AIRS - AirSculpt Technologies: Continued Expansion In Q3 Capital Deployment A Standout

2023-11-11 08:00:00 ET

Summary

- AirSculpt Technologies reported strong Q3 numbers, indicating revenue and caseload growth.

- The company's performance is solidifying its position in the market.

- The Q3 results highlight the success of AirSculpt Technologies' reinvestment into de novo facilities to grow.

Investment Update

AirSculpt Technologies, Inc. ( AIRS ) posted its Q3 numbers yesterday, solidifying its revenue and caseload growth. In my last AIRS publication , I noted the following observations:

- The primary differentiator is its AirSculpt procedure,

- Growth is via same-store and de novo strategy,

- New facility openings are the primary use of AIRS' capital,

- Square footage per facility is small, as operations are rooms-based.

- There continues to be emerging value in AIRS.

Shifting forward, AIRS' Q3 earnings results corroborate this view. After tracking sideways for the better part of the year, the company has demonstrated its ability to withstand turbulent markets and maintain some level of market value. Here I'll unpack the company's latest numbers and link this back to the broader by thesis. Net-net, I reiterate AIRS as a buy.

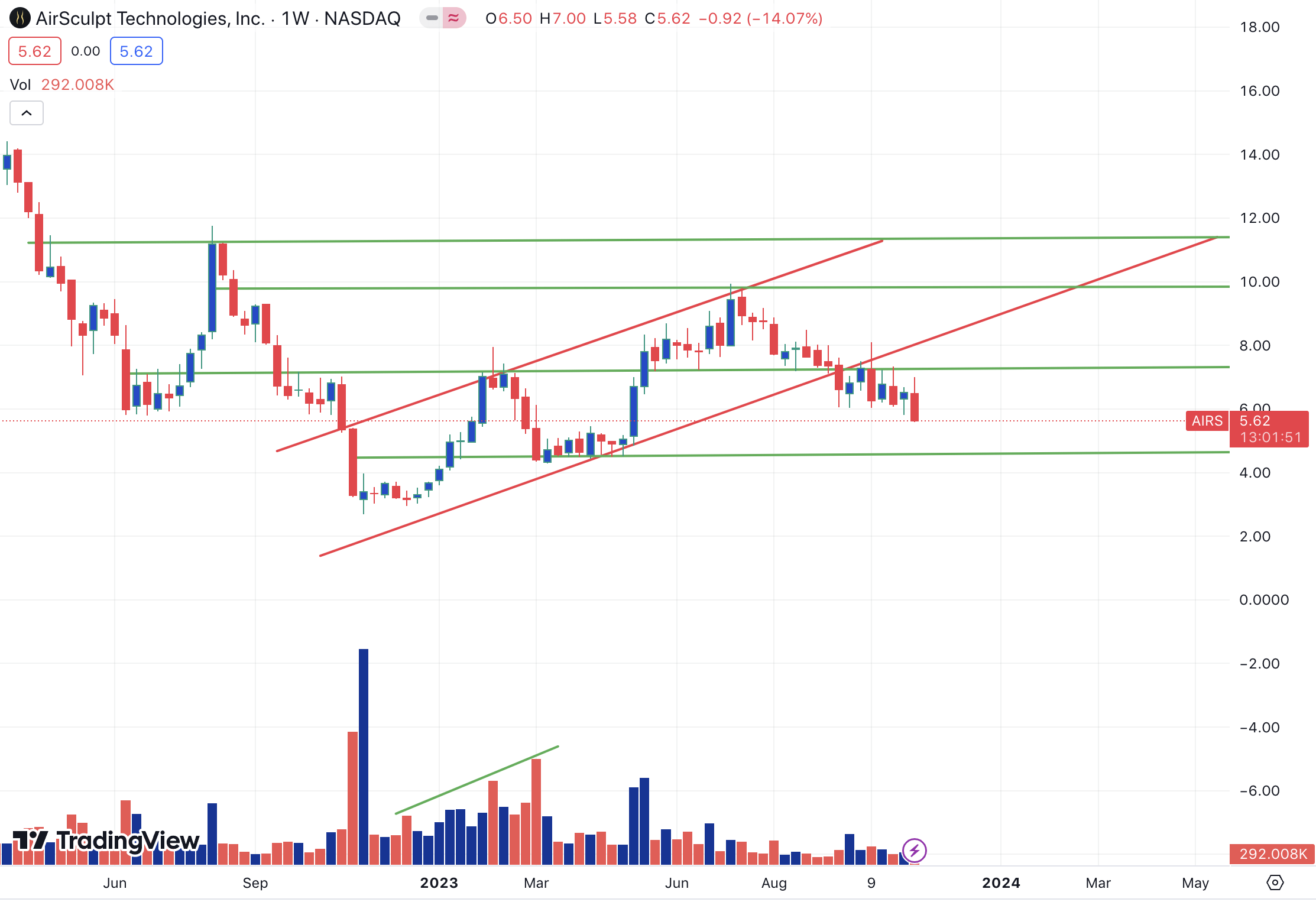

Figure 1. AIRS long-term price evolution, '23. Notice how the previous marabuzo levels have been key levels in the subsequent trend? This is insightful. The marabuzo lines are indicating key levels of price control. These could be magnets for price. Net target may be $4.70 based on this.

{kind=link}

Key Risks

Investors must realise the following sets of risks that could not find investment thesis:

- AIRS relies on a de novo strategy for growth and must continue to demonstrate its capacity to reinvest and remain cash flow positive. If not, then it may hinder the growth outlook.

- We cannot overlook the spate of economic risks currently in play, in particular the rates/inflation axis. Thankfully, AIRS financed most of its CapEx from operating cash flow. But it may need to add further leverage to its balance sheet.

