AKAM - Akamai Technologies: Business Model Transition Could Be Transformative

2023-11-01 08:53:13 ET

Summary

- Akamai’s revenue has grown at a CAGR of 9%, as its Delivery segment experiences a decline due to competition. Offsetting this is an impressive performance by its Cybersecurity and Compute.

- Both segments have been developed by the company’s deep expertise and supportive M&A. We see a long trajectory over an extended period of time due to industry tailwinds.

- Akamai is performing well relative to its peers, although is lacking growth. We believe the coming 2-4 years will be critical to transitioning the business into a better growth company.

- Akamai’s valuation does not suggest an upside currently, trading in line with its historical average multiple and a sufficient discount to peers.

Investment thesis

Our current investment thesis is:

- Akamai is a market-leading business, with deep expertise and a quality business model. The company is transitioning toward Cybersecurity and Edge Computing, with execution thus far being exceptional.

- We believe these segments will continue to grow at 10-20% consistently in the coming years, with an overall performance of 5-10% (Weighted down by Delivery). Following FY26, we suspect the Group's growth will improve as Delivery is sufficiently diluted.

- Margins and FCF continue to be highly attractive, needing an improvement in growth to accelerate shareholder returns.

- Akamai's valuation does not suggest an upside in our view so investors should remain patient for future opportunities.

Company description

Akamai Technologies, Inc. (AKAM) is a leading cloud services and cybersecurity solutions provider headquartered in Cambridge, Massachusetts. Founded in 1998, Akamai has become a key player in the technology industry.

Share price

Akamai's share price performance has been respectable during the decade, returning over 100% to shareholders while the S&P has exceeded 170%. This is due to solid financial development during this period, allowing the company to improve its value.

