AKAM - Akamai: Caution Warranted Despite Accelerating Growth

2023-12-21 23:13:16 ET

Summary

- Akamai's stock rebounded in 2023 due to improved sentiment towards growth stocks and solid performances from its security and compute businesses.

- Competitors like Fastly and Cloudflare appear to have an advantage in edge computing that may limit Akamai's long-term success.

- Akamai's stock is beginning to look expensive, given that the company's technology lags peers and investment requirements are likely to be high in coming years.

Akamai's ( AKAM ) stock rebounded sharply in 2023 and is now near the highs of 2021 and early 2022. This appears to be the result of improved sentiment towards growth stocks, stabilizing market conditions and solid performances from Akamai's security and compute businesses.

While Akamai is likely to do well in the near-term, just based on its distribution footprint and existing customer relationships, I am not convinced by the company's cloud strategy or technology. Competitors like Fastly ( FSLY ) and Cloudflare ( NET ) appear to have a distinct advantage in edge computing that will likely limit Akamai's long-term success. If this proves to be the case, Akamai's stock is likely to perform poorly from current levels.

Market

While it is too early to know whether Akamai's end markets are rebounding, there are signs of stabilization, although the data is mixed. Akamai has suggested that many companies remain cautious. The company has also observed a small increase in bankruptcies, but this has not had a significant impact, particularly in relation to its security business.

F5 ( FFIV ) stated on its fourth quarter earnings call that the demand environment has shown signs of stabilization, particularly amongst enterprise customers. F5's technology and financial services customers were areas of strength in the fourth quarter.

Cloudflare remains cautious in the face of geopolitical uncertainty and mixed macroeconomic data. Demand for Cloudflare's data storage products is strong and the company is excited about the potential of AI inference workloads. Of note, Cloudflare observed a significant increase in massive DDoS attacks in the third quarter.

Fastly's third quarter earnings call was surprisingly pessimistic, with the company stating that customers are still tightening their budgets . Some deals are taking longer to close as they are receiving more scrutiny. Fastly saw several key deals slip out of the third quarter, although this was not material.

Competition

Akamai doesn’t believe that there has been any fundamental change in the market, in regard to either competition or pricing. Given the deterioration of Akamai's gross profit margins, despite the expansion of its security and compute businesses, it is hard not to feel that Akamai is facing pricing pressure though.

Fastly has made significant strides in controlling its costs, improving the productivity of its infrastructure and negotiating better bandwidth pricing as its business scales. This hasn't provided any benefit to its margins, though, as gains have been passed through to customers in the form of lower prices.

Consolidation appears to be occurring within the CDN market at the moment as a result of competition and pricing pressure. This should be supportive of growth for Akamai's delivery business, but it remains to be seen whether this improves the economics of content delivery.

Akamai has traditionally been more of a hardware focused infrastructure company, and it is questionable whether it has the software expertise to be competitive in security and edge computing. Akamai has scale, but its network is based on an outdated architecture.

Akamai

While Akamai's background is in content delivery, its future lies in security and edge computing. Akamai Connected Cloud is a distributed platform for cloud computing, security and content delivery. It combines Linode's 11 core data centers with Akamai's 4,100 edge computing locations. This allows workloads to run closer to end users, reducing latency and data sovereignty concerns.

Akamai believes that it is differentiated by the fact that its data centers are integrated with its edge platform. This is in contrast to Cloudflare, which is positioning itself as a connectivity cloud rather than a fourth hyperscaler.

Given the scale and maturity of the hyperscalers, it is difficult for companies to compete directly with them though. Edge computing offers advantages, but I expect it will be more of a niche solution that capitalizes on these advantages, rather than a direct competitor. For these reasons, I think Cloudflare's strategy makes more sense than Akamai's.

Akamai is pleased with the progression of its cloud and edge computing platform so far and is continuing to invest in product development and infrastructure to support this business. Akamai has opened 13 compute regions in 2023, adding to the 11 it acquired from Linode. Akamai is still investing in its PoPs , making them capable of running containers, VMs and Kubernetes. Akamai is also still growing its marketplace, adding to the tools that are available to customers. This suggests that Akamai's compute business is still fairly nascent though.

Running inference could be an important use case for edge networks and a growth driver for Akamai in coming years. Akamai has already had several partners port their inference engines to its platform. It feels like Akamai's efforts in this area are immature though. The company plans on running inference workloads on CPUs, stating that this is more cost-effective than trying to procure GPUs. This stands in stark contrast to Cloudflare's heavy investment in GPUs to support inference. Cloudflare already has inference-optimized GPUs running in 75 cities and plans on hitting 100 cities by the end of 2023. While leveraging CPUs for AI may lower CapEx, it is likely to result in dramatically higher operating costs if inference workloads genuinely begin to scale.

