AIG - AIG 2024 Outlook: Underwriting Improvement Is In The Valuation (Rating Downgrade)

2024-01-17 04:07:22 ET

Summary

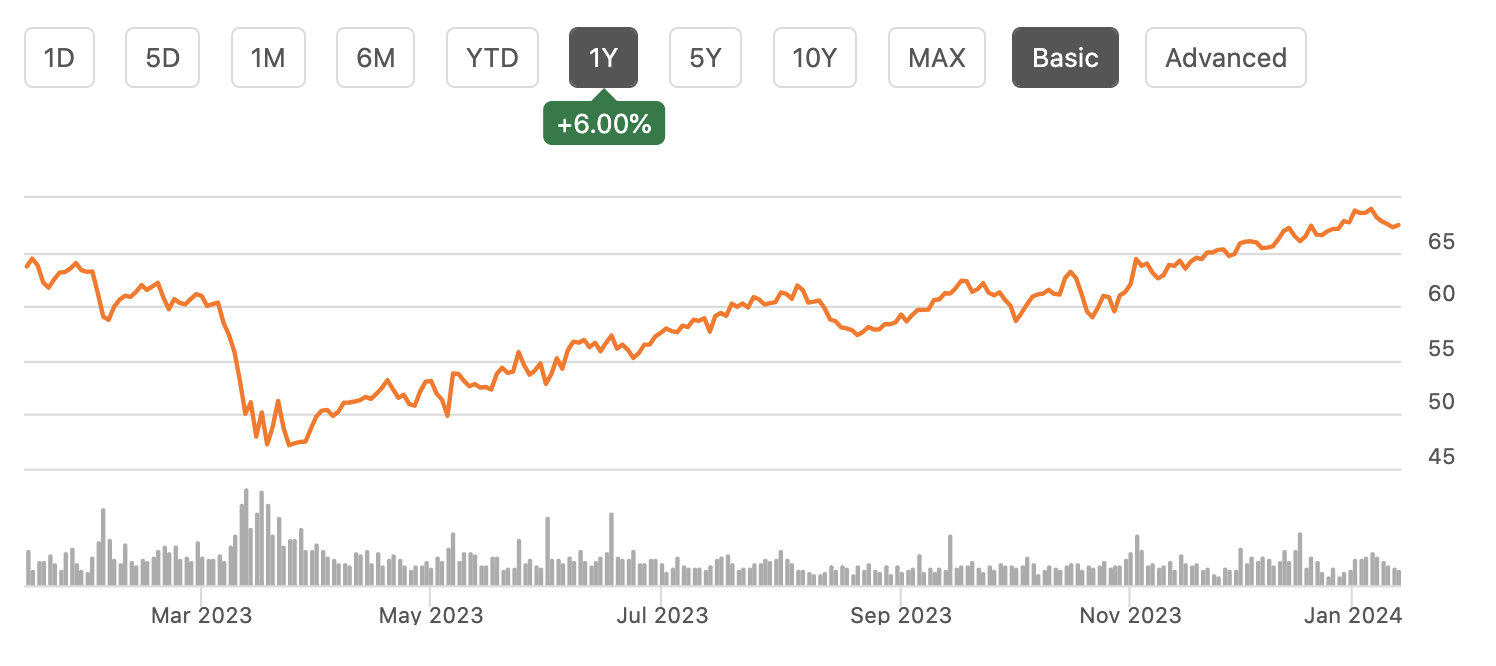

- American International Group shares have steadily risen since April 2023, up over 40% from their lows and up 14% since my buy recommendation.

- AIG's underwriting quality has improved, leading to higher premiums and underwriting income.

- The Company's investment income is expected to remain strong, supported by higher interest rates and positive reinvestment activity.

- At nearly 12x earnings, excluding its Corebridge stake, AIG shares have neared fair value and the upside is limited.

While only up 6% from a year ago, American International Group ( AIG ) shares have been steadily rising since their lows in April 2023 following the regional banking crisis, up over 40% from their lows. Writing about the company in September , I rated AIG a buy, arguing that shares could rally to about $70 over the next twelve months. With shares returning over 14% since then and within 4% of my price target, now is an appropriate time to revisit the stock and consider expectations for 2024.

{kind=link}

In the company's third quarter , it earned $1.62 in adjusted EPS, and the company's $78.17 adjusted book value is up 3% from last year. However, these consolidated results include financials from consolidated subsidiaries. While it has been reducing its stake, AIG still holds 52% of Corebridge Financial (CRBG), its former retirement unit that it spun off via an IPO. That stake is worth about $8 billion today. When examining AIG's financials, I exclude the consolidated results from CRBG, instead valuing AIG on a stand-alone basis and adding back the market value of its CRBG stake. For more details on Corebridge, which I rate a buy, you can read my article on the company from December. This stake is worth about $11/share.

With its "retirement" unit now sitting inside Corebridge, AIG is now a property & casualty insurer with its stand-alone results reported in its "General insurance" reporting unit. My bullish thesis on AIG has been underpinned by its continued improvement in underwriting quality as it has pushed through higher prices and exited some more aggressive strategies. This has continued to play out.

