AHODF - Ahold Delhaize: A Great Combination Of Dividend Yield And Growth

2024-01-14 07:49:05 ET

Summary

- Ahold Delhaize is a quality dividend growth stock with enough opportunities to keep sustainably growing in the future.

- The company offers a safe starting yield of 4% and is well on track to deliver long-term dividend growth.

- Based on discounted cash flow analysis, Ahold is undervalued and offers significant upside from a share price point of view.

- Persistent inflation and further margin compression are short-term factors that must be taken into account before investing in Ahold.

Investment thesis

It's always good to have some defensive blue chip stocks in your portfolio. This offers lower risk, lower volatility and stability in uncertain times. Especially in the consumer staple sector there are a lot of companies that meet those criteria. The consumer staple sector in general has underperformed last year, but this always creates attractive investment opportunities. This brought Ahold Delhaize N.V. ( ADRNY ) into the spotlight.

{kind=link}

Ahold is a solid long-term compounder and is offering a relatively high dividend yield compared to its peers.

In this article I want to show you why I think Ahold is an attractive dividend growth investment at current prices.

Company overview

Ahold operates different retail food stores and E-commerce globally. The company has a market cap of €25.22 billion and is headquartered in Zaandam (The Netherlands).

Ahold Delhaize (Investor relations)

Shares of Ahold are trading at Euronext Amsterdam (AD.AS), but is also available as an ADR ( ADRNY ).

Ahold was formed not too long ago (2016). However, some of the brands have been around for a very long time. This includes brand such as Delhaize (1867) and Albert Heijn (1887). It all started with small grocery stores and the rest is history.

{kind=link}

Despite the fact that Ahold is a European company, most of its sales are generated in the United States. Think about brands such as Food Lion, Giant Food, The Giant company, Stop & Shop and Hannaford.

Ahold is operating in many other countries, such as, The Netherlands, Belgium, Luxembourg, Greece, Czech Republic, Serbia and Romania.

{kind=link}

Since the merger (2016), the financials look solid. Based on the numbers of Seeking Alpha, Ahold has a revenue CAGR of 3.57% (Dec 2017-Jan 2023), which is decent. The company has a basic EPS CAGR of 7.8% in the same period and the FCF per share CAGR of 12.5% is even better. The last metric is the most important, because this has to do with the ability of the company to generate a healthy amount of FCF. This allows the company to make new investments or return capital to shareholders.

Catalysts

The metrics we just covered are a representation of the past, but the most important thing is whether they can do this in the future as well. It is clear that Ahold knows how to grow a business sustainably. One of the largest brands in the US, Food Lion, has achieved positive sales growth for 44 consecutive quarters, which is impressive.

However, it is always good to know where future growth can possibly come from. Don't expect fast growth from a company like Ahold, but there are certainly some potential growth drivers to mention.

M&A

On October the 30th 2023, Ahold has announced its plans to acquire 100% of the Romanian retailer Profi. This will double the total business of the company in Romania and will be fully funded by debt. Ahold Delhaize will pay an Enterprise Value of €1.3 billion and is likely to close in 2024.

