AIF - AIF: A Strong 11.8%-Yielding Loan CEF Performer

2023-11-30 11:15:30 ET

Summary

- The Fed's rate hikes have benefitted loan funds like the Apollo Tactical Income Fund.

- AIF is a diversified credit CEF with a focus on floating-rate first-lien loans and has a current yield of 11.8% and a 12.6% discount.

- The proposed merger between AIF and BDC MidCap Financial Investment Corp. is not attractive for AIF shareholders due to several downsides and increased fees.

The Fed's aggressive series of rate hikes has generated a lot of volatility across markets. One of the few beneficiaries of this development have been loan funds such as the CEF Apollo Tactical Income Fund ( AIF ) which we have held in our High Income Portfolio for a long while now.

In this article, we take a closer look at the fund and, specifically, highlight the recently proposed merger with the BDC MidCap Financial Investment Corp. ( MFIC ). In our view, the proposed merger is not particularly attractive for AIF shareholders.

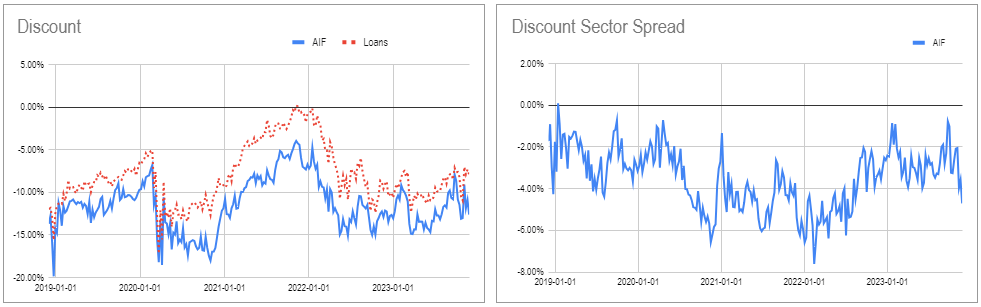

AIF trades at an 11.8% current yield and a 12.6% discount.

Fund Snapshot

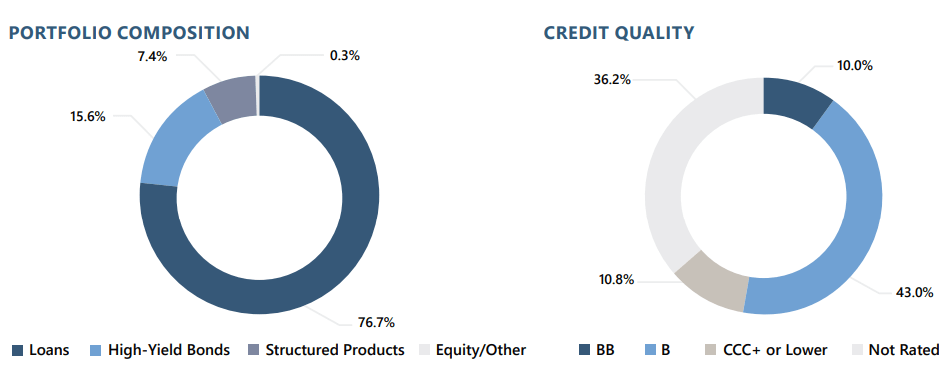

AIF is a diversified credit CEF, with a particular focus on floating-rate first-lien loans which comprise about three-quarters of the portfolio. In addition to loans, the fund holds corporate bonds (16% of the portfolio) as well as CLO Debt securities (7% of the portfolio). These are attractive diversifiers to a loan portfolio and allow the fund to pursue attractive opportunities across a wider spectrum of credit markets.

{kind=link}

The fund's rating profile is concentrated in single-B rated assets with a modest amount of CCC-rated assets. The unrated portion of the portfolio is primarily due to its private credit allocation which, as the chart below shows, has grown to a third of the portfolio.

AIF

This significant private credit allocation is fairly unusual for a loan CEF. However, it does have a couple of benefits for the fund. One, is that private loan valuations tend to be more stable which lessens the risk of a forced deleveraging. And two, private loans tend to trade at higher yields than their public counterparts.

The risk is that private loans are much less liquid which can put some stress on a leveraged fund like AIF if it does need to liquidate some of its portfolio. However, so long as the private credit allocation remains a minority allocation this risk is relatively low.

Top sector allocations of the fund are Technology and Healthcare / Pharma. These sectors are also those favored by BDCs due to their strong historical performance.

AIF

Fund Profile

Given the fund's primarily floating-rate profile, its net investment income has grown over the last few years. The chart below shows annual figures for 2021 and 2022 and the latest annualized available semi-annual figure as of Jun-23.

Systematic Income CEF Tool

It's no surprise then that the fund's distributions have grown since the Fed embarked on its aggressive rate hiking path. The most recent hike brings the distribution to a nearly 50% rise above the trough in 2022. Its current distribution yield is slightly above the median level.

Systematic Income

In terms of performance, AIF has matched or exceeded the broader loan CEF sector across various time horizons in total NAV return terms.

Systematic Income CEF Tool

The fund's historical outperformance is not due to its higher-beta stance, however. Its risk-adjusted performance is one of the best in the sector.

Systematic Income CEF Tool

Moreover, its largest total NAV drawdown is pretty much in line with the sector. This suggests to us that the fund is not just swinging for the fences to generate outperformance.

Systematic Income CEF Tool

Another metric we like is the percentage of years since inception the fund has outperformed the sector in total NAV terms. It is a clear winner here.

Systematic Income

Despite this strong absolute and risk-adjusted performance, its valuation remains cheap, trading at a discount that is 4% wider than the average loan CEF.