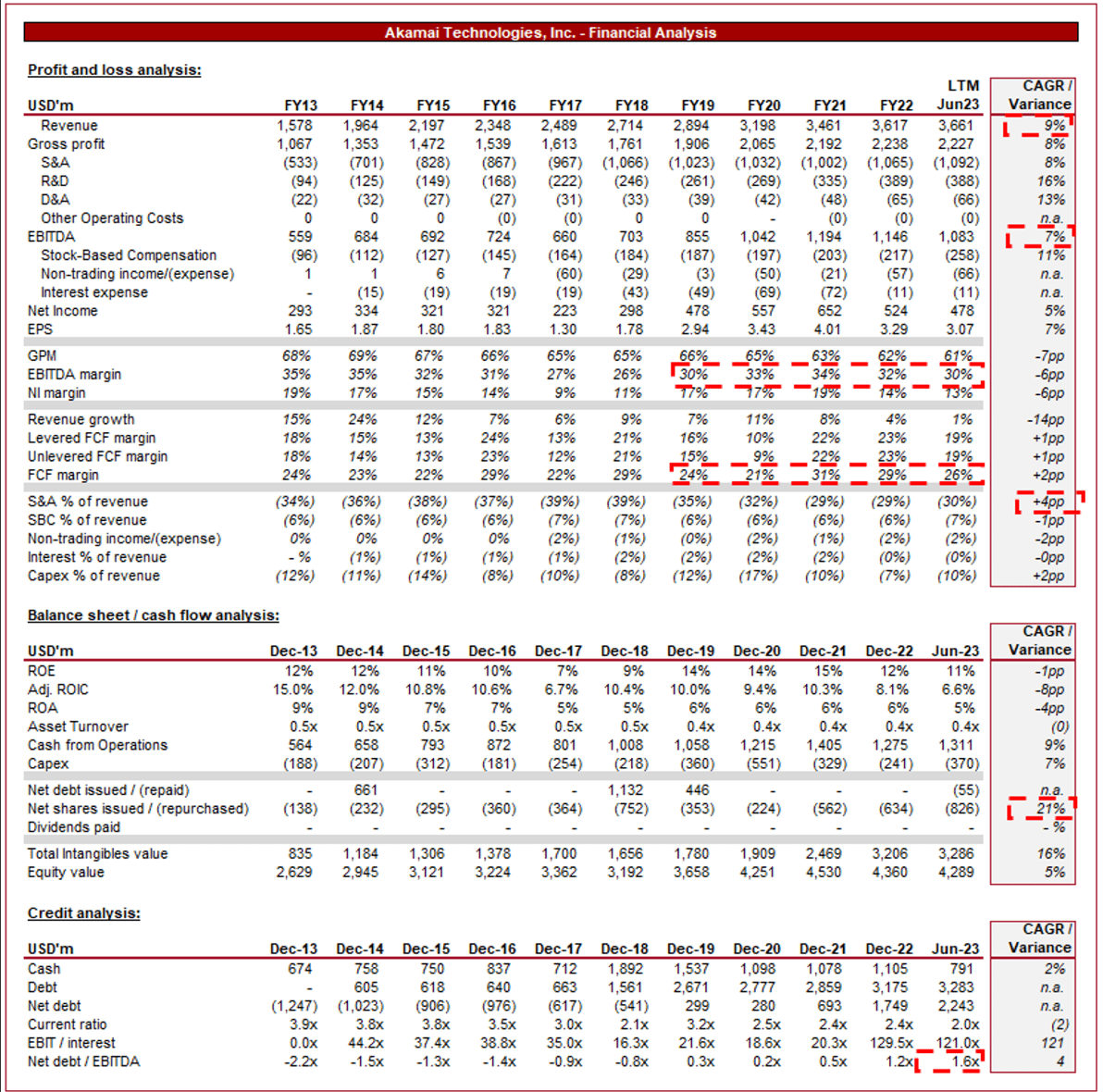

Financial analysis

Akamai financials (Capital IQ)

{kind=link}

Presented above are Akamai's financial results.

Revenue & Commercial Factors

Business Model

Delivery

Akamai operates one of the world's largest and most advanced content delivery networks. This network consists of strategically located servers and data centers worldwide. The primary function of the CDN is to optimize the delivery of web content, ensuring it reaches end-users quickly and efficiently. This is critical for businesses looking to provide a seamless online experience to their customers. This is the core service provided by Akamai, although its growth has been lackluster in recent years. Akamai has faced intense competition and its response has been mediocre, contributing to a loss in market share.

IDC Market Content Delivery Network (Akamai)

With the proliferation of digital content, streaming services, and e-commerce, the demand for fast and reliable content delivery has surged. Akamai's CDN and media delivery solutions are well-positioned to meet this demand, despite the softening interest in its services ("A rising tide lifts all boats").

For this reason, and Akamai's inherent attractive proposition (despite competition), we suspect demand will remain broadly resilient.

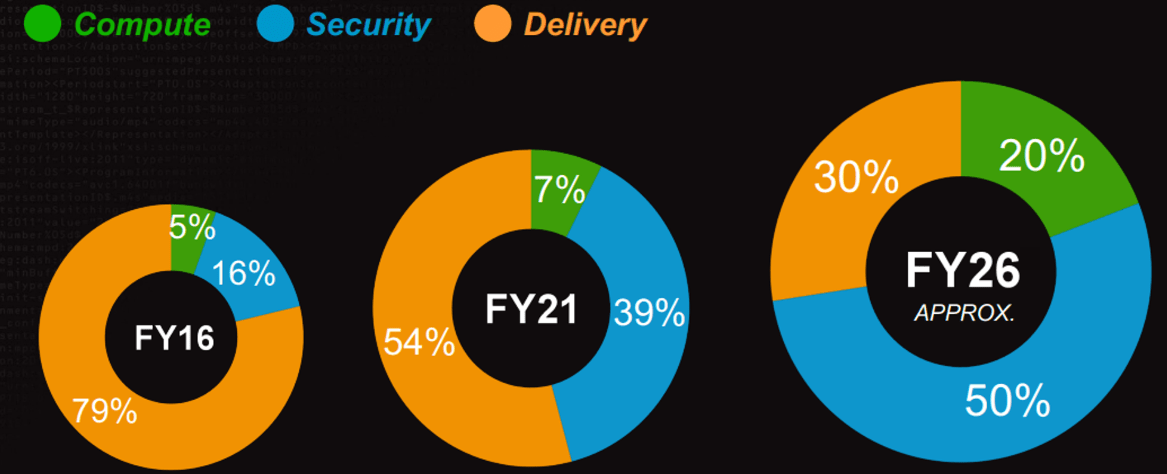

The company's response has been to diversify, seeking new growth opportunities to improve its current trajectory. As the following illustrates, the target is for Delivery to decline to 30% of revenue by FY26F.

{kind=link}

Security

Akamai offers a comprehensive suite of cloud security solutions designed to protect websites, applications, and infrastructure from a wide range of cyber threats, including DDoS attacks, web application attacks, and data breaches.

Akamai collects vast amounts of data from its network, which it leverages to provide security intelligence. This data-driven approach helps organizations proactively identify and mitigate emerging threats. The rise of AI and in particular, GenAI has the potential to bring significant improvements to Akamai's capabilities.