Akamai’s content delivery business was supported by increased traffic growth in the third quarter. Akamai also benefitted from the recent acquisition of enterprise customer contracts from StackPath and Lumen Technologies, after they decided to exit the content delivery business. This provided Akamai with over 200 net new customers. Akamai expects the transactions to add approximately 17-20 million USD revenue in the fourth quarter and 60-70 million USD revenue in 2024. There is also potential upside if Akamai can successfully sell security and compute solutions to these customers. Akamai will incur costs associated with these customers though, which is expected to be roughly a 1% gross margin headwind. The StackPath contract had an upfront free of around 35 million USD, along with a small earnout. The Lumen contract had an upfront fee of 75 million USD with no earnout.

Security is now Akamai's largest segment, with the company offering solutions across infrastructure, application and zero-trust security. Akamai’s Guardicor segmentation production is now at a 100 million USD annualized run rate, a 97% YoY increase, driven by the demand for protection against malware and ransomware. Most of the growth in Guardicore has come from outside Akamai's installed base . Micro segmentation is a network security approach where granular network security zones are constructed to separate and protect workloads. Akamai's segmentation solutions protect against ransomware and data exfiltration attacks and provides visibility into internal infrastructure. There is also reportedly solid demand for Akamai’s web application firewall solution and strong interest in Akamai’s API security solution.

Financial Analysis

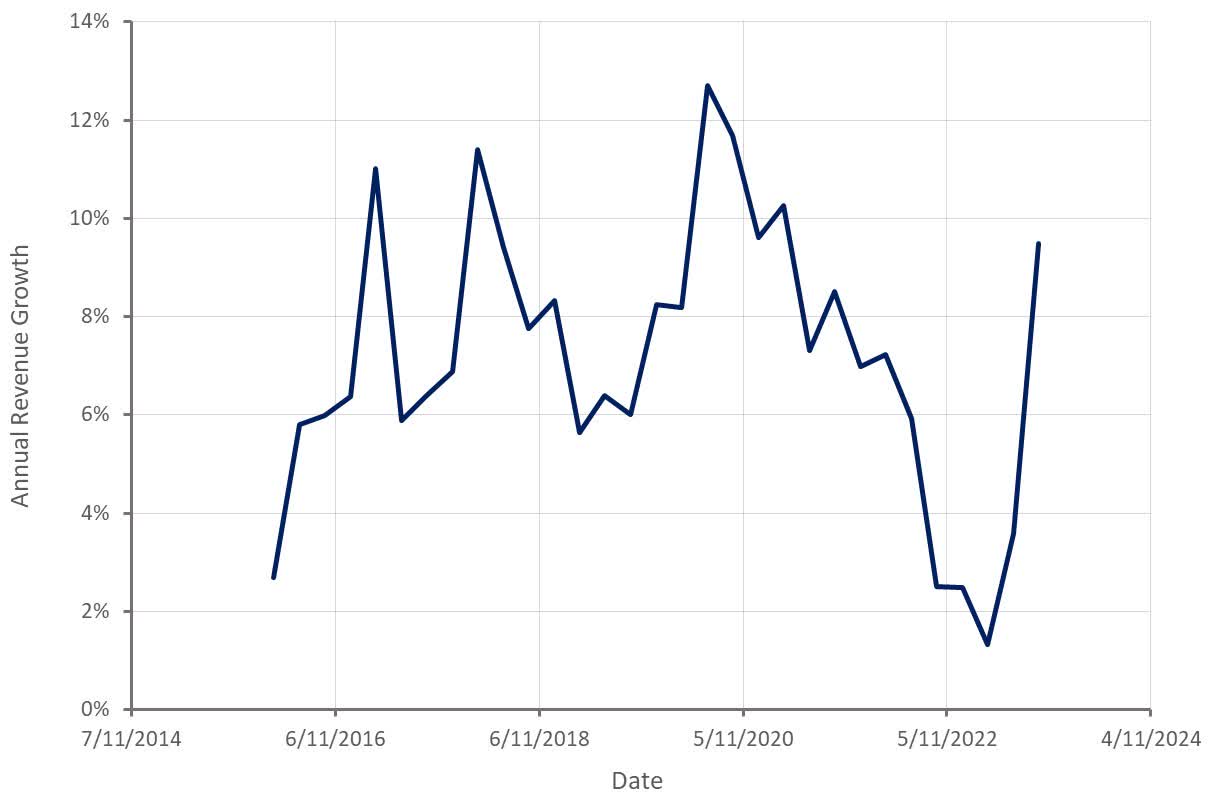

Akamai’s third quarter revenue was 965 million USD , a 9% increase YoY. There was 10 million USD in one-off benefits in the third quarter though, without which growth would have only been around 8%. Security revenue was up 20% YoY to 456 million USD and compute revenue increased 19% YoY to 130 million USD. Delivery revenue was 379 million USD, declining 4% YoY despite Akamai benefitting from roughly 4 million USD revenue associated with CDN customer contracts acquired from StackPath.