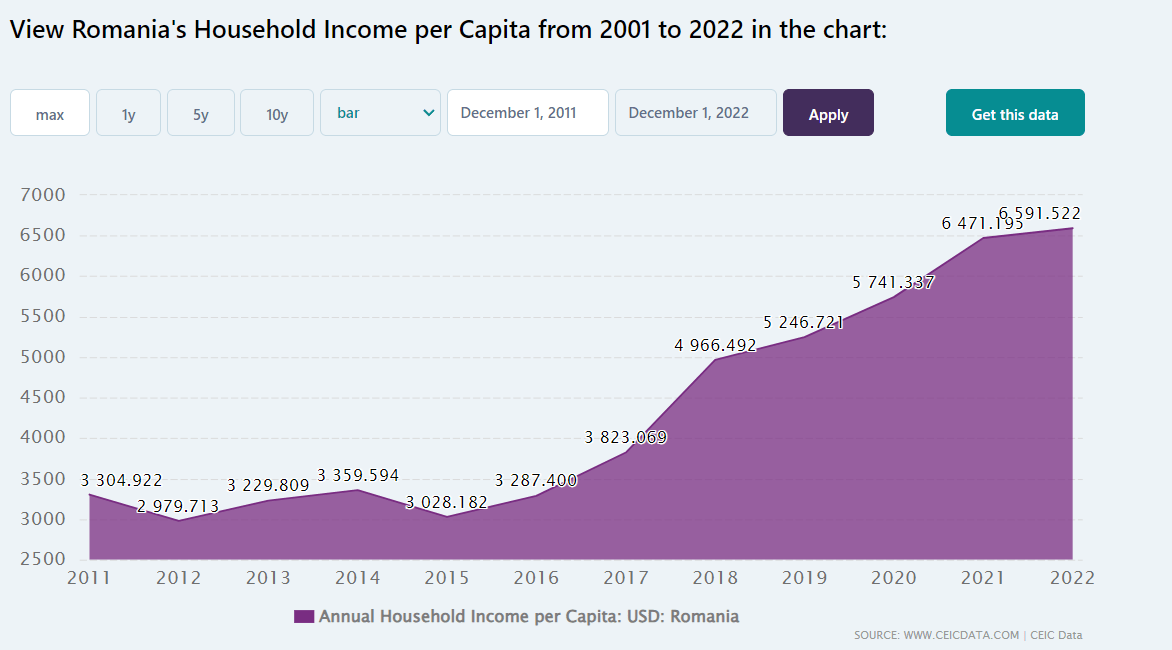

In my opinion this is a good deal, because Profi also seems to fit in well with the stores they already have in Romania (Mega Image). The Romanian economy is also steadily growing and the market isn't entirely saturated when it comes to grocery stores. Also the household income per capita is growing nicely, which could lead to more expenditure on (premium) food and drinks.

{kind=link}

In the last 12 months Profi generated €2.5 billion in sales, which amounts to a total revenue increase of 2.8% for Ahold. The acquisition could also lead to higher profitability because of the potential attractive EBIT margins, which should be higher than the average EBIT margin they achieve in Europe right now (3.5%).

E-commerce

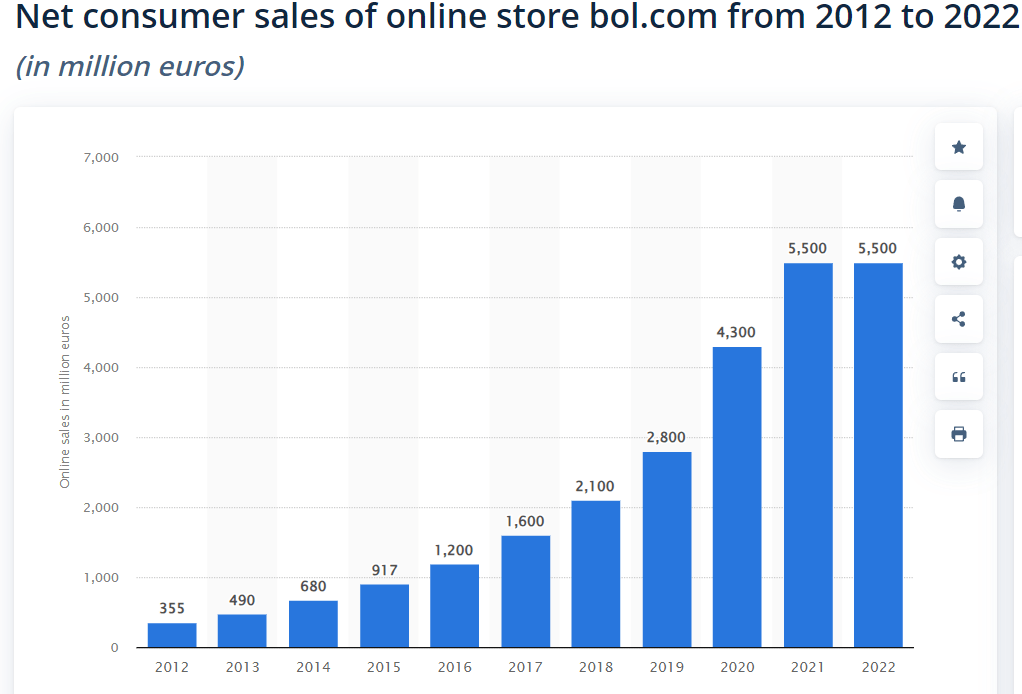

Ahold is a company that can benefit from the long-term growth trend in E-commerce with Bol. Bol is often called the Amazon ( AMZN ) of the Netherlands. More than 13 million people in the Netherlands and Belgium are using Bol and over a 10-year timeframe they achieved significant sales growth.

