AKAM - Akamai: Positioned For Future Growth But Current Price Lacks Appeal

2023-10-20 16:59:29 ET

Summary

- AKAM has demonstrated resilience and growth in a challenging global economic landscape, particularly in the face of pricing adjustments in the content delivery network segment.

- AKAM's emphasis on security, strategic acquisition of Guardicore, and the introduction of AI-driven security solutions highlight its adaptability and strength in the security domain.

- However, I recommended a hold due to a lack of margin of safety.

Investment action

Based on my current outlook and analysis of Akamai Technologies, Inc. ( AKAM ), I recommend a hold rating. While AKAM is undeniably a high-quality stock with a bright future, its present share price doesn't offer enough margin of safety in my view. Navigating through global economic challenges, AKAM posted admirable results in the second quarter of 2023. A significant portion of its earnings were attributed to the security and compute segments. Although there was a downturn in content delivery network revenue, possibly due to earlier pricing adjustments, there's a discernible trend towards pricing stabilization. AKAM places great emphasis on the strategic role of its delivery business, tapping into its expansive delivery network to bolster its security initiatives. The acquisition of Guardicore and the debut of an AI-driven API security solution are testaments to AKAM's commitment to innovation and top-tier security. The company's upward revision in its revenue guidance underscores both its strong market position and the management's confidence and optimism about the future.

Basic Information

AKAM is a global leader in content delivery network [CDN] services and cloud security solutions. The company's primary mission is to ensure fast, reliable, and secure delivery of digital content, applications, and services over the internet. AKAM's platform is one of the world's largest distributed computing systems, leveraging a vast network of servers to accelerate and optimize content and application delivery. This helps businesses provide a seamless and high-quality user experience to their customers, regardless of device, location, or network conditions. Akamai also offers a suite of cloud security solutions to protect websites, applications, and data centers from cyber threats. Over the years, Akamai has expanded its product portfolio to address the evolving needs of enterprises as they navigate the complexities of the digital landscape.

For the past six years, AKAM has consistently demonstrated strong growth, maintaining an average growth rate of 8%. However, in 2022, growth dipped to 4%. This decline can be attributed to several global challenges, including the persistent effects of the COVID-19 pandemic, the conflict in Ukraine, and escalating inflation. These events curtailed Akamai's business momentum, as many companies scaled back their IT expenditures. Nevertheless, the management remains optimistic about the forthcoming quarters in regards to revenue growth, which I will delve into in subsequent discussions.

Review

During the second quarter of 2023, AKAM showcased robust performance even amidst worldwide economic hurdles. The firm reported revenue of $ 936 million , marking a 4% increase from the previous year, a figure that remains consistent even after adjusting for foreign exchange fluctuations. In this quarter, the revenue from security and compute constituted 59% of the total earnings, reflecting 14% annual growth, or 15% upon adjusting for foreign exchange.

In line with expectations, AKAM's CDN revenue saw a decrease, which can be attributed to a significant price reduction that occurred in the first half of 2022. This pricing shift has had a pronounced impact on the CDN segment. However, there are emerging signs of stabilization in the pricing landscape. AKAM has noted a moderation in pricing declines, particularly among their larger clientele, suggesting a plateau in aggressive price cuts from the past. Additionally, there's been a sequential increase in traffic, which is a positive indicator as higher traffic can lead to augmented revenues, even if prices per unit are lower. AKAM emphasizes the strategic value of its delivery business, encompassing CDN. The company capitalizes on economies of scale and the invaluable data derived from its expansive delivery network, which is pivotal for their security ventures. Their dominant stance in the delivery market provides them with a competitive edge, especially in the prevailing macroeconomic climate characterized by tighter funding. The broader economic environment has introduced challenges, especially in traditional web sectors like commerce. AKAM projects that these challenges might require a year or more to fully stabilize. In essence, while the CDN sector has encountered hurdles, AKAM is identifying positive trends that hint at a more optimistic outlook in the upcoming period.

AKAM's strategic acquisition of Guardicore has proven to be a significant asset. Guardicore, a segmentation solution, has garnered attention from global entities, including a prominent insurance company in France and Telstra, Australia's leading telecom provider. This solution has been pivotal in assisting businesses to adhere to regulatory standards and bolster their security measures. In addition to Guardicore, AKAM has launched an innovative API security product. This product, powered by AI-based analytics and threat hunting capabilities, is crucial for detecting, analyzing, and safeguarding APIs against potential vulnerabilities and threats. Notably, this product operates independently of AKAM's CDN, underscoring AKAM's adaptability and prowess as a standalone security provider.