Fourth quarter revenue is expected to be 985-1,005 million USD, a 6-8% increase YoY. This appears slightly conservative given that growth has been accelerating and there is a substantial tailwind associated with acquired customer contracts.

Figure 1: Akamai Revenue Growth (source: Created by author using data from Akamai)

{kind=link}

Figure 2: Job Openings Mentioning Akamai in the Job Requirements (source: Revealera.com)

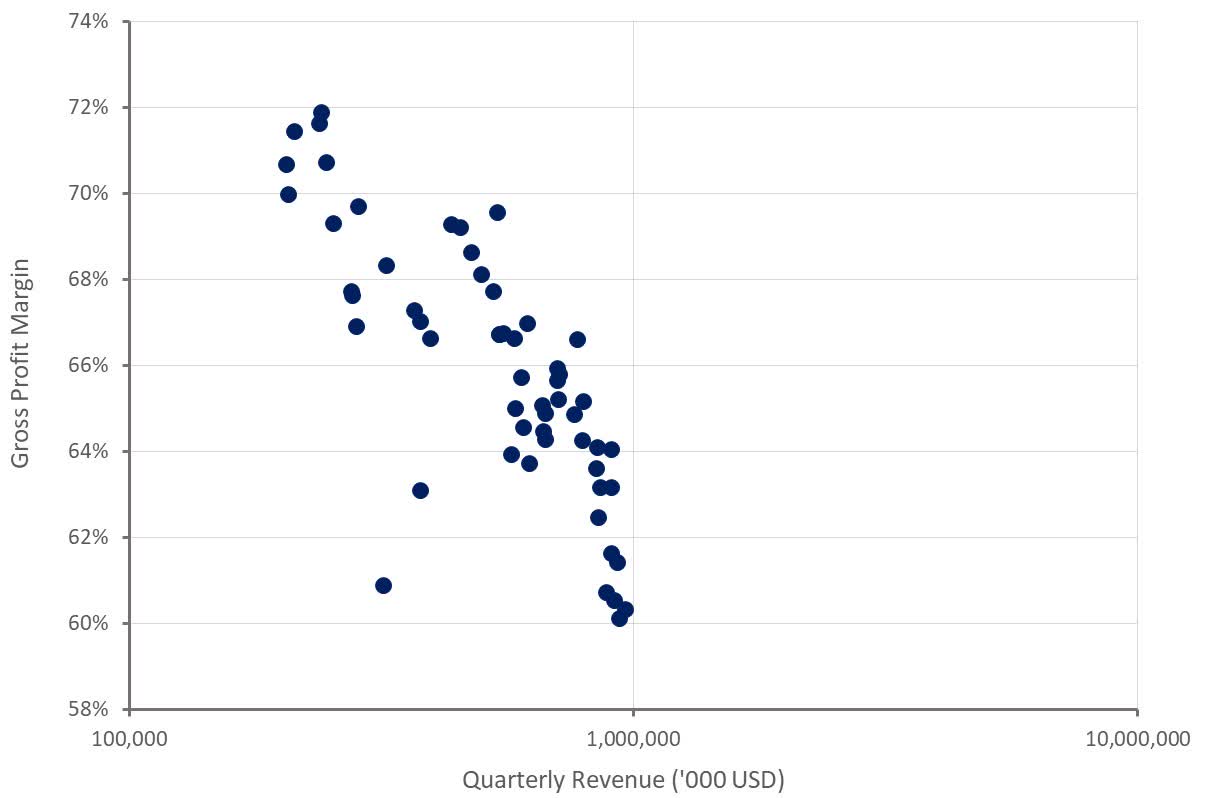

Akamai's gross profit margins continue to decline, which is somewhat surprising given growth of what should be high margin security and compute revenue. Akamai has been investing heavily in infrastructure though, which may be depressing margins until the compute business scales further. Third quarter margins were also depressed by costs associated with the acquisition of customers from StackPath.

