AIQUF - Air Products and Chemicals: Recent Investor Concerns Make It A Top Pick For 2024

2023-12-21 11:59:45 ET

Summary

- Air Products and Chemicals stock price has underperformed due to growing investor concerns over rising costs and project delays.

- These concerns are overdone and enable investors to purchase a high-quality compounder at attractive valuations.

- Air Products will grow much faster than competitors thanks to the ramp-up of recent projects and new projects coming on-stream over the coming years.

In July 2020, Air Products and Chemicals ( APD ) unveiled its clean energy and mega projects strategy with the announcement of the NEOM project . Since then, the stock performance started to lag peers, which put an end to a long period of outperformance. This underperformance results from growing investor concerns about the timing, costs and off-take arrangements of these projects (at what price and to whom the products are sold).

(Source: Bloomberg)

Recent concerns seem overdone

The Covid pandemic brought its share of disruptions in the labor market and global supply-chains, leading to a soar in inflation. The latter has been exacerbated by years of accommodative monetary policies across the world. Within that context, some projects have been delayed while others have faced increasing costs. In February 2023 , the company announced that the total cost of the Neom project will increase from $5bn to $8.5bn. Besides, while originally planned for 2025, the project has been delayed to 2026. The Louisiana project is another example. In November 2023 , the company mentioned that the $4.5bn capex associated to this project will increase to $7bn. As a result, investors are increasingly worried that these cost increases and delays will lead to lower economic returns and will spread across all project backlog.

These concerns are overstated, in our view. Firstly, cost inflation makes up only a portion of these large cost increases. For Neom , cost inflation is $0.5bn out of the $3.5bn total cost increase. Additional project scope (to make the project more self-sufficient and cost efficient), project financing costs due to the use of debt to fund the project (which has the advantage of reducing the initial cash outlay from $1.7bn to $ <0.8bn) and decisions to pay an upfront fee instead of leasing the land for 50 years explain the bulk of this increase. All these costs are brought forward but they will reduce ongoing costs over the coming decades. A similar story happened to the Louisiana project: $1bn out of the $2.5bn total cost increase are related to cost inflation. Project expansion and capitalized interest costs explain the difference. Nevertheless, all projects are not subject to cost inflation and delays. For instance, recent projects such as Jiutai, UNG Uzbekistan and GCA, which came on stream in 2023, have been completed in time and under budget despite supply chain disruptions and COVID-related lockdowns.

Current CEO, Seifi Ghasemi , who has been at the helm of the company since 2014 and built an exceptional operational track record, has confirmed that, despite cost inflation, these projects will still meet the 10% minimum return hurdle (EBIT of $0.10 per year for each dollar of capital invested). In addition, this minimum 10% hurdle does not take into account the benefits from the Inflation Reduction Act. Indeed, in August 2022, the US Inflation Reduction Act passed, which creates tax incentives to produce blue and green hydrogen. It awards a tax credit of up to $3/kg for hydrogen produced in the US. Of course, the tax credit varies depending on the level of greenhouse gas emissions. In that context, green hydrogen from carbon-free renewables would receive the $3/kg tax credit while current blue hydrogen technologies, if they qualify at all, would likely qualify for the lowest credit of $0.60/kg.

More importantly, most projects are expected to deliver returns that are above the 10% threshold. For instance, the return of the $12bn Jazan Project, which is already on stream, is more than 15% . Based on company comments, the New York Green Hydrogen project is expected to return ~18%, excluding IRA benefits. Once adjusted for these benefits, the return is expected to be ~25%. The Texas Green Hydrogen project should deliver similar-type economics. Prior to the announcement of the $2.5 bn additional project costs, the Louisiana blue hydrogen project was expected to return ~27% (including tax credits resulting from CO2 sequestration). Once the IRA benefits are excluded, the return is closer to 17%. Thus, even if cost inflation may act as a headwind, returns will most likely be much higher than the current 10% threshold. For instance, the Louisiana project should still deliver a ~13% return (excluding IRA benefits and assuming $1bn cost inflation and $1.5bn project expansion earning a 10% return) and a ~20% return if tax credits are included in the forecast.