- The current value of broad equity markets is heavily concentrated in a handful of mega-cap stocks. Distribution of returns is not even.

- The company faces competition in its operating domain.

Investors should understand these before proceeding.

Q3 Earnings Insights

- Key financials

The company posted sound results, beating consensus estimates at the top line. Revenues came in reasonably strong at ~$47mm, up to 20% YoY. YTD revenues came to $148mm, up 16% YoY. It pulled this to adj. EBITDA of $9.1mm, up 12.2% year-on-year, on a net loss of $1.7mm, compared to a loss of $7.4mm last year. Critically, same-store sales were up 5.3% YoY. This is telling on both:

(1). Demand for the AirSculpt procedure, and

(2). The company's de novo growth strategy.

The company left the quarter with around $9mm in cash on the balance sheet, plus another $5mm in additional liquidity. This is after it repaid ~$10mm to its existing term loan, effectively strengthening the balance sheet. Finally, operating cash flow produced was $0.6mm, bringing the total OCF to $19mm for the YTD.

- Unit economics continue to stretch higher

As to the company's core competencies, one can observe reasonable growth percentages dotted throughout the numbers. In particular, it performed 3,426 cases during the quarter, culminating in a 19% growth over the 12 months. This brings the total case volume to 11,252 for the year-to-date, a growth of 15.7%.

It also opened an additional 2 centres in Q3, meaning it has now opened 5 new centres and hit its target sets earlier in the year (per management: we have now opened five new centres in 2023 "). As a reminder, AIRS' employs a de novo growth strategy where it invests recycled earnings into opening new centres and build its footprint across a broader domain. This has the benefit of increasing its cases per centre, and driving same-store sales growth. Critically, for the quarter, pre-opening and de novo costs were in the range of $0.5-$1.1mm, and for the YTD they were $3.3mm, around 2.3% of sales for Q3 and YTD, respectively.

