ADC - Agree Realty: Why This Recession-Resistant REIT Is A Strong Buy Today

2023-04-17 08:30:00 ET

Summary

- ADC's enjoys arguably the most recession-resistant portfolio and tenant roster among net lease REITs and perhaps in all of REITdom.

- The balance sheet is also in tip-top shape with among the lowest leverage in its peer group and exceedingly few debt maturities until 2028.

- ADC also boasts a peer-leading cost of capital, going into 2023 with around $1.5 billion in total liquidity.

- For very conservative investors, ADC also offers a preferred stock currently yielding ~5.9% with 38% upside to par.

Thesis: Built To Survive And Thrive In Recessions

Agree Realty Corporation ( ADC ) is a net lease real estate investment trust ("REIT") focused on high-quality, single-tenant net lease retail properties leased to the nation's 30-35 leading retailers.

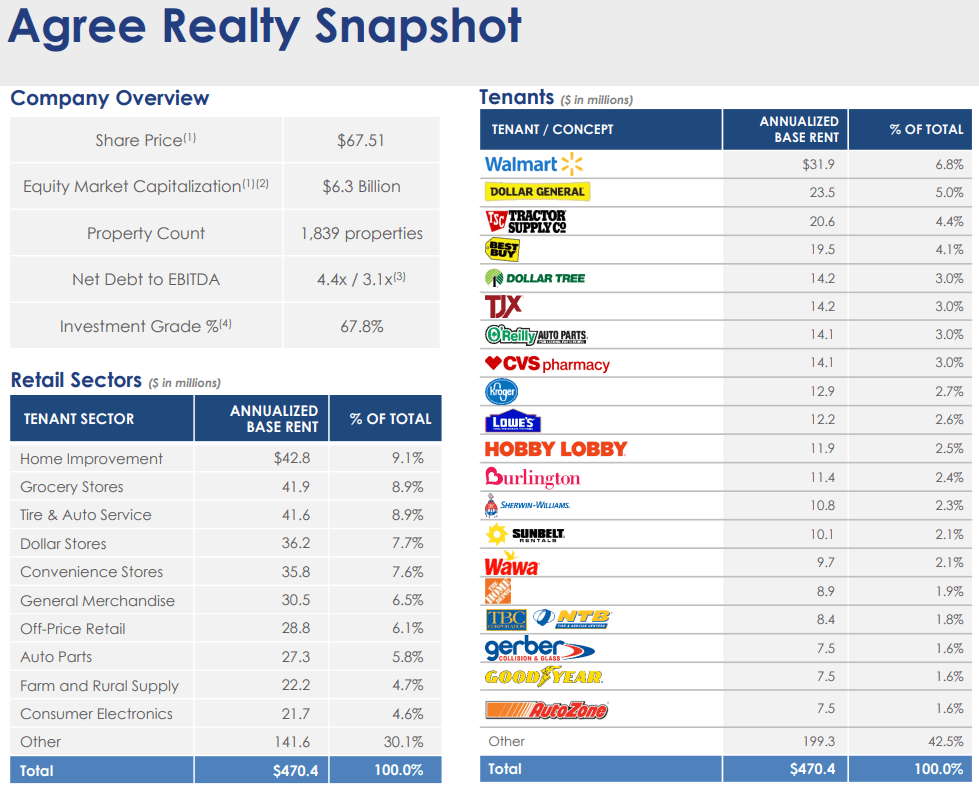

Its portfolio of 1,839 properties (as of the end of 2022) is populated uniformly by high-credit tenants with ample cash to weather a recession as well as to invest in their omnichannel platforms. Better yet, its tenant base is overwhelmingly recession-resistant with a mix of essential and discounted goods. Some tenants, like Walmart ( WMT ) and Dollar General ( DG ) (ADC's #1 and #2 tenants, respectively) are also arguably countercyclical in that they have established a record of growing sales through past recessions.

This portfolio, including a tenant roster of industry-leading retailers occupying well-located properties with long-term leases at below-market rent rates, is one major reason why ADC is perhaps the most recession-resistant REIT.

Another major reason is the strength of ADC's BBB-rated balance sheet, illustrated by the peer group-low leverage ratio of 4.4x (or 3.1x if you include forward equity) and miniscule amount of debt (5.4% of the total) maturing until 2028.

