AHODF - Ahold Delhaize: Significant Outperformance With More Potential

2023-05-01 10:46:28 ET

Summary

- Ahold Delhaize is a non-trivial consumer defensive position for me, and since my latest very bullish stance, I've seen outperformance of over 30% compared to the index.

- I'm updating my thesis for Ahold Delhaize - and telling you that you can still "BUY" the company, but the upside is now less.

- If you didn't buy back in late 2022, or in February, it's worth considering if you're "too late" here.

Dear readers/followers,

Whenever quality defensive stocks go on sale, you should be first in line, buying whatever shares that your allocation rules and strategy allow. That was what I did when Ahold Delhaize (ADRNY) became cheap. I "knew" it would pay off eventually - I just did not expect 30%+ outperformance in as short a time since September of 2022.

ADRNY Outperformance (Seeking Alpha)

Defensive stocks tend to do very well in an environment like this. That was, more or less, what I was counting on when I made that particular investment.

I've already given you my update for early 2023 - now it's time for an update for the later parts of 2023.

Ahold Delhaize is still decent - but the upside is lower

As I mentioned in my last piece, the company has done much better than expected. Double-digit inflation in food prices including producer prices has really put the screws to both producers and vendors to keep food prices down while keeping profits up. In Sweden, we've seen some of the worst consumer defensive/FMCG margin compressions since the GFC, dipping below 4% for some of the major players.

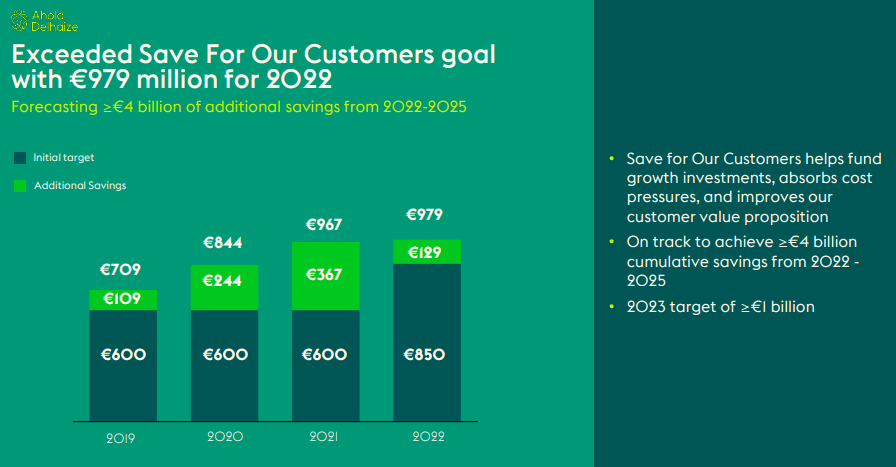

Ahold Delhaize has actually fared far better. The company has managed to keep savings going, including its Save for Our Customers cost savings, and this yielded more than 15% more than expected. Of course, some of those savings were due to higher food prices overall.

Ahold Delhaize IR (Ahold Delhaize IR)

{kind=link}

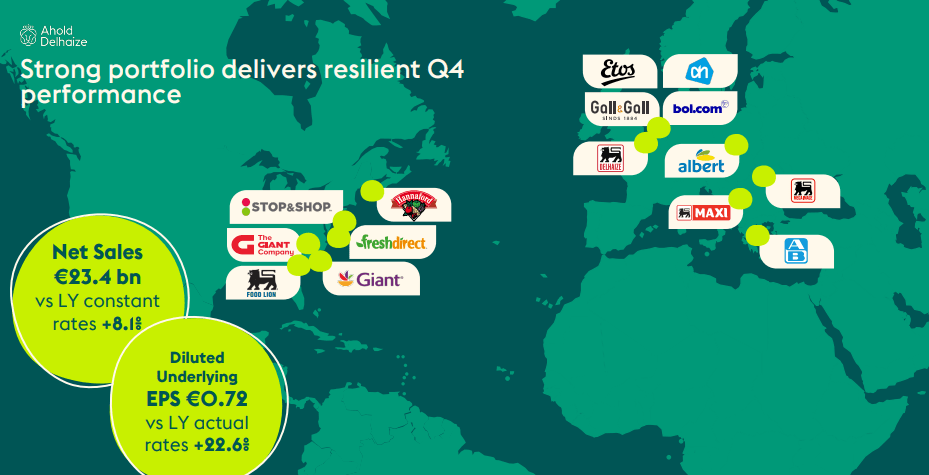

Top-line results were excellent - as expected. 4Q22 are the latest numbers we have. If the 1Q results, due in about 2 weeks, change things considerably, then I will do an update on this article at that time reflecting for those changes. For now, I will work on 4QA results, with expectations and forecasts. For 4Q, that is up 8.1% and almost 7% at constant exchange rates.