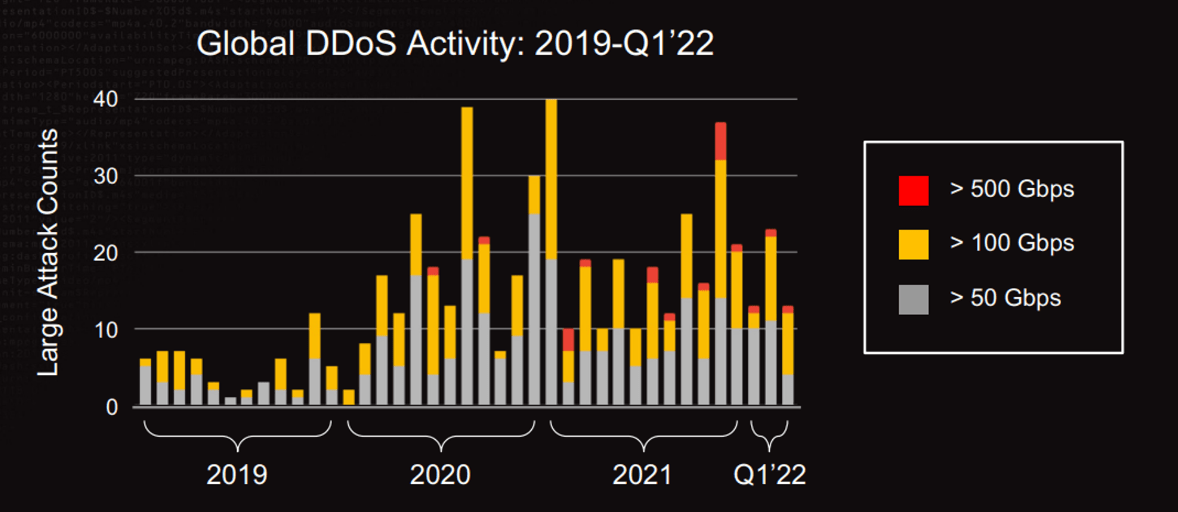

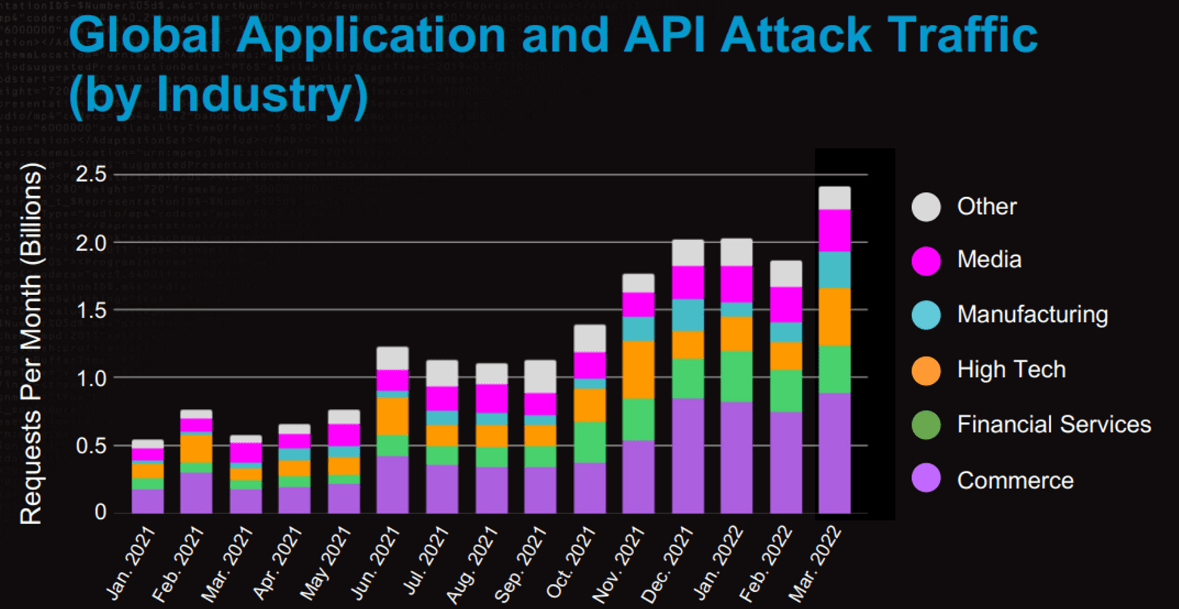

The threats from breaches have consistently grown, as corporations and society as a whole continue to move sensitive and valuable data online. IBM estimates that a data breach costs on average $4.5m , with many estimates in excess of this amount.

The following data points speak for themselves, and the situation will only get worse over time. As cyber threats become more sophisticated and frequent, the demand for cybersecurity services will only increase (and prices will likely follow).

