AHODF - Ahold Delhaize: The Cornerstone Of My Portfolio

Summary

- Koninklijke Ahold Delhaize N.V. delivered excellent financial results for its Q4 2022 and FY22, easily beating consensus estimates due to stronger growth and margins.

- Cost-saving initiatives resulted in higher cost savings than previously anticipated, which drove margins in primarily Europe.

- The outlook for Ahold looks solid, and combined with a strong dividend yield and continued buybacks, Ahold stock looks attractive.

- Based on FY23 estimates and a P/E of 14x, I believe Ahold still has over 20% upside potential from current price levels.

- Ahold continues to be the cornerstone of my portfolio due to its low volatility, strong capital returns, and resiliency during economic downturns.

Introduction

Koninklijke Ahold Delhaize N.V. ( ADRNY ) is a multinational owning multiple supermarket chains, online grocery, liquor stores, and European e-commerce company Bol.com, which is an alternative to Amazon. The company consists of a total of 21 different brands and has a presence in over 11 countries in both Europe and the U.S. The company derives close to 60% of its revenue from the U.S. and the remaining 40% from Europe, with most of this coming from The Netherlands and Belgium.

Ahold Delhaize brand portfolio (Ahold Delhaize)

In my initial coverage on Ahold Delhaize, which I recommend reading first if you are unfamiliar with the company, I called it a safe place during uncertain times , as the company functions as a hedge against market volatility due to its anti-cyclical nature and the simple necessity of its products. Also, Ahold has been consistently increasing its revenue, EPS, market share, and presence over the last decade resulting in very steady growth. Ahold manages to consistently keep its margins around 4% and returns solid amounts of cash to shareholders in the form of dividends and share buybacks to increase returns.

As a result, Ahold Delhaize has become a cornerstone in my personal portfolio. I concluded the following back in November when I reviewed the third quarter results:

Ahold remains one of my favorite companies and one of the best recessionary and inflationary picks as proven by their financial results. Ahold continues to grow its top and bottom line and increased the FY22 outlook once again. Ahold is very well positioned to make use of a difficult economy to win extra market share and strengthen its position. Ahold remains a buy for the long-term, but as their market share is increasing and strong growth remains (supported by a stronger dollar), I upgrade Ahold to a strong buy as I think the company is an excellent pick in a difficult environment.

On February 15, 2023, Ahold released its 4Q22 and FY22 results . It managed to beat the consensus quite easily despite increasing its own outlook back in October. Ahold delivered another strong quarter and managed to beat the revenue consensus by €100 million and the net income consensus by €220 million. The beat and strong quarter resulted in a 7% jump in share price when the market opened in Europe. As a result, the stock price increased by over 10% since my previous article on the company, roughly in line with the performance of the S&P 500 (SP500).

Now, let’s see how Ahold Delhaize did over the latest quarter and what the expectations are for FY23. Is ADRNY stock still a strong buy after the latest financial result, outlook, and share price increase?

Let’s dive in!

Quarterly review

CEO Frans Muller was positive about the results and remains confident about 2023, as illustrated by this quote below:

Despite increasing macro-economic and geopolitical challenges, we expect to deliver consistent results in 2023, with a strong focus on cash-flow generation.

