AIRS - AirSculpt Technologies: Capital Productivity Procedure Rates Warrant Buy

2023-05-16 10:32:06 ET

Summary

- AirSculpt Technologies, Inc. came in with another strong quarter, backed by underlying unit economics.

- Key business metrics continue to improve, particularly at the gross profitability level.

- The market is expecting a big year from AirSculpt Technologies, and my numbers have it to potentially rate to the $8–$9 range as an initial target.

- Net-net, revise AIRS stock to buy.

Investment Summary

After tracking sideways since the last publication, AirSculpt Technologies, Inc. ( AIRS ) has staged a tremendous rally following its Q1 FY'23 results. Investors added another $112mm in capitalization to AIRS' market value over the last week, tracking back near its 2023 highs. I was critical of AIRS' outlook back in August last year and again in January. Key points underlining the hold thesis:

- Niche and potentially differentiated offering, offset by profitability issues.

- In that vein, without the core value drivers, AIRS may struggle to create meaningful value.

- Negative economic earnings.

- Added to that: tight money, industry-level headwinds, higher cost of capital, etc.

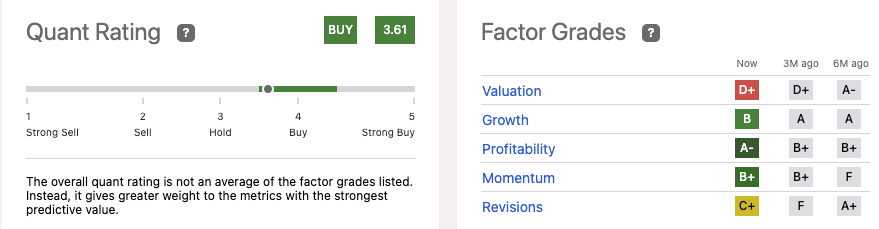

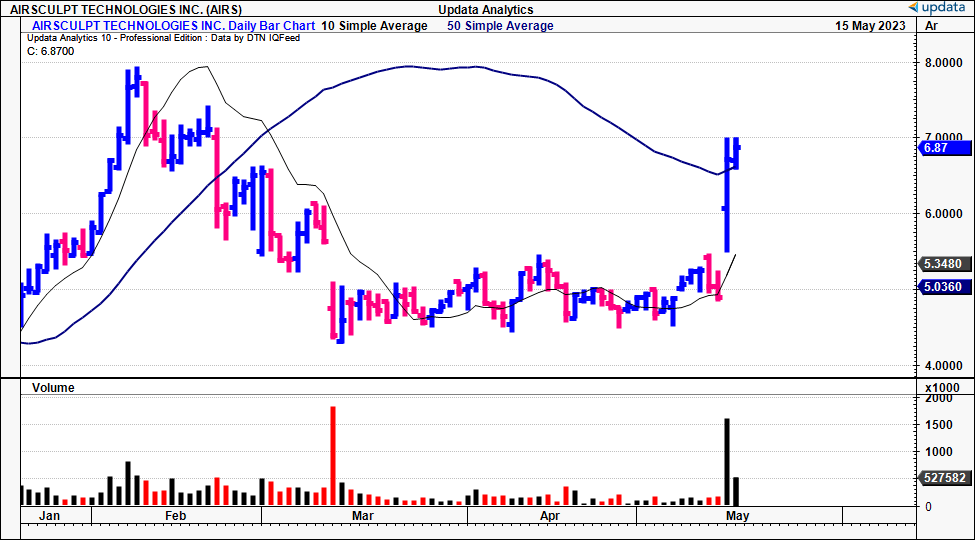

Shifting forward 1 period, we're in a different landscape. AirSculpt Technologies' unit economics are showing praise, adding 40bps of revenue per case in Q1, despite a $60 sequential lift in customer acquisition costs. The quant system now has it rated as a buy based on the composite of factors seen below. Further, technicals are supportive, given the stock crossed the 50DMA and 200DMA in vertical fashion over the last week of closes [Figure 2].

As to what has changed, this report will outline the fundamental differences observed in the AIRS investment debate. Chief among these, is the $50–$55mm in projected EBITDA this year, and generous recycling of free cash flow ("FCF") back into future growth, underpinned by the company's de novo strategy.