{kind=link}

Despite the presence of other e-commerce platforms in the Netherlands, like AMZN, Bol is gaining market share again.

{kind=link}

Bol achieved an increase in gross merchandise value of 6.5% compared to FY 2022. What is also good to see is that the advertising revenues and logistic offerings are gaining traction as well.

What is also good to know is that it is still possible that Ahold is going to publicly list Bol. However, they keep postponing this and they are still looking for a better "IPO-climate" to think about this again. I think that Bol will go public at some point. It will also be a good way to raise capital to finance further growth to compete with AMZN.

Omnichannel retail strategy

Further rolling out their omnichannel strategy can trigger growth in the future too. This strategy blends various shopping channels, like physical stores, apps, online stores, into one unified customer experience. This should lead to a more personal shopping experience, more brand loyalty, more customers and sales. Ahold's business model is ideal for this approach and they invest into this as well.

{kind=link}

Balance sheet

Ahold's balance sheet looks decent. The company has got a BAA1 credit rating from Moody's and a BBB from S&P global. This means that they're in the investment grade range, but they're subject to moderate credit risk and adverse economic conditions.

Ahold has an interest coverage ratio of 15.19, which means they don't have any problems paying their interest.

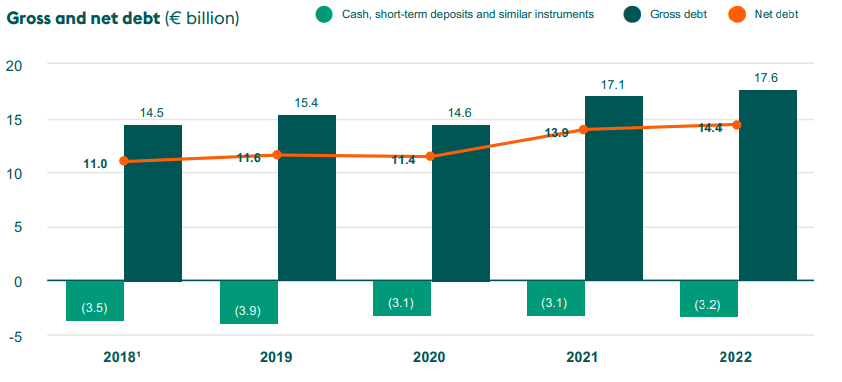

Looking at the liabilities it is visible that their gross- and net debt is slowly increasing over time.

{kind=link}

It is good to know that the non-current portion of their debt is €15.164 billion (86.1%) and there are no important maturity dates in the short term. The increase in net debt was the result of exchange rate movements on the US dollar, increase in leases, and the payment of dividend (€979 million) and their share buyback program (€1 billion).

Their net debt-to-EBITDA is 2, which is considered healthy. With the acquisition of Profi in prospect, this will increase to approximately 2.2 and is in my opinion still acceptable.

What is important to mention is that the total of the share buybacks and the dividend (€1.979 billion) is quite high compared to the FCF of 2022 (€2.188 billion). At this moment in time I think the company is stable enough to handle it, but it should not happen year after year that they pay shareholder distributions by raising debt, especially if they also make acquisitions. This could potentially put too much pressure on the balance sheet.

In the future, I will look at the way Ahold uses its capital when it comes to shareholder distributions and how the company manages its debt.

Dividend

Ahold has a clear ambition to sustainably grow their dividend year-over-year. I always look in the annual reports if I literally see this as an objective. Especially for European companies, as the amount of real dividend growers is limited compared to US companies.