In my opinion, the fact it has met its target of new openings by the 3rd quarter is a bullish signal. It represents demand for the company's major offering. But it also suggests that (1) it envisions a strong runaway of future investments to (2) drive additional case volumes. This is critical for the company's investment outlook. Keep in mind, a company creates value from the rate of earnings it produces on its invested capital, but also the length of reinvestment runway it has to deploy surplus capital at these rates of return. In my last analysis on AIRS, I performed a deep dive into the economics of the company's re-investment strategy. My findings concluded that if it were to open six new facilities this year, at an average spend of $2.1mm per new facility, and maintain its current trajectory of sales and pretax earnings, then it could spin off a return on incremental capital deployed of ~27%. Based on what we've seen this quarter, the company looks set to produce a similar set of results, in my opinion.

- Guidance points to an additional growth period

Management reaffirmed its full year guidance and expects ~$196mm in sales, calling 16.1% growth from FY'22. It is eyeing ~$45mm in adj. EBITDA for the year on this, a 23% pretax margin. Critically, given that it has met its target in new store openings, the company is looking to open five new centres.

Moreover, it envisions a conversion of 65% from adj. EBITDA to OCF, collecting ~$30mm in cash from operations. If it were to hit this target, based on its current base of operating facilities, this would translate to an average cash per facility of $1.07mm, ultimately producing a nearly 50% return on capital deployed to operations. This is an overwhelmingly bullish fact, if it were to come to fruition.

It would show (1) the company's efficient use of capital, and (2) evidence of the popularity of the AirSculpt procedure, when combined, solidify the investment offering in my opinion. So I would be looking to gauge what profits and cash flows it produces this year as a priority. If it hits these numbers, it will provide excellent clarity into the profitability of each facility and the franchise in total.

Valuation

The company sells at 14.8x earnings , 10x forward EBITDA, and 13.8 x cash flow. You are therefore buying a 7.2% cash flow yield if owning AIRS today. The earnings yield is around 7% as well at these multiples. I would also point out the following key facts as it relates to the company's valuation:

- The market has valued AIRS at 4.3x book value, indicating it places a high valuation on its net assets. In effect, the company has created more than $4 in market value for each $1 in net assets employed on the balance sheet.

- Presuming the market is a fairly accurate judge of fair value over time, this is quite telling. It implies periods of strong business for AIRS into the coming periods, based on the market's discounting mechanism.

- Added to this, you are receiving both cash flow and earnings yields that are above marketable securities such as treasury bills and bonds, which in the current environment, is extremely attractive. Even more so given the company has to continuously reinvest surplus capital into new facilities to grow.

- Collectively, these factors weigh in positively on the valuation debate. In other words, there is value to be had in paying these current multiples, and you would be buying a set of core assets that are valued highly by the market, insinuating that the earnings power on these asset factors is high.

In that vein, I am constructive on AIRS at these given valuations. I am also satisfied with management's FY'23 projections, as these look conservative and haven't been revised higher, despite a period of good business for the company in Q3. At 10x management's projected adj. EBITDA of $45mm, this gets you to $450mm dollars in market value or $7.90/share, around 26% upside potential from the time of publication. This supports a buy rating on the valuation front.

Discussion Summary

In short, there are multiple economic levers that AIRS is employing to sustain its growth potential. Q3 earnings were respectively strong and corroborated the findings from previous analyses. What is most important is the company is able to recycle its surplus capital into new facilities and continuously be cash flow positive. This is what we have seen this quarter, and management believes this trend will continue for the remainder of the year. At the current price of around 10x EBITDA, this is both an attractive multiple and supports a cash flow yield of around 7%, giving you around two points of the upside from the risk-free rate. Furthermore, I arrive at a valuation of ~$450mm in market value, around 26% upside from the time of writing. In that vein, we had three factors which feed into the reiterated by thesis:

(1). Fundamental - continued growth in same-store sales and overall sales,

(2). Operational - Continued reinvestment into new store opening, remaining cash flow positive in doing so,

(3). Valuation - Attractive multiples that still give scope for additional upsides into the coming 12 months.

Net-net, I reiterate AIRS as a buy on its future prospects, eyeing $7.90/share as the next objective.

For further details see:

AirSculpt Technologies: Continued Expansion In Q3, Capital Deployment A Standout