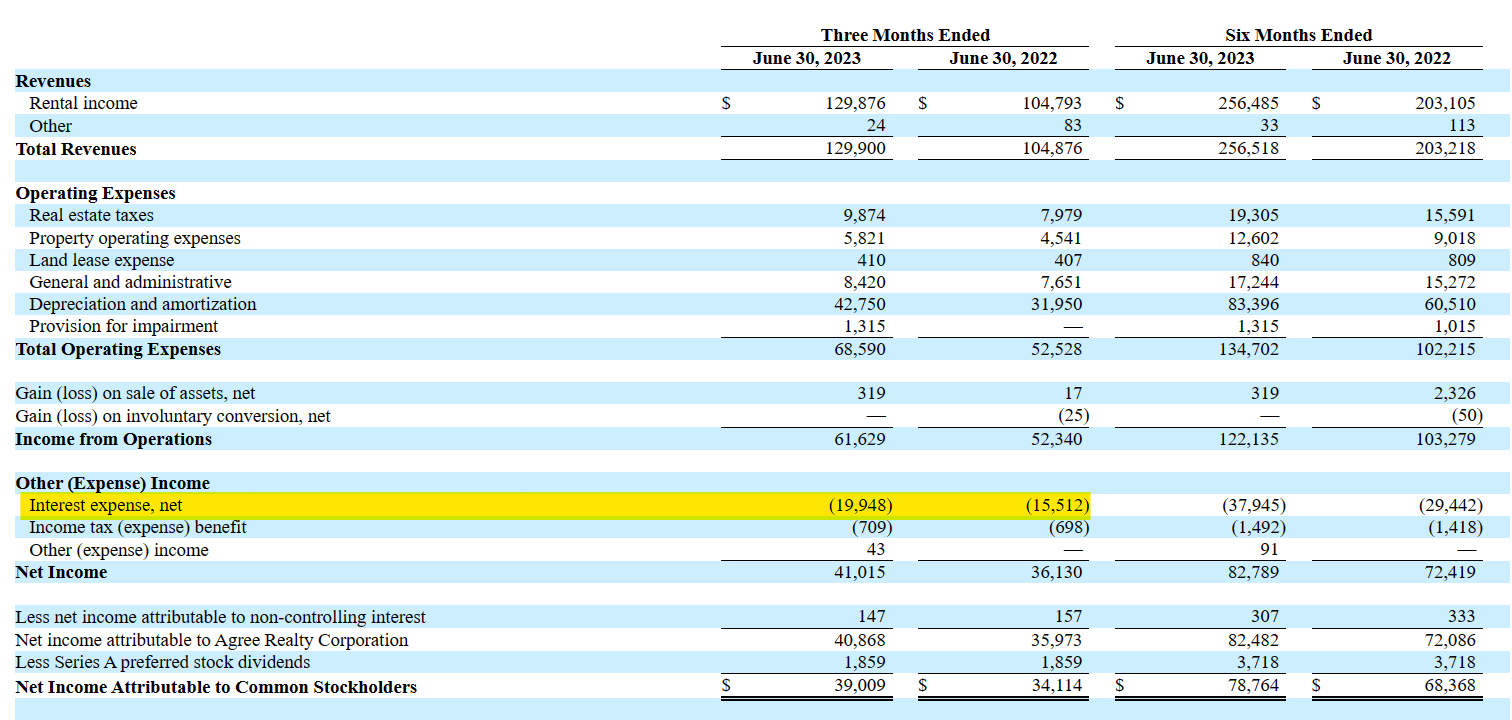

All of this activity cannot be funded by operational cash flows alone as most of it goes towards dividends. Borrowings, along with equity issuances, have a hand in filling the funding coffers. Additional borrowings via public notes and its revolving credit facility at higher interest rates, resulted in a 29% increase in year over year interest expenses.