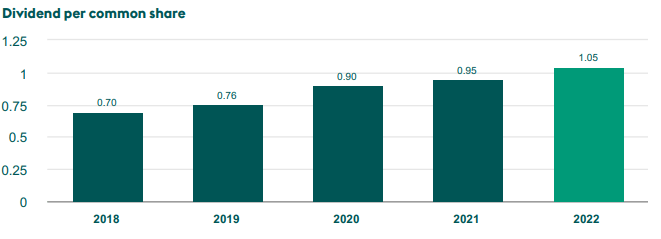

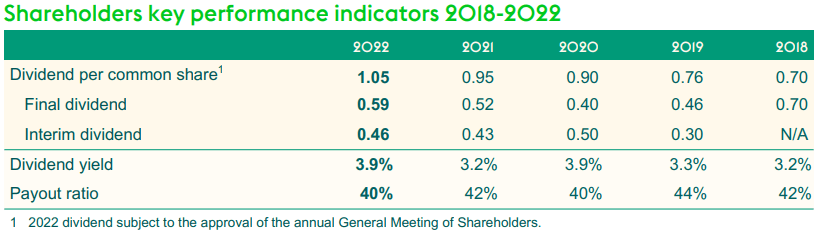

Ahold pays a semi-annual dividend, which was a total of €1.05 in FY 2022.

