AC:CC - Air Canada Q1 Review: Record Revenue And Impressive Guidance

2023-05-17 04:58:47 ET

Summary

- Air Canada announced record revenues in their Q1 earnings release, along with improved guidance and a path toward long-term financial stability.

- One week prior, the company announced an increase to their expected EBITDA for 2023, increasing the range by $1Bn, from $2.5-3.5Bn to $3.5-4.5Bn.

- AC:CA's results highlighted strong demand, with advance ticket sales increasing $1Bn from Q1 2022, forecasting a blockbuster summer for travel.

- I am increasing my price target by $1, to $31, as the stock looks primed to rise in the next 12-18 months. All numbers in CAD unless otherwise noted.

Introduction

Air Canada ( AC:CA ) reported its Q1 FY2023 earnings on May 12, 2023, surpassing analysts' expectations on both revenue and profit. The company posted a significant surge in revenues, reaching a Q1 record of $4.9Bn, as nationwide restrictions gradually eased and consumers utilized accumulated savings to embark on domestic and international travel. Operating expenses rose by 57%, attributed to capacity growth, a rise of approximately 83% in passengers carried, and a 30% increase in jet fuel prices. Despite an operating loss of $17MM, there was notable improvement compared to the $550MM loss in Q1 2022. AC:CA achieved $4MM in net income, marking a $978MM increase from the previous year. Adjusted net loss improved to $188MM, as adjusted CASM improved by 6.9% from Q1 2022. AC:CA reported adjusted EBITDA of $411MM, at a margin of 8.4%. Net cash flows from operating activities and free cash flow experienced substantial growth, increasing by $1.07Bn and $896MM respectively, compared to the Q1 of 2022. The stock soared over 10% on May 4, after updated EBITDA guidance was announced before earnings. Given the updated guidance and strong demand, I foresee AC:CA stock reaching $31 within the next 12 months, fueled by a 10x EV/EBITDA and a swing back to substantial profits.

Highlights

AC:CA had several operational improvements that lead me to believe the best is yet to come from the company. The first key is overarching strength of demand. Advanced bookings surged to $5.3Bn , up $1Bn from last year, an all-time record. Ahead of a busy summer season, there seems to be no letup in demand. Executives also noted on the conference call that new routes to Copenhagen, Toulouse, Brussels, and Amsterdam are meeting or exceeding expectations. The revenue mix was also a welcome surprise, as premium cabin revenues showed impressive growth, accounting for 30% of the total increase in passenger revenues compared to Q1 2022 and 49% compared to Q1 2019. These higher margin volumes will need to continue to grow as the company looks to exponentially increase profits. The load factor of 84.8% was stellar, beating estimates and handily beating 2015 to 2019 figures, which averaged 81.4%.

AC:CA also saw Aeroplan hit 7MM members, one year ahead of their 2024 estimate. This comes on the heels of a new Chase Aeroplan credit card offering for Americans, as penetration south of the border continues to improve. With $10.5Bn on the books, and an emphasis on deleveraging, the balance sheet is also finally in a position to improve. Canadian passengers volume is still lagging 8% below 2019 levels, so this tailwind will be interesting to track heading into a busy summer season.

{kind=link}

Risks

Cost inflation will remain a significant challenge for the airline industry, affecting unit costs. This issue is not specific to AC:CA, and there is less concern about the increased adjusted cost per available seat mile (CASM) targets after the recent guidance. However, it will be important to keep an eye on WestJet's ( ONEX:CA ) pilot compensation negotiations , which remain without a resolution as of May 15. AC:CA will have to engage in negotiations before their collective bargaining agreement expires next year. Additionally, oil prices have remained elevated and higher price will increase CASM outside of the airlines control.

While the company has ample liquidity now, deleveraging will need to remain a focus to achieve significant profits. Analysts grilled executives on interest expenses that remained over $200MM in the quarter. The company previously set a target leverage ratio of ~1.5x by the end of 2024, though the company has not provided an updated outlook for 2024 and the hope is that a push in additional free cash flow compared to previous projections will help them cut into debt, of which ~30% is variable . Sticking to this plan amid unforeseen circumstances and additional capital spend will be important to watch heading forward.

