ABNB - Airbnb: The Advantages Are Unsustainable Look Out Below

2023-12-08 17:20:18 ET

Summary

- ABNB is one of the more expensive tech stocks, but should it be?

- The company has sustained resilient revenue growth and impressive profit margins.

- The company's current competitive advantages are not sustainable long term.

- The valuation looks stretched when factoring in the likelihood that competition will eventually catch up.

Airbnb ( ABNB ) is a fantastic company at the wrong price. I can believe the sentiment that the company can show above-market growth in the near to medium term as it takes lodging market share. The company is highly profitable in large part due to not needing to pay for external advertising. However, I have the view that the home rental market will eventually look a lot like the hotel market: a commoditized market with Alphabet ( GOOGL ) being the gatekeeper. I can not think of any reason why ABNB should be able to defy gravity as its first mover advantage may fade away as competitors catch up. If there’s one thing that has been certain over the last decade, it is that price is an escapable focus from consumers - I am hard pressed to believe that ABNB is somehow different from the rest. As the saying goes, “if it looks like a duck, swims like a duck, and quacks like a duck, then it probably is a duck.” Investors should look beyond the near term advantages and question how innovation can keep the company ahead of the competition. I reiterate my underperform rating as I expect long term margin contraction and multiple compression to offset above-market growth rates.

ABNB Stock Price

ABNB, benefitting from a broader tech rally, is still trading near 52-week highs. That’s surprising given that the company is already showing signs of imminent deceleration.

I last covered ABNB in October where I cautioned that consensus estimates looked too aggressive. In this report I seek to further discuss the multitude of long term headwinds that face the business. It may take a while for the party to end, but you won’t want to be around when it does.

ABNB Stock Key Metrics

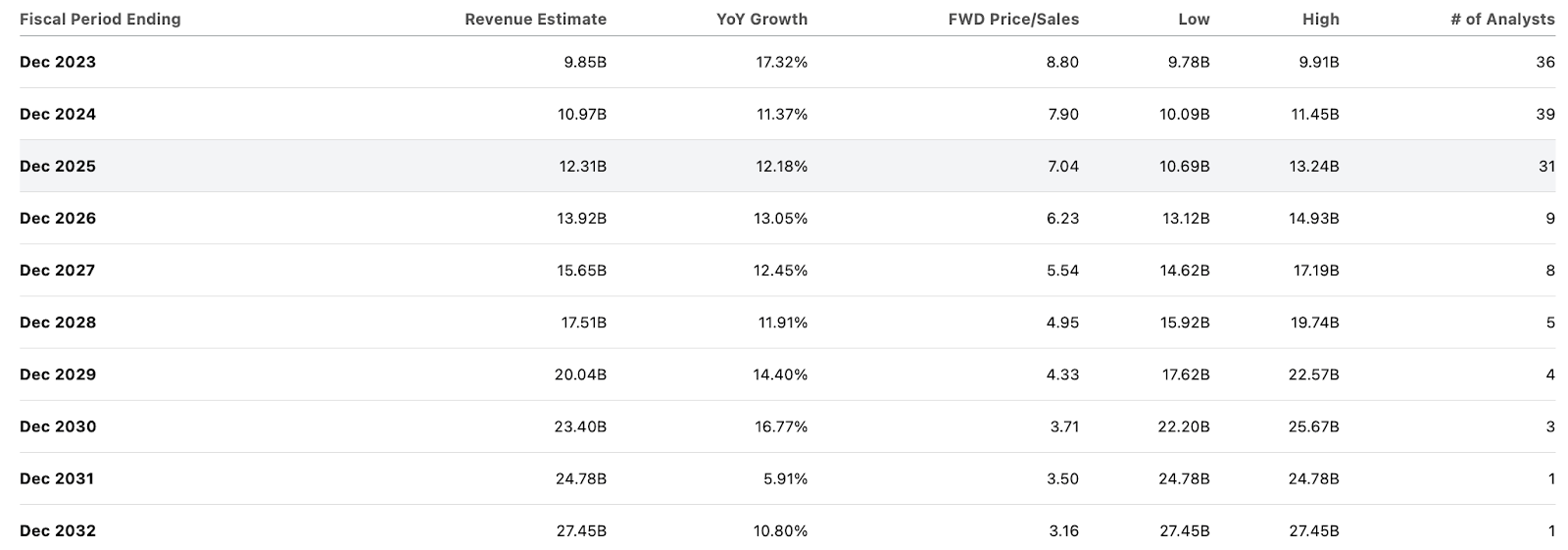

In its most recent quarter, ABNB delivered 18% YoY revenue growth to $3.4 billion, in-line with guidance.