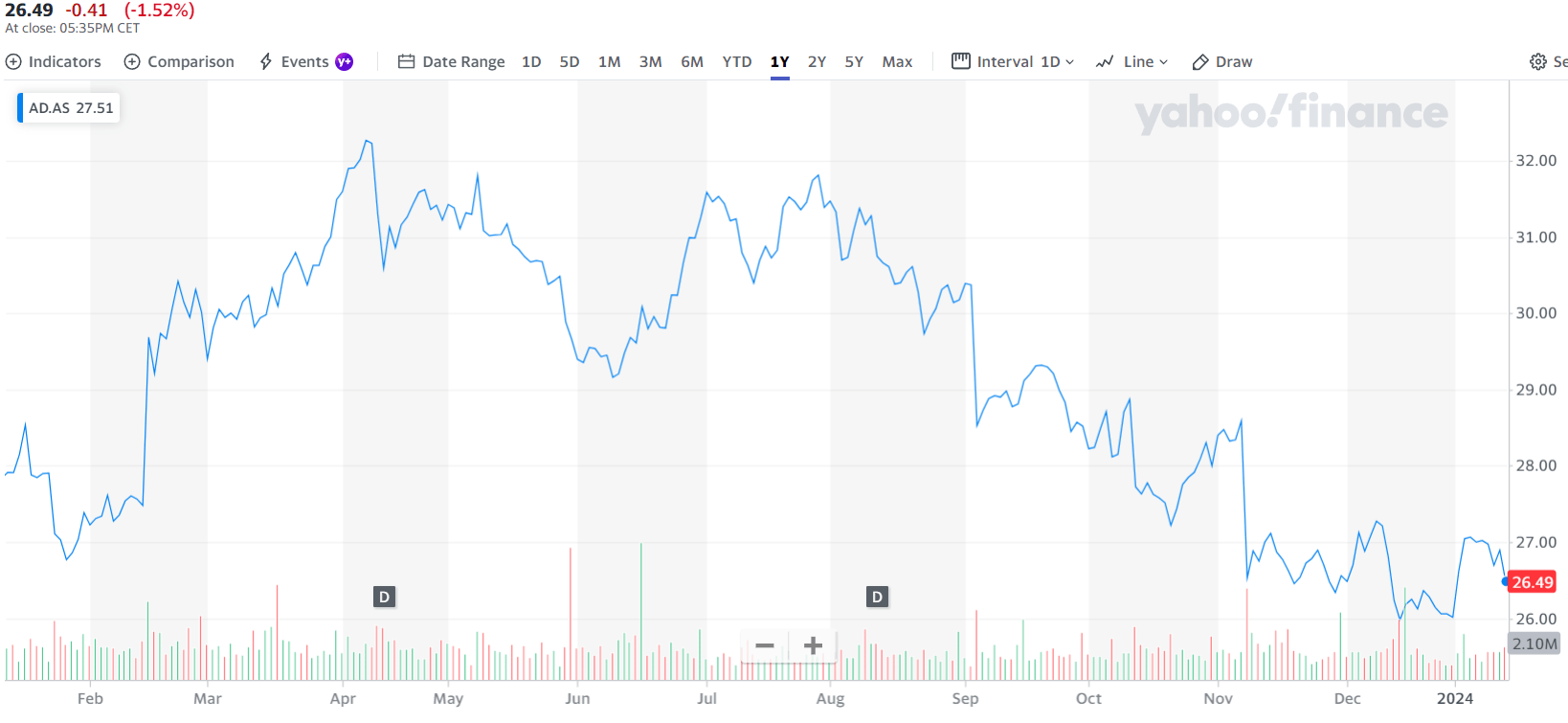

If we take this number and divide it with the current share price of €26.49 we get a dividend yield of around 4%, which is a great yield to start with. The yield is also significantly higher compared to the sector median of 2.43%.

Over the last 5 years, Ahold has been able to steadily increase its dividend with a 5Y CAGR of 8.4%.

{kind=link}

The combination of the current dividend yield and dividend growth looks attractive at first glance. Personally, I use the Chowder rule as a screener to assess the combination of these parameters. If the yield is greater than 3% the 5Y dividend growth CAGR + the dividend yield must be greater than 12%.

At the moment Ahold has a Chowder score of 12.4, which means it could be an attractive dividend growth investment. However, the Chowder score relies entirely on past performance and it is relevant to ask yourself whether these results can be extrapolated into the future. I think Ahold has the ability to grow its dividend nicely over time. I do think that the dividend increases will be less high in the short term, but given the stable business model, the long-term picture will not change.

Ahold has the goal of paying 40-50% of its underlying income in the form of dividends. Looking at a 5-year period they were well capable to grow their dividend in a sustainable way.

{kind=link}

I like the fact that Ahold is able to keep the payout ratio below 50%, because it still gives the company some flexibility to invest into growth.

At the moment, Ahold is not yet close to a dividend aristocrat-like status, but I think with the business model of the company and their relatively safe dividend they are in a good position to further increase the dividend in the years to come.

Share buybacks

What also makes the investment case attractive is the amount of share buybacks. Ahold has been able to reduce its share count significantly over the last few years. Since 2016, the number of shares shrank from 1272 million to 977 million, which is a reduction of -23.2%. And the company isn't even finished yet.

{kind=link}

The company has completed its €1 billion buyback program just before the end of 2023 and on top of that the company has announced another €1 billion program for 2024. With its current market cap, we talk about 3.7% and including the dividend it comes down to a total shareholder yield of 7.7%!

Q3 2023 results

The Q3 2023 numbers were not received well by the market as the company failed to meet analysts' expectations, especially from a profitability point of view.

