AIRS - AirSculpt Technologies: Rotating Capital Into De Novo Strategy Continued Profit Growth Reiterate Buy

2023-08-14 02:01:08 ET

Summary

- AirSculpt Technologies continues to offer long-term investment potential with solid Q2 FY'23 numbers.

- The company's AirSculpt body contouring procedure offers potential advantages over alternative procedures, attracting customers with its efficiency and quick recovery time.

- AIRS has been inflecting higher via its unit economics with increasing case volumes and plans to open more de novo facilities to drive growth.

- Net-net, reiterate buy.

Investment briefing

AirSculpt Technologies, Inc. ( AIRS ) continues to offer potential to unlock long-term risk capital in my informed opinion. The company's Q2 FY'23 numbers were solid and evidenced the capital rotation strategy it is employing to grow operations. Here I'll run through the latest figures and update investors with the critical investment facts. Net-net, I continue to rate AIRS a buy for the reasons discussed in this report.

This analysis will pay close attention to 1) the economic characteristics driving AIRS financial performance, 2) demonstrating how it is recycling earnings back into funding de novo facilities, to 3) grow procedural volumes of the AirSculpt body contouring segment. Reiterate buy at $11.95.

Figure 1. AIRS price evolution

Data: Updata

Critical facts to AIRS investment debate

The primary differentiator and growth lever for AIRS is its AirSculpt body contouring procedure. It books revenues via the delivery of procedures through its various sites, dotted throughout the U.S., UK and Canada. On closer inspection, the procedure itself isn't wholly differentiated from modern conventions of laser-derived liposuction. It is more or less a form of liposuction that removes body fat. But it does offer several potential advantages over alternative and/or comparable procedures.

For instance, the actual mechanism of action is different. The patient's respective body area (thigh, arm, abdomen, tailbone, etc.) is first numbed (usually with lidocaine), and a cannula is inserted into the skin through two, pencil-sized holes. Whereas conventional liposuction 'scrapes' fat cells, or adipose tissue, from beneath the dermal layers, AIRS' design works more in a corkscrew and jack-hammer mechanism. It supposedly breaks the desired tissue into breadcrumb-sized cells and then suctions these out through AIRS' proprietary cannula. Critically, the procedure does not require general anaesthesia and touts more efficient results.

The benefits of the minimally invasive surgery are easy to glean for both patient and surgeon. Specifically, the patient economics are as such:

- Quicker surgery time given the lack of pre and post-operative steps;

- Faster discharge times for the same reasons;

- Length of downtime reduces from ~2 weeks to ~24 hours in most cases;

- Patients are back to full function in a matter of days.

Bear in mind that similar procedures on the marketplace offer similar benefits. But AIRS has clever marketing (via the "AirSculpt" brand), and there is no denying the appeal to customers. The prospect of booking a procedure, being in and out in a matter of hours, having no anaesthesia, and back to work within the week are tremendously attractive in my view. Not to mention the patient turnover rates for surgeons on these patient economics.

Q2 numbers illustrate adoption trends

The company's value equation is a same-store and de novo strategy. It must open new clinics, drive AirSculpt case volumes at each site, and then open more de novos to repeat the same process. To date, the economics have been inflecting higher based on my assessment.

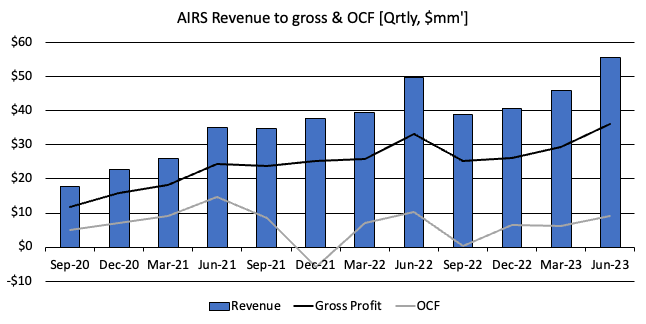

Q2 sales were at $55.7mm, up 12.2% YoY on a 13% jump in case volumes. It did 4,186 cases for the period. AIRS also added 6 de novos over the 12 months to June 30th, meaning it had 25 centres on the books. You can see the ramp on its quarterly revenue, gross profit and OCF trends below. Q3 2022-date have been the steepest, resulting in record quarterly numbers for the firm since listing.

Figure 2. Note the ramp from 2022

Data: Author, AIRS SEC Filings

{kind=link}

A key point I'd raise is the potential interplay between the weight-loss class of drugs called GLP-1 inhibitors (think Ozempic). One might perceive the emergence of a weight-loss category as a threat to AIRS. However, I'd stress that the AirSculpt brand focuses on body contouring, and not pure 'weight loss'. There is a difference in principle. In fact, it could even be a potential tailwind. Management touched on this on the call:

We see-it's been a tailwind for us now, and we see it so often. We internally call it "AirOzempic", because we see so many people who are on Ozempic actually getting AirSculpt because now they can give themselves permission. If you lose 25, 30 pounds, and your arms and chins still bother you, you're even more likely to come in...".

Therefore the relationship between both domains could be symbiotic rather than competitive, which is something to consider moving forward in my view.