2023 Q3 Presentation

ABNB saw nights and experiences booked grow by 14% YoY which helped drive 17% YoY growth in gross booking value (also in-line with guidance). ABNB has seen gross booking value per night growth stall post-pandemic in part due to the one-time nature of the pandemic growth as well as the increasing amount of lower priced offbeat stays.

2023 Q3 Presentation

As advertised, ABNB delivered stunning profitability, with adjusted EBITDA coming in at $1.834 billion or 54% of revenue.

2023 Q3 Presentation

ABNB generated $1.6 billion in adjusted net income after ignoring $2.8 billion in tax benefit from the release of a valuation allowance. That represented solid 32% YoY growth.

2023 Q3 Presentation

ABNB ended the quarter with $11 billion in cash and $6 billion in funds held on behalf of guests versus $2 billion of debt. The company repurchased $500 million of stock in the quarter with $1.5 billion remaining under the authorization.

Looking ahead, management is guiding for up to 14% YoY revenue growth to $2.17 billion. Management expects geopolitical conflicts and macro pressures to cause nights booked growth to moderate sequentially.

On the conference call , management noted that supply grew 19% YoY, with double-digit growth in all regions and the highest growth in highest demand regions. Management highlighted Korea as being one of their new high-growth regions, seeing 54% growth in gross nights booked relative to Q3 2019. Management expects “greater momentum for Airbnb in underpenetrated markets” as international travel recovers.

Management continues to believe that their 19% supply growth is a reliable leading indicator of forward revenue growth, perhaps with the implication that their past performances have been limited solely by their available supply. While this may have been true in the past, I question whether this trend can continue indefinitely, especially as competitors build up their own supply.

Is ABNB Stock A Buy, Sell, or Hold?

ABNB aims to disrupt the travel lodging industry by allowing hosts to rent out their properties, or parts of their properties. One key feature recently released was “Co-hosts” to help newer hosts get situated with the platform.