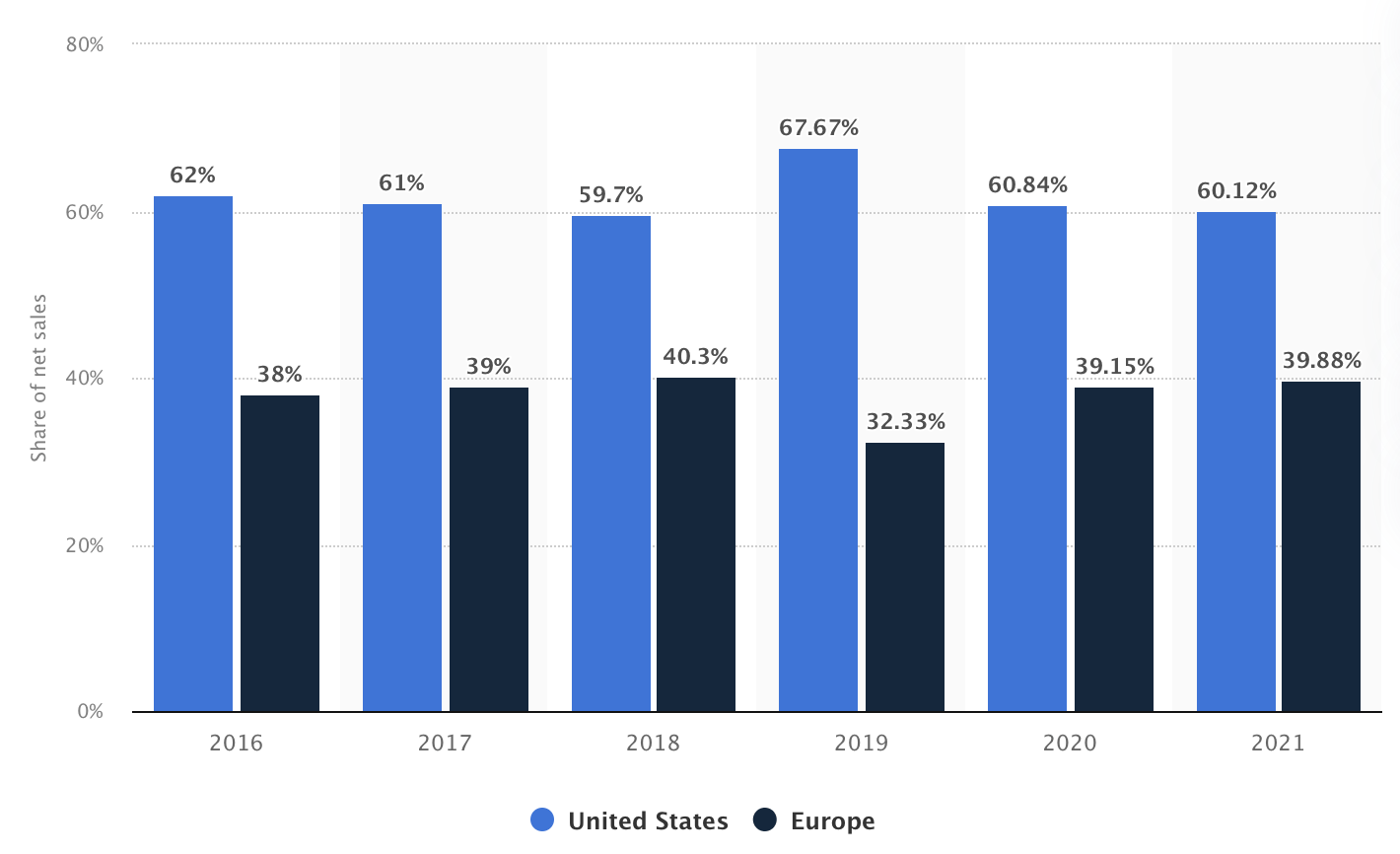

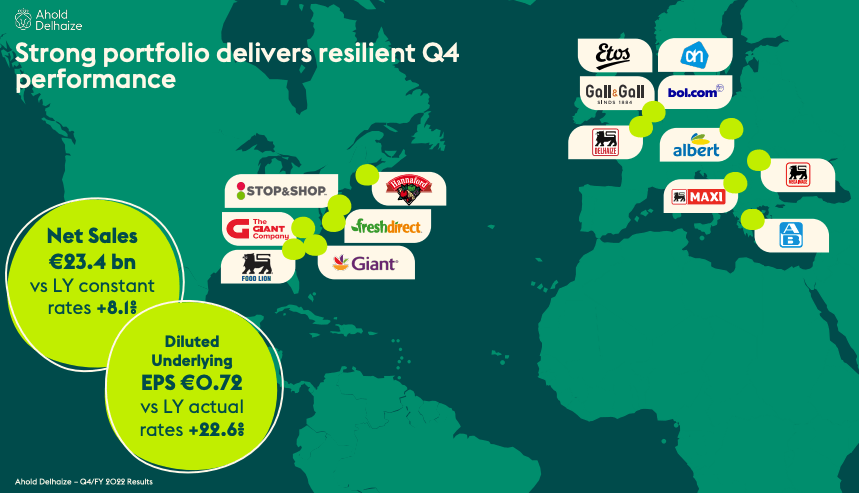

Ahold reported revenue of €23.4 billion for 4Q22 or comparable sales growth of 7.9%. Net sales increased by a rapid 15.9% YoY as Ahold had a significant FX tailwind during FY22, with Ahold deriving most of its revenues from the U.S. while the company reports in euros. With revenue from the U.S. operations coming in at €14.8 billion, this region represents a little over 63% of total revenue. The European business segment saw revenue come in at €8.6 billion and represented close to 37% of revenue.

Revenue split by region (Statista)

{kind=link}

As has been the trend over 2022, the U.S. appeared as the primary growth driver, reporting 9.3% comparable sales growth. Revenue growth accelerated for all U.S. brands compared to 3Q22, which was partially driven by the holiday season activity. Still, this shows the brand strength of all of Ahold’s U.S. brands. To strengthen its brands, Ahold is heavily focusing on loyalty programs, which results in higher online sales and customer loyalty. This is a trend that has been accelerating during 2022, leading to record-high online sales and over 10 billion personalized offers annually.

Growth for the European segment was just 5.7% YoY, coming in quite a bit lower compared to the U.S. Still, excluding bol.com, which is seeing continued headwinds with the drop in e-commerce spending, comparable revenue growth was 6.9%, which is in no way bad for a conservatively operated company such as Ahold. This solid revenue growth is driven by the introduction of more entry-priced products and the expansion of its own-brand offering, which sees higher margins while prices for customers are generally lower.

Ahold continues to see strength across many of its brands in both the U.S. and Europe. Its leading American supermarket brand Food Lion has now achieved 41 consecutive quarters of comparable sales growth and should see its total Food Lion To Go availability increase to over 700 stores in 2023, from 655 in 2022. In Europe, it is the supermarket chain Albert Heijn that is showing strong performance. The Dutch supermarket chain managed to expand its market share last year by 1.3%, to 37%.

{kind=link}

Online sales growth was once again strong, with revenue coming in at €2.5 billion. This 12.4% YoY increase (7.4% on constant currency) was driven by a 17.3% increase in the U.S., which, on top of over 30% growth one year ago, is really impressive. Meanwhile, Europe was flat YoY. Excluding Bol.com, grocery online sales even increased by 14.4% YoY, as the grocery delivery market keeps growing with demand increasing.