Model Shows Upside

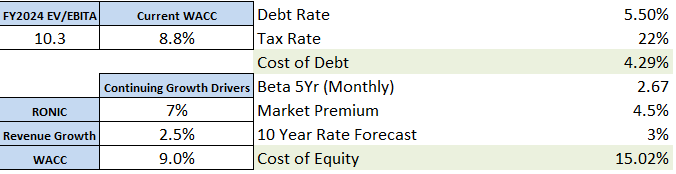

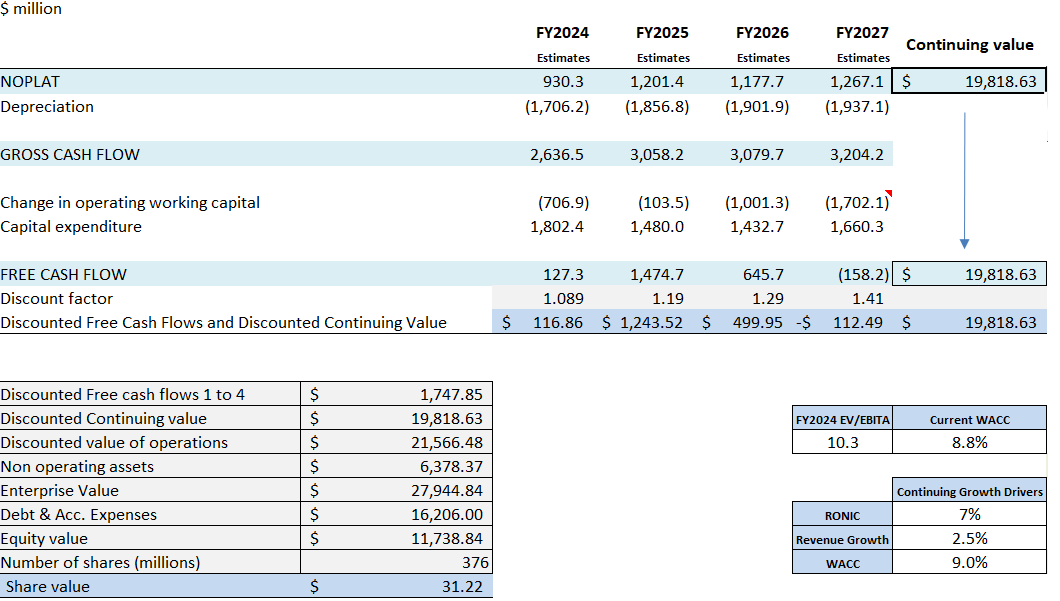

While AC:CA experienced a stagnant stock price in recent months, the company has jumped in the past week after updated guidance and earnings. AC:CA maintains a strong cash position of ~$10.5Bn, which ensures ample liquidity to support its ongoing growth initiatives. According to the model's forecast, the current weighted average cost of capital [WACC] stands at 8.8%, which is high, but manageable if revenues remain strong.

{kind=link}

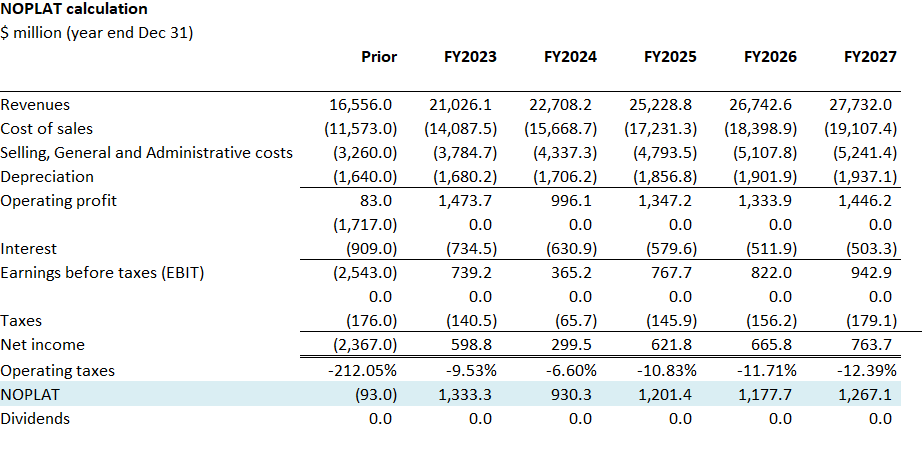

I forecast the continuing value of ~$19.8Bn, given a 25% revenue increase this year and blended revenue growth of ~7% for three years as choppy growth eventually flatlines. I anticipate adjusted EBIDTA next year to hit $3.2Bn, just below the guided range of $3.5Bn-$4Bn. I see margins holding steady into the end of the year and hold other cost ratios mostly in line with guidance, though reduce 2024 estimates after what I expect to be a difficult pilot compensation negotiation. I see the load factor increasing over time toward 83.5%, and available seat miles to hit 91% of 2019 figures. Coupled with a terminal WACC of 9% and a terminal revenue growth rate of 2.5%, a $31 share price (see below) can be supported by fundamentals, but the stock will be volatile.

{kind=link}

{kind=link}

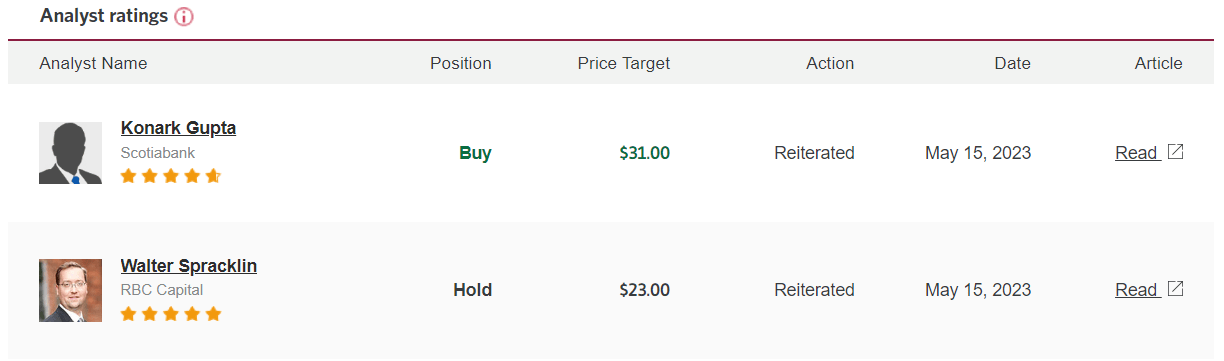

Analysts remain bullish on the stock post-earnings, but there is a significant range.

{kind=link}

Conclusion

AC:CA remains the leader in the Canadian airline industry and is worth a buy at these levels post Q1 earnings release. The company sports robust operations and continues to improve its load ahead of the summer travel season. Management has consistently delivered impressive returns on capital and the company has a history of strong CASM rates compared to top competitors . Despite the volatility of global oil prices, AC:CA shows promising prospects due to its robust demand in domestic and international markets. Keep an eye on advanced booking trends and CATSA passenger data, as these metrics will be important as we approach the summer season. Based on these factors, I forecast a stock price recovery to ~$31 within the next 12-18 months.

For further details see:

Air Canada Q1 Review: Record Revenue And Impressive Guidance