In Q3, general insurance premiums rose by 1% to $6.4 billion, and the firm generated $611 million in underwriting income, up significantly from $168 million last year, leading to a 12.4% return on equity. It adjusted pre-tax income rose by about 75% to $1.37 billion.

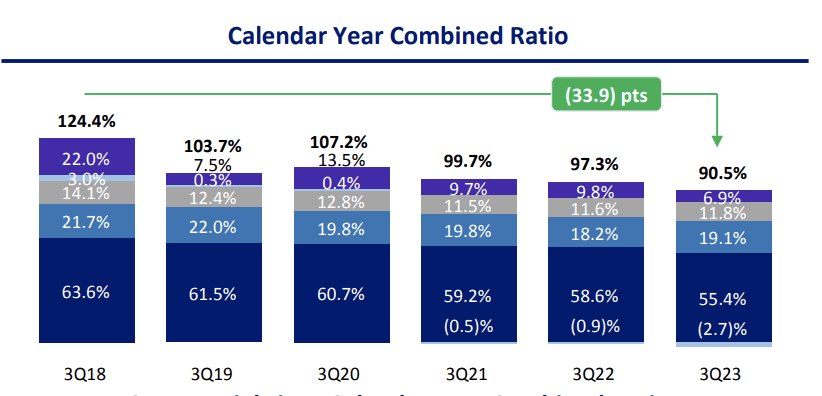

The company's calendar year combined ratio of 90.5% was down from 97.3% last year. As a reminder, an insurer's combined ratio represents its insurance costs relative to premiums, with 100% representing breakeven, so AIG is making about 9.5% on its policies from an underwriting standpoint. Some of this strength was due to favorable catastrophe outcomes with $367 million of losses mainly tied to the Hawaiian wildfires vs $556 million from Hurricane Ian in 2022. While the relatively quiet catastrophe environment flattered results, as you can see below, AIG has been consistently bringing down its combined ratio.

{kind=link}

Now, while AIG continues to make progress on underwriting, results are not yet entirely where they should be. In North America, its commercial business is leading the improvement with a combined ratio of 88.9%. There likely is limited room for improvement here. However, while personal lines continue to improve, they are still loss generative at 113% from 116.4%. AIG's business is concentrated in more lucrative commercial lines, but gradually bringing personal closer to breakeven can help AIG achieve genuinely strong underwriting margins.

Now, catastrophe losses tend to be concentrated in Q3 as that is the peak hurricane season. If we reduce these by 75% (to weigh them evenly across the year and provide a more accurate run-rate earnings picture), AIG generated about $880 million in underwriting income during Q3. Additionally, insurers consistently revalue existing reserves based on how policies are performing relative to their actuarial expectations.

During the quarter, AIG had favorable prior-year developments of $210 million. In other words, policies are performing better than expected. This is consistent with the company's underwriting steadily improving. This action makes me feel more comfortable with the company's reserving and book value; however, such developments should not be considered part of run-rate earnings. Subtracting this out, this $670 million in "run-rate" general insurance underwriting profits is consistent with the high-end of the $2.6-$2.8 billion range I have used to value AIG.

Importantly, I expect 2024 underwriting results to at least maintain current levels of momentum, even though product mix shift may slightly increase the accident year combined ratio in Q4 earnings. The reason I expect 2024 underwriting results to be at least as good as 2023 (barring a major escalation in catastrophes, which are unpredictable year to year) is the lag in inflation. Most insurance premiums are set on a 6-12 month basis. When repair costs rise quickly due to inflation, losses can be higher than modelled, with insurers later trying to recoup these costs by increasing premiums. In 2021-2022, we saw inflation rise considerably, and it has now moderated. However, insurance premiums have lagged and are actually now at 10-year highs. The combination of higher premiums and lower inflation should help to expand insurance margins in 2024.

