AIG - AIG: Strong Top-Line Results Made Us Reaffirm Our Buy Rating

2023-10-05 05:25:30 ET

Summary

- American International Group gets its July buy rating reaffirmed today.

- AIG's strengths point to an attractive valuation, revenue YoY growth, a share price that is a buying opportunity, strong capital levels, and outperforming the S&P 500.

- Its offsetting factors include poor dividend growth and YoY profitability declines.

Analysis Summary

Today I'll be covering American International Group ( AIG ) , in the financials sector, subsector of multi-line insurance.

This is a re-rating after my initial coverage of this stock back in July, at which time I gave it a buy rating . As you can see, I called it correctly because as of the writing of this article the price has gone up 2.20% since then:

AIG - price since last rating (Seeking Alpha)

However, in my re-rating today I used my updated research methodology to see if my outlook has changed in 3 months.

The New York City-based company trades on the NYSE and has roots dating to 1919. It offers insurance products for commercial, institutional, and individual customers in North America and internationally, according to its company profile.

One of its listed peers is Zurich Insurance Group ( ZURVY ).

This time I again gave this stock a buy rating, due to having more strengths in today's review than offsetting factors. In fact, it had 5 strengths vs 2 offsetting factors.

The strengths include valuation, revenue growth, performance vs S&P 500, share price vs moving average, capital and liquidity.

The offsetting factors include dividends, net income and EPS.

A risk to my bullish outlook is exposure to commercial real estate, which has been addressed.

My updated rating methodology as of October 2023 involves analyzing the stock holistically across the following 7 categories of equal weight, and if it has more strengths than offsetting factors it gets a buy rating:

dividends, valuation, revenue growth, net income and EPS, capital and liquidity, share price vs moving average, performance vs S&P 500.

Dividends

Here I will discuss dividend yield , the 10 year dividend growth trend, and dividend stability. As a dividend-focused analyst and investor, I believe these are vital metrics to look at.

Though not all investors are dividend-oriented, and I also appreciate my readers that are not, I think it is an opportunity to generate regular cashflow rather than just holding a stock.

First, let's look at the yield, which is 2.40% as of this article, along with a dividend payout of $0.36 per share, on a quarterly basis.

Before gauging if this is a good yield, let's compare it to the overall industry this company is in. We always want to compare to the same sector and no other sectors, as that would be like apples and oranges.

AIG - div yield (Seeking Alpha)

{kind=link}

In comparison to its sector average, this yield is 41% below the sector average, which does not add confidence to my rating as I am looking for a yield in the 3.5% - 5% range for stocks in this sector.

AIG - div yield vs sector (Seeking Alpha)

The following compares AIG's dividend yield to 3 insurance peers, showing AIG being somewhere in the middle range. In my opinion, it is not terrible but not great either.

AIG - div yield compared to peers (Seeking Alpha)

{kind=link}

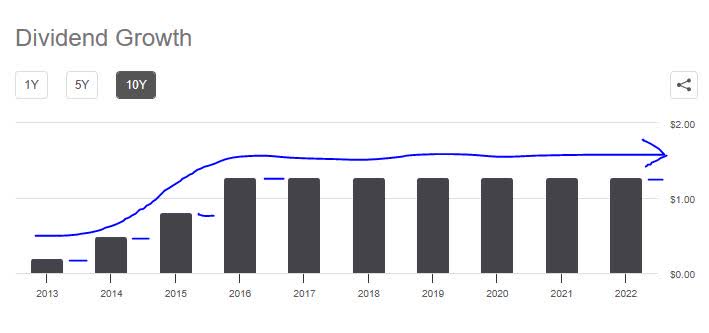

Next, let's look at the 10-year dividend growth rate, shown in the chart below, which shows a trend of no growth for over 6 years. I think that is a negative point and I always look for a good dividend growth story to tell, backed by the data, whereas this story says no growth!

