IYW - AIQ ETF: AI's Appeal When Learning From The Dot-Com Bubble

2023-08-12 00:24:23 ET

Summary

- The article discusses the performance of an ETF and attributes its success to the AI driver.

- I aims to assess whether the outperformance relative to the Nasdaq can continue and also addresses the hype around AI.

- The ETF could rise by a further 21% but a correction of around 3% should also be priced in by investors.

- The underlying theme is that a lot can be learned from the Dot Com bubble of 2020.

- AIQ is a buy after considering opportunities and risks as well as using actual figures for market opportunities, productivity gains and potential market correction.

I already covered the Global X Artificial Intelligence & Technology ETF (AIQ) in February this year and was bullish with a price target of $26.3. This forecast has been achieved with the share price currently sitting at around $27.9. However, past performance is not a guarantee for future gains, and, for those who missed the opportunity or others who hold its shares and are wondering whether it is time to sell, this thesis aims to provide an answer.

In this connection, as charted below, AIQ has outperformed the Nasdaq Composite during the last six months thanks to the market enthusiasm around everything relating to AI.

This is the reason why ChatGPT's Generative AI is sometimes likened to hype with some even comparing the present situation to the tech bubble of 2000. This makes it imperative to differentiate between these two market events, before showing how this innovation can positively impact sales and labor productivity and substantiating with figures.

2000's Bubble Vs 2023's AI Appeal

Commonly known as the year 2000 Dot-com bubble, it was a speculative episode in the long history of the stock market that started impacting technology stocks in computing and telecommunications-related sectors in the mid-1990s. The problem at that time was relatively young eCommerce companies like eBay ( EBAY ), Netscape, AOL, and many others with untested business models were seeing their market capitalizations explode to unprecedented levels as a result of investors' enthusiasm for their stocks.

This resulted in the Nasdaq growing by five times from 1995 to 2000, from less than 1,000 to around 4,800 as charted below. By comparison, from 2017 to its 2022 peak, it grew by roughly three times, from around 5,500 to 16,057.

Therefore, there is a significant difference in the percentage of gains provided by the tech-heavy index between the two market events.

Furthermore, in 2000, to finance their growth, tech companies issued large volumes of equity and contracted debt while not generating significant levels of profits or cash. The formation of the bubble was also encouraged by loose monetary conditions with cheap credit widely available, especially from venture capitalists, as well as a global surplus of savings.

Today, it is the contrary, and interest rates remain high amid tight monetary conditions with banks scrutinizing credit-seekers more closely, especially after the March banking turmoil . Also, despite the tech sector earnings likely to experience a deceleration this year as per a May report by Bloomberg, most of them remain profitable with cash positions far better than in the 1990s as illustrated below.

Therefore, unlike 23 years back, when investors mostly based their investment decisions on management promises concerning prospects (or speculation), and venture capitalists looked to dispose of excess cash, today, investors have relatively more conviction as they also have the option of being long cash and harvesting over 4.5% with CD accounts.

Valuing AIQ Amid Opportunities and Risks

Now, the above chart contains only ten of AIQ's holdings, but the ETF holds 87 stocks in total with the first thirteen holdings listed below.

Top 13 holdings (www.globalxetfs.com)

Going deeper, the selection process for inclusion in the underlying fund is based on each one's ability to benefit from the utilization of AI in their product offerings, with the issuer, Global X forecasting the market to surge from $30 billion in 2020 to $300 billion by 2026.