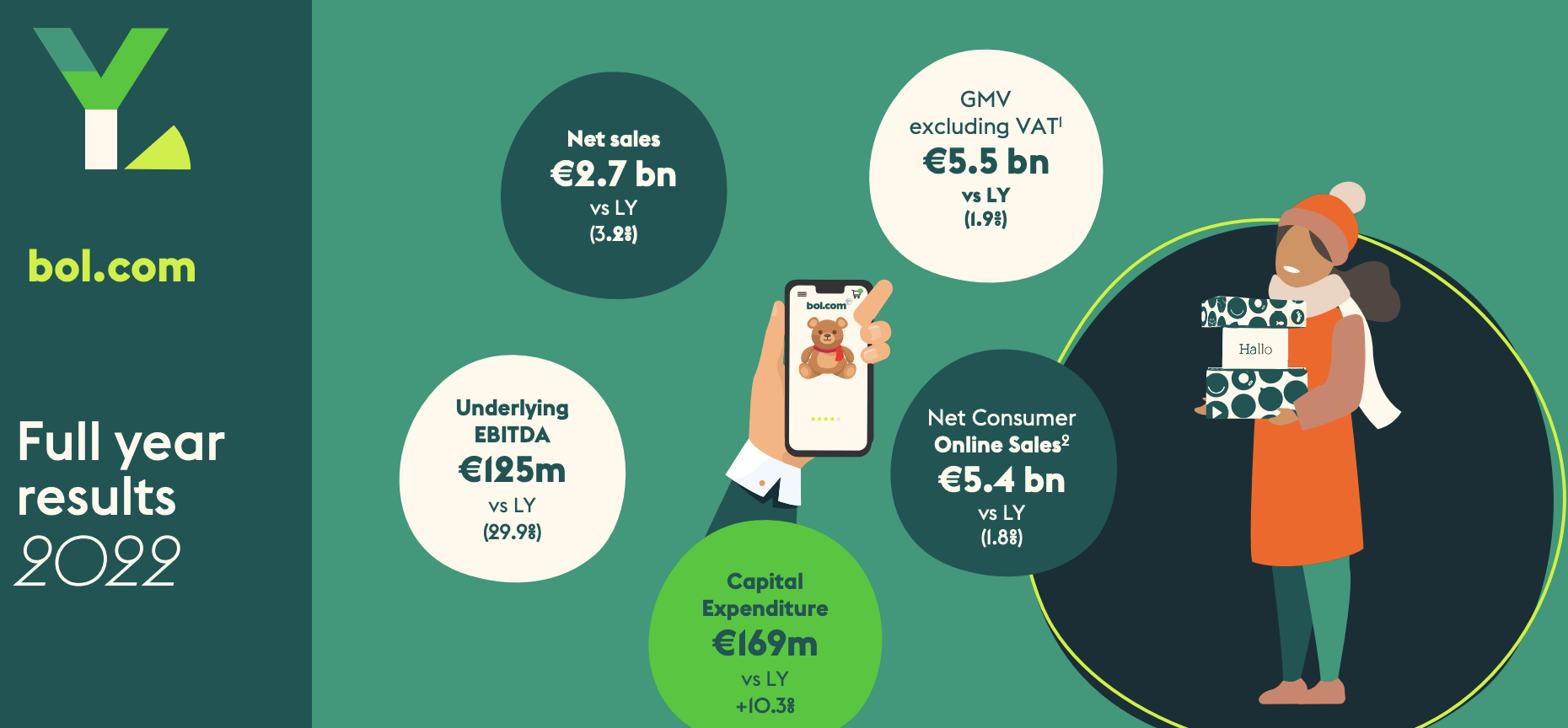

Bol.com is seeing some overall weakness due to the significant decrease in e-commerce activity, as also shown by the international results from Amazon. Bol.com revenue declined by 2.9% YoY and third-party sellers declined by 1.6% and represented 57% of sales. With an EBITDA result of €125 million, the business segment did remain profitable. Also, interestingly, advertisement revenue for the e-commerce platform was up by 43% YoY and could potentially become a solid additional revenue stream.

{kind=link}

The operating margin for 4Q22 was 4.4% and was in line with the FY22 operating margin of 4.3%. As I mentioned in the introduction, Ahold manages to keep its operating margin steady at around 4%, no matter the quality of the economy. U.S. operating margin was 4.7% ( 4.2% consensus ), while the operating margin for the European segment came in at a slightly lower 4% due to a 0.5% impact from high energy prices. Still, the operating margin was much better than the Wall Street consensus of 3.5%, and the strong European margin performance was primarily due to the cost-saving measures taken by management. Overall margin performance by Ahold was really strong and resulted in EPS of €0.72 and increased by 22.6% YoY. Free cash flow for the quarter came in at €1.5 billion, resulting in FY22 free cash flow of €2.2 billion.

Crucial to delivering this solid bottom-line result in a time of extremely high inflation and an energy crisis were the cost-saving initiatives by management. Over FY22, Ahold managed to save close to €1 billion in costs, which is over €100 million more than originally planned.