{kind=link}

{kind=link}

{kind=link}

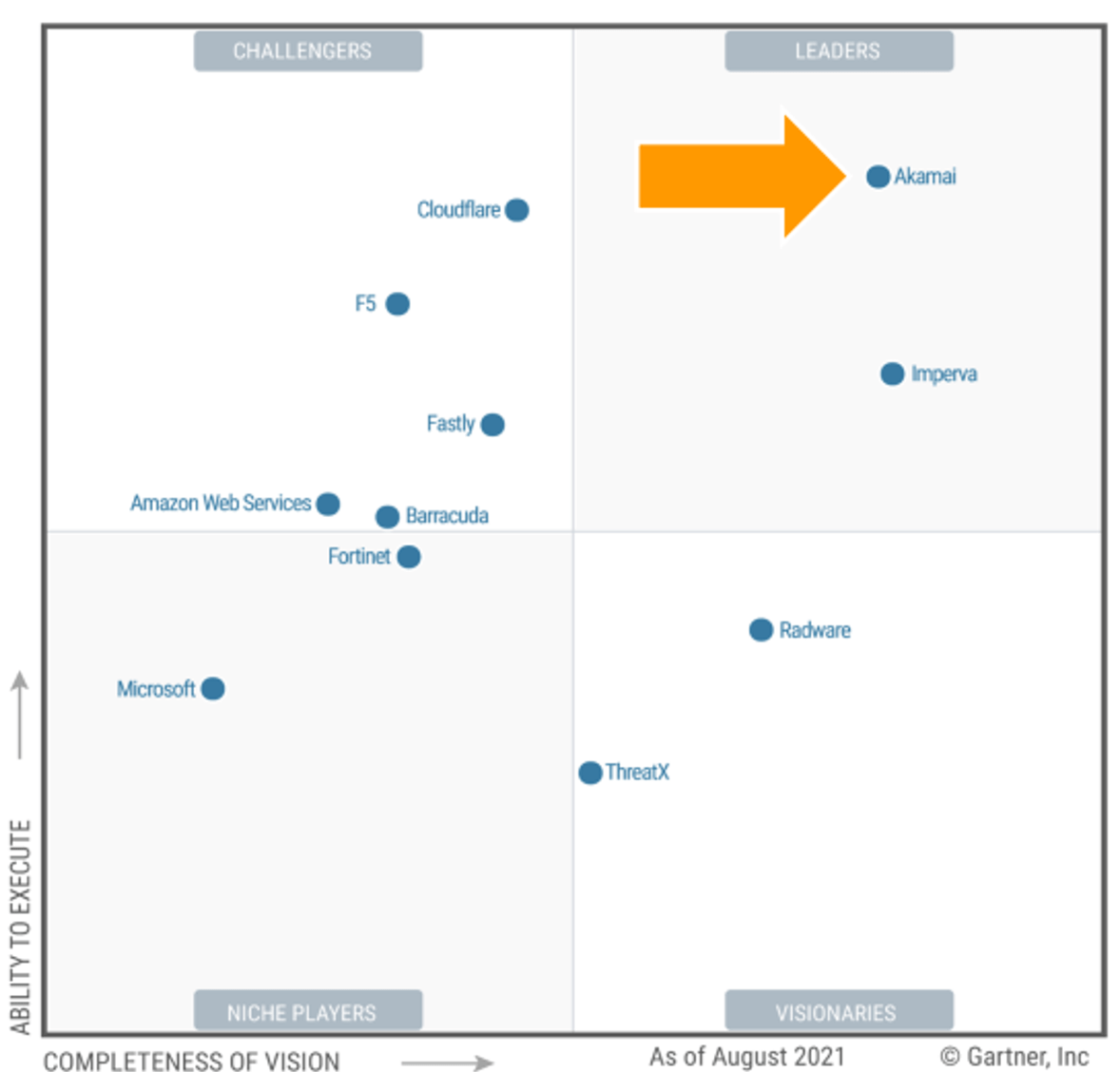

Akamai has impressive expertise and capabilities in this area, receiving an impressive rating from Gartner as part of its Web Application and API Projection Magic Quadrant. This supports Management's ability to execute growth focused on cybersecurity. Thus far, Management estimates that the Security segment has grown at a 5Y CAGR of ~20%, far exceeding Delivery (-4%-0%).