(Source: Company, Barclays and Author)

Concerning the off-take arrangements, the company locks the price of a portion of its future production for de-risking these projects. However, the company thinks differently and prefers to wait for these projects to come on-stream as it believes the value of blue/green hydrogen and ammonia will increase over time due to a supply/demand imbalance.

Well, on that point, I have been very kind of -- very clear about what is our philosophy. We could have signed agreements, long-term agreements for selling that product two years ago. But we always said that we do not want to do that because as we go forward, it is going to become very clear to prospective customers that there are not that many plants or sources of low carbon.

(Source: Company Q4 2023 earnings call)

We have another two years, three years before these plants come on stream. We should not be in a hurry to go and sell this stuff cheap just because that makes everybody feel happy. Our business, our goal, our responsibility is to make as much money as we can for the shareholders. We think the value of these products will become higher as we get closer to where the demand is. There are not that many people who are supplying it. So do not expect for us to come in and make a big announcement about selling this product in the near future, because we are just not going to do that

(Source: Company Q4 2023 earnings call)

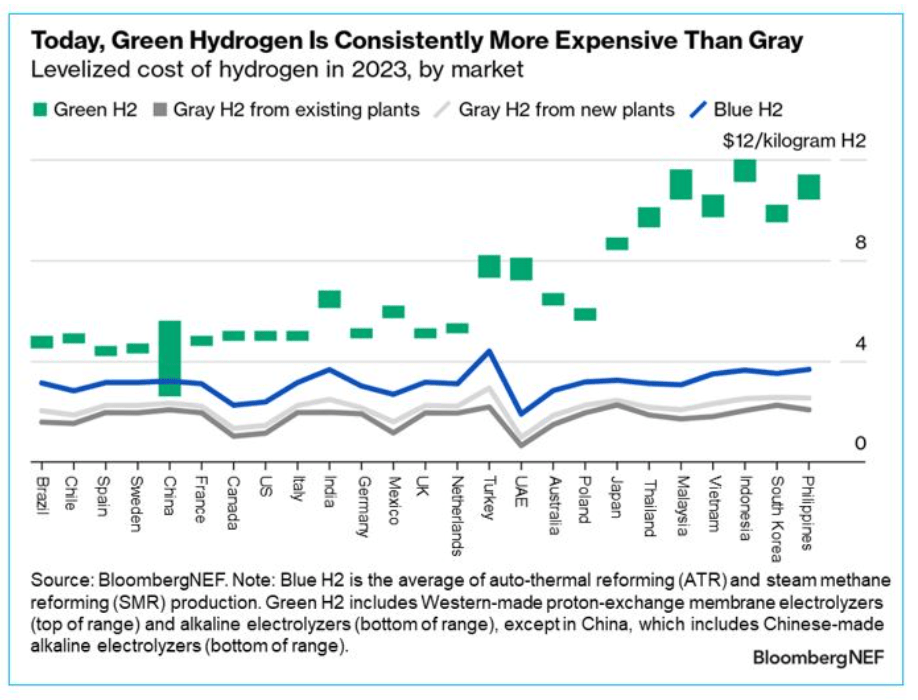

Even though not locking off-take arrangements make the company slightly riskier for the time being, the strategy to maximize shareholder value makes sense and seems to be more a timing-related question than a reflection of fundamental weaknesses. In the US, the cost of gray and blue hydrogen are around $1.50/kg and $2.50/kg while the cost of green hydrogen is closer to $5/kg. With the full IRA benefits, the cost of green hydrogen goes down to roughly $2, which is competitive. As a result, the demand for green hydrogen should not be an issue, especially considering than the green hydrogen economics will improve over time thanks to productivity gains and economies of scale.