{kind=link}

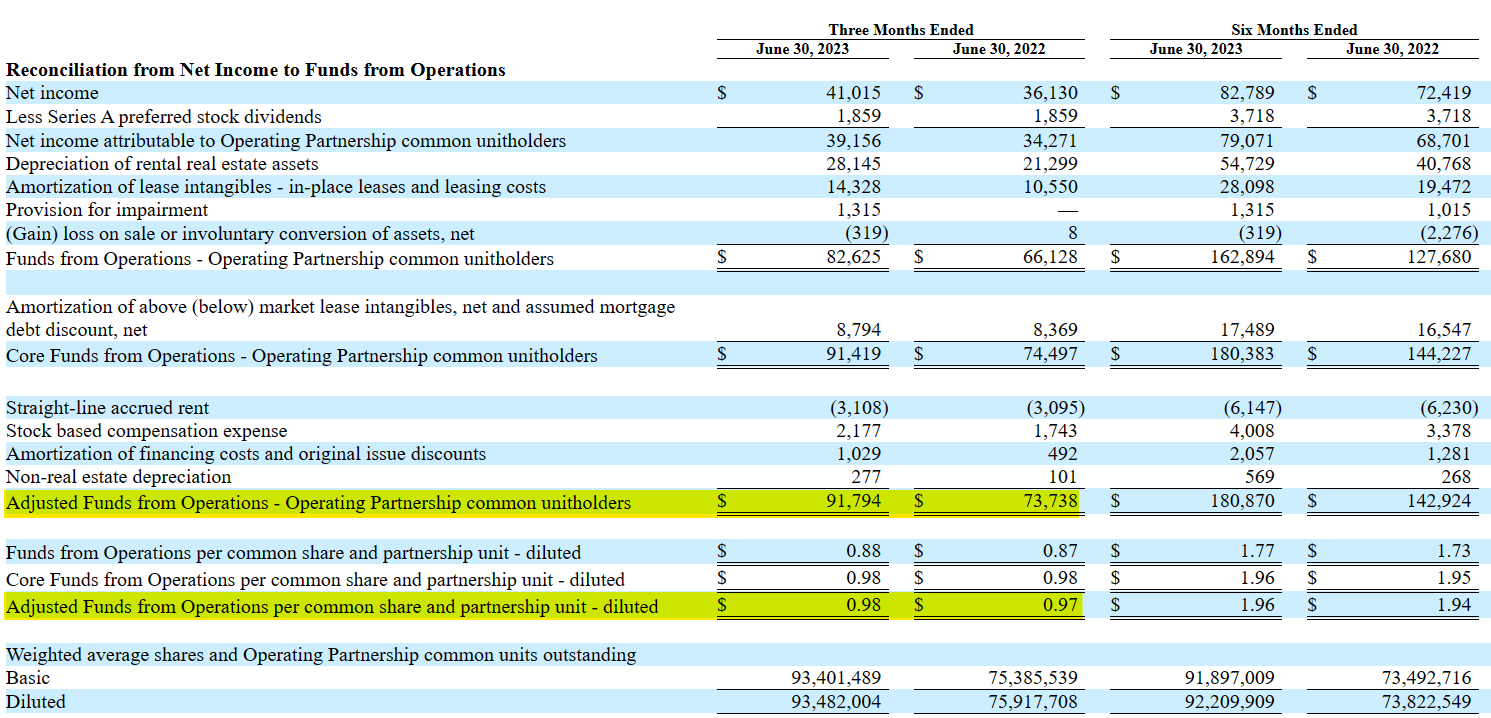

Increase in expenses notwithstanding, the total funds from operations or FFO matched the rental revenue by reflecting an increase of 24% year over year.

{kind=link}

The per unit amounts showed an increase, but a considerably muted one. That is not unusual for a REIT that is active in the acquisition and development front. Recall that we mentioned that equity issuances are one of the two modes that support growth endeavors. We can see that in action above with the higher ending units compared to the prior period. Also evident with the graphic below is that common equity issuances have been the vehicle of choice for this REIT.

{kind=link}

And this has not been a bad choice for the last few years, when its cost of equity was well under the yields at which the REIT made its purchases. At present, ADC's cost of equity using the FFO inversion method is around 6.75% (forward FFO estimate 4.03, current price $59.79). The REIT's acquisitions in Q2 have been at a weighted average capitalization rate of 6.8%. The purchases have been accretive, but not by much. As a result there is little room for the growth in the total FFO to translate into an substantial increase in the per unit amounts. However, that is part and parcel of investing in a growth oriented REIT and unitholders are more interested in where the REIT will be in a few years versus the present.

Debt and Liquidity

While considerably lower than at the end of 2022, ADC had $12.2 million of cash and cash equivalents at June 30, 2023.