{kind=link}

Compute

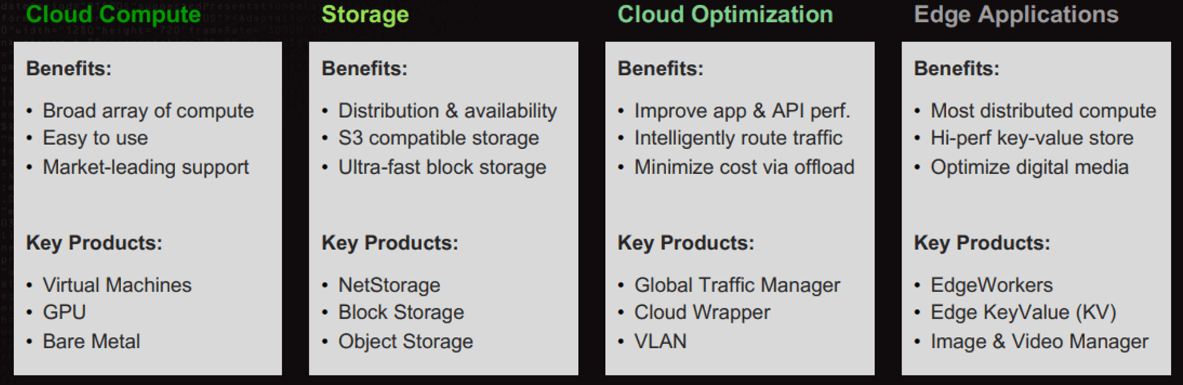

In addition, Akamai is expanding its "Compute" segment, which is estimated to have grown at a CAGR in excess of +30%. Akamai leverages its network infrastructure to bring computing closer to end-users. This reduces latency and enhances the performance of applications that require real-time processing.

The shift towards edge computing has been driven by IoT and real-time applications, with technological development trending toward increased demand for these services. As the following illustrates, Akamai has a comprehensive suite of services.

{kind=link}

Operations

Underpinning the company's repositioning efforts is M&A. Management is not only acquiring similar companies to supplement growth but also to acquire the expertise necessary to execute its strategic goals. In the last decade, the company has spent over $2.7bn of cash, with the most important being Linode. Linode is a cloud hosting service business, that was acquired to support Akamai's Compute segment, allowing it to build its own cloud and edge computing segment.

Akamai operates on a subscription-based model, where customers pay for the services they require. This model fosters recurring revenue and long-term relationships with clients. Over time, Akamai is positioned well to increase existing prices, benefit from industry tailwinds via usage, and focus on winning new customers (rather than replacements).

This is an interesting period for Akamai. The company is seeking to transform its business model but in a controlled and intelligent way. We do not see significant risk associated with this (risk to financial performance) despite the fundamental shift in services provided. The steps taken by Management appear correct, with great acquisitions in our view. By leveraging its wider network and expertise, it de-risks the transition.

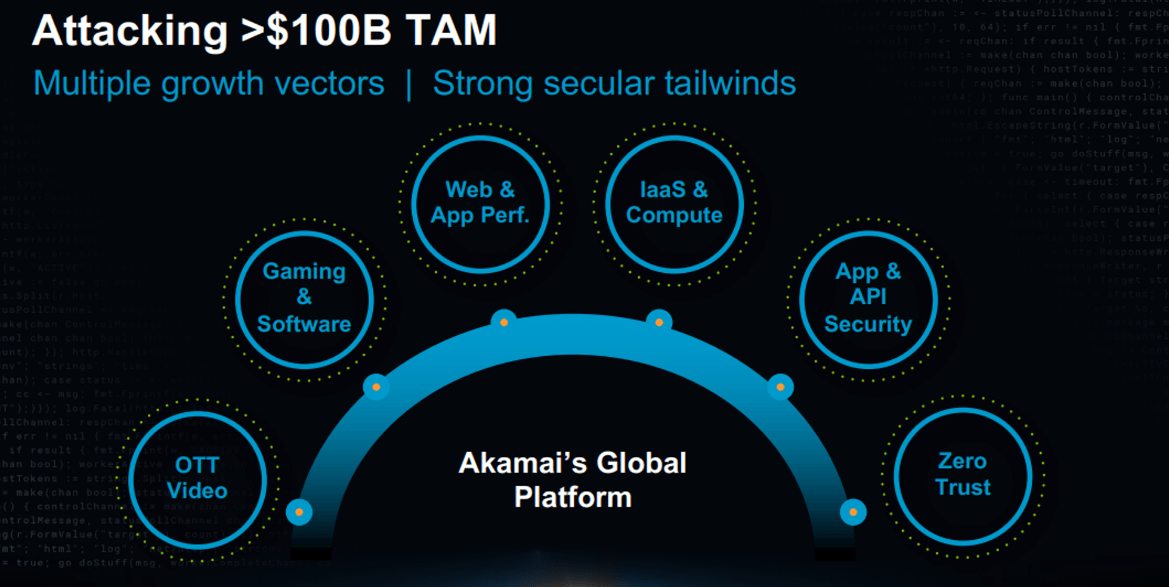

Management estimates that its new TAM is >$100bn and we believe improved growth is possible, with a conservative view implying the company can improve from its current c.7-9% trajectory to 10-15% (only) once Delivery shrinks as a portion of revenue. In the meantime, however, a continuation is reasonable.