AIG - div 10 yr growth (Seeking Alpha)

{kind=link}

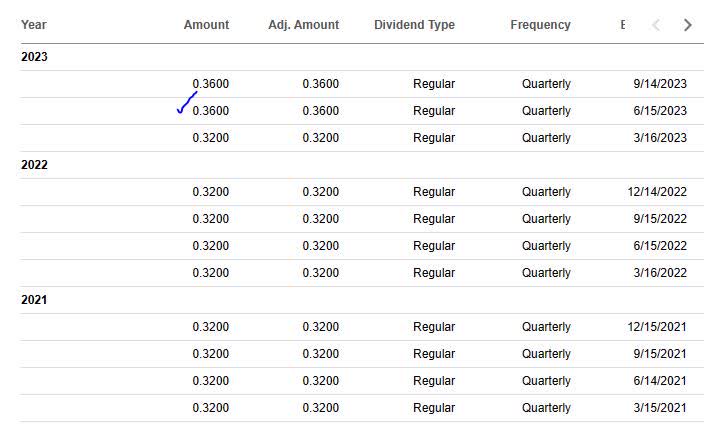

Finally, I want to see dividend stability, in terms of a 2 to 3 year history of uninterrupted payouts, which this stock shows, and it appears to have raised its dividend just 1 time in this period.

If I was holding 1,000 shares, for example, I could realize $360 in quarterly cashflow from the dividends on this stock. (1,000 shares x $0.36 per share).

AIG - dividend stability (Seeking Alpha)

{kind=link}

Based on the evidence, I consider the category of dividends an offsetting factor for this stock, on the basis of steady dividend payouts being overshadowed by little to no dividend growth over 10 years and a yield well below average for this sector.

Valuation

To analyze the valuation , to simplify things I have chosen a single metric to focus on, and that is the price-to-earnings ratio (P/E) , both the trailing and forward P/E, as it tells me what the market is pricing this stock at in relation to its earnings.

Although a lower-than-average fwd P/E may indicate the market is having lower confidence in the forward earnings potential of this stock, it also presents a value-buying opportunity, in my opinion, if most of the other fundamentals are strong.

In the case of AIG, however, it is a case of modest above-average valuation , with the forward price to earnings being almost 12% above the sector average, even though the trailing P/E is only slightly above average.

AIG - PE ratio (Seeking Alpha)

I consider this stock modestly overvalued compared to its industry, both on a trailing and forward basis.

Based on the data, since the valuation is within close range of the average (8x earnings to 11x earnings), I would not necessarily call this one an offsetting factor but it could be considered a strength . Had it been a much higher valuation, such as 12x to 15x earnings, I may consider that too overvalued and therefore an offsetting factor.

Revenue Growth

Now, we've come to a topic I think many analysts and investors look at, which is the top-line revenue growth. Because this metric essentially shows money made before expenses and taxes, it does not indicate this firm's effectiveness at managing costs, but at growing its revenue side of the house.

Manageable growth is important, in my opinion, because companies have competition and are striving to capture market share in their space.

For this company, although the total revenue did see a slight decrease on a YoY basis (about a 6% YoY drop), I want to touch upon the various revenue categories:

AIG - revenue YoY growth (Seeking Alpha)

{kind=link}

Three positives I want to call out is YoY increases in the core business of insurance premiums, income from interest-earning assets, as well as lower YoY losses on sales of assets.

It seems where they took a hit was in "other revenues".

One positive data point I want to call out is that one of its core markets, insurance North America, saw a significant YoY increase in net premiums written. For those readers less familiar with this industry, net premiums written represents how much of the premiums the company gets to keep for assuming risk.

AIG - North America YoY net premiums (company presentation)

Overall, I think that even though total revenue took a slight YoY hit, it was barely a 6% drop and most of this firm's business segments have powered through Q2 successfully. So, in this case, I will make the call that the revenue growth category is a strength towards this stock's overall rating.

Net Income and EPS

Net income and earnings per share get their own section here to make the analysis easier to understand.