Fig. 1

{kind=link}

Fig. 2

{kind=link}

For investors to commit capital to any AIRS investment (equity, warrants, options, turbos, etc.), it would be wide to understand the following risks in full:

- – Small cap stocks are inherently more volatile than their large cap peers and there is greater pricing risk with small cap equities in that regard.

- – Market activity can therefore become wildly disconnected from fundamental realities, with little-to-no apparent catalysts.

- – AIRS' is also spending plenty of capital in order to ramp up productivity and free cash flow. There is execution risk in these initiatives that may or may not be detrimental to shareholder value down the line.

- – AIRS is currently unprofitable in tax-adjusted operating income, creating financial risks that may require external financing to overcome.

Net-net, with these risks in mind, I believe there's sufficient evidence to re-rate AirSculpt Technologies, Inc. stock a buy.

Fair view of AirSculpt Technologies' Q1 earnings

Investors would be pleased to know of the growth percentages AIRS booked last quarter. Starting at the top-line, it pulled in $46mm in quarterly revenue on adj. EBITDA of $10.7mm to grow 16% YoY.

Growth was underscored by the following principles:

- Case volumes leading the way with 15% upside on Q1 FY'22, a testament of AIRS' capital budgeting strategy over the 12-months. Many comments were made on AIRS' incremental returns on capital in the last publication. The numbers called for the firm to add value through its de novo/existing facilities, which seems to have pulled through this quarter. It added 4 de novo centers in Q1 off last year's Q1 base. In total, it added 14 de novo's over the year, now operating 23 sites.

- Unit economics are adding incremental value to the top-line. The firm's revenue per case will typically hover between $12,000–$13,000 each period, and it expects this range over the near-term. Thus, anything close to the upper limit is telling of AIRS' revenue trajectory in my opinion.

- In Q1, revenue/case was $12,600, up $400 sequentially. This implies a rate of 3,650 cases for the quarter (14,600 annualized).

- Related to point (2), the quarterly cost of services margin pulled in ~200bps higher YoY to 39.3% of turnover. To this, you're looking at a mix of general business cost and $60 YoY increase in customer acquisition cost to $2,360.

With respect to unit economics, the two most important drivers to AIRS' top-line moving forward are demand (evidenced through volumes) and revenue per case in my opinion. In that vein, the key takeaways from the quarter are the 15% volume growth and $12,600 revenue/case. Looking at this rate per case, another 10% jump in demand from the 3,650 cases in Q1 could translate to a $50mm quarterly run rate for AIRS. This is based on 4,015 cases a $12,500 rate per case ((3,650x1.15 = 4,015) x $12,500 = $50.18mm), getting you to management's c.$200mm FY'23 revenue forecasts.

I believe this is a fair number and my estimates have AIRS to do $198–$208mm in turnover this year, and it could pull this down to $130–$140mm in gross on this. These are attractive numbers going forward.

Speaking of going forward, management expect very healthy contributions from the de novo centers to drive its projected 11–14% YoY growth in turnover. It also expects to be FCF positive this year which is another welcomed sign.

Figure 2 shows the progression of AIRS' free cash flow on a rolling TTM basis. We have data ranging back to FY'20, prior to AIRS' listing for a cleaner analysis. FCF is defined at the net operating profit after tax ("NOPAT") minus incremental investments (periodic capital investments + NWC delta). Importantly, this calculation includes intangible investments, and treats goodwill as capital at risk. A format that uses operating cash flow is also observed with differing results.

You'll note that management has been heavily recycling retained capital back into productive assets for the business, especially from Q3 FY'22 onwards. This aligns with the evolving de novo strategy, and capital flows to existing facilities. Management confirmed the same from the Q1 call:

We continue to expect our primary uses of cash flow during the year will be to fund growth investments for the business such as adding de novo centers and driving technology innovations.

Fig. 2

Note: Free cash flow is calculated as NOPAT less investments per quarter. NOPAT is calculated on a rolling TTM basis, along with operating cash flow. (Data: AIRS 10-Q's)