Both gas and food sales increased across all of the company's geographies. My expectations for 1Q23 include a retaining of the company's crucial operating margin at above 4%, and for underlying EPS to be at or above the YoY levels. I also forecast similar levels of FCF.

Ahold Delhaize IR (Ahold Delhaize IR)

{kind=link}

The company's M.O. is the same as most defensive consumer companies. Keep its margins intact, keep its market share intact, and keep its targets "working" using whatever mix it can. For the last part of 2022, the signals were good. The operating margin was at 4.3%, with an underlying growth rate of 16.5%. The company also announced an improvement in the dividend and more share buybacks. The company's performance was very resilient, with a diluted underlying EPS growth rate of 22.6%.

The company's various brands mostly did well - especially Food Lion, which had an excellent quarter with expansion and the 4th consecutive quarter of positive comparable sales growth. I expect 1Q23 to be the 5th.

Ahold Delhaize IR (Ahold Delhaize)

{kind=link}

The other brands, such as Stop & Shop and Albert Heijn are also doing well - remodeling, CapEx, and increases in market share are delivering good results, and contributing to an excellent annual set of performance indicators. Overall, 2022 was above LY in IFRS-results - double digits in operating income.

A reminder - the company is also the owner of Bol.com, the Europe/Netherland-centric marketplace comparable to Amazon ( AMZN ) here. Advertising revenues here are significant, 43% up YoY. The company's electronics market share is higher than it has been ever before. Company debt is mostly unchanged, but company debt really isn't a significant worry here, as it isn't for most consumer defensive, as long as sales and trends are strong, which is the case for Ahold Delhaize.

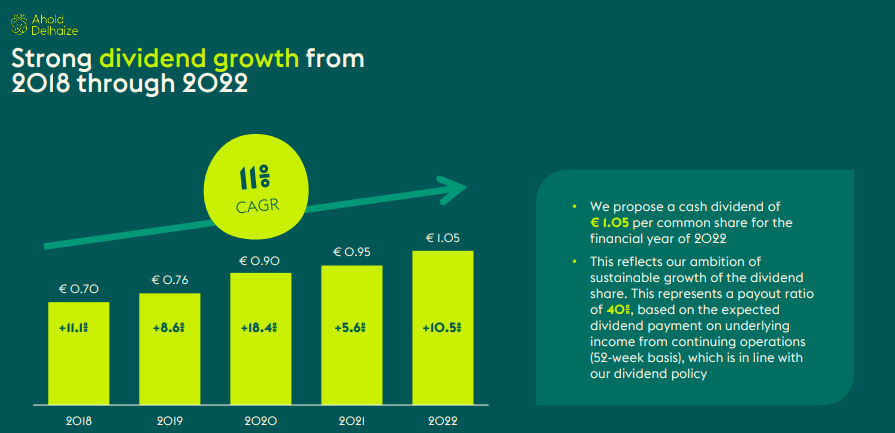

The dividend is a major argument for Ahold Delhaize - it's been growing year after year, outpacing inflation, and delivering solid growth.

Ahold Delhaize IR (Ahold Delhaize IR)

{kind=link}

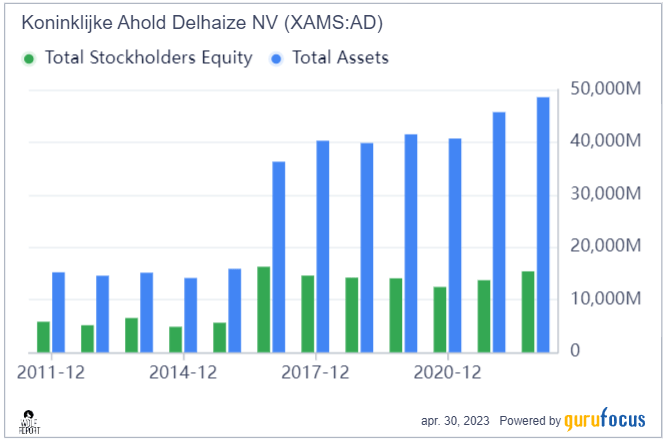

Fundamentally speaking, Ahold is one of the better companies in the entire retail defensive sector. It's definitely above average in every single respect when it comes to profitability. Companies that are objectively better and safer are quite rare. The peer group involves businesses like Kroger ( KR ), Loblaw, Woolworths, Tesco, Coles, Carrefour, and other companies that I've reviewed before.