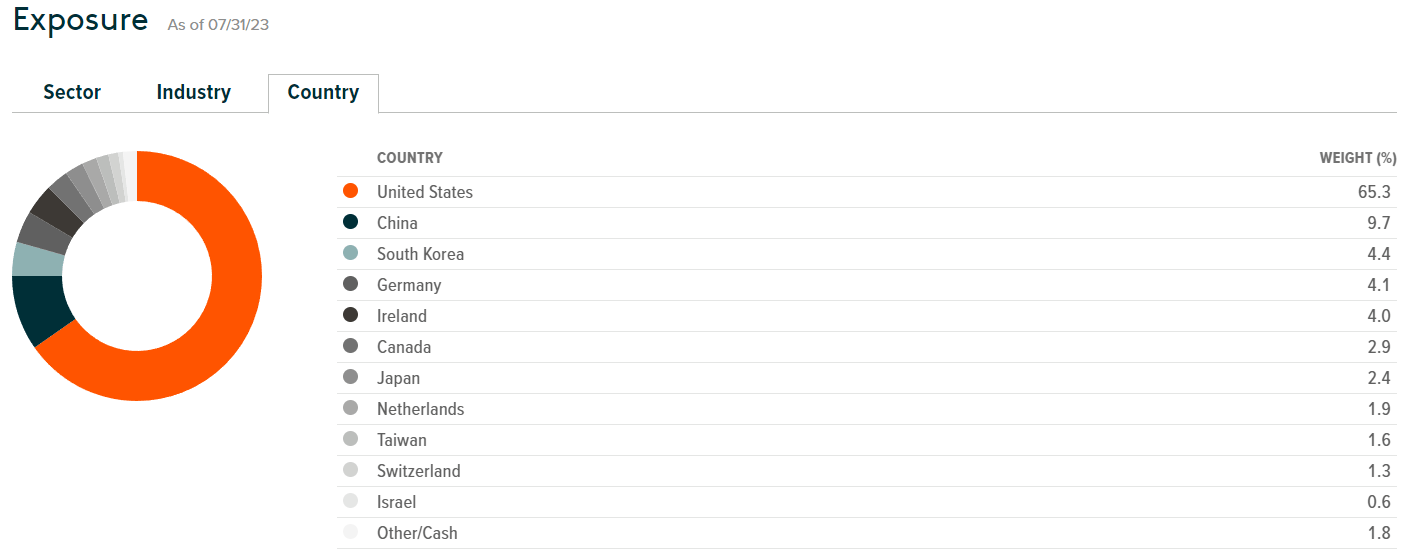

This is a ten-fold increase and assuming that it reverberates across the ETF's holdings through additional sales, it signifies that AIQ which was priced at $18.20 at the start of January 2020 could be valued at $182 by the end of 2026. However, in practice, things are not so straightforward as the market suffers from volatility due to economic cyclicality, inflation, corrections, and geopolitical risks. In this context, with 9.7% of its overall weight dedicated to China as pictured below, AIQ remains more vulnerable to related volatility risks compared to the iShares U.S. Technology ETF ( IYW ) which holds only American stocks.

Country Exposure (www.globalxetfs.com)

{kind=link}

To account for these risks, I consider that AIQ could rise by a modest 2.5 times (instead of ten) to reach $45.5 (18.2 x 2.5) by 2026 as tabled below.

Then, by dividing the difference of $27.3 (45.5-18.2) by 7 to account for the number of years between 2020 and 2026, I have yearly increments of $3.9. Eventually, this adds up to $15.6 (3.9 x 4) after considering that there are four years from the beginning of 2020 to the end of this year. This in turn yields a share price of $33.8 (15.6 + 18.2) for end-2023.

Table Built Using Data from (www.globalxetfs.com)

Well, since this represents a 21.1% gain over the current share price of $27.9, it is a still high number that needs to be further justified and for this purpose, I consider the value add that Generative AI can bring to labor productivity.