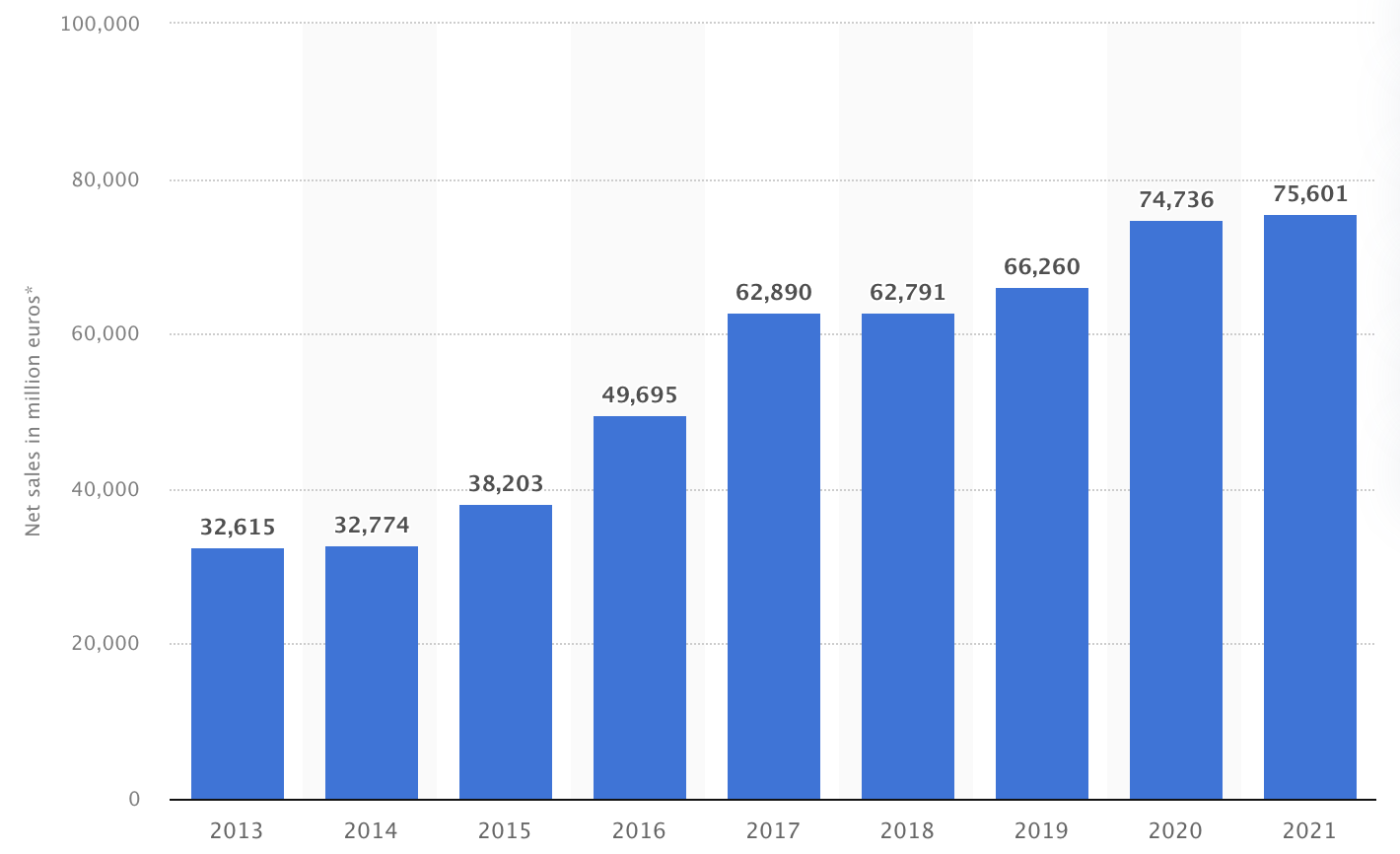

To also summarize the FY22 results quickly, FY22 revenue came in at €87 billion and increased by an impressive 15.1%, or a more reasonable 6.9% on constant exchange rates. Operating income was €3.77 billion with an operating margin of 4.3%. The underlying EPS grew by 16.5% for the full year and came in at €2.55.

