AJXA - AJXA: Failed Merger Raises Risk For This Note That Matures Next April

2023-12-01 09:45:00 ET

Summary

- This article compares the Great Ajax Corp. 7.25 CV SR NT 24 to a five-month CD, highlighting the risks involved in the trade.

- My analysis focuses on the issuer, Great Ajax Corp., and its financial position, including recent quarterly results and available sources of cash.

- The yield-to-maturity (YTM) for the Great Ajax Corp. note is estimated to be around 12.2%, making it an attractive option for risk-takers. Low trading volume could be an issue.

Introduction

Recently, I have done several articles looking at whether a bond or high-yielding preferred were worth the risk for the extra return the investor could expect over a CD maturing at the same time. In both cases, I was comfortable with the added risk for the potential of more return, one of which I already held. There are links to both articles at the end of this one.

In comparing the Great Ajax Corp. 7.25 CV SR NT 24 ( AJXA ) against a five-month CD which yields 5.4%, I’m not comfortable recommending this trade except for risk-takers since I got burned recently on a similar Note. That said, I see defaulting on the Note as a very remote possibility. With the Ajax Note selling near Par, the market is expecting Great Ajax Corp. ( AJX ) to be able to retire the Note.

Let's start the analysis by looking at the Note. I like this site for basic data on preferreds and baby bonds.

seekingalpha.com AJXA homepage

As with most fixed income assets, prices have declined as interest rates climbed.

{kind=link}

quantumonline.com/search.cfm

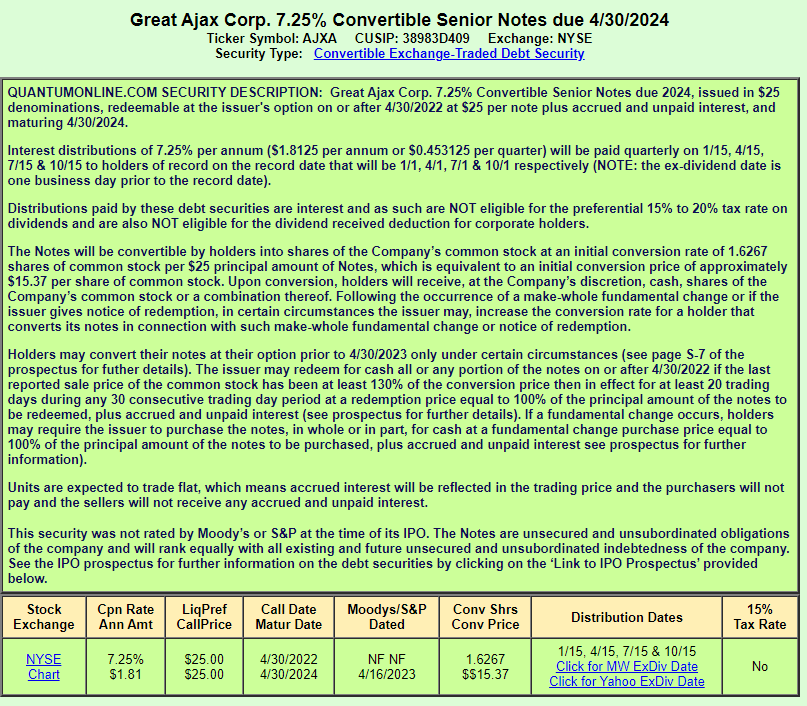

This Note matures in just over five months. There is the option to convert the Note into AJX common stock per $25 principal amount of Notes. As stated in the Prospectus , the initial conversion rate will be into 1.6267 shares of AJX stock, or a conversion price of approximately $15.37. As allowed when new common shares are issued, the conversion rate has increased to 1.7405. AJX has the option of giving the Note investor cash instead of shares. Conversion isn’t in the cards with AJX selling for under $5/share and as far as I can tell, never at a price that would have warranted conversion, thus the Call feature was never activated.

The bottom line is AJX will need $87.5m, plus interest, when the Notes mature. Now, let’s take a look at the issuer, the Great Ajax Corp.

Here is how Seeking Alpha describes the company.

Great Ajax Corp. operates as a mortgage real estate investment trust. It acquires re-performing and non-performing loans; acquires or originates small balance commercial mortgage loans that are secured by multi-family residential and commercial mixed use retail/residential properties; and invests in single-family and smaller commercial properties. The company elected to be taxed as a real estate investment trust for U.S. federal income tax purposes. It generally would not be subject to federal corporate income taxes, if it distributes at least 90% of its taxable income to its stockholders. Great Ajax Corp. was incorporated in 2014 and is based in Tigard, Oregon.

Great Ajax provides this description of their mREIT strategy.

Great Ajax Corp is an externally managed real estate investment trust that acquires, invests and manages a portfolio of mortgage loans secured by single- family residences and single-family properties. We also invest in loans secured by multi-family residential and commercial mixed use retail/residential properties. In addition, we hold real-estate owned (REO) properties acquired upon the foreclosure, other settlement of our owned non-performing loans, or that we acquire in the market.

In July, Ellington Financial ( EFC ) announced it would merge with Great Ajax Corp, which valued AJX around $7.33, or about a 20% premium from the prior day’s closing price. Then on October 20th, the merger was cancelled, with these terms imposed.