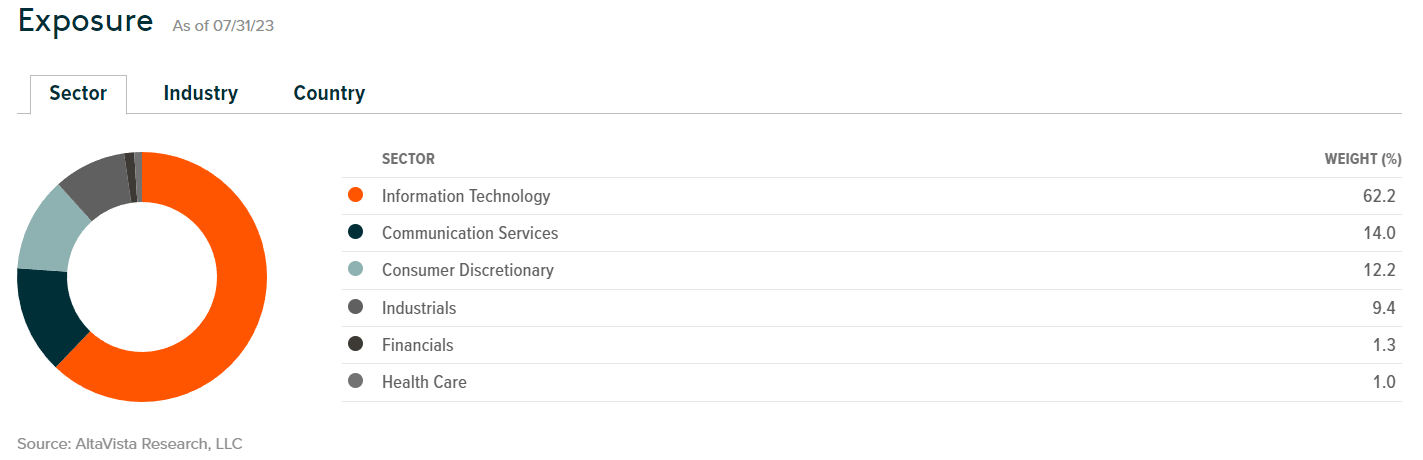

In this respect, after analyzing potential impacts on the workforce, research firm McKinsey has predicted that Generative AI should drive productivity gains of 24% over what is already expected for the 2022-2040 period and across all industry sectors, and, for this matter, AIQ does provide broad exposure as pictured below. Another study by Boston Consulting Group focusing on the conversational aspect of AI puts productivity gains at 30% to 50% .

Sector Exposure (www.globalxetfs.com)

{kind=link}

Still, potential gains will also depend on the pace of AI adoption and the ease with which artificial intelligence (including traditional flavors like Analytics AI) is embedded into existing software to enable a higher degree of automation for manual tasks.

Therefore, based on these two studies by independent research firms, AI is not only about promises and hype but involves real opportunities. However, as innovative technology, in addition to the risks I mentioned earlier, there is also the timing factor.

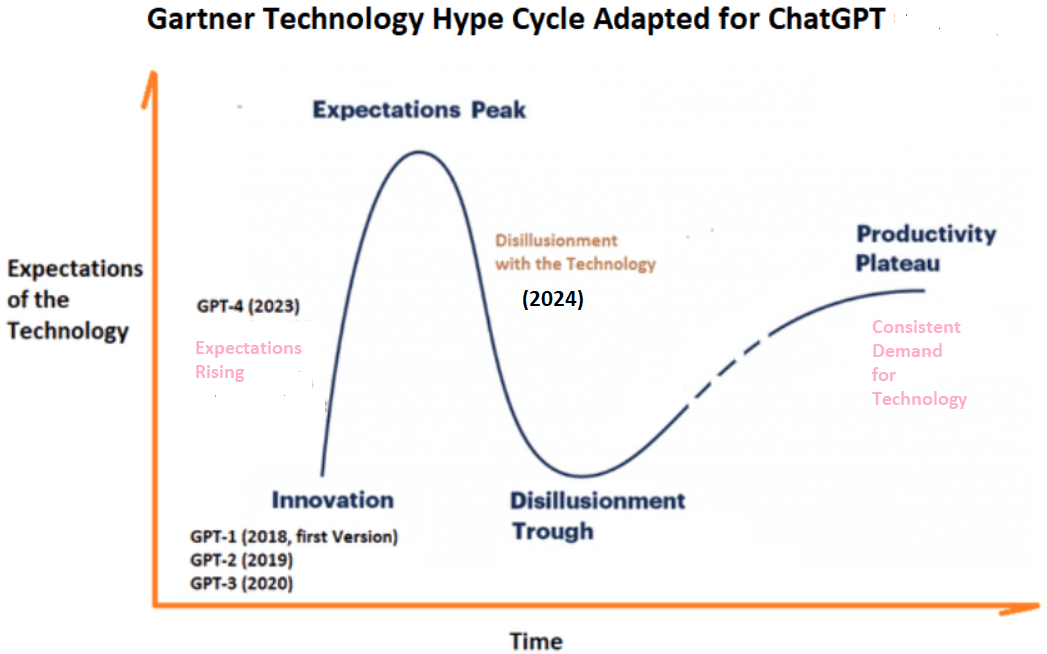

Highlighting Other Risks With Gartner's Hype Cycle

In this respect, one key characteristic of the tech bubble of 2000 is that gains were expected in the short term without much understanding that opportunities offered by new technology like the Internet and eCommerce need time to mature from the development phase till they become commonly used. Thus, while these innovations have surely revolutionized the way business is carried out today, the process took time due to the lag between development in the lab till reaching productivity status in the field.