The combination of

- a high-quality and defensive portfolio,

- fortress balance sheet,

- peer-leading cost of capital, and

- focused and shareholder-aligned management team led by CEO Joey Agree

is what makes ADC such a recession-resistant investment.

Meanwhile, it's a valuation near the 5-year low based on AFFO multiple and dividend yield that makes ADC a strong buy today.

ADC April Presentation

Why ADC Is The Ultimate Recession-Resistant REIT

Let's address those four points listed above.

A High-Quality And Defensive Portfolio

ADC's real estate portfolio can be likened to that of a bodybuilder: lean, strong, and containing little to no "fat." It's a well-curated portfolio populated by what management calls their "sandbox" of the largest and strongest retailers in the nation.

These are characteristically high-credit national and super-regional companies, exemplified by the 67.8% share of total tenancy. Even this undersells the portfolio's credit quality, as many of its non-rated tenants like Hobby Lobby and Publix have investment grade-equivalent balance sheets.

{kind=link}

Notably, ADC's top four tenants of WMT, DG, Tractor Supply Co. ( TSCO ), and Best Buy ( BBY ), in addition to many others, all increased their sales through both the Great Recession of 2008-2009 and the COVID-19 pandemic of 2020-2021.

These are highly recession-resistant, non-cyclical or even countercyclical businesses. When times get tough, people tend to shop at low-cost stores like Walmart, Dollar General, and T.J. Maxx ( TJX ) more , not less.

These are retailers with the financial wherewithal not only to survive recessions but also to continue investing heavily in their omnichannel strategies that will solidify their positions as industry leaders.

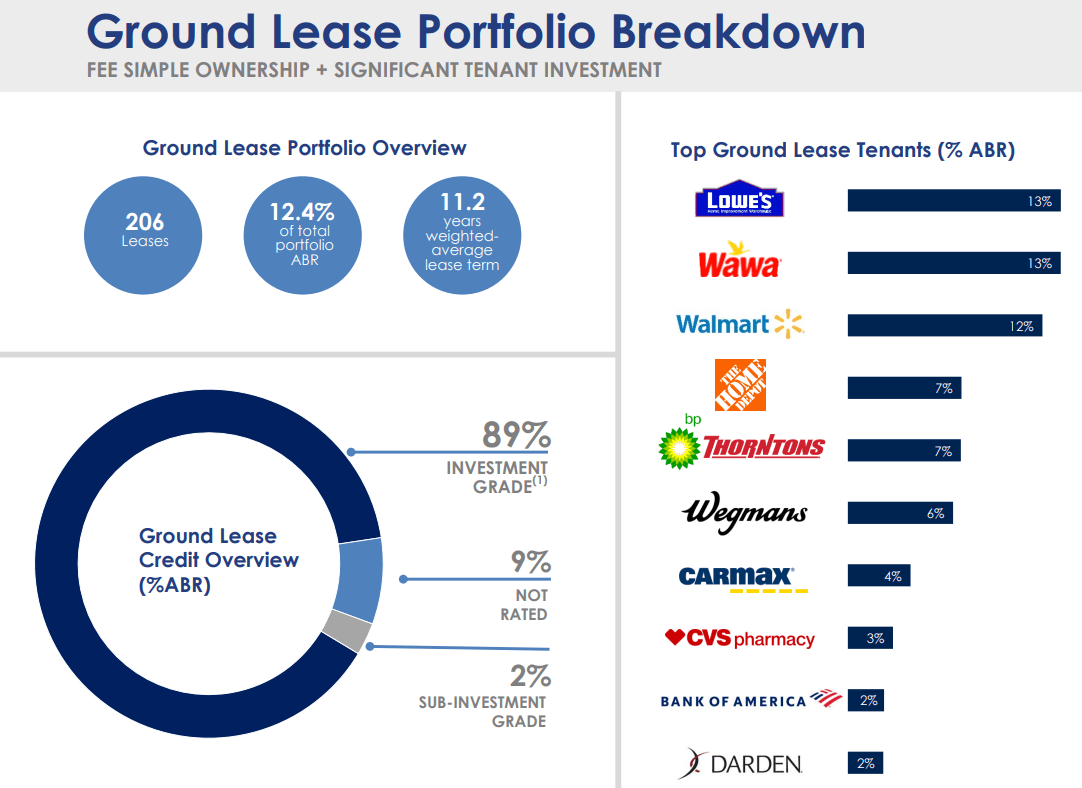

Further solidifying the defensiveness of the portfolio is the fact that 12.4% of it is in ground leases, wherein ADC owns the land while the tenant owns the improvements (building or structure) on it.