{kind=link}

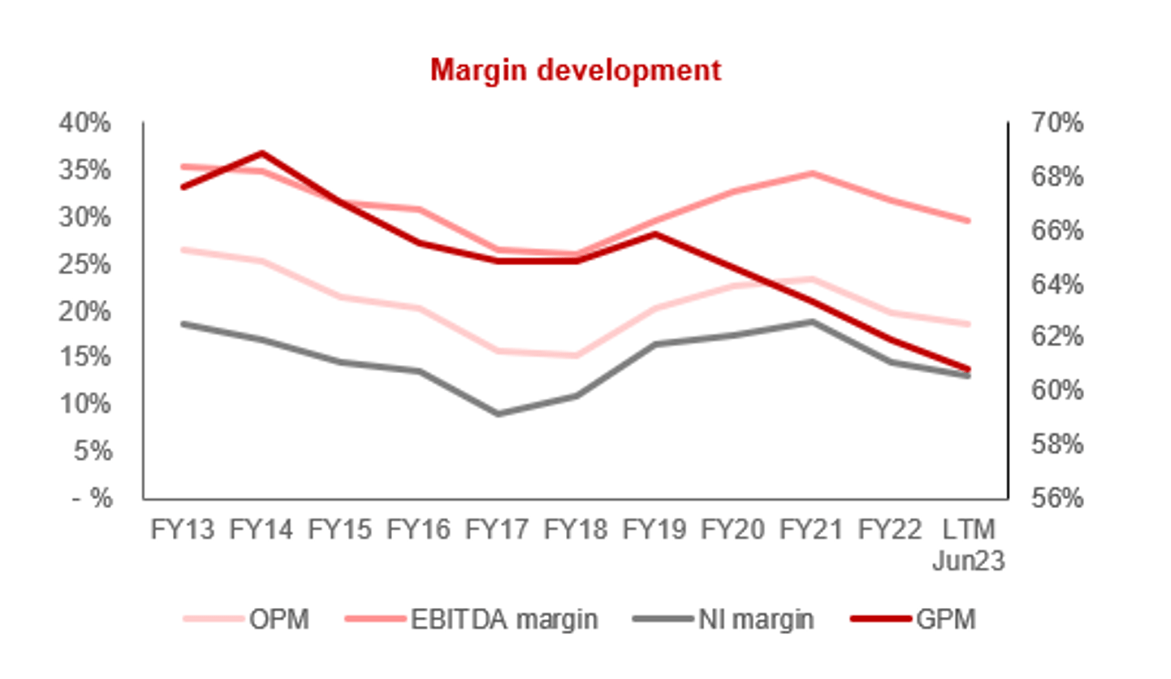

Margins

{kind=link}

Akamai's margins have remained broadly flat during the historical period, although the company has experienced a noticeable drop in the most recent few quarters. This is in large part FX, with Non-GAAP Net income increasing +5% (exceeding revenue).

Q2

Key takeaways from Akamai's Q2 are:

- Top-line revenue growth was 4%. Security revenue growth of 14%, Delivery decline of (9)%, and Compute growth of 16%. Much of this growth is driven by International markets, implying global expansion efforts are bearing fruit.

- The company is seeing benefits from operational efficiency. Net Income decline of (7)%, although +5% when adjusted for FX.

- Management has raised its earnings guidance for the remainder of the year, implying no concerns.

Overall, the business is progressing well with transitioning its services, with no hint of a slowdown.

Balance sheet & Cash Flows

Akamai's balance sheet is relatively uneventful. with a conservative debt balance and consistent distributions to shareholders. ROE has remained flat, as has FCF, which leaves more to be desired but on an absolute basis, is strong.

Management's choice of distributions is buybacks. with a 21% growth rate since FY13. This level appears broadly sustainable, although growth will need to slow.