Overall, Ahold saw European weakness and margin pressure being offset by strong operating performance in the U.S., resulting in a strong overall performance for both the 4Q22 and FY22. Ahold easily outperformed both the consensus and its own expectations set at the start of FY22. With the company growing by double-digits and the share price declining by around 3% over the last year, ADRNY stock has become cheaper and more attractively priced.

Dividend & Share Repurchases

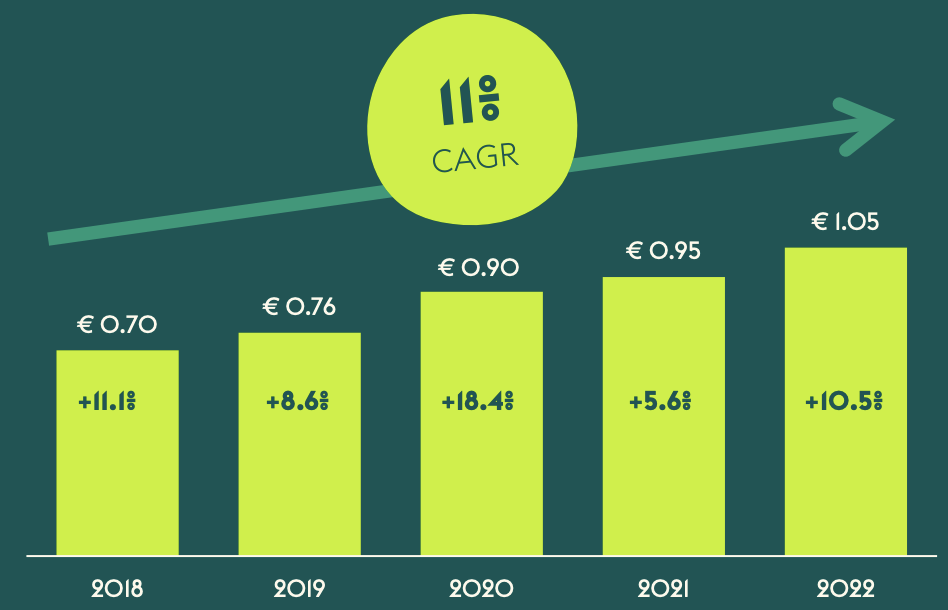

Ahold continues to target a dividend payout ratio of between 40%- 50% of its underlying operating income. It reassesses the dividend every 52-week period and has done so again with the end of FY22. With an underlying income of €2.55 billion generated in the last 52 weeks, management proposed a dividend payout of €1.05, or a 10.5% increase. This brings the dividend payout to just 40% and is still at the low end of the guided range, leaving plenty of upside potential. I believe Ahold is well-positioned for solid dividend growth, and with the dividend growing together with underlying income growth, I believe we should expect a dividend growth rate of approximately 7% over the next 5 years. Based on a share price at the time of writing, this results in a dividend yield of 3,58%.

Ahold Delhaize dividend growth (Ahold Delhaize)

{kind=link}

In addition to the solid dividend, Ahold also continues to buy back its own stock. During 4Q22, the company bought back 10.5 million shares for a total price of €286 million, bringing the total FY22 repurchases to €1 billion. During the 3Q22 earnings release , management already announced a new €1 billion share buyback program, which started on the 1st of January 2023.

Outlook & Valuation

Besides strong financial results over the last year, Ahold management also gave a solid outlook for FY23, although conservative as ever. They expect an underlying operating margin of 4% for FY23, as inflation will remain a challenge for the first 6 months of 2023 and should improve by the second half of the year. A 4% operating margin is slightly lower than the 4.4% the company reported for FY22 but in line with its historical average. Margins should be driven by the cost savings initiative which should result in savings of above €1 billion for FY23. Management expects EPS to be in-line with last year’s EPS of around €2.55 ($2.72). This results in a free cash flow of €2 billion.