The same applies to Generative AI today, with ChatGPT initially developed in 2018 by OpenAI as pictured below in the Gartner Technology Hype Cycle developed by researchers aiming to understand how innovations play on expectations with time. Currently, we are at the fourth version (GPT-4) which has witnessed a phenomenal rise in monthly active users.

Gartner Technology Hype Cycle populated using data from (www.techtarget.com)

{kind=link}

Thus, enthralled by its ease of use, namely to generate reports on the fly and through the use of commonly used (natural) language in contrast to complex computer codes which only experts can understand, ChatGPT has been accessed by many. This has resulted in higher demand for related services, enabling Microsoft (NASDAQ: MSFT ) and other public cloud providers to sell more AI-as-a-Service to customers worldwide. Now, to build their infrastructures, these service providers need to source more Nvidia (NASDAQ: NVDA ) GPU chips.

This is about real demand trickling through the tech ecosystem with the semiconductor witnessing 50% more revenues for its second quarter than initially expected by analysts. However, such figures give rise to high expectations as more corporations get a taste of Generative AI, but a peak should be reached as pictured above. I believe that this will possibly occur at the end of this year, but will be followed by disillusionment with the technology as many find that it will not necessarily solve their problems.

As a result, demand for related services and chips should fall in turn inducing volatility in the associated stocks. This should be contagious to tech stocks in general prompting investors to sell.

A Buy After Learning from the Dot-Com Bubble

Still, this will likely be a correction, not the type of market crash seen in 2000. There are three reasons for this. First, the Nasdaq has not appreciated to the same degree in the last five years as I explained earlier. Second, AIQ has been outperforming the Nasdaq by less than 3% in the last year as illustrated in the introductory chart, which means that by itself, the AI factor has produced relatively modest gains. Thus, the ETF could shed about 3% of its value during a correction.

Third, contrary to 2000, this time around, the tech sector is proving to be more agile in its ability to use AI not only to deliver value-added services but also in using the technology to optimize operations and reduce costs. This is evidenced by the more than 150K job cuts announced by tech companies including Meta Platforms ( META ), Google ( GOOG ), Amazon ( AMZN ), and AIQ's other holdings according to a list compiled by Tech Crunch . These cuts should result in better profitability, as much as 24% as per the labor productivity improvement numbers.

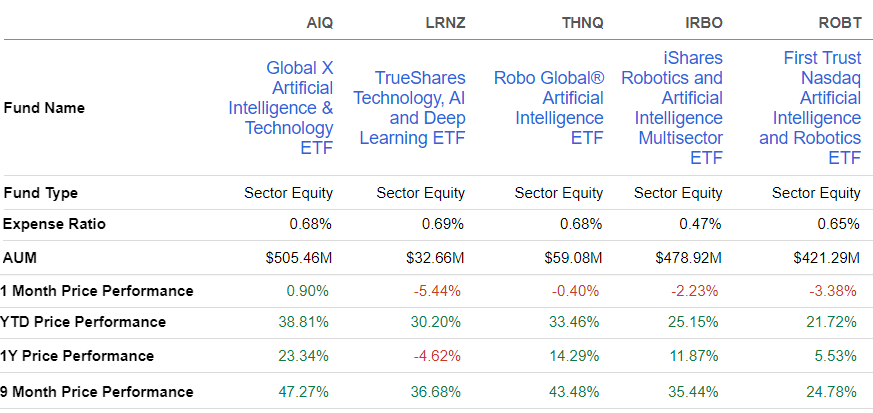

In conclusion, while there should be episodic volatility resulting in a market correction because of high expectations, this thesis has shown that are enough arguments to support an investment case in the Global X ETF at the current juncture. Furthermore, the AI driver should continue helping AIQ to outperform the Nasdaq. To further support my bullish position, as an actively managed ETF which charges 0.68%, AIQ has also outperformed other funds in its category during different periods as illustrated below.

Comparison with Peers (seekingalpha.com)

{kind=link}

This makes AIQ a buy with potential gains of 18% to be reaped by the end of 2023, after subtracting a 3% correction from the 21% calculated gains.

Finally, this thesis has also shown that while there are opportunities to sell more AI-embedded products and raise productivity levels, the actual gains will ultimately depend on adoption and, learning from the tech bubble, it may take time before a consistent level of demand is achieved.

Editor's Note: This article was submitted as part of Seeking Alpha's Best AI Ideas investment competition , which runs through August 15. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

AIQ ETF: AI's Appeal When Learning From The Dot-Com Bubble