Akamai has been migrating workloads from third-party cloud vendors to its internal cloud platform. As a result, Akamai's third-party cloud spend declined 26% YoY in the third quarter. This is potentially important as Akamai's cloud spend was in excess of 100 million USD before beginning insourcing.

Figure 3: Akamai Gross Profit Margin (source: Created by author using data from Akamai)

{kind=link}

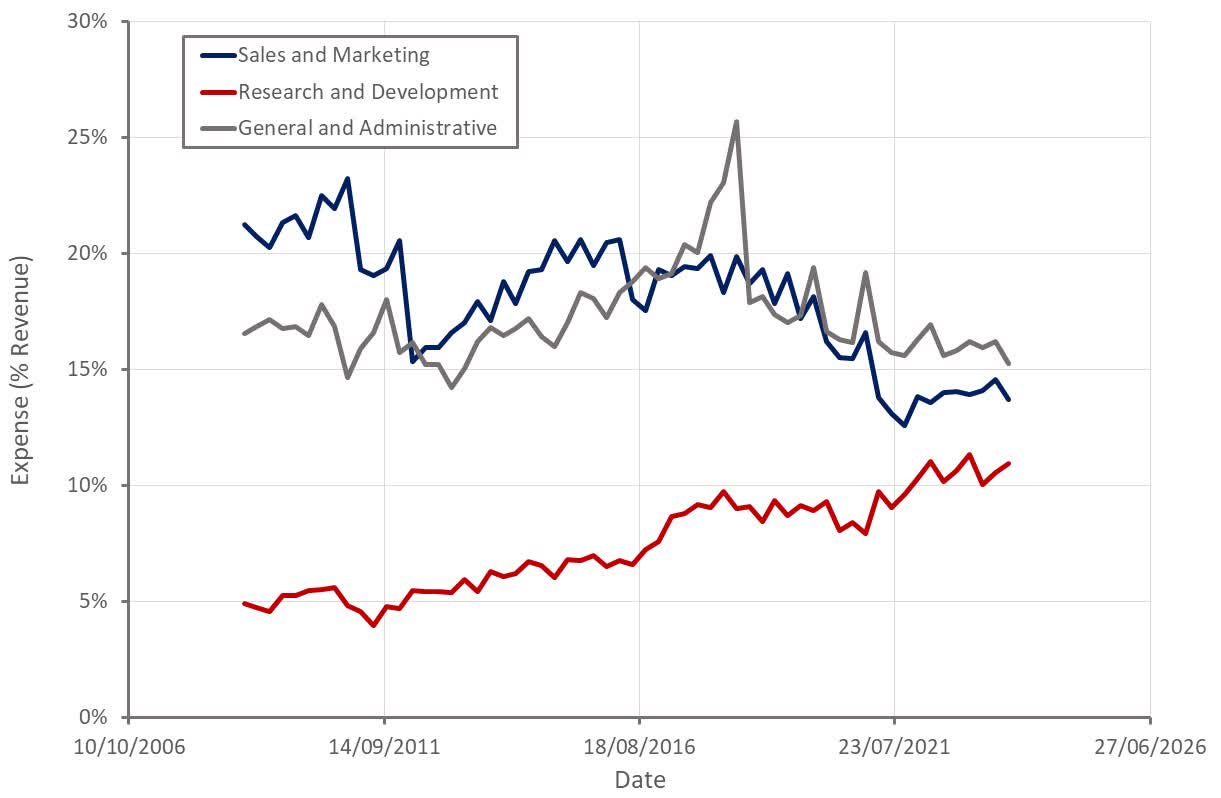

The expansion of Akamai's services has required greater investment in R&D, which is a headwind to operating profitability. The burden of Akamai's sales and marketing and general and administrative expenses continue to decline though.

Figure 4: Akamai Operating Expenses (source: Created by author using data from Akamai)

{kind=link}

While Akamai's operating profitability has rebounded somewhat in recent quarters, I expect margins to remain under pressure in the near-term. Akamai's gross profit margins have been declining and Akamai will need to continue to invest in R&D and sales and marketing to support its newer businesses.

Conclusion

The rising importance of security and compute will likely turn Akamai from a leader in its most important market to just one of many competitors. While there is now a larger growth opportunity, Akamai's margins are likely to be pressured by a less favorable competitive position and greater investment requirements. From an absolute perspective, I think Akamai's stock still represents reasonable valuable at current prices, but there are a large number of stocks with better prospects that are more attractively priced.

{kind=link}

For further details see:

Akamai: Caution Warranted Despite Accelerating Growth