{kind=link}

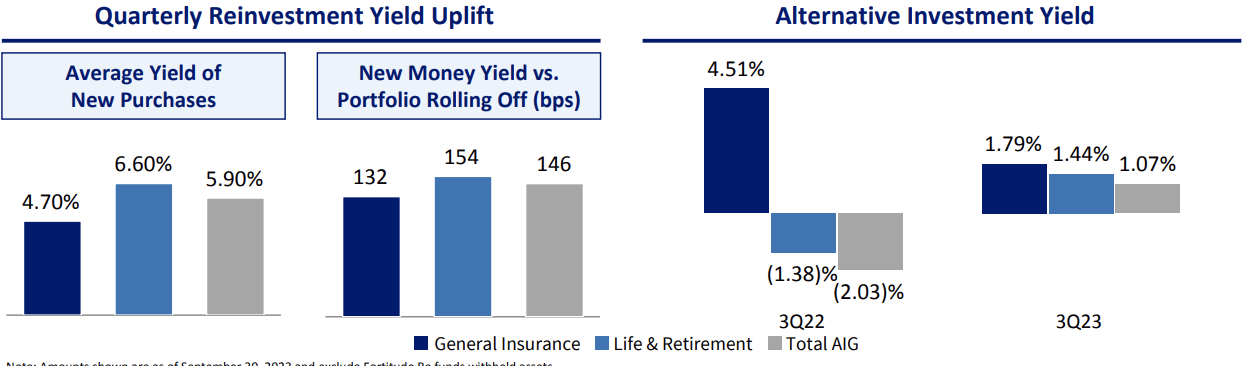

With AIG's underwriting screening leading to improved results, the rate increases and higher customer retention levels it is now generating should support solid underwriting results to continue. Aside from this, AIG has been a beneficiary of higher interest rates as it invests its $77 billion investment portfolio into higher yielding securities. Its investment income of $756 million was up from $582 million last year, consistent with my ~$3 billion forecast run-rate.

AIG delivered this growth despite earning just a 1.8% yield on alternatives. I would expect another poor return in Q4, as alternative investment returns often lag the S&P 500 by about one quarter. The strong recovery we have seen in the stock market in the past two months should provide a tailwind to Q1 and Q2 2024 results. The bigger driver of AIG's investment earnings are interest rates. AIG's portfolio duration is 4.1 years, so substantial portions are rolling off each year and being reinvested. The portfolio yields 3.61%, so even if the Federal Reserve cuts rates several times this year as widely expected, AIG should be able to reinvest maturities at higher yields.

As you can see below, its general insurance unit in Q3 bought bonds at 4.7% on average, about 132bp above maturing securities. Given this reinvestment spread, we should continue to see positive reinvestment activity through 2024, unless the Fed cuts interest rates by over 150bp. While this tailwind should slow, investment income should remain at least $750/quarter in 2024, if not slightly higher.

{kind=link}

AIG's portfolio is also conservative, focused in investment grade corporate and government securities, as well as several billion in cash equivalents. That said, it does have 5% of its portfolio in commercial mortgages with one-third of this sum in office. While office is an area of concern for me, a ~1.7% weighting is quite low. Additionally, there is a 59% weighted average loan to value ratio on its commercial mortgages, meaning property values can fall significantly before AIG suffers losses. While this exposure should be monitored, I do not view it as a material risk.

Finally, AIG's cost reductions continue to take hold with corporate costs of $421 million from $518 million last year. On the balance sheet front, AIG has a 26% debt to adjusted capital, and its insurance company is conservatively capitalized with a 465-475% risk-based capital ratio (being over 400% is the critical level here).

AIG's holding company had $3.6 billion of liquidity as of 9/30. This is the entity that pays dividends and executes share repurchases, a key part of AIG's value story. There were $785 million in repurchases in Q3. Thanks to buybacks, there has been a 5.7% share count reduction over the past year.

Now, subsequent to quarter end, it sold Validus for $3.3 billion in cash and $275 million in RenaissanceRe ( RNR ) stock. This specialty reinsurer was bought to add to AIG's underwriting expertise. On a standalone basis, this deal was a failure because AIG acquired Validus for $5.6 billion in 2018. Now, AIG's own underwriting has improved dramatically since 2018; whether this improvement can be tied to this transaction is hard to know.

Regardless, AIG's parent company liquidity should be over $6 billion when it reports Q4 results. Aided by these proceeds, management aimed to accelerate repurchases in Q4 and into 2024, as well as reduce debt with the goal of completing its $7.5 billion buyback and reducing the share count about 15% . The company should be doing about $1.5 billion in quarterly buybacks, which given these proceeds, continued sales of its Corebridge shares, and dividends from the insurance company to holding company, is sustainable through 2024.

Indeed, the shares' strong performance during Q4 may have been assisted by the increased buying from AIG itself. This repurchase program should help provide a lift to shares. In 2024, I continue to expect about $2.6-$2.8 billion in underwriting pre-tax income and about $3.1 billion in investment income, less $1.7 billion of corporate costs, for run-rate pre-tax earnings of $4.2 billion. Assuming conservatively a year-end 2024 share count of 625 million, that translates to about $4.80-$5 in earnings power by the end of next year.

Interest-rate earning companies like insurers have seen multiples compress as investors fear lower rates will gradually reduce their earnings. Given AIG's 4-year duration and reinvestment spread, this is unlikely to be a material issue unless fed funds is cut below 3%. Nonetheless, I expect this to limit its earnings multiple. At 12x, AIG is worth about $58-60 on a stand-alone basis. Adding back its $11 CRBG stake, and I continue to get a fair value of about $70, or about 90% of book value.

With shares above $67, I believe the majority of the return has been achieved in AIG and am moving shares to a "hold," as they are likely to provide market-like returns. I would view the primary upside risk as being greater personal line underwriting improvement while more dramatic Fed rate cuts would be a downside risk. Rather than own AIG, I believe investors would be better off in its publicly-traded subsidiary, Corebridge, which has ~20% upside to my $28-30 price target.

For further details see:

AIG 2024 Outlook: Underwriting Improvement Is In The Valuation (Rating Downgrade)