Breakdown on the quarter's unit economics is as follows:

- The average revenue per case for the quarter settled at around $13,300, indicating a modest 1.1% decrease YoY.

- Sequentially this number was up 700% from Q1 FY'23, primarily influenced by the procedure mix.

- Notably, this exceeded AIRS' internal target range of $12,000-$13,000. This can be tied back to the bundling promotional strategy, where multiple body parts are billed on the same procedure (think doing the thighs and buttocks in one sitting for example). This raises the average revenue per case.

- Critically, the percentage of patients opting for financing to cover procedure costs has consistently held in the 40% range. This talks to the pricing point, and suggests price is below marginal utility for ~60% of patients.

Moving down the P&L, the cost of service came to ~36% of turnover, keeping the cost of acquisition per customer ("CAC") at ~$2,250, and gross profit per case at ~$8,500. The gross to CAC was 3.7 to 1, handsome leverage that offers increasing profitability going forward if CAC remains flat.

Management guide to $192mm in sales at the top end of range, calling for 14% YoY growth at the top. It eyes ~$45mm in adj. EBITDA on this, also up 16%. My numbers have the company to do $203mm in revenues on $25mm after-tax income [full projections are outlined later].

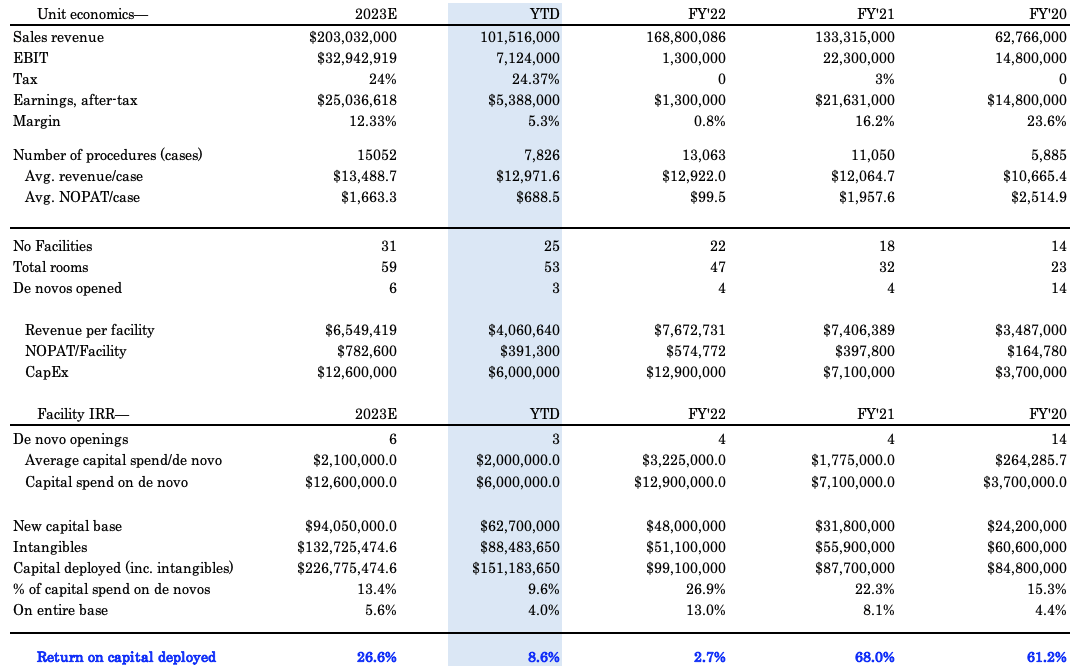

Facility IRR building shareholder value

As mentioned, a large portion of the investment value for AIRS hinges on its ability to successfully bring de novos online and grow same-store sales as it expands its footprint. Simply-grow new and existing revenues + profits to grow the internal rate of return ("IRR") per clinic. A few key points on the firm's de novo strategy.

One, new facility openings are the primary use of AIRS' capital at the time being, with the bolus of earnings being recycled-along with its cash on hand-to setting up more clinics. This is because each de novo is dubbed to be more attractive to driving growth at this stage. The reason boils down to the cost of service. Each de novo comes with a higher cost of service for year 1 until it matures-typically 2 years. Hence, whilst it adds new sites, these will pull in lower gross for 24 months, say. Alas, whilst this occurs, more clinics must be added to keep the flywheel in motion. Not only that, but in order to increase its national/international footprint, it must open new clinics.

Two the square footage of each facility is quite small as the 'operational' component is rooms-based. Each site has a set of rooms where procedures are done, combined with the standard features of any clinic (reception, waiting area, etc.). I'm not entirely sure about carparks and so forth. Hence, the capital charge on each is well-contained in my view.

Just how contained is observed below:

- From FY'21 to H1 FY'23, it has opened ~3-4 de novos per period. On my estimations, the average capital spend per de novo has ranged between $1.75mm-$3mm. It is $2mm/site this YTD with the 3 sites it has brought fully online.

- Revenue per facility is up from $3.5mm in 2020 to $4.1mm by H1 this year, and could reach $6.55mm by yearend in my estimation.

