AAIGF - AIA Group: Doesn't Build Much New Business Has An Unfortunate Reserve Portfolio

2023-03-06 05:37:41 ET

Summary

- VONB margin falls as industry pricing sees the cost side of its economics catching up with policies becoming more competitive.

- With substantial exposure to mainland China, AIA Group's VONB fell, but existing policies carried profits and the bulge of higher margin policies underwritten in 2020-2021 is growing in the mix.

- We are seeing a recovery in China VONB, and the ASEAN markets in general offer areas for greater penetration as well as mean reversion for good income expectations in 2023.

- The valuation could be better though, despite a good secular growth picture, especially when we don't like where they've invested their reserve portfolio and the state of risk-free rates.

AIA Group ( OTCPK:AAGIY ) is a pretty comprehensive insurance stock for the life and health insurance market in the ASEAN countries and China. Valuation is reasonable considering the growth potential since there's a lot of penetration to go in China especially, but also most other ASEAN geographies for L&H insurance. 2022 was a difficult year due to restrictions in China, which limited new business creation, but it is already seeing recovery. We don't love their reserve portfolio, and in general we don't see the need to make bets with these sorts of multiples just for some growth when you can getter more globally optimal deals elsewhere in the markets to outrun rates.

Notes on Performance

Let's start with the H1 before moving onto the Q3.

{kind=link}

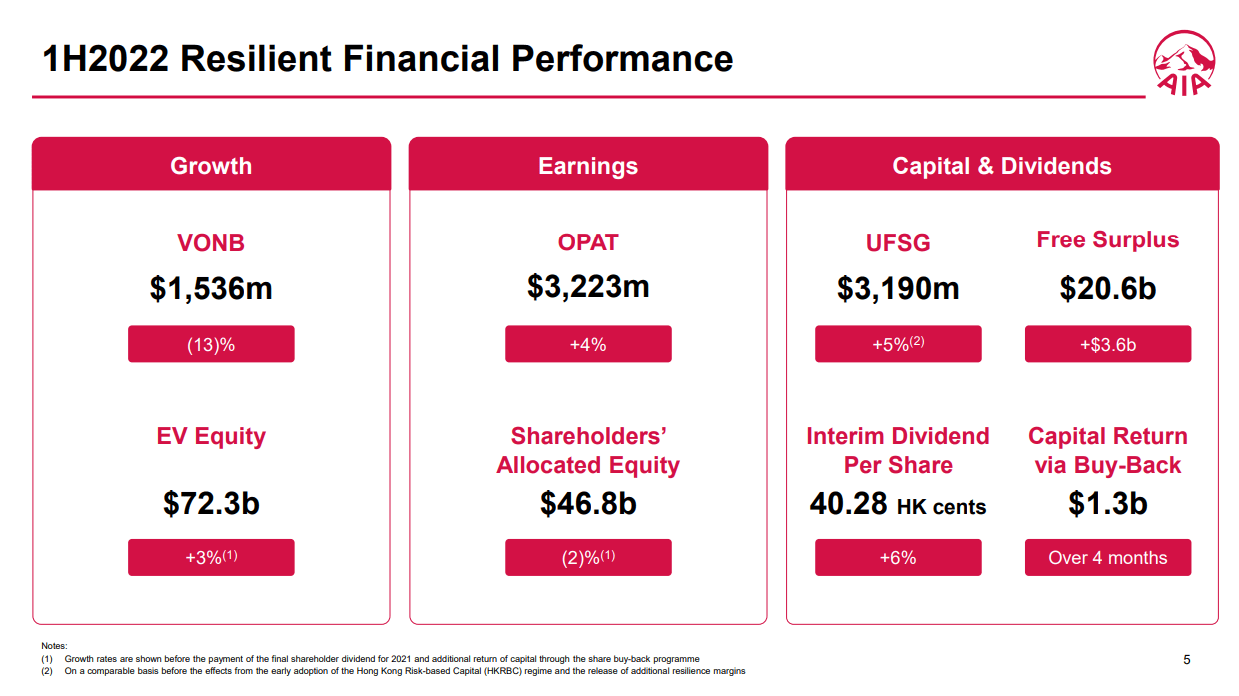

VONB, which stands for value of new business is down due to pressures from severe lockdowns in China. Other markets like India are doing well, it's really only China that is a problem in this regard since their distribution model is affected by lockdowns. Hong Kong was similarly bad, but has already made steps to recovery. The growth in OPAT at around 4% is achieved thanks to the current policies in force, where underwriting growth in 2021 and 2020 at higher margins due to better pricing in the insurance industry is growing in the mix and lifting incomes. New policies being written are actually seeing lower margins, and the margin pressure started somewhere halfway in 2021, so the base effects are no longer noticeable in the Q3 data in terms of VONB margin.

Q3 Highlights (Q3 2022 PR)

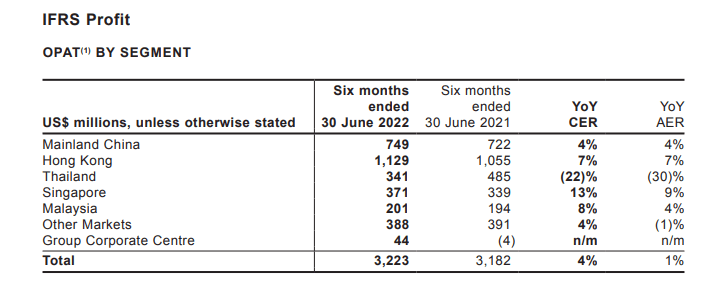

We don't see this as a major threat, just the industry readjusting itself in terms of pricing. Q3 also begins to show that a broader recovery that started in China already in H1, has accelerated with the approach to an end of COVID-zero and the most severe of the lockdowns in Q3, with VONB in China not being as much of a drag on overall results - Shanghai was still bad at this point and other important markets too, but not all of the Chinese markets Moreover, the investment in CPL at the beginning of 2022 has meant some recognized growth inorganically too in new volumes, but the benefits of the acquisition are not going to be realized until its typical distribution model through agencies becomes fully effective again. COVID-zero ended in December so the full effects aren't visible yet.

With policies in force and a recovery in the generation of new businesses, the FY picture is trending up to be able to show some growth, starting clearly in this Q3.

There's also the benefit of Thailand's reversion to the mean. The performance in this pretty important market accounting for about 10% of income was bad due to the use of private hospitals by customers being treated for Omicron. Since that was quite bad wave, we don't see the numbers repeating in 2023. Moreover, there's been VONB growth in Thailand which means that after these high claim levels that geography should return to growth. Claims are falling quarterly quite clearly for Thailand.

{kind=link}

Bottom Line

We think that AIA could get OPAT growth above 10% for the FY 2023 very easily, which explains their run-rate multiple at around 18x in forward PE. While on a relative basis the multiple seems fair, if not decent value, even with the growth we don't think the earnings yield is enough in the current environment. Rates are coming easily up to 6% and will stay for a while there. You need unequivocal value, and betting on growing geographies is not nearly enough to create returns in the current market. Moreover, we don't like the heavy exposure to Chinese fixed income in the reserve portfolio. In a deglobalizing world, such credit exposures can have unexpected geopolitical risks and we don't appreciate that. There's no real yield here either from a dividend perspective, and it doesn't get better enough considering the past buyback tenor.

For further details see:

AIA Group: Doesn't Build Much New Business, Has An Unfortunate Reserve Portfolio