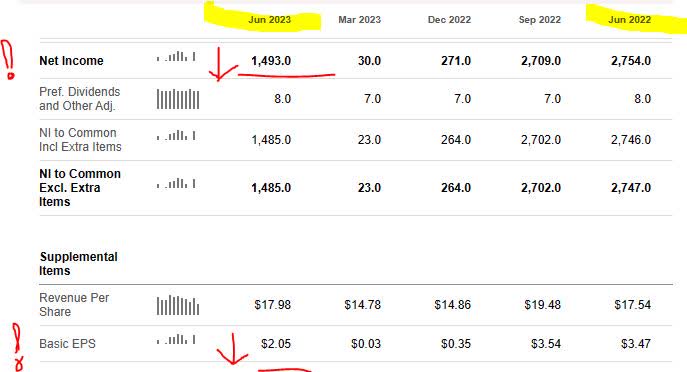

Looking at the most recent quarterly results available, even though most of the top-line revenue figures were excellent, when it came to the bottom line this firm achieved a YoY drop in net income and earnings per share.

AIG - net income & EPS (Seeking Alpha)

{kind=link}

According to the firm's Q2 presentation , "net income attributable to AIG common shareholders of $1.5B decreased 46% compared to $2.7B in 2Q22."

To make sense of the Q2 results, one thing to call out is that operating income was clearly impacted by a significant YoY increase in policy benefits paid out.

AIG - policy benefit costs (Seeking Alpha)

{kind=link}

Another call-out is the significant YoY increase in catastrophe-related charges:

AIG - catastrophe charges (company q2 presentation)

I think this category of net income and EPS is an offsetting factor for this stock's rating.

The perfect storm of claims events seem to have occurred in Q2 with the impacts being felt by this company's bottom line.

The downside of the insurance business, from research into companies lately, is that you cannot always predict certain weather events yet they can have a business impact since the whole point of an insurance policy is to "pass the risk" on from the property owner to the insurance company.

Capital and Liquidity

In this section, we will focus on one or more fundamentals such as whether this company is well-capitalized, has positive equity, positive cashflow, and so on. I think these are important factors to consider and are among the very basics of any serious business.

According to the company's Q2 results : "AIG Parent liquidity of $4.3B at June 30, 2023, compared to $3.9B at March 31, 2023."

In addition, Chairman & CEO Peter Zaffino provided interesting commentary on this topic in his Q2 remarks :

With respect to capital management, we continued to execute against our balanced strategy. In the second quarter, we increased our quarterly common stock dividend by 12.5% to $0.36 per share, representing the first increase since 2016 and we returned $822 million to shareholders through $554 million of AIG common stock repurchases and $268 million of dividends.

Further, from its cashflow statement we can see that the firm has $0.83 in free cashflow per share.

From its balance sheet , the company ended Q2 with $2.2B in cash, $537B in total assets, and $490.6B in total liabilities, leaving $46.4B in positive equity .

Based on the evidence found, I consider this firm's capital and liquidity situation a strength to its overall rating.

Share Price vs Moving Average

My portfolio goal is to look for crossovers below the 200-day moving average that creating value-buying opportunities for a longer-term investor.

First, let's take a look at the price chart as of the writing of this article:

The share price is $59.41 , which is 3.12% above the 200-day SMA of $57.61 . It appears a crossover below the average already occurred this summer, followed by a rebound then a reversal back towards the average.

Using the chart above, I created the following trading simulation where I buy 100 shares at the current price and hold for 1 year, with a goal of achieving an unrealized capital gain at that time of 5% or better.

At the same time, I should anticipate potential drops in share price as well so I have established a maximum loss tolerance: an unrealized capital loss of 20%.

AIG - trading simulation (author analysis)

{kind=link}

In the above simulation, I tested outcomes against two potential future prices, one that is +15% above the current 200-day SMA and one that drops -15% below it.

The outcome is projected capital gains of 11.52% and potential capital losses of 17.58%. Both outcomes are in line with my portfolio goals and loss tolerance.