{kind=link}

These investments are ultra-defensive because:

- The tenant has greater investment in the property via ownership of the improvements

- Rents per square foot are lower

- The improvements revert to the ground owner ( ADC ) in the case of a tenant move-out or lease default

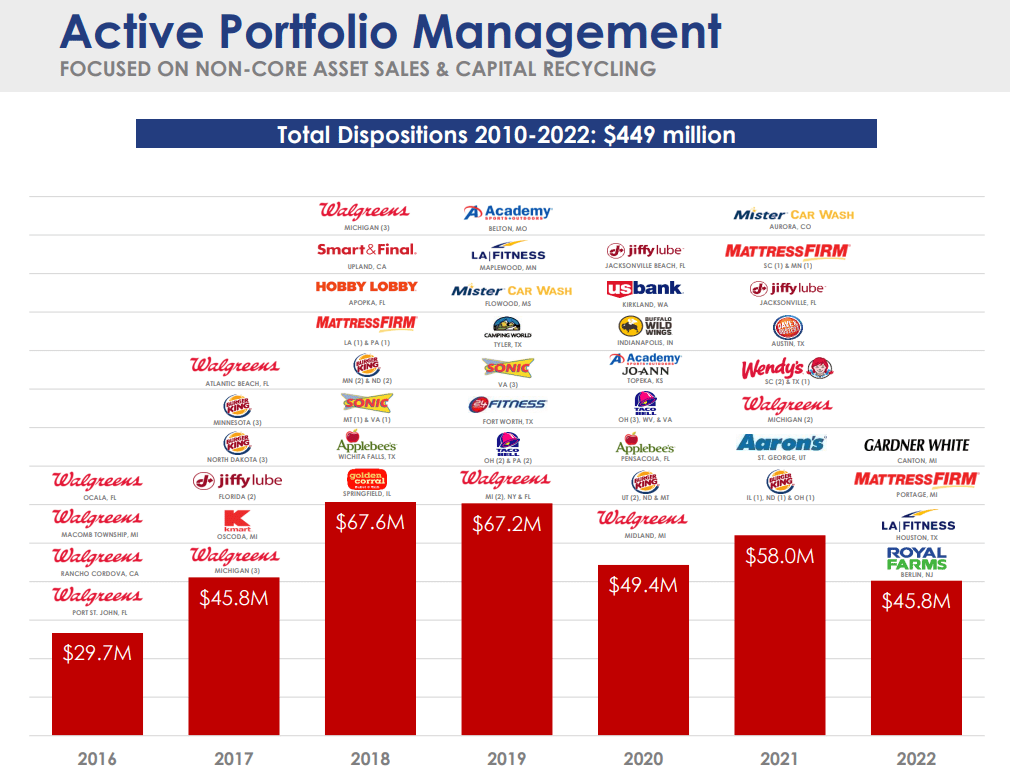

Like a beautifully carved statue (pardon the mixed metaphors), ADC's portfolio got the way it is now through disciplined chiseling away of the unwanted pieces. These dispositions of non-core assets have stripped the portfolio of weaker retailers, less desirable locations, older buildings, and private equity-backed tenants.

{kind=link}

But the quality of ADC's portfolio is not in its tenant credit ratings alone, but rather in the real estate more broadly. That includes factors like the location and the fungibility (reusability) of the buildings.

In a recent interview I conducted with CEO Joey Agree (which will soon be published exclusively for High Yield Landlord subscribers), he explained his view of what ultimately determines the value of net lease real estate:

"The magic of being a net lease investor is that while you have bond-like cash flows, you don’t have the principal repaid at the end of the lease. You have a piece of real estate. You have to assess what the terminal value of that real estate is. What drives the terminal value of that real estate is the ultimate demand for it given its size, shape, location, market, and so on."

Strong real estate retains or grows both its market value and its market rent over time. That is no less true for net lease than for any other CRE sector.