{kind=link}

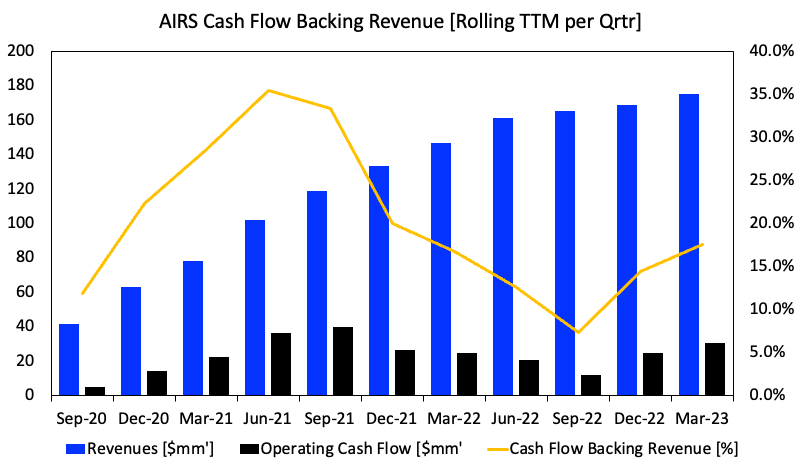

Additional cash flow findings suggest AIRS' top-line growth is sustainable as well. Note the following from Figure 3. Here, rolling TTM revenues are observed against operating cash flows. The percentage of cash flow backing turnover is then calculated on the same rolling basis, to quantify the cash collection on forward revenues. It shows that:

- From Q3 FY'20–Q1 FY'23 turnover ramped from $41mm to $175mm illustrating the procedural demand, competitiveness.

- OCF cyclical but follows heavy period of reinvestment to growth and thus plenty of NWC delta and additional depreciation etc each quarter.

- There is a key caveat to this, however. Stock-based compensation fulfilled the bulk of OCF each quarter from 2020-Q1 2023 (TTM basis).

- Using FY'22 as an example, of the $24mm booked in OCF last year, it realized $29mm of SBC, added back as a non-operating cost. Mauboussin and colleagues (2021) argue that SBC should be treated as a financing cost: "...[t]he company first sells shares (financing) and then uses the proceeds to pay employees (compensation for service). Combine these ideas and it makes sense to move SBC from the cash flow from operating activities section to the cash flow from financing activities section. This portrays the cash flow statement more accurately."

Whether you agree with this or not, the point is, the $29mm add-back in SBC seems unreasonable to produce $24mm in annual OCF. Backing it out, you get to a $5mm TTM cash outflow for FY'22. This is important, because the firm's incremental investments are flowing through to OCF, at a 4% return (15.8% annualized) last period. Hence, this may not be as lucrative as on face value. Looking AIRS' book values, there is 17.5% of cash flow backing revenues as of Q1 FY'23, up from lows last year.

Fig. 3

{kind=link}

Another point on the liquidity front – cost management. AIRS is committed to this, which is pleasing given some of the challenges outlined last publication. Management note it is aiming for $5mm in cost savings for 2023 and has employed 3rd-party help to achieve this. Expanding on this, consider these potential benefits:

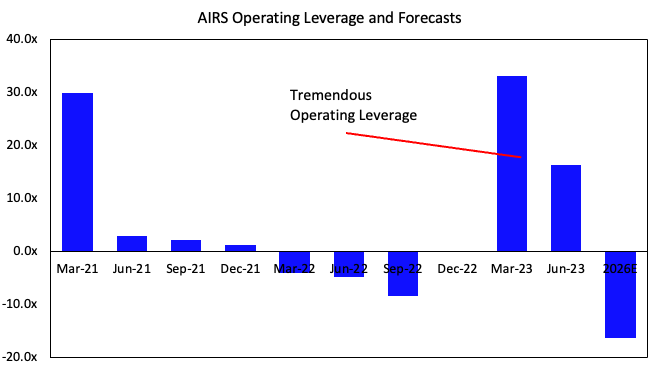

- There has been, in certain instances, periods where AIRS has produced tremendous operating leverage, north of 15x in Q1 [Figure 4].

- This is telling of the cost structure. In periods where the leverage is high, fixed costs made up the bulk of total business costs, sending plenty of income down to pre-tax earnings.

- My numbers have this to carry through in FY'23 and would suggest AIRS' de novo centers coming online is a meaningful driver to operating income.