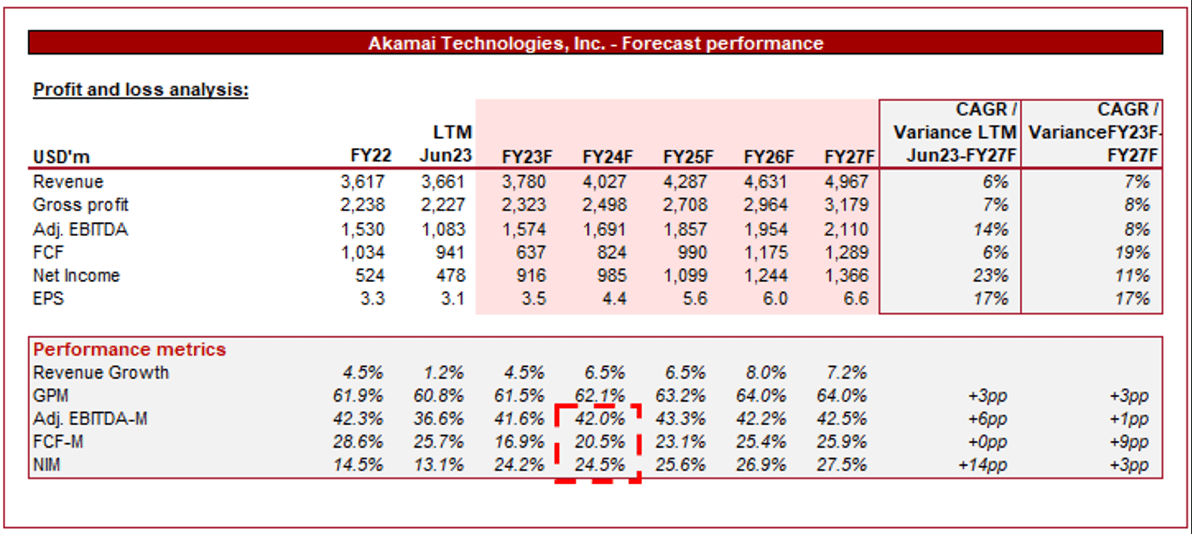

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a continuation of its current growth trajectory, with a CAGR of 7% into FY27F. Further, margins are expected to broadly remain flat. This appears reasonable (medium-term) in our view, as Delivery will weigh on the outperformance by Compute and Cybersecurity. We would expect the growth rate to start improving in FY26F onward.

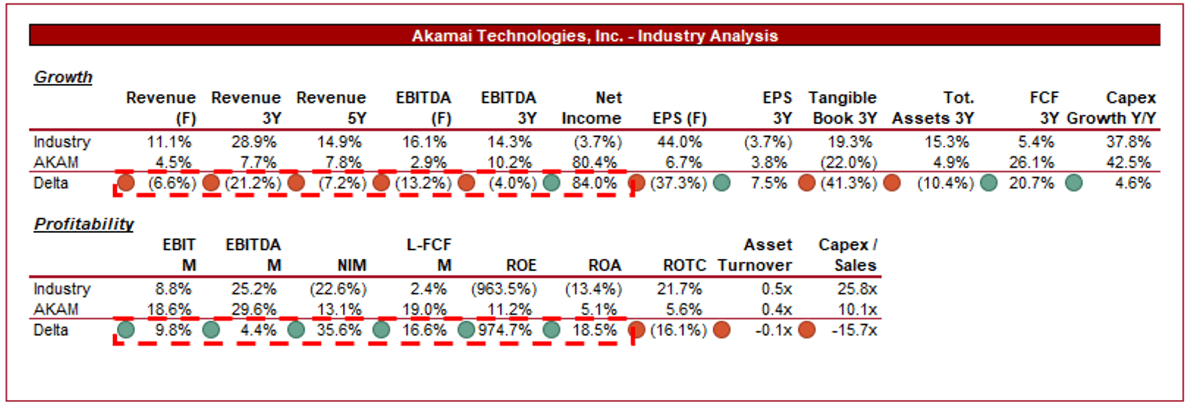

Industry analysis

Internet Services and Infrastructure Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of Akamai's growth and profitability to the average of its industry, as defined by Seeking Alpha (12 companies).

Akamai is performing modestly relative to its peers. The company's growth has been underwhelming, primarily due to the increased pressure on its core CDS business. We suspect the company will continue to underperform in this regard as its growing ventures still need further scale before "moving the needle" sufficiently.

Akamai's margins are impressive, with a large FCF premium and healthy EBITDA delta. This is a combination of the company's scale and lifecycle location relative to peers, but also its strong competitive position despite pressures.

Given the broader growth trajectory of IT services, we prefer growth to margins, as scale will bring margin improvement subsequently. For this reason, we believe Akamai should trade at a discount to its peer group.