Interestingly, so far this year ADC has significantly underperformed many of its top retailer tenants like Walmart and Tractor Supply:

I suspect this is because of the rise in interest rates. But how vulnerable is ADC to the headwind of higher interest rates? Answer: Not very.

Fortress Balance Sheet

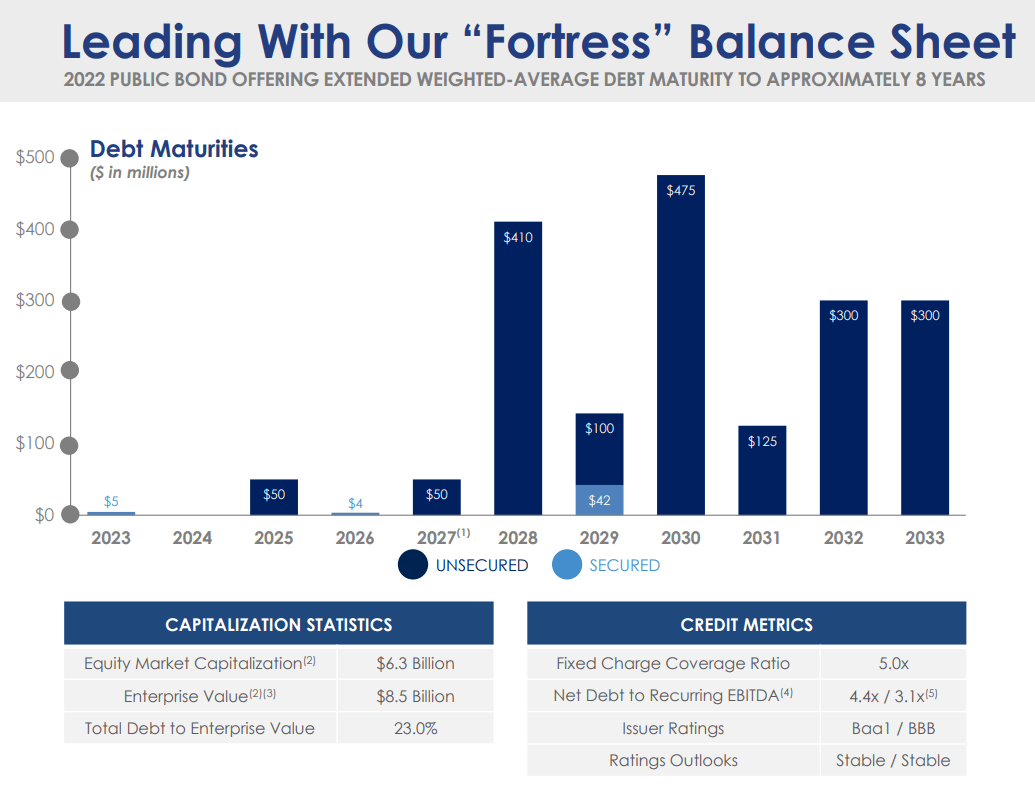

ADC enjoys a strong balance sheet with leverage among the lowest in its peer group. This is measured by total debt to enterprise value of a little less than 25% and net debt to EBITDA of 4.4x, as of the end of 2022.

Perhaps more importantly in the current high interest rate environment, ADC has exceedingly little debt maturing anytime in the next 4.5 years.

{kind=link}

What little is maturing through 2027 could easily be paid off with retained cash after dividends, if management chose to do so.

If ADC's balance sheet remains in more or less the same condition going forward, it should be only a matter of time before the REIT earns a credit upgrade from its current BBB to BBB+.

Peer-Leading Cost of Capital

An investment strategy focused on high-quality net lease properties requires an adequately low cost of capital, because net lease REITs are constantly issuing capital for acquisitions and other investments. The crucial margin in net lease investing is the sustained spread between weighted average cost of capital ("WACC") and effective yields on investments.

ADC came in to 2023 with around $1.5 billion in total liquidity between $900 million available on the credit facility, $557 million in unsettled forward equity, and cash on hand.

At the end of 2022, ADC's credit facility featured a spread over the SOFR of 88 basis points, but the pricing is based on the leverage ratio. As leverage rises, so also will the spread over SOFR. We might assume that as ADC draws more on its revolver, the spread will average around 100 basis points this year. So, with SOFR at 4.8% as of April 14th, we might assume ADC's interest rate on the credit facility currently sits at around 5.8%.