{kind=link}

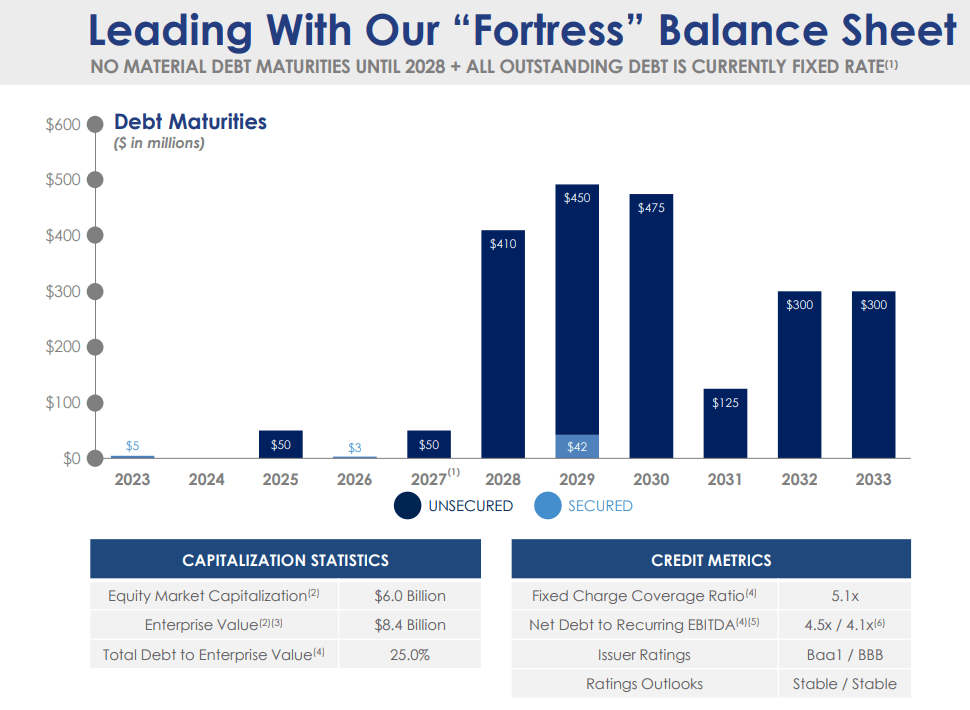

In addition, it had $697 million available to borrow on its revolving credit facility. In terms of maturities, the REIT was well set, with nothing substantial coming up due until 2028.

{kind=link}

We can see by comparing the cash and revolving credit resources, to what is due in the next little while, that ADC will not be breaking a sweat on the refinancing front. The debt to EBITDA is at the low end of the triple NET REIT spectrum and the credit ratings are well deserved.

Verdict

ADC has finally got a reasonable multiple. At 15X FFO, you can certainly get a solid long-term return from here. So bulls wanting a safe and solid, triple-net play, won't get any red (or even orange) flags from us. But we will bring attention to the fact that it still remains expensive on a relative basis . Whether you run the FFO multiple against NNN, O or W. P. Carey ( WPC ), ADC is still expensive. The same metrics also mean that you can get literally 2% higher dividend yield for WPC than you can with ADC. So you can argue that 15X is absolutely cheap, but relatively expensive.

Now, there are two advantages here that might be used as arguments as to why it is ok to pay more for ADC. The first being that it pays its dividend monthly. This appeals to the masses, but it is not one we give any consideration to. If you prefer $162 a month versus $670 every three months (for WPC), please let us know and we can finance that for you. We don't believe even Warren Buffett can beat that internal rate of return, so we will be glad to take it.

The second factor is that it has grown faster than the average triple-net REIT over the past few years. We don't dispute that. But that is a logical consequence of having a high multiple. If two REITs are buying 6% cap rate properties, then the one sporting 20X multiple will grow faster than the one with the 14X multiple. So ADC's growth while faster, is what you expect when you pay that premium multiple. The risk remains that the market smashes this to match the multiples of the other REITs in the current environment. We prefer the beaten down names in this sector which offer more downside protection and a higher dividend yield.

Agree Realty Corporation 4.250% DEP PFD A ( ADC.PR.A )

When we look at a company, we examine all parts of the capital structure to see if one merits an investment. The preferred shares are certainly interesting here as they currently yield 6.3% and have a monthly payout system. They were issued at the peak of the "cash is trash" mania and have only a 4.25% coupon on par value. But the large decline in price has resulted in a solid yield. Moody's rates the debt of ADC at Baa1, and the preferred shares at Baa2 (equivalent to BBB of S&P). So these are actually two notches over the junk territory and well into investment grade category. We agree that the rating here is accurate and these may be a consideration for those that want a low risk yield from a quality company. They are also likely to benefit in a heavy rate cutting cycle and could give 20% capital gains if rates fall. For us, we need a minimum of 7% on these to get interested. So they remain on our watch list. At present we like Rexford Industrial ( REXR ) preferred shares, which are of even higher quality in our view and offer a slightly better yield.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Agree Realty: The Monthly Payer Is Absolutely Cheap But Relatively Expensive