Ahold Delhaize is one of the more predictable of these companies in the sector, alongside Kroger in terms of the stability of its revenues and earnings. What's more, the company has remained ROIC-profitable net of its WACC for every single year since the GFC. Not a single negative year here. The company has an excellent record of improving equity and assets, delivering solid value.

Ahold Delhaize Equity/assets (GuruFocus)

{kind=link}

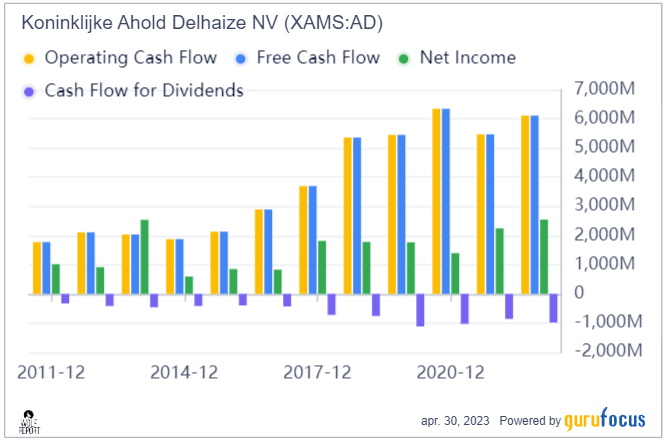

What's more, you can see step-by-step improvements in cash flows. Yes, there is some variance and ups and downs in net income related to the overall market trends and company investments, but the underlying trends are absolutely stellar.

Ahold Delhaize cash flows (GuruFocus)

{kind=link}

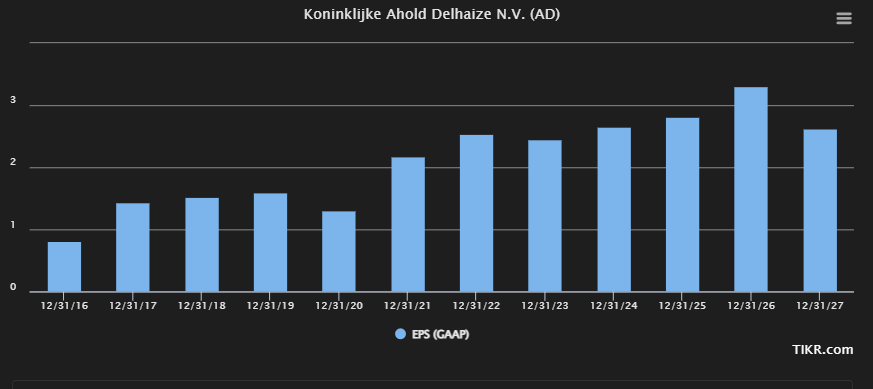

So, the case for Ahold Delhaize in terms of its future potential is unchanged. Working from my current assumptions and forecast models, I'm expecting an improvement to around €2.55/share on a GAAP basis - marginal, only a cent or so, but this is above the overall analyst estimate. I believe the company's margins to be more resilient, and for Bol.com to continue to outperform. Beyond that, I believe the company will continue to slowly grow at 4-6% per year. These are the forecasts from S&P Global.

Ahold Delhaize forecast (TIKR:com)

{kind=link}

The difference to my expectation is that I believe the 2026E target to be too high - I believe in more of a slow growth akin to what we've seen from Ahold. Sudden growth spurts do exist, and declines are extremely rare. One of the only ones over the past decade we've seen was in 2021.

In this case, I want to show you why I believe there is an upside to Ahold even at this point after a 16% RoR, but why I believe that upside is now probably the last chance you have.

