AKAM - Akamai Technologies: Stable And Predictable Fundamentals Fuel Consistent Growth

Summary

- Recurring revenue and subscription-based business model provide stability and predictability.

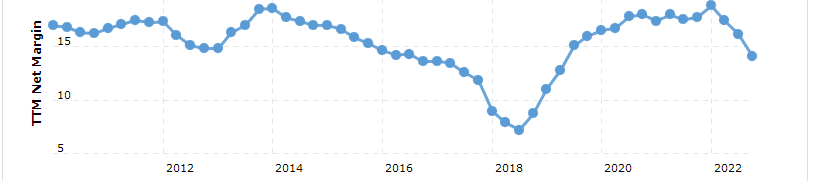

- The net profit margin has remained positive for nearly two decades with an average ROE of 15% per year.

- Future capital gains likely to stem from intrinsic growth rather than expansion of earnings multiple due to the company already being valued at a fair price.

- It seems that the company is trading at a fair valuation, as it is near a standard valuation multiple of 15, but slightly below its average earnings per share multiple of 20.

Introduction

Akamai Technologies ( AKAM ) shows impressive characteristics, including steady growth, a manageable level of net debt, and a well-considered approach to capital allocation. Strong financial fundamentals, such as those found in Akamai Technologies, are not frequently seen in undervalued companies. These financials typically prevent a stock from being undervalued, which seems to be the case with Akamai Technologies.

With their just released strong quarterly earnings report , it may be some time before the company becomes undervalued again. Nonetheless, I believe that AKAM is fairly valued at present and it may be wise to keep a close watch on it.

Akamai Technologies is a tech company that excels in offering cloud-based solutions for delivering, enhancing, and protecting online content and business applications. With a comprehensive network of servers worldwide, they assist their customers in enhancing the performance of their web and mobile platforms.

Modern technologies and cutting-edge cloud solutions guarantee that businesses can give their clients a quick, trustworthy, and secure online experience regardless of the device or location they're using. Akamai Technologies has a long history of success and has worked with several Fortune 500 firms as well as some of the largest organizations in the world.

Q4 2022 Earnings

In its most recent earnings report , Akamai Technologies reported security revenue of $400 million, up 10% from the prior year and up 14% when accounting for foreign exchange. In contrast, the company's compute sales soared, increasing by 61% year over year and 65% when adjusted for foreign exchange, to reach $109 million.

In terms of geography, the United States accounted for $483 million in revenue, a little 1% rise over the prior year. Additionally, they generated $445 million in international revenue, an increase of 13% after accounting for currency rates and 6% over the previous year.

The reported revenue beat analysts’ expectations by $22.98 million.

The company also achieved better-than-expected profitability, with earnings per share of $1.47 surpassing the predictions made by analysts by $0.11. However, despite exceeding expectations, the net income experienced a decrease of 8% compared to the previous year and saw a drop of 2% in constant currency due to the normalization of the return on equity.

Fundamentals

With its recurring revenue and subscription-based business model, the fundamentals of Akamai Technologies appear stable and predictable. The company's top-line growth has been consistent and steady, showing an average yearly increase in the mid-single digits.

The company's net profit margin has remained positive for nearly two decades and is expected to continue its positive trend. This demonstrates the company's consistent profitability. The return on equity has been gradually improving over the past decade, after experiencing a dip in 2018. With an average ROE of around 15% per year, and a significant portion of profits being reinvested back into the business, it is not surprising that the earnings per share have grown by double digits annually.

{kind=link}

However, the use of profits for share buybacks at a multiple of around 20 does result in reduced intrinsic growth and slightly decreases the average annual growth rate of earnings per share by a few percentage points.

Given that the company can reinvest capital at a rate that is higher than what dividends and share buybacks would provide at its average earnings multiple, I would consider its capital allocation approach to be prudent.