- Critically, whilst this is slightly down on the 3-year average, the after-tax profit per facility is at $391,300 on H1 FY'23 post-tax earnings of $7.1mm.

- Thus, I get to $782,600 in profit per facility by yearend, solid growth on prior years.

- As of H2 FY'23, I've also got the total capital spend on its de novos to reach $12.6mm for the year-in-line with FY'22, and above the $7.1mm in 2021.

- In terms of the capital deployed on these assumptions, to see AIRS bring ~26% return back on this in FY'23 is not unreasonable in my view. My assumptions have the company to have brought on 6 new sites this year, bringing its total to 31, producing $25mm in post-tax earnings off a $94mm capital charge.

Figure 3.

Data: Author, AIRS SEC FIlings

{kind=link}

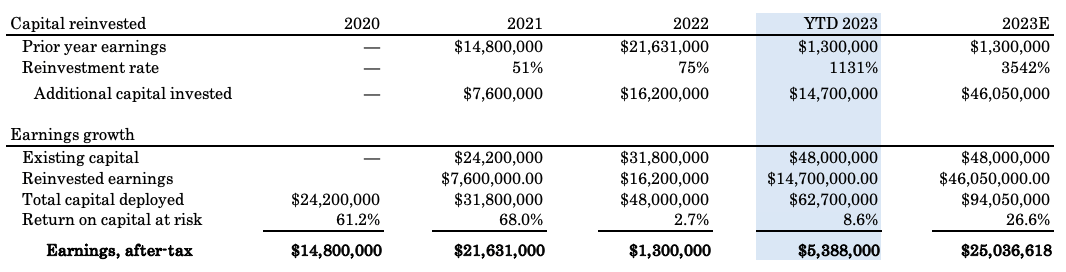

The interplay on this between capital recycled into new de novos and the corresponding earnings growth from 2020-H1 FY'23 are seen below. New capital deployments have produced earnings growth at attractive rates of return in FY'23, where the company piled all its surplus cash into growing operations.

For FY'23, my estimates have the firm allocating an additional $46mm this year in total, other words, another $31.35mm from H1 FY'22 (this gets me to $94mm in capital at risk for AIRS, as mentioned earlier). The $25mm after-tax would come at a margin of 12.3% with 59 rooms, and 31 facilities in operation by yearend should this come true.

As a reminder, management's goals are to add 6 more locations in 2024, eventually looking to hit 500 locations globally. Using the H1 FY'23 actuals of $4mm/site and $0.391mm in NOPAT per site, at 500 sites, this gets you to $195.65mm in profit after tax, off ~$2Bn in sales (4mm x 500 = ~$2,000mm). At 6 de novos per year it would take another 78 years to do this (500-31 sites in FY'23 = 443; then 443/6 sites per year = 78). Hence, it will need to up the pace drastically on the current cadence of openings over the decade to generate outsized value for shareholders. This would be a key risk to the investment thesis that investors should realize.

Figure 4.

Data: Author, AIRS SEC FIlings

{kind=link}

Valuation and conclusion

The equity stock trades at 15x forward earnings and 2.5x forward sales. As a testament to its offering, the market has valued its net assets at ~6x book value. In effect, this means AIRS has created $6 in book value for every $1 in market value. And it makes sense too-its asset base produces the capital, via the facilities that do AirSculpting.

With the growth numbers outlined this period I'm surprised to see AIRS trade at a 23.5% discount to the sector multiple of 20x earnings. I do believe it will rate at least in-line with the sector over time. Further, the stock trades at 7.1x its invested capital, and I am in favour of valuing the stock on this convention, given the findings discussed in this report. At 7.1x my FY'23 capital estimates for the company of $94mm, I get to $11.95/share in equity value, or 54% upside potential as I write. This supports a buy rating.

Figure 5. AIRS earnings multiples vs. sector

Data: Seeking Alpha

In short, I continue to see emerging value in AIRS, and the potential to unlock risk capital moving forward. The company has a clear growth route of adding de novo facilities with a reasonable investment on each, where maintenance CapEx is contained. Each centre is proving to be profitable once brought online, and thus its AirSculpt procedure is the next thing that needs to shine in the investment debate. It looks to 500 sites as a goal, currently at ~5% of that by the end of Q2. Net-net, I rate AIRS a buy at $11.95 price objective.

Risks to investment thesis:

- The market continues to demand exceptional economics from healthcare companies at the moment and there's been a selloff in broad healthcare equities in August as evidence of this. AIRS needs to demonstrate its propensity to hit the numbers outlined here to catch a bid.

- Macro-level risks are ever the more present with the rates/inflation axis and this could impact discretionary income of AIRS' potential customers, thus hampering sales growth.

- Similarly, cost of money being its highest in over a decade could hit feasibility of rolling out new clinics.

- Operating costs per clinic could also ramp up as a result of each of these figures, clamping profit/clinic and the ability to reinvest internally generated capital toward growth.

These risks must be understood in full before proceeding any further.

For further details see:

AirSculpt Technologies: Rotating Capital Into De Novo Strategy, Continued Profit Growth, Reiterate Buy