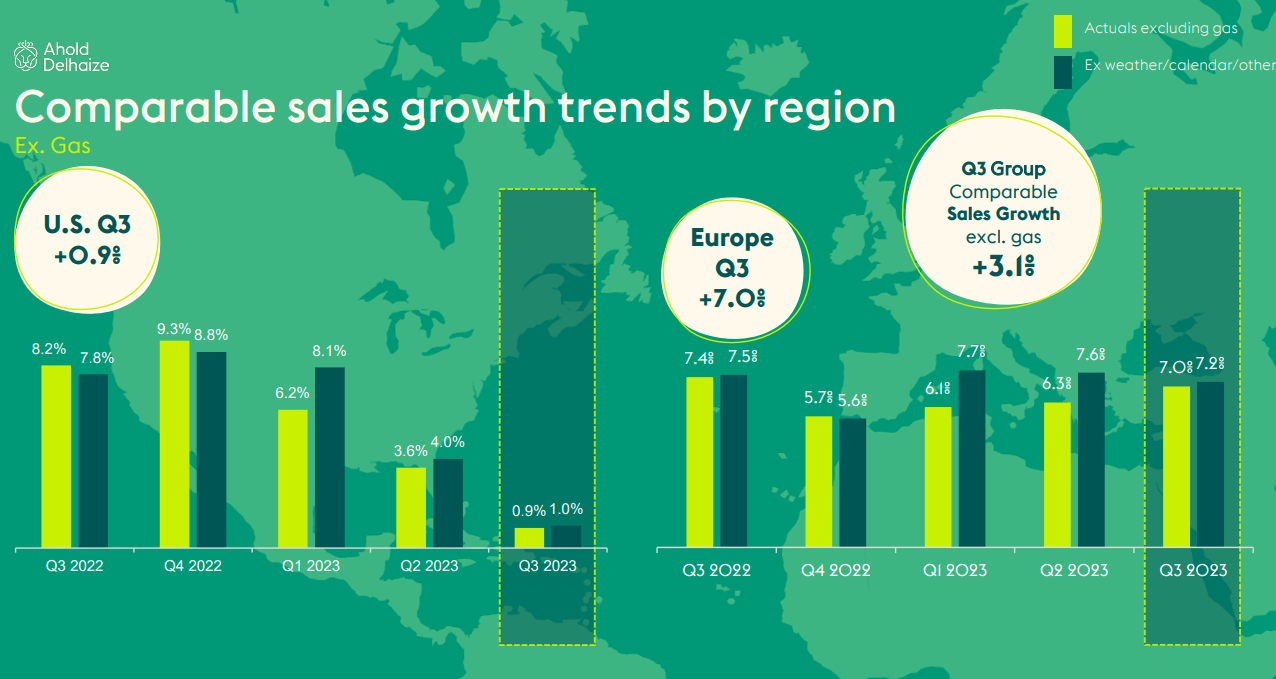

The total revenue of €21.9 billion was down 2.1% due to currency headwinds, which isn't that bad. The sales growth in Europe was much more resilient compared to the growth in the US.

{kind=link}

The overall underlying operating margin decreased to 3.8%. This was mainly due to a decrease in margin in the US (4.2%). Margins in Europe were the same compared to last year (3.5%). This shows that Ahold is having difficulty with persistent inflation and fully passing on these increased costs to its customers.

This has led to a decrease of 17.1% in underlying EPS of 0.58. This was due to a combination of decrease in margin and insurance-related adjustments.

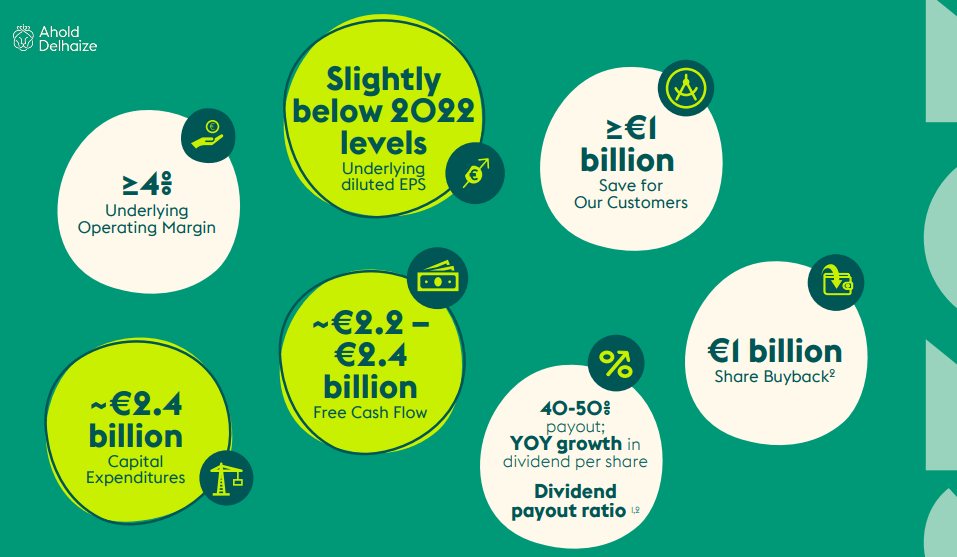

Based on their outlook, Ahold expects that the underlying EPS will be slightly below 2022 levels. Despite the margin pressure they still expecting an underlying margin of at least 4% for 2023. They also updated their free cash flow to €2.2-€2.4 billion, which is actually higher compared to their previous outlook (€2.0-€2.2 billion).

{kind=link}

In summary: Not bad in terms of free cash flow, but margin development and results in the United States were less than expected. It is certainly possible that this trend could continue next year, but if I look at the bigger picture this should not be a threat in the long-term.