{kind=link}

Therefore, we believe the recent concerns offer a compelling opportunity to invest in a high-quality company that will outgrow peers for years and is relatively immune to most macro-economic conditions.

A High-quality company operating in an attractive industry

The industrial gas market is an oligopoly dominated by Linde ( LIN ), L'Air Liquide ( AIQUF ), and Air Products. The industry structure should remain stable going forward as additional consolidation seems highly unlikely and the high barriers to entry should prevent the emergence of new competitors. Indeed, given the importance of industrial gases into clients’ daily operations, clients tend to favor incumbents which have a long history of operations and an outstanding track-record. The use of long-term contracts with high renewal rates, large upfront investments and the need for a dense distribution network further reduce the likelihood of the emergence of new competitors. In addition, even though not immune to the economic cycle, industrial gas companies are very resilient thanks to a combination of contract lengths, take-or-pay and cost pass-through provisions and the time lag for ramping up new projects.

Among peers, Air Products stands out with the highest exposure to the on-site distribution mode (52% while peers are closer to ~25%) and the lowest exposure to packaged gases (13% versus 33% for Linde and 20% Air Liquide, respectively). We believe that the former is the most attractive mode of supply and the key to the business resiliency and visibility while the latter is the least attractive (due to short-term contracts and the lack of specific contract provisions such as cost pass-through or take-or-pay agreements).

(Source: Barclays)

Strong growth prospects regardless of the economic situation

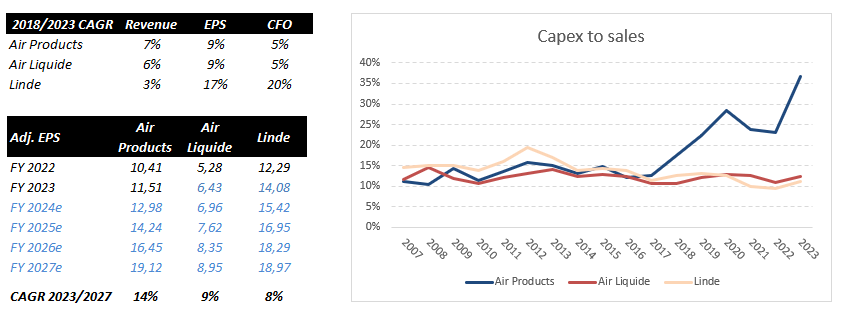

After spending like its peers, Air Products started to increase its investments in 2019 as highlighted by the divergence in the capex to sales ratio. However, these investments have yet to bear fruit. Indeed, despite these investments, the growth of EPS and the cash from operations was in line with Air Liquide over the last five years (the comparison with Linde is more difficult given the synergies resulting from the merger with Praxair). It is also interesting to note that EPS did not benefit from share repurchases because buybacks have been inexistent since 2014.

(Source: Annual reports and Bloomberg consensus)