Valuation

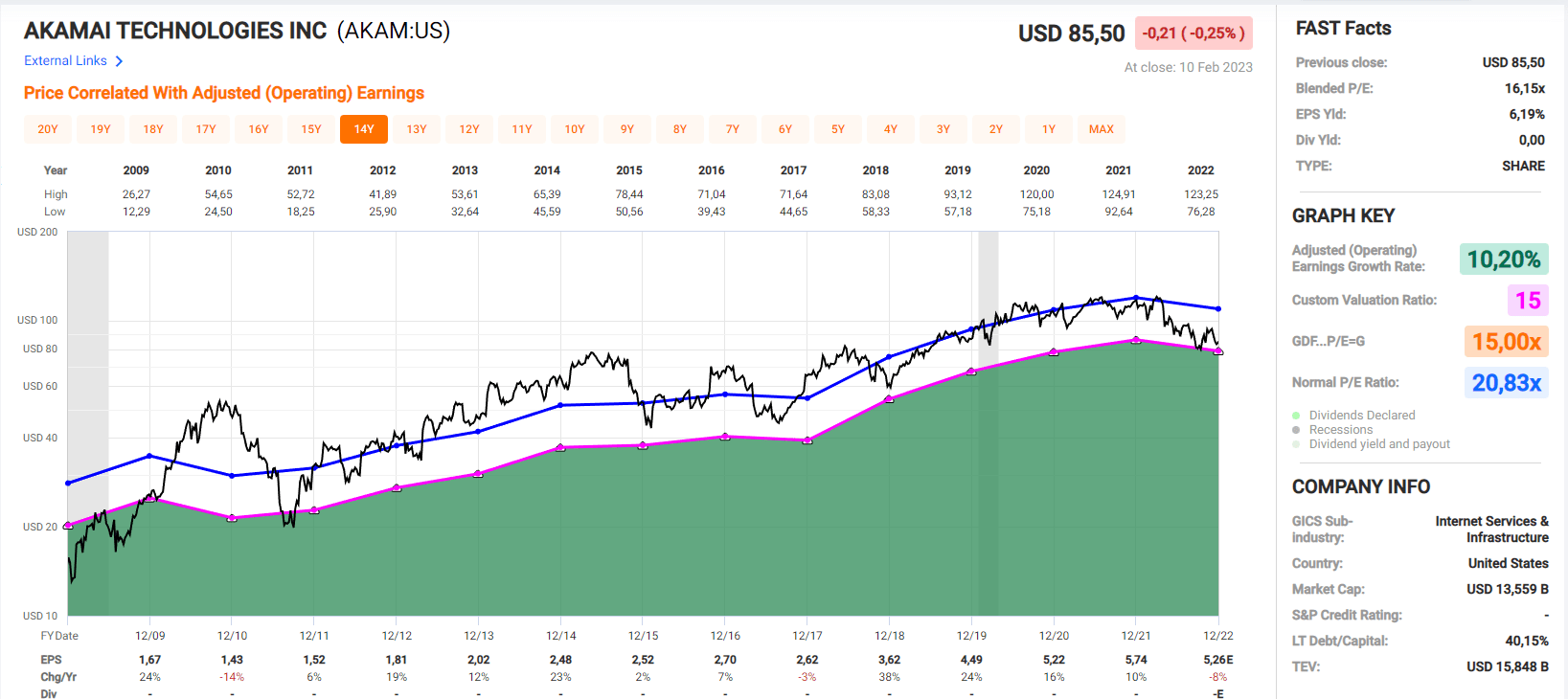

The market has generally placed a fair valuation on the company's stock, with times closer to a premium valuation. I credit the company's healthy balance sheet, which consist of little net debt relative to a fair market capitalization and the constant growth in earnings per share for this.

The company's latest earnings report shows that they have net debt of only $2.28 billion, which does not seem significant when compared to the company's market capitalization of $13.5 billion at a standard 15 earnings multiple. I do not foresee this level of debt causing a significant contraction in the earnings multiple.

Since 2008, the company has demonstrated an impressive annual growth rate of 10.2% in earnings per share, and this trend shows no signs of slowing, as confirmed by the latest earnings beat. Currently, the company is near a standard valuation multiple of 15, although slightly below its average multiple. This leads me to believe that the company is currently trading at a fair valuation. This implies that future capital gains are likely to stem from the company's intrinsic growth, rather than an expansion of the earnings multiple.

As previously mentioned in the "Fundamentals" section, it is reasonable to expect a continuation of low double digits intrinsic growth going forward.

{kind=link}

Stock Chart

Quick disclaimer: A technical analysis in itself is not a good enough reason to buy a stock, but combined with the company's fundamentals, it can greatly narrow your price target range when you buy.