{kind=link}

This combination of strong performance and attractive valuation is a key reason why it remains in our High Income Portfolio.

Merger Thoughts

The BDC MidCap Financial Investment Corp. recently announced a proposed merger agreement with AIF and its sister CEF [[AFT]]. The presentation lists a number of benefits such as scale, potentially greater liquidity and a special cash payment of $0.25 (about 2% of current fund prices) to the fund shareholders. Some of the other benefits are more dubious such as research analyst coverage (MFIC is currently covered by several analysts), diversification and "potential operational synergies".

The downsides of the merger are obviously not mentioned which is where we come in. MFIC suggest that AIF investors will gain diversification in the new entity by highlighting that the larger entity will have more companies in the portfolio.

MFIC

However, this is a pro-forma estimate which simply assumes $15m average company exposure for incremental assets. In other words, it's a promise, not a fact. Even if it does happen down the line, it will take a significant amount of time for MFIC to add new borrowers to its currently 150 company portfolio. Each new addition typically requires a lengthy process of due diligence, pricing and negotiating a term sheet. It's not like the company can just buy loans in the market - direct, i.e. private lending is not as streamlined.

Another important point is that diversification is not just about how many companies there are in the portfolio - asset class diversification matters as well. High-yield corporate bonds, which AIF holds but MFIC does not add duration to the portfolio which allows bonds to be more defensive than loans during market meltdowns, all else equal, because interest rates typically fall in these cases. The fund's CLO Debt portfolio is also useful as it does not take principal losses in case of defaults until a certain level of defaults has been reached, which can allow it to outperform linear bond and loan portfolios during "typical" recessions.

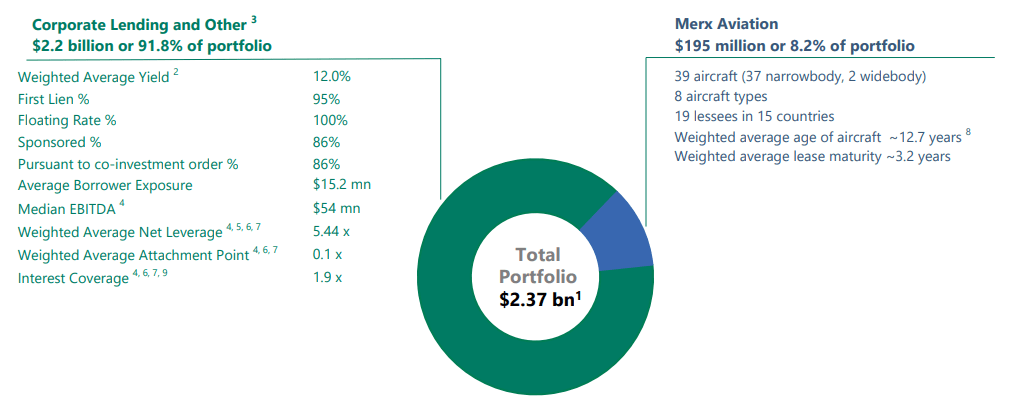

Two, while the MFIC portfolio does have more companies it is also lumpier. This is particularly the case for its legacy position in Merx aviation which soaks up 8.2% of the portfolio (or nearly 20% of net assets). And although it sounds like MFIC will be exiting the position (and it has reduced over time) it will take time (in fact the position increased slightly in the last quarter).

{kind=link}

Finally, we can't ignore the impact of leverage. MFIC carries 2.5x the amount of leverage of AIF (MFIC at 1.44x vs. AIF at 0.57x debt-to-equity). This can be visualized as follows. The sum of the bars are the equity and debt portions that make up AIF and MFIC portfolios which are normalized to be at the same $100 of equity for illustration purposes.

Systematic Income CEF Tool

The consequences of the larger MFIC leverage is that a 1% loss in the portfolio is a larger portion of the NAV than for the lower-leverage AIF portfolio. From a downside perspective this significantly dilutes the greater company exposure of MFIC.

Another consequence of the higher MFIC leverage is that its net income is much less efficient. For example, on 60% of its assets MFIC has to first clear a hurdle of 8.5% (counting interest expense and management fees) before delivering any net income to shareholders, even without counting incentive fees. The same hurdle for AIF is a fee of 7.5% (it has no additional incentive fees) on about 36% of its total assets.

If the merger is consummated, AIF investors will now pay considerably more in fees . At the moment they are paying CEF fees of 1% on total assets for access to a portfolio that has a third allocated to private credit. The management fee will increase to 1.75%, without counting the additional potential incentive fees.

Another important point is that with the merger, AIF investors will go from one of the best loan CEF performers to a sub-par BDC. The following chart shows how MFIC has performed over various time periods in total NAV terms. Only over the last year has it outperformed the sector, and even then fairly marginally. Its longer-term performance has been terrible. It's certainly possible that under new management (recall that MFIC used to be AINV until fairly recently), MFIC may become a strong performer however it will take quite a long time to fully turn over the portfolio it largely acquired by the old team.

Systematic Income CEF Tool

If AIF shareholders really want to be part of a BDC, there are other better BDCs they can choose from, while, at the same time, keeping AIF in existence.

Finally, the AIF discount of 12.6% remains very wide and too wide given its strong performance. The MFIC discount, however, of 13.2% is well deserved in our view. By merging, AIF investors may lose out on potential capital gains from future discount outperformance of the fund.

Overall, we continue to like AIF on its own merits and don't view the proposed merger as an attractive outcome for shareholders.

For further details see:

AIF: A Strong 11.8%-Yielding Loan CEF Performer