{kind=link}

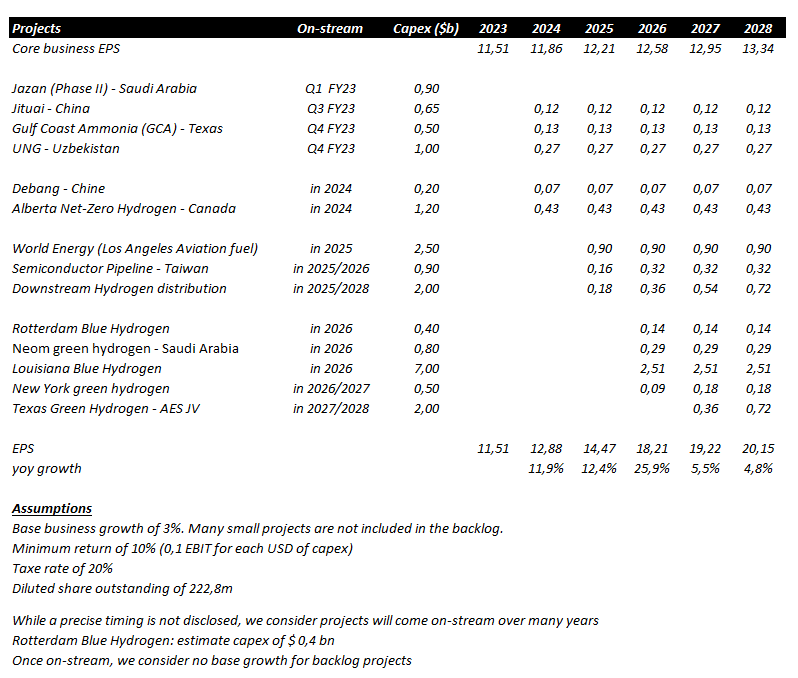

Thanks to these years of investments, Air Products has a bright outlook ahead regardless of macro-economic conditions. Indeed, the $19.4bn backlog (including $15bn related to clean hydrogen and energy transition projects) should support revenue and EPS growth over the coming years.

{kind=link}

As of 2024, the company will benefit from the contribution of the ramp-up of most recent projects ( ~ $ 3bn investments including Jazan, Jiutai, Gulf Coast Ammonia and the Uzbekistan projects…) and from new projects coming on-stream ( ~ $ 2bn investments including Debang and the Alberta projects). As a result, EPS growth will start to accelerate in 2024 and should remain solid afterwards supported by the mega projects coming on stream (Louisiana Blue Hydrogen, New York Green Hydrogen, and the Los Angeles Aviation fuel projects).

Attractive valuation

Air Products is trading at a P/E of 19.9x while peers are trading closer to 25x. The FCF yield metric is misleading given that Air Products has decided to invest much more than peers. Once adjusted for this extra growth capex (assuming a 11.5% capex to sales ratio for all players), the FCF yield is 3%. This 3% level is cheaper than Linde and similar to Air Liquide. Nevertheless, Air Products has the highest exposure to the most attractive on-site distribution method and is growing faster than peers. Therefore, we believe it should trade at a premium valuation.

(Source: Bloomberg and Author)

We believe that the de-rating is now over as the interest rate environment is now more supportive. Besides, the current P/E ratio is close to its long-term average and significantly lower than peers. Finally, we believe earnings growth will start to accelerate, which provides further valuation support.

Going forward, investors should be rewarded by an expected double-digit price appreciation (in line with the EPS growth of >13% CAGR) and a 2.5% dividend yield that will grow over time (The dividend has grown consecutively for more than 40 years). As a result, the expected return should be >15% in 2024 while a valuation multiple rerating could bring additional upside. We believe such return is very compelling for a low-risk and high-quality business with such high visibility.

Conclusion

Recent concerns around the cost, timing and off-take agreements have weighed on the share price. However, we believe these issues do not impact the company's long-term prospects and are short-term in nature. Indeed, the announcement of an off-take agreement prior to the project start has no impact on company valuation while a 12-month delay on a 30-year project has a very negligible impact. While cost inflation has an impact on project return, the unexpected benefit of the Inflation Reduction Act will mitigate these headwinds. As a result, we believe the potential reward is very compelling for a low-risk and high-quality business that has strong visibility regardless of macro-economic conditions.

Risks

A main risk is failing to execute projects on time and on budget. In addition to impacting project returns, failing to comply with customer agreements could lead to litigation and impair the company's reputation.

A collapse of ammonia and hydrogen prices would lead to lower project returns.

Customer bankruptcies would have a significant impact on the company's financials given that the production of on-site plants is mainly allocated to one specific customer.

A Slowdown in industrial production would negatively impact the demand for industrial gases.

A rapidly rise in energy costs such as electricity and natural gas could hurt margins in the short-term. Especially, if the pricing of the merchant business fails to catch up.

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Air Products and Chemicals: Recent Investor Concerns Make It A Top Pick For 2024