ABNB - Airbnb: Consensus Estimates Are Too Aggressive Reiterate Underperform

2023-10-03 12:36:39 ET

Summary

- Airbnb, Inc. stock continues to trade at high valuations, despite concerns about increasing competition and diminishing returns on their supply advantage.

- The company has benefited from organic search traffic and has a significant net cash position.

- Wall Street expects continued growth, but consensus estimates look too aggressive.

- Airbnb, Inc. stock is priced for perfection despite the likelihood of disappointment over the long term.

Airbnb, Inc. ( ABNB ) stock continues to trade at rich valuations as Wall Street is too focused on the impressive profit margins. ABNB has benefitted from organic search traffic, giving it a sizable boost to profitability relative to other online travel agencies. ABNB has a significant net cash position, again in stark contrast with direct peers. The company is likely to have some first mover advantage as it will take time for competitors to ramp up supply, but I question the premium being placed on the stock price.

In particular, I expect ABNB to be met with diminishing returns upon increasing its supply advantage and view it to be just a matter of time before competitors catch up in this respect. The stock is not so ridiculously valued to justify a short position, but it appears quite dangerous given that the close competitors trade at steep discounts in valuation. I expect the stock to underperform the broader market over the long term.

ABNB Stock Price

ABNB stock recently traded near 52-week highs, perhaps bolstered by news that it was added to the S&P 500 Index (SP500), but also possibly due to the mathematical fact that all-time highs were reached more than a year prior.

I last covered ABNB in July, where I explained why I was downgrading the stock from “buy” to “hold.” With bookings growth continue to moderate, I see little reason to change my view.

ABNB Stock Key Metrics

In its most recent quarter , ABNB delivered 18% YoY revenue growth to $2.484 billion, ahead of guidance for $2.45 billion. Revenue growth , shown below, has decelerated rapidly after the company benefited from pent-up demand in 2022, but that 18% mark remains impressive, all things considered.

2023 Q2 Shareholder Letter

Unlike in 2021 where ABNB benefited from strong growth in average daily rates ("ADR"), ABNB has seen ADR flatline over the past several quarters. Management stated that this was in part due to more guests venturing into urban and geographies with lower ADRs, which offset higher prices from hosts.

2023 Q2 Shareholder Letter

Even as many tech companies have taken advantage of the macro environment to make progress on profitability, ABNB still remains one of the more profitable names in the sector. ABNB generated $650 million of net income in the quarter, making up 26% of revenue. ABNB underwent its own cash flow transformation during the pandemic.

2023 Q2 Shareholder Letter

Due to many guests pre-paying for future stays, ABNB once again delivered free cash flow in excess of net income.

2023 Q2 Shareholder Letter

ABNB ended the quarter with $10.4 billion of cash and $9.1 billion of funds held on behalf of guests versus no debt. The company repurchased $500 million of stock in the quarter, and I wouldn’t be surprised to see the company continue to repurchase stock moving forward (even though I have doubts whether this use of cash is optimal).

Looking ahead, management expects the third quarter to see up to 18% YoY revenue growth to $3.4 billion with a “few points” of benefit from currency exchange tailwinds. Management expects take rates to expand in the third quarter versus the prior year. Management expects growth in booking value to increase sequentially from the 13% rate this past quarter. This is expected to lead to another record in adjusted EBITDA - management now expects the full-year to post an adjusted EBITDA margin higher than that generated in 2022.

On the conference call , management again emphasized growing supply as their top priority, noting that the platform saw 19% YoY growth in active listings. Management again noted that 90% of their traffic is “direct or unpaid,” making ABNB quite unique as other travel platforms have more or less been disrupted by Google Search ( GOOGL ).

Some investors may be wondering why ABNB has not yet rolled out advertising on the platform. Management directly addressed such concerns, noting that advertising is “not one of the most perishable opportunities” and they instead continue to prioritize growing supply. It is not immediately clear to yours truly what perishable means in the context but perhaps the implication is that management views supply growth as being a race for a “winner takes most” kind of market.

Is ABNB Stock A Buy, Sell, or Hold?