2023 Q3 Presentation

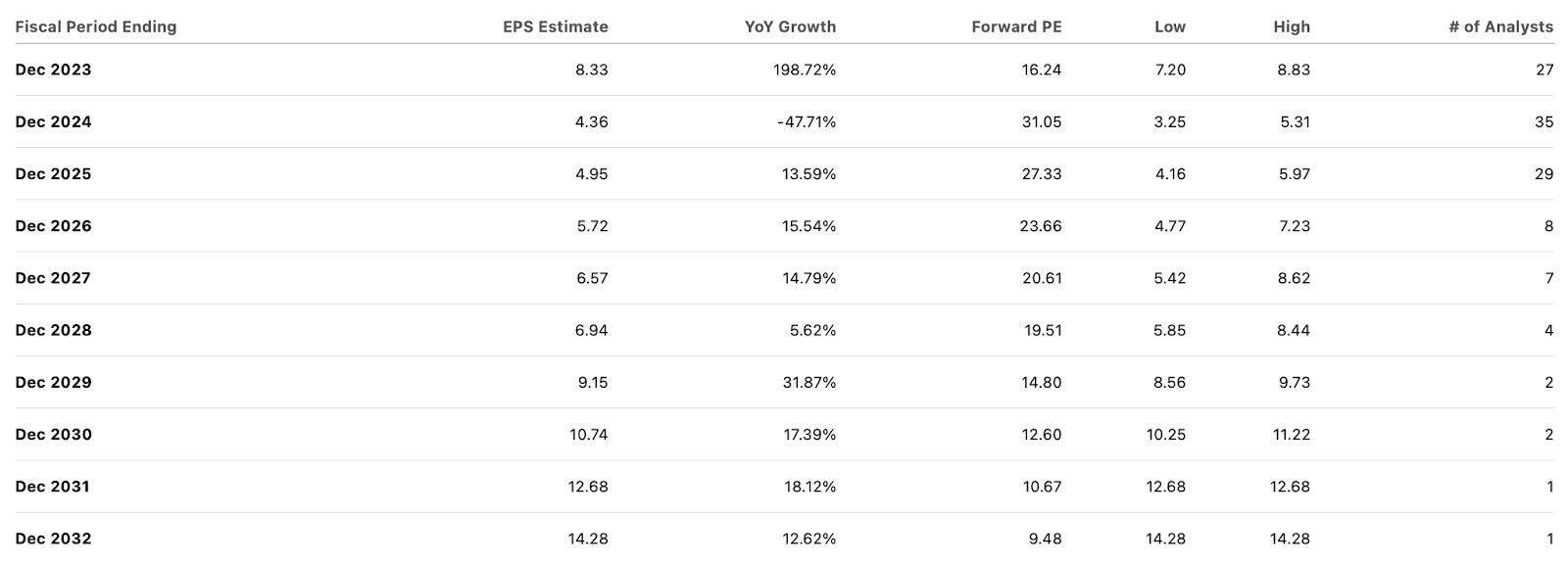

ABNB has generated envious top-line growth and profit margins, which may help somewhat to explain why the stock is trading at 31x 2024 consensus earnings estimates.

{kind=link}

In my opinion, consensus estimates look somewhat aggressive given that they are incorporating minimal deceleration in top-line growth alongside significant operating leverage.

{kind=link}

For an indication for why I view ABNB to be so expensive, consider that competitor VRBO-owner Expedia ( EXPE ) was trading at 4.5x 2028 consensus earnings estimates versus 19.5x for ABNB.

It may be difficult to frame my skepticism given the forward-looking nature of this analysis. Consider - how many online platforms have been able to avoid disruption from Google search (with disruption being defined as consumers starting their search process on Google instead of on specific platforms). I can only think of one, that being Amazon ( AMZN ), and that distinction has been earned in large part due to the irreplaceable investment in logistics infrastructure. Yes, ABNB currently has a clear advantage in terms of unit supply, ease of use, consumer satisfaction, and others. But it would be a mistake to focus on these advantages and think that they can persist indefinitely, as all of those stated advantages appear to be factors that can be easily replicated by competitors with time. In the absence of a distinct and irreplaceable advantage (like logistics for Amazon), investors should not trust that ABNB’s current competitive advantages can last over the long term. Given what happened with EXPE and BKNG, I am not of the view that ABNB posses the advantages of network effects from currently having the highest supply. Instead, I am of the view that ABNB is currently “over-earning” in terms of profit margins and will eventually see its margins and growth rates contract to levels more in-line with peers like EXPE and Booking ( BKNG ).

The main catalyst would be increased supply on behalf of competitors like VRBO and others. Services like Vacasa, which help home-owners list their properties on all platforms, may help to accelerate the trend. The main way that ABNB might be able to justify the valuation premium would be if it has the potential to drive higher take rates over time - this would be a similar investment thesis as something like Costco ( COST ) or Amazon ( AMZN ). However, as I noted in my prior report, ABNB is already charging a 3% host fee and 14% guest fee , which do not appear obviously low. No matter how much of an advantage that ABNB currently possesses, I view it to be a matter of time before the competition catches up. That makes consensus growth estimates look too optimistic (as ABNB would likely see growth rates decelerate meaningfully due to competitive threats) and the valuations look too stretched (as ABNB would likely see its valuation compress to trade more in-line with peers). EXPE currently trades at around 15x earnings and BKNG at 22x earnings. Based on aggressive consensus estimates, ABNB is trading at 21x 2027 earnings. I reiterate my underperform rating as the valuation premium appears unsustainable.

For further details see:

Airbnb: The Advantages Are Unsustainable, Look Out Below