The termination was approved by both companies’ boards of directors after careful consideration of the proposed merger and the progress made towards completing the proposed merger. In addition, Ellington Financial has agreed to pay Great Ajax $16 million of which $5 million is payable in cash and $11 million was paid as consideration for 1,666,666 shares of Great Ajax common stock, which were purchased at a per share price of $6.60. Ellington Financial will now hold approximately 6.1% of Great Ajax’s stock. In addition, an affiliate of the external manager of Ellington Financial owned 273,983 shares of Great Ajax common stock as of June 30, 2023. Ellington Financial remains a securitization joint venture partner as well. The two companies intend to continue to work together on mortgage loan opportunities.

Details as to why were not shared, but the fact the EFC took shares for paying $11m more in cash is a positive indication toward the prospects for AJX. Plus, it did generate cash that can be used to retire AJXA in April. That said, as can be seen in the above price chart, the market reacted negatively to the merger being cancelled. AJXA fell too but not as much and has recovered since. It seems to me that a merger with the stronger Ellington Financial would have lowered the defaults risk for this Note, though I see that cancellation as only moving the needle slightly.

So the analysis now turns to whether the Notes will be redeemed or not.

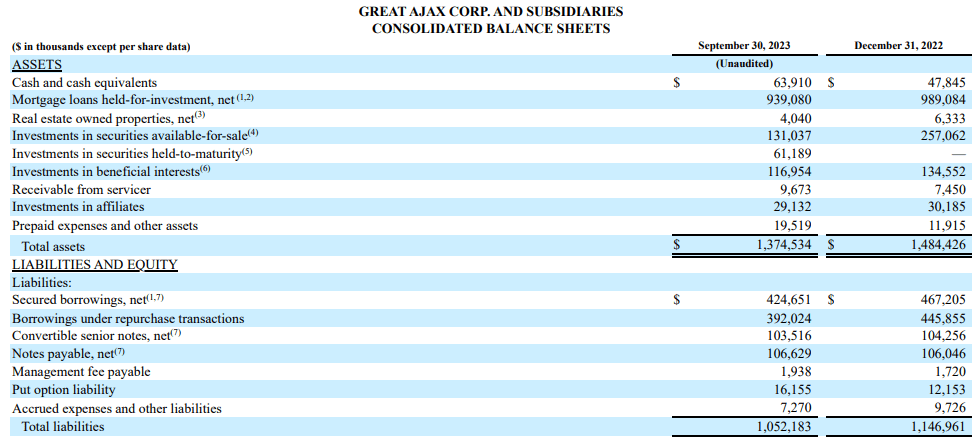

AJX's recently released quarterly results were “positive”. By that, I mean, although they recorded their sixth straight quarterly loss, the $.25 loss was the smallest of the six! Critical to the Note holders, the GAAP book value was $11.07 per common share at the end of September, down $.79 over the quarter. The decrease in book value was driven primarily by the increase in outstanding common shares. Data shows the book value was over $16 in December 2021. While that is concerning long-term, not before the Notes mature in my view. That said, one has to wonder why EFC walked away from a merger price 40% below the book value.

The most recent Balance Sheet (less Equity details) shows $63m in cash on hand, which does not include the $5m from the merger cancellation payment.

{kind=link}

d18rn0p25nwr6d.cloudfront.net/CIK-0001614806/3d519028-5239-460c-b184-92e2b3e0cac1.pdf

Potentially sources of cash would include $131m listed as investments available to sale. AJX list two preferreds on the Balance sheet which apparently do not trade in the market, most likely private placements. Issuing additional shares there or floating a new Note are other means of funding AJXA's maturity payments. Since non-payment would require a bankruptcy filing, I would rate it unlikely and AJAX holders will be paid on time.

Return comparison

As noted, a 5-month CD yields about 5.4% currently. My estimate of the YTM for AJXA is around 12.2%, almost 680bps above the CD! That does tell me the market might not be convinced as that spread is wider, by far, that the other comparisons I have done.

For risk-takers, the YTM is very attractive and rates a Buy. Today's Bid/Ask spread is only $.09, but there is almost no volume, and the recent average is under 3.5k, which could hamper establishing a meaningful position. For more conservative investors, I cannot get "if it seems too good to be true, it isn't" off my mind.

The next chart provides some idea how the YTM will move with price and time.

Author's YTM XLS

Portfolio strategy

Each investor, based on their own portfolio’s risk profile and where that matches up against their acceptable risk level, is this a TGTBT trade or a situation waiting to be exploited. The other consideration is the short length does entail a high YTM, but little money gained per Note held, estimated around $150. Point being, trying to amass a meaningful position that generates a large net cash gain could be hard with the low average trading volume for AJXA. The other thing to consider again is the short time frame of this trade, which has both good and bad points for the same reason: interest rates. If the effect of the interest-rate curve peak in the spring, this Note matures at a perfect time. If bonds start responding before that, the investor has funds committed that could have deployed into a longer duration investment. Yes, they can sell, but remember trading volume is minimal.

So while I see defaulting on the Note as remote, the ability to execute a decent size trade has me at Hold for buying AJXA.

Final thoughts

Here are the links to the articles that did a similar analysis, comparing a risky asset to a CD.

- WCC 'A' Preferred Vs. CD: I Chose The Preferred With the current YTM below 6%, I would pass on this trade now.

- IBHF Or 3-YR CD: I've Decided Which Is Better I still like this trade as the price hasn't moved much since publication.

For further details see:

AJXA: Failed Merger Raises Risk For This Note That Matures Next April