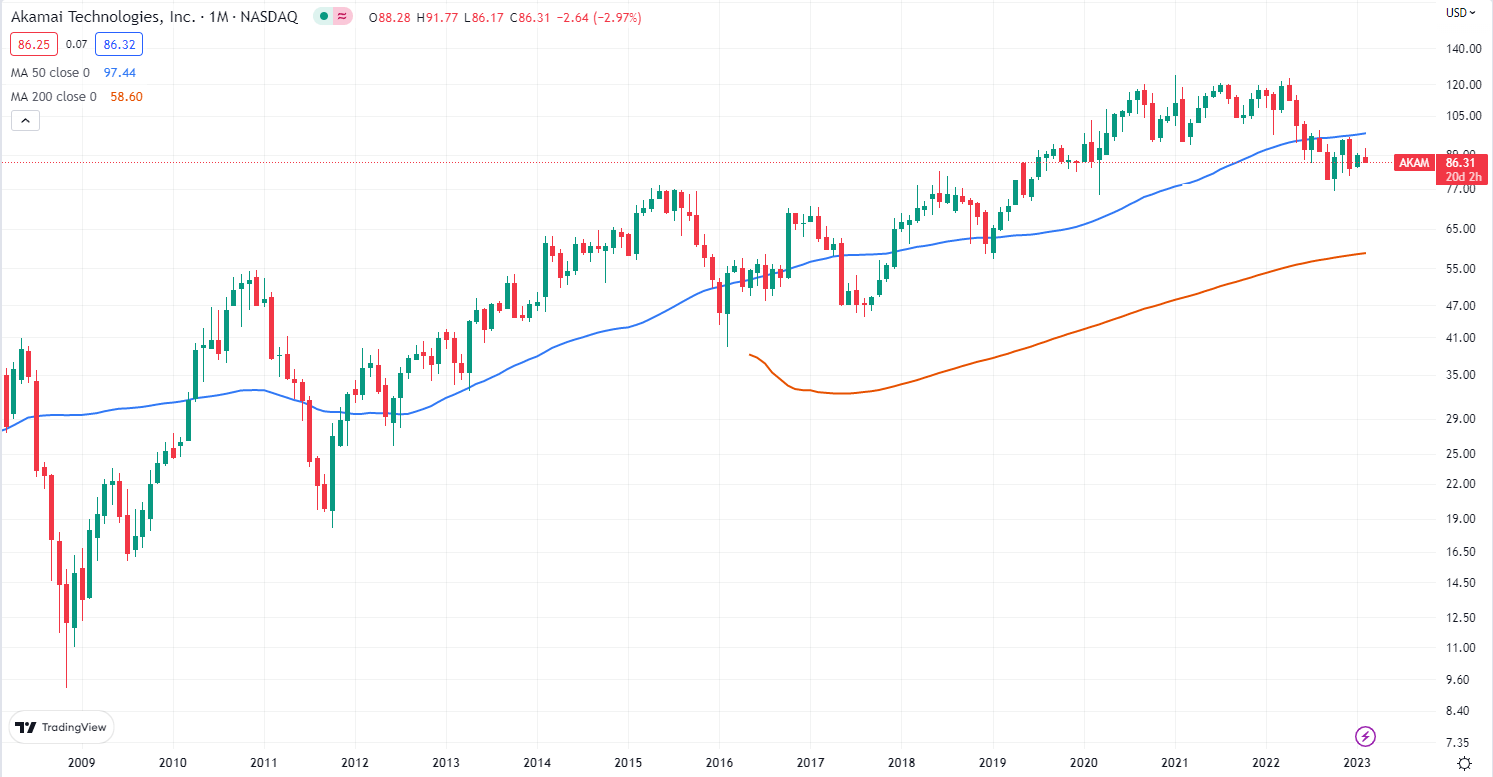

The current position of the stock being below the 50- moving average, which often is a good guideline to intrinsic valuation, was the first thing that caught my interest. Upon closer examination of the company's underlying fundamentals, I found the situation even more intriguing.

The stock has never dipped to its 200-day moving average, and there is no reason to suspect that this trend will change in the near future, unless there is a sudden and significant decline in the business's fundamentals, which seems highly unlikely.

Even considering the fairly large range between the two moving averages, acquiring shares in between could be wise.

{kind=link}

Final Thoughts

The company has seen consistent and steady growth, with positive net profit margins for nearly two decades and an improving return on equity. Earnings per share have grown by double digits annually, driven primarily by reinvestment of profits back into the business.

The latest earnings beat continued the trend of steady growth, confirming my belief that annual double digits are possible. Management further hinted that its net profit margin would decline slightly in the coming quarters due to higher-than-usual capex, currency fluctuations and third-party cloud costs. These factors may pressure the valuation of the company in the short term, but management made it clear that it is only expected to be a temporary decline.

Going forward, we anticipate that our margins will likely remain slightly under 30% in the near term, and our goal is to grow margins back over 30% during the medium to long term.

The company's debt level of $2.28 billion continues to be manageable compared to its market capitalization, and the company is currently trading at a fair valuation with expected low double digit intrinsic growth in the future.

The stock's position below the 50-day moving average, combined with its strong fundamentals, make it an intriguing investment opportunity, as long as shares are acquired in between the two moving averages.

In my opinion, the stock is currently fairly valued. Capital gains in the future are expected to stem from internal growth rather than an increase in the earnings multiple, which is a factor worth considering before making a potential investment.

For further details see:

Akamai Technologies: Stable And Predictable Fundamentals Fuel