Web Application Firewall [WAF] and bot management are integral components of AKAM's security suite, playing a vital role in intercepting and neutralizing cyber threats, thereby enhancing their clients' overall security framework. AKAM's security growth trajectory has been on an upward curve, with a marked uptick in the number of customers opting for their security solutions. The company has successfully penetrated diverse sectors, including education and government, primarily through offerings like Guardicore. Reflecting their confidence in the security business's future, AKAM has revised its security revenue growth guidance upwards, now projecting a growth rate of 12%–14%, up from the earlier forecast of 10%–12%. This optimistic outlook, backed by robust product performance and strategic initiatives, paints a promising picture for AKAM's stakeholders and investors. Regarding overall revenue, management has expressed optimism and increased revenue guidance to a range of $3.76 million to $3.79 million.

Valuation

I'm optimistic that AKAM can achieve high single-digit growth over the next two years for several reasons. First, AKAM delivered strong results in the second quarter, even in the face of global economic challenges. Second, while there was a decline in CDN, the management highlighted stabilizing pricing trends and a quarter-over-quarter traffic boost. These positive indicators suggest a positive outlook for AKAM. Third, AKAM's acquisition of Guardicore and its cutting-edge API security product, enhanced with AI-driven analytics and threat detection, has set them apart in the market. This is evident from the surge in customers choosing their security solutions and their successful penetration into various sectors. The upward revision in the security revenue outlook, driven by Guardicore's success, further underscores their confidence and positive outlook. For 2023, my projections align with the guidance provided by AKAM's management. For 2024, my estimates are consistent with market consensus. Furthermore, considering the strengths highlighted, I anticipate that AKAM's revenue will trend towards its six-year historical average growth rate of approximately 8%.

{kind=link}

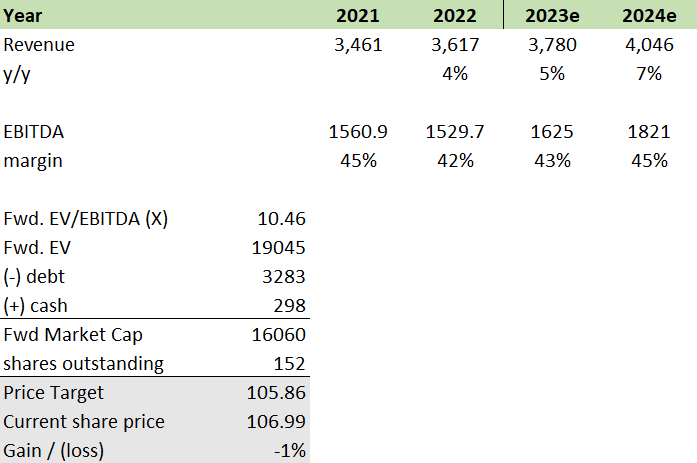

Currently, AKAM trades at approximately 10.4x forward EV/EBITDA, while its peers have a median trading value of 54.20x. This significant difference in valuation is primarily attributed to the anticipated next twelve months growth rate: AKAM's peers are projected to grow at 35%, in contrast to AKAM's 9%. However, on the brighter side, AKAM boasts a net margin of 16.79%, which is commendable compared to its peers' negative 12.11%. In the tech sector, the metric of revenue growth is often prioritized. Shareholders and investors tend to value revenue growth and market share expansion over immediate profitability, explaining the higher forward EV/EBITDA of AKAM's peers. My price target for AKAM stands at approximately $105.9, indicating no potential for capital appreciation. Based on this analysis, I recommend a hold rating for AKAM.

Risk and final thoughts

A potential risk to my hold recommendation is an improvement in macroeconomic conditions. Should inflation decrease more than expected, the Federal Reserve may cut the Federal Funds Rate [FFR]. The FFR plays a pivotal role in shaping downstream interest rates. A reduction in interest rates typically spurs tech spending. Such a scenario could propel AKAM's revenue growth beyond current projections. If AKAM manages to elevate its revenue growth closer to its peers' rate of 35%, its forward EV/EBITDA of 10.46x could see a substantial rise, potentially aligning with its peers' level of 54.20x.

AKAM displayed resilience and growth during a challenging global economic landscape. While the CDN segment saw a decline due to earlier pricing adjustments, there are clear indications of stabilization in pricing. The company's strategic acquisition of Guardicore and the introduction of innovative products, such as the AI-powered API security solution, underscore AKAM's adaptability and strength in the security domain. Their offerings, including WAF and Bot management, have fortified their security suite, leading to increased customer adoption across diverse sectors. With a revised upward security revenue growth projection and an optimistic overall revenue guidance, AKAM's future trajectory appears promising. AKAM is undeniably a high-quality stock with a positive outlook for the future. However, its current share price aligns with my target price. Despite its promising prospects, the absence of a margin of safety and the lack of potential upside lead me to recommend a hold rating for the time being.

For further details see:

Akamai: Positioned For Future Growth But Current Price Lacks Appeal