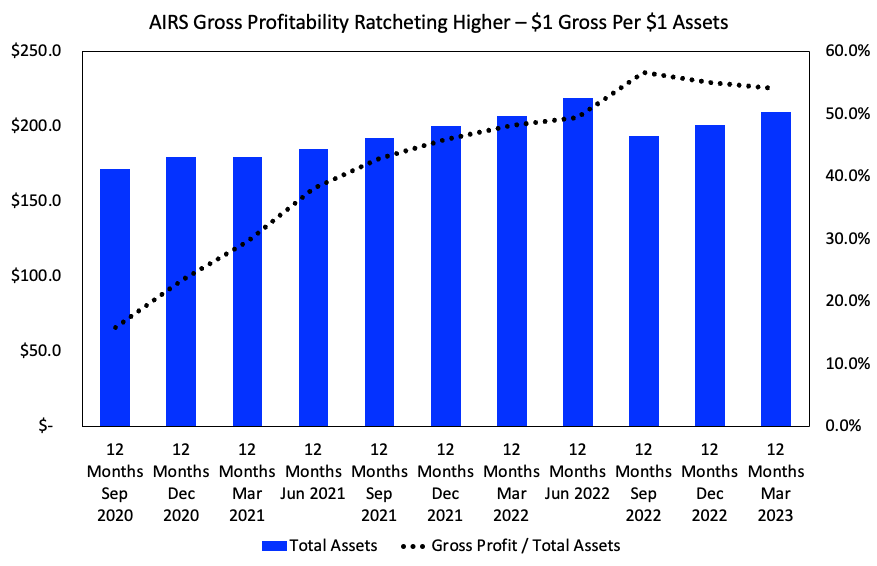

Further evidence of the same is plotted in Figure 5, showing the firm's gross profitability. Here, the TTM gross profit is taken against the book value of AIRS' assets each quarter. It shows superb growth in capital productivity over the testing period. Gross profitability has ratcheted from 16% in 2020 to 54% last quarter. This is key to the change in my thesis for a couple of reasons.

One, it is evidence of AIRS' success in capital allocation. Each $1 in assets is scaling up in gross profit, what more could one ask. Two, if these trends continue, it will attack the gross margin, and potentially lift a few points from the 65% in trailing gross the company booked in Q1. A shift towards 70% in gross margin would be superb evidence of AIRS ability to make money at pace.

Fig. 4

{kind=link}

Fig. 5

{kind=link}

The data pulled from AIRS first quarter suggest it is in for a strong FY'23. I am calling for $208mm in revenue at the upper range, as mentioned, and the points on capital productivity are certainly welcomed in that regard.

AIRS Stock Valuation

The market expects 15x forward earnings (non-GAAP) from AIRS at the time of writing, below the sector's 19.5x. The c.30% rally in market value must have stemmed from somewhere. Investor expectations have undoubtedly changed for the company, question is from where.

Without operating margin, I'd be focusing on AIRS' gross profit and EBITDA delta to understand its valuation, in-line with earlier analysis. I am looking to a 12% discount rate for AIRS as this effectively prices in the opportunity cost and a few points of risk in my opinion. At the 12% hurdle rate, the market is expecting $48mm in forward EBITDA getting to the $390–$400mm market cap range today ($48 / 0.12 = $400). This is in-line with management's forecast for 2023 as well.

Hence, in my opinion, the market's expectations are still short of the upside potential. My numbers are pointing to $55mm in FY'23 EBITDA and a the 9x multiple (still a 33% discount to peers) gets to the $495mm market valuation range, or $8.83 apiece. At the sector multiple of 13.6x, you're looking at ~$750mm ($13–$14/share). Both numbers are attractive and I'd be happy to pay either multiple, and suspect AIRS could trend to the sector multiple if it continues at this trajectory.

Added, to that, point and figure studies have thrown off a new upside target to $8.80 after the latest rally. I am therefore looking to the $8–$9 range given the confidence of data around this initial estimate.

Fig. 6

Data: Updata

Conclusion

In summation, AirSculpt Technologies, Inc.'s latest numbers have given a clear picture to profitability looking forward. This is bullish in my opinion. The following points sum it up best:

- Capital productivity now a key feature and driving gross margin down the line.

- Free cash flow positive and recycling FCF back into business growth, namely, de novo centers and expanding new facilities.

- Operating cash flow backing revenue pushing higher and at a very healthy 17% (TTM basis) even with revenue upsides.

- Valuations supportive with AIRS trading at a discount to peers but offering plenty of valuation upside to the $8-$9 mark as an initial price objective.

Net-net, I am revising the rating on AirSculpt Technologies, Inc. stock to a buy, looking to $8-$9 as an initial objective.

For further details see:

AirSculpt Technologies: Capital Productivity, Procedure Rates Warrant Buy