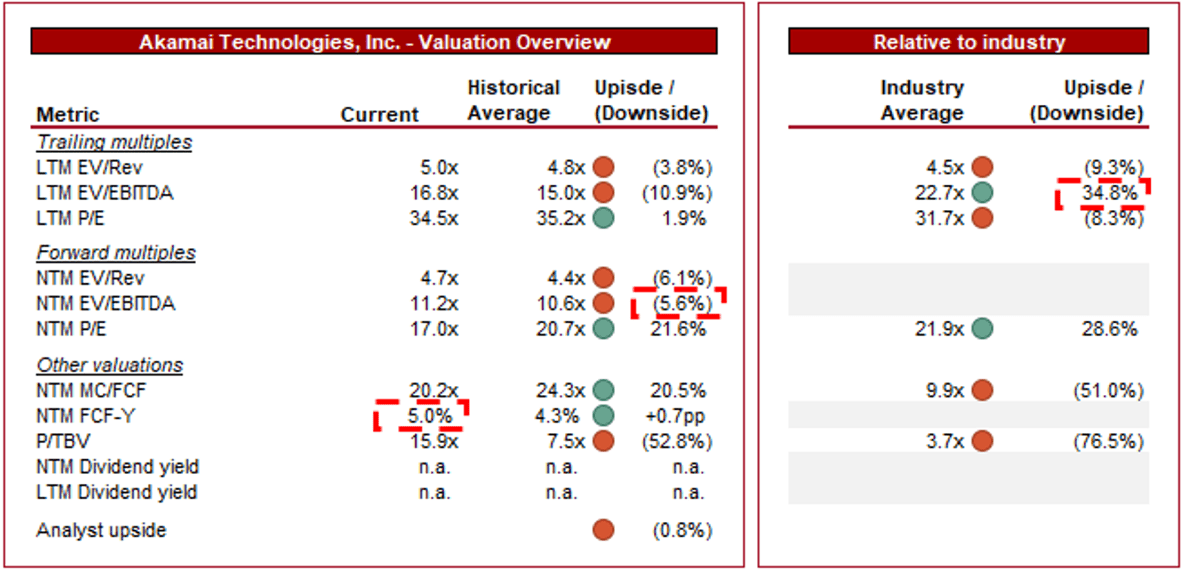

Valuation

{kind=link}

Akamai is currently trading at 17x LTM EBITDA and 11x NTM EBITDA. This is a premium to its historical average.

A small premium relative to its historical average appears reasonable in our view, which is broadly how the company is trading. We believe this because of the scope for an improvement in financial performance driven by its new focus. Much of this upside is shrouded in execution risk, however, which is why we are not more bullish from a valuation perspective.

Further, the company is trading at a discount to its peer group on an EBITDA basis (35%) and a NTM P/E (29%). Our view is that this sufficiently reflects the weakness in growth.

Akamai's valuation has marginally trended down during the last decade, while its FCF yield has improved. This suggests accumulating value, although we are hesitant to suggest the trigger should be pulled yet.

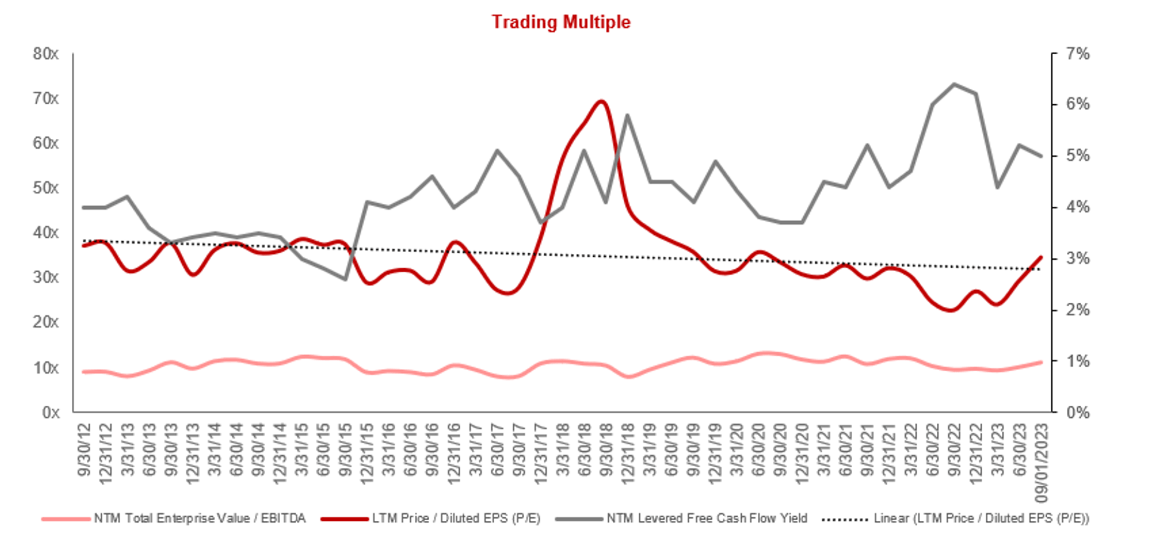

Valuation evolution (Capital IQ)

{kind=link}

Final thoughts

Akamai is a well-positioned business in our view. Its core business is strong despite the declining revenue, allowing the company sufficient time and resources to invest in expanding its Cybersecurity and Compute segments. We believe this will be successful, with healthy growth continuing.

This said, the company's valuation does not suggest an upside at its current price, given the execution risk associated with maintaining Cybersecurity's/Compute's strong growth trajectory.

For further details see:

Akamai Technologies: Business Model Transition Could Be Transformative