Ahold Delhaize Valuation - There's still an upside, but the upside is small

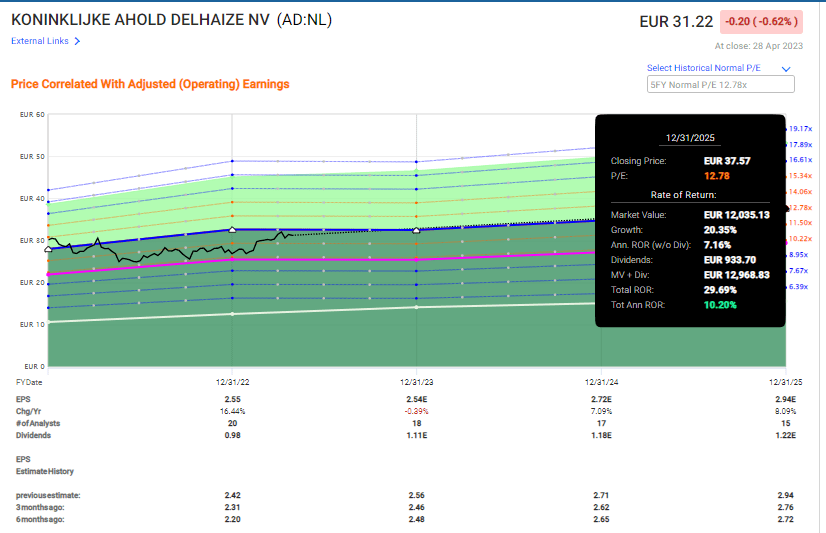

In my last article on Ahold Delhaize, I made it clear that my PT for the company was around €35/share. This is, and was above the S&P Global average which lies around €32.5/share. That's from 17 analysts, of which 12 are at "BUY" or "outperform" here.

That €35/share represents a 12.5x P/E for 2024E based on my current estimates for the company. This might seem bullish for you, but it really only represents the 5-year average for the company. For 2025E, we have double-digit upside at a 12.7x P/E.

Ahold Delhaize Upside (F.A.S.T graphs)

{kind=link}

So let me clearly state that while I do believe that Ahold Delhaize has an upside here, and while I say that there is an upside until that €35/share - and I wouldn't touch my holding until well above that particular target.

These assumptions aren't just based on my or the analyst's forecasts or theoretical appeal levels. A simple DCF with a 3-4% forward growth estimate based on a reverse EPS without NRI gives us an implied FV of €36.8/share in this environment. But the heaviest part of this positive thesis is really how fundamentally safe this company is. How predictable its earnings and cash flows are.

Analyst misses for Ahold Delhaize are rare. They do happen - 17% of the time - but more often, 25% of the time, the company significantly beats estimates. No negative miss from the analyst side has happened since after 2014, which gives some safety here.

As before, I'm not shifting my price target an inch. This is a good example where I believe I've made a superb price target that accurately reflects what the company is worth, and where it could go. This is how I try and calculate my targets. I combine peer averages, historicals, sector trends, forecasts, and fundamentals, and use valuation models like DCF to arrive not only at a PT that I consider to be in the ballpark but long-term indicative.

The only way I even slightly shift my price targets for stocks I invest in is if the company's thesis changes materially - and Ahold hasn't changed for the worse.

No company is risk-free. Ahold Delhaize will never be risk-free. Heck, not even a savings account can be considered "risk-free" in the dictionary meaning of the word. Everything has some risk after all, no matter how remote.

However, the risk for AD is remote - and I believe, comparable to a savings account - only better.

That is why I invest in Ahold Delhaize.

Thesis

My thesis for Ahold Delhaize is the following:

- The company is one of the more appealing EU/US grocery retailers that is trading at what I consider to be a significant discount to conservative multiples. This discount has gone down since my last article.

- I'm keeping my PT and sticking to my "BUY". Despite inflation and SCM issues, I believe the company is one of the best in the entire market to stick to during these troubles, and I believe 4Q22 and what we expect in 1Q23 to be even further proof of just how well the company is managing.

- My PT is €35, and I'm at a "BUY" here.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I can say that this company is a "BUY", but I can no longer call it cheap. This is as high as I would "BUY" the company, and I'm starting to look at other potentials here, as there is a lot of value in the market at this time.

For further details see:

Ahold Delhaize: Significant Outperformance With More Potential