That would imply a narrow spread if ADC is still acquiring properties at cap rates of 6.0-6.2% as it did last year. But cap rates are creeping up this year, which indicates that ADC will probably be able to acquire properties in the mid-6% cap rate area this year.

Adding in the $557 million in forward equity ADC had available at the end of the year, priced at an AFFO yield of 5.8%, as well as whatever ATM equity issuance ADC has completed YTD (at, let's call it, a 5.5% AFFO yield) and $85 million in free cash flow after dividends (zero cost), I would estimate ADC's weighted average cost of capital ("WACC") to be around 5.25% so far this year.

Thus, even in this difficult capital raising environment, ADC still maintains the WACC to grow its portfolio accretively.

I would assume that the recently announced 1.2% hike to ADC's dividend is lower than usual (c.f. ADC's 10-year dividend CAGR of 6%) because of management's desire to preserve more cash for reinvestment. (ADC's pattern is to hike their dividend twice a year: once in the Spring and another time in the Fall.)

Of course, BBB bond yields have been trending down over the last month...

...so if bond yields or term loan rates come down enough this year, ADC will perhaps be able to lower its WACC even further by locking in long-term debt.

And, of course, the bond market seems to be pricing in Fed rate cuts by the end of this year, which would also lower the effective interest rate on ADC's credit facility.

Note that while ADC's largest peer in the net lease REIT space, Realty Income ( O ), enjoys a lower cost of debt due to its A3/A- credit rating, its current AFFO yield of around 6.5% is significantly higher than ADC's 6.0%. Moreover, O's 2023 payout ratio of 77% is a bit higher than ADC's 74%, which means ADC has slightly more FCF after dividends to deploy into acquisitions.

What if interest rates remain higher for longer and never go back to their ultra-low levels of 2021? If that happens, then cap rates will stabilize at a correspondingly higher level as sellers capitulate to the new reality, and ADC's investment spread will widen again.

There are periods in which the spread between capital costs and cap rates is wide, and periods where the spread is thin. Right now, the spread is thin. But if interest rates stabilize at a higher level, so too will cap rates, and ADC will continue to enjoy a peer-leading cost of capital.

Valuation

According to Seeking Alpha data , ADC's forward price to AFFO sits at 16.95x right now. However, I would guesstimate ADC's 2023 AFFO per share to come in around $3.96, which would represent 3.5% year-over-year growth. That would give the REIT a forward AFFO multiple of 16.7x

In 2022, comparing price to 2022's AFFO per share of $3.83, we find that ADC briefly traded as low as a forward AFFO multiple of 16.3x and as high as a forward AFFO multiple of 21.0x with an average multiple of 18.2x.

If we follow the same exercise for 2021, we find that ADC traded only as low as a 17.8x multiple and as high as a 21.5x with an average of 19.8x.

For 2020, ADC traded as low as a 15.2x multiple during the deepest depths of the initial COVID-19 market selloff ( ahem , right around the time I first highlighted ADC as " A Recession-Resistant Net Lease Growth Machine ") and as high (before COVID hit) as a 24.9x multiple with an average of 20.8x.

We can go back over at least the last five years to find that ADC hasn't been this cheap on a price-to-AFFO basis outside of a few brief periods such as the onset of COVID-19 and in early 2022. In any case, ADC is definitely trading on the very low end of its normal AFFO multiple range.

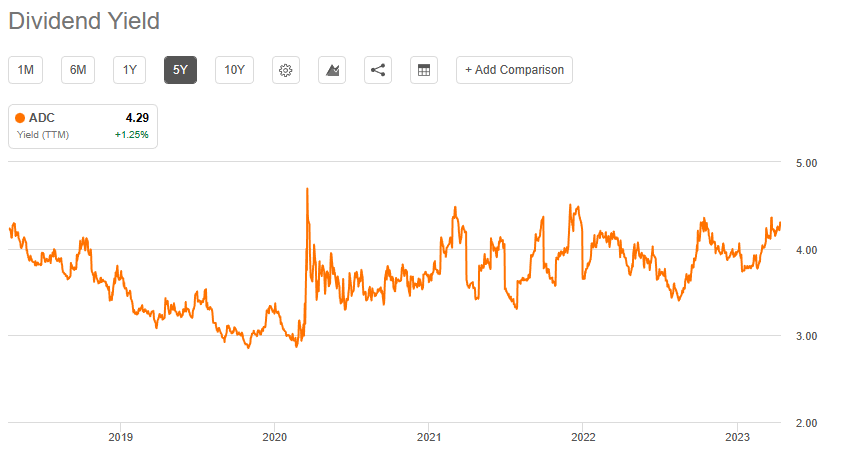

And then there's ADC's dividend yield history over the last five years. Here, again, we find that the current annualized dividend yield of 4.4% has really only been higher for a very short period during the COVID-19 selloff of early 2020:

{kind=link}

If ADC's fundamentals were eroding, perhaps the lower valuation would make sense. But the opposite is true. The portfolio and balance sheet have only gotten stronger in the last several years.

Risks

As you may have surmised from the preceding, I don't believe there to be many material risks to ADC in terms of its portfolio or balance sheet. But there are a few for investors to keep in mind.

- ADC's pipeline of development and PCS (Partner Capital Solutions) projects has been growing lately. These are long-term projects: around 12-18 months from signed contract to commencement of rent. The worst case scenario for these deals is that ADC locks in a cap rate today, and then capital costs rise significantly thereafter, eroding or eliminating the crucial investment spread. These deals only account for 7% of 2022's total committed investments, though.

- If capital costs stay high and sellers refuse to budge on prices, ADC's investment pipeline could dry up, cutting off external growth. But given ADC's available capital, the REIT would probably be one of the last remaining all-cash buyers in the market, which should present the REIT with some attractive deals this year.

- Finally, there's valuation risk. ADC is one of the higher valued names in the net lease sector, and deservedly so based on its portfolio, balance sheet, and track record. If we are entering a macroeconomic period in which the spread between capital costs and cap rates remains thin, all net lease REITs will suffer, but ADC may perform particularly poorly because of its higher valuation.

Note, however, that the risk of a dividend cut is very low for ADC because of the resilience of its portfolio, the strength of its balance sheet, and the healthy dividend coverage represented by its 74% payout ratio.

ADC April Presentation

An Even Safer Option: The Preferred Stock

If you want an even safer option than ADC's common stock, look to the 4.25% Depositary Cumulative Preferred Series A ( ADC.PA ) shares. I wrote a full article on ADC.PA highlighting the investment cast for it.

As a testament to ADC's peer-leading cost of capital, the REIT was able to issue this preferred series at a par yield of 4.25%, the second lowest level any REIT has ever issued preferreds.

That may sound unappealing to buy, but since the original issue date, ADC.PA has sold off to $18.10, bringing its yield up to ~5.9%. Sure, there may be higher yields available out there, but none, I would argue, as safe as that of ADC.PA.

Plus, as I explained in the article, ADC.PA is basically a bond proxy and should see significant upside if interest rates fall. So, the worst you can do with ADC.PA is a 5.9% return from the dividend. And the best you can do would be that 5.9% yield plus upside to par of 38%.

If interest rates stabilize at a lower level but not all the way back down to their ultra-low levels from 2021, then ADC.PA's upside is probably somewhere between 0% and 38%. Where exactly? I'm not sure.

ADC April Presentation

Bottom Line

If it walks like a duck and quacks like a duck, it's probably a duck.

Likewise, if ADC's portfolio and tenant roster are recession-resistant, balance sheet is recession-resistant, and cost of capital is recession-resistant, then it seems safe to say that ADC is a recession-resistant REIT.

ADC is built to survive and thrive during recessions. To illustrate this, in March 2020, in the middle of severe market panic surrounding COVID-19, ADC secured a new forward equity deal in order to load up on dry powder to take advantage of any good deals to come during the market disruption. Also, during the pandemic, ADC's rent collection rate never dropped below 87%, and the REIT ultimately collected virtually all contractual rent that went unpaid during the crisis.

ADC is cheap, offers a very attractive 4.4% dividend yield, and boasts a 10-year record of 6% average annual dividend growth.

If you're worried about the upcoming recession, I would argue that there is no better sleep-well-at-night REIT (or, for that matter, stock ) to buy today.

Editor's Note : This article was submitted as part of Seeking Alpha’s Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Agree Realty: Why This Recession-Resistant REIT Is A Strong Buy Today