Based on this simulation, I think the current share price is a strength in my overall rating, and is still within the zone for being a buying opportunity even though the most recent crossover below the average has already passed.

Performance vs S&P 500

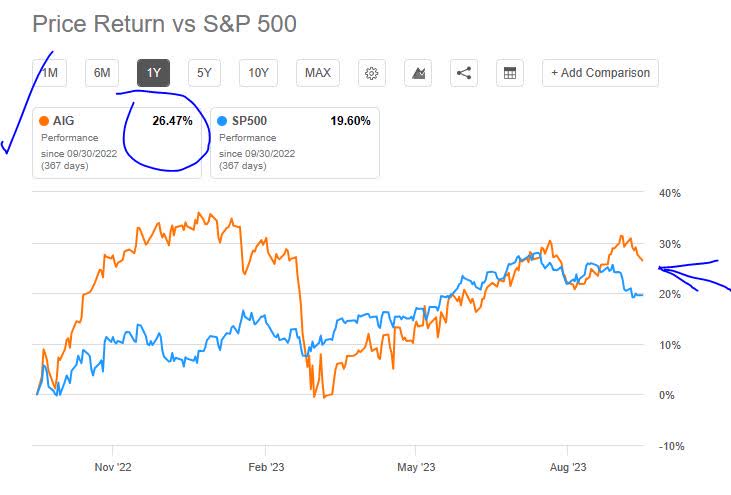

The following is a comparison of the 1-year price performance of this stock vs the S&P 500 index. I have included this metric in my updated rating methodology so as to compare this equity to a major market index that is tracked often, and whether this stock was able to outperform it.

AIG - performance vs S&P500 (Seeking Alpha)

{kind=link}

This data shows the stock outperforming vs this index , which I consider a strength to my rating.

In fact, as the chart shows it has been outperforming vs this index a few times during the year being tracked.

Risk to my Outlook

My bullish outlook faces a downside risk of this company's asset exposure to commercial real estate, particularly mortgage loans on office properties. Due to recent media stories, I think the market could be increasingly bearish on companies with office exposure. My concern is that 26% of AIG's CRE portfolio is tied to office properties, so it is a valid risk concern:

AIG - CRE - office exposure (company Q2 presentation)

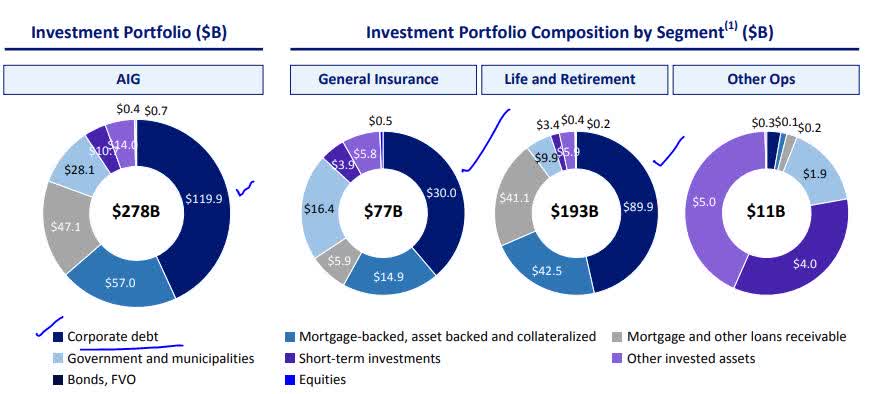

However, my counterargument is that CRE as an asset class makes up a smaller part of the overall asset portfolio at AIG, which appears to be heavily exposed to corporate debt :

AIG - asset portfolio (company Q2 presentation)

{kind=link}

I think that the current interest-rate environment will continue to provide tailwind to its fixed-income holdings that earn interest, along with improving net interest margin, so that should offset the risk of the exposure to office loans.

In closing, my bullish sentiment on this stock remains and I am reaffirming my buy rating from July.

For further details see:

AIG: Strong Top-Line Results Made Us Reaffirm Our Buy Rating