Longer term, management continues to see growth of long-term stays as a secular story. Long-term stays of 28 days or more made up 18% of gross nights booked, in-line both sequentially and year-on-year. That said, management notes that their 2023 Summer Release update has led to an increase in searches for monthly stays, potentially signaling an inflection point in the near future. Management offered two underappreciated use cases for long-term stays, that being young people without a family that can work remotely, as well as families that wish to travel in the summer. To this less sophisticated thinker, I’m of the view that normal residential-type stays will likely be the main use case long term.

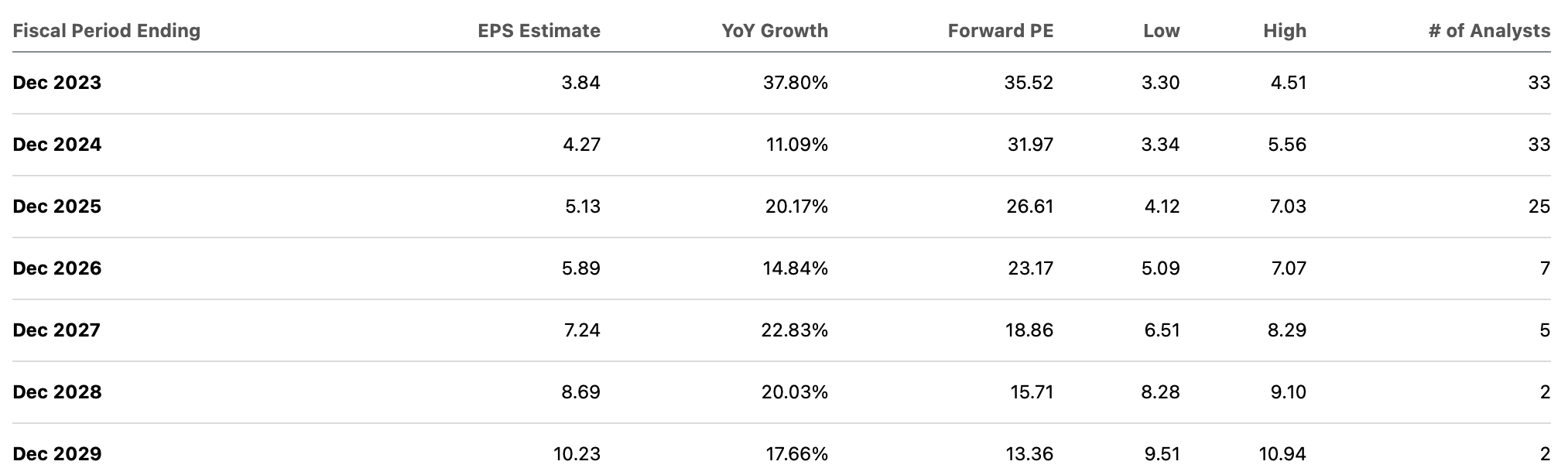

As of recent prices, ABNB traded at just under 36x this year’s earnings.