Valuation

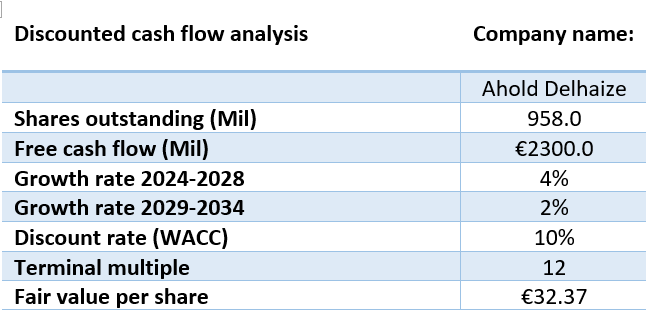

For the valuation of Ahold discounted cash flow analysis was used. I my opinion this valuation model fits the company quite well. Due to their business model their FCF is more predictable and should lead to lower margins of error in the assumptions.

I used a FCF of €2.3 billion, which is right in the middle of Ahold's own FCF range.

Over the last 6 years the company has managed to grow its FCF per share at a CAGR of 5.5% (Dec 2017-Jan 2023).

{kind=link}

I used a little bit more conservative 5 year growth rate of 4%, and for the 5 years thereafter 2% because it's harder to make accurate assumptions over longer periods of time.

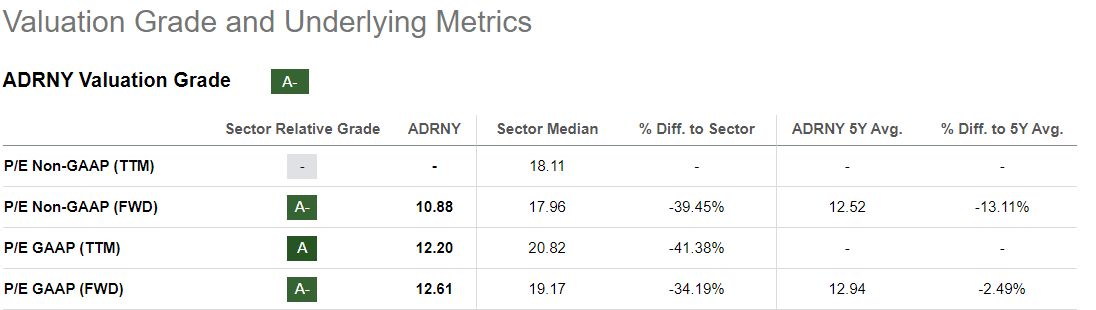

At the moment Ahold is trading at a forward P/E Non-GAAP of 10.88, which is below its own 5Y average.

{kind=link}

I used a terminal multiple of 12, this is also in line with its 5Y average. I fully agree with the A- to A grade when it comes to valuation because of the difference compared to the sector median. In my opinion, Ahold has enough quality to justify a P/E of at least 12.

I applied a discount rate of 10%, because I want this as a minimal annual return on investment.

{kind=link}

If we do the math my calculated fair value is €32.37 per share. This means that Ahold is currently undervalued.

Conclusion

Ahold is a stable business that certainly deserves a place in a well diversified dividend growth portfolio. Don't expect a fast growing company, but at current prices solid returns can be expected in the form of an above-average combination of dividend yield and growth, share buybacks and potential share price appreciation.

Of course, there are also investment risks to consider.

It's the question if Ahold can keep up its margins, which I think they can. However, in the retail food store industry, margins are very thin and that is why a small decrease can make a big difference. I do think persistent inflation isn't a good thing for Ahold and can lead to a reduction in household purchasing power, which could lead to less profitability. It could also mean higher labor, energy and transportation costs, which leads to margin erosion.

The question is also whether Bol can compete with larger companies such as AMZN. M&A as a growth strategy entails certain risks, as it can lead to value destruction in a significant number of cases.

I also will keep an eye on their shareholder distributions compared to total free cash flow. Personally, I don't like companies that leverage up their balance sheet for dividends or share buybacks for long periods of time.

At the moment I don't have shares of Ahold, but at these prices it is likely that I am going to buy shares myself. That's why I give the company a buy rating at current prices.

For further details see:

Ahold Delhaize: A Great Combination Of Dividend Yield And Growth