(Ahold will supply a more detailed outlook when it releases its Annual Report 2022 on March 3, 2023.)

Analysts currently guide for revenue of €89.6 billion for FY23, or growth of just 3% YoY. The EPS consensus currently stands at €2.46. That growth is not going to be as strong as last year should be no surprise due to the currency tailwinds disappearing for the company. Still, I believe growth will come in slightly higher than these current estimates reflect. In response to the earnings release, Jefferies stated that it believes the analyst consensus for 2023 should go up by at least 5% following the earnings beat. Degroof Petercam also said that they will increase their estimates for FY23 by 6%, while believing the overall consensus will need to increase by 4% to correctly consider the latest results.

This confirms my belief that the current consensus is too low. I believe the current consensus will need to be revised upwards by 6% to correctly reflect the strong performance of Ahold and the high possibility of the company outperforming its own 2023 outlook. This would result in FY23 revenue of €95 billion (9% growth YoY) and EPS of €2.60 (2% growth YoY).

I expect Ahold to keep posting very solid growth for the next several years, as the company is well-positioned through its strong presence in both the U.S. and Europe. Most of its brands hold solid market shares and the company seems to be a frontrunner when it comes to the transition to digital and new ways of getting groceries to customers. I expect this to keep benefitting the multinational over the next couple of years, when the digital transition gets increasingly more important. Also, the ownership (and possible IPO) of Bol.com positions the company well to benefit from the secular e-commerce growth driver.

In addition to strong organic growth, there is also still the opportunity for Ahold to grow through M&A, which will most likely take place in the U.S. as the company tries to strengthen its position there. Although I am not a big fan of risky acquisitions resulting in increased debt levels, this could grow the company into a stronger force. Overall, I expect Ahold to keep growing revenue at a steady pace over the next decade while it increases its position and market share as it has been doing over the previous decade.

Ahold Delhaize revenue growth (Statista)

{kind=link}

Based on these estimates and a current share price of €29.69, Ahold is currently valued at a forward P/E of 11.4. I believe that, considering the low volatility, resiliency, and solid growth prospects of the business, I believe a 14x P/E ratio is fair for this high-quality business. This results in a target price of €36.40 per share, representing a 22.6% upside potential. For ADRNY this results in a target price of $39 (representing a similar upside of 23%) based on an EPS of $2.78.

Ahold looks undervalued, despite the jump following the results, based on its expected earnings, and offers strong upside potential from its current share price.

Conclusion

Ahold continues to execute to perfection and is one of the best-performing companies in its sector. The excellent exposure to both the U.S. and Europe continues to benefit the company, and cost control measures by management drive solid bottom-line growth. The company plans to achieve another €1 billion in cost measures for FY23 and achieve total cost savings of over €4 billion for the period 2022 until 2025.

While Bol.com's performance was disappointing in FY22, we should expect growth to return by the second half of 2023. The overall e-commerce trend is still strong, and Bol.com is well-positioned to benefit in the Benelux. Other factors like consumer loyalty through loyalty programs and the increased roll-out of its own-brand offering will continue to drive revenue growth for the years to come.

With the strong quarterly and FY22 performance, my thesis and thoughts on the company remain unchanged. While one should not expect it to necessarily outperform the market (although it most likely will in a bear market), the resiliency, low volatility, and 4%+ annual capital returns make this an excellent long-term holding.

With Koninklijke Ahold Delhaize N.V. projected to see very steady revenue and EPS growth of between 4% - 8% per annum, and the dividend growing at a similar pace, I believe this company is still a bargain at its current share price. I calculate a price target of €36.40 ($39) per share, leaving investors with over 20% upside potential from current levels.

I, therefore, rate Koninklijke Ahold Delhaize N.V. stock a strong buy at any price below €31 a share, or below a share price of $33 for ADRNY.

For further details see:

Ahold Delhaize: The Cornerstone Of My Portfolio