{kind=link}

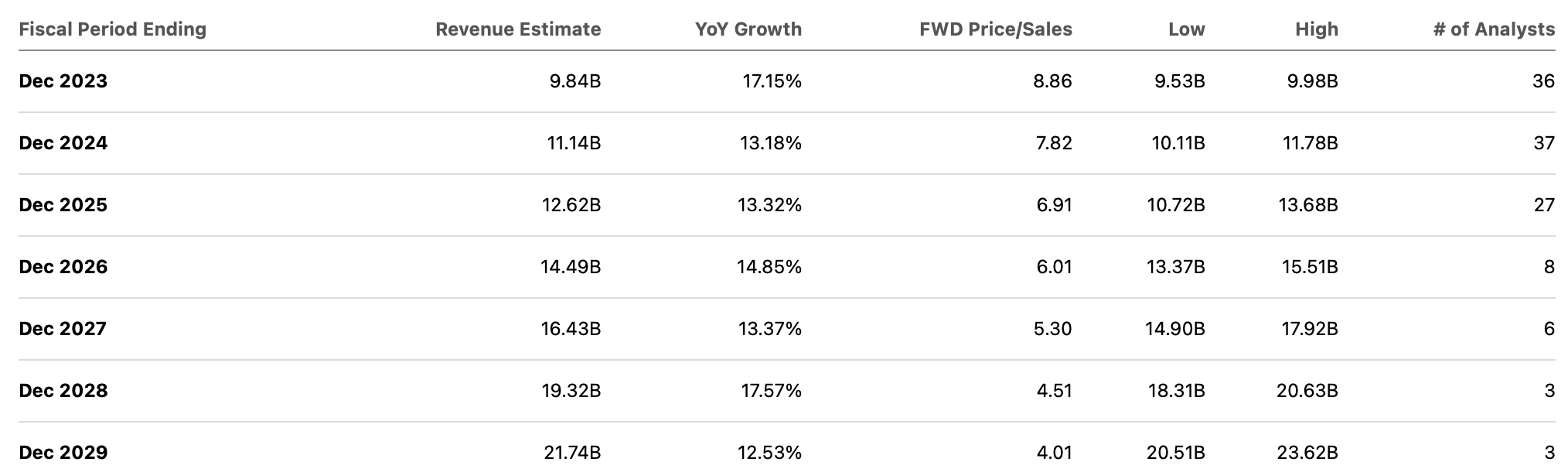

Those with experience investing in the tech sector might not think such a valuation is crazy at first glance, but we must consider that ABNB is trading at 9x sales, which for some might be more telling of overvaluation. In particular, I question whether consensus estimates are too optimistic. Wall Street expects around 13% revenue growth next year, which seems reasonable given that bookings growth stood at 13% in the latest quarter. But consensus estimates call for minimal deceleration in top-line growth in the years following, which seems to defy gravity.

{kind=link}

Perhaps Wall Street shares management’s view that execution on growing supply may help the company sustain its current growth rate for longer than expected. I do not share such a view, as it is akin to implying that users of Google primarily use the site due to having 10 pages of results. Yes, additional supply should offer some benefit to a certain extent, but over the long term it does not address the problem of competition. Having 100 additional listings relative to competitors may not make ABNB more appealing if competition also has 20 available listings for booking. Meanwhile, I expect hosts to list on other platforms. Yes, ABNB has their Airbnb Plus offering which requires hosts using that service to abide by exclusivity agreements . However, this detail does not scale over the long term. If you’ve ever used TSA Precheck at airports, then you’ll understand the issue - as more hosts join the Airbnb Plus offering, its value may diminish, making hosts want to offer their property across more sites.

What about the potential for take rate expansion? Currently, ABNB charges hosts a 3% fee and guests a 14% fee . The guest fee is not too dissimilar from the “resort fee” that travelers have come to love. I am doubtful that ABNB would be able to demand a higher fee from guests, especially as competitive platforms ramp up supply. As for the 3% host fee, I expect that fee to decline over time, as ABNB may need to offer lower fees for its Airbnb Plus hosts to remain exclusive (currently Airbnb Plus hosts pay the same 3% fee). But even if we assume that the overall take rate expands to 20% over time, that still does not explain why ABNB is trading at a noticeably large premium to Expedia ( EXPE ) and Booking Holdings ( BKNG ).

Seeking Alpha

ABNB does have a net cash balance sheet , whereas EXPE and BKNG operate on a leverage neutral basis, but the EV/EBITDA valuation already accounts for that. Given that EXPE and BKNG are already paying “the Google toll” as I like to call it, one can even argue that this premium is undeserved due to ABNB having the most to lose from a margin perspective.

Where does that leave us? With EXPE trading at 9x 2024e earnings and ABNB trading at 11x 2030 earnings, I fear that ABNB presents a large likelihood of being dead money over the next decade. ABNB may be able to offset increasing competition by taking market share away from traditional hotels, but I again am of the view that this is already reflected in the valuation. Between the potential for elevated marketing costs and increasing competition over the long term, I cannot recommend buying ABNB stock at this valuation - I reiterate my neutral rating and expect the stock to underperform the broader market over the long term.

For further details see:

Airbnb: Consensus Estimates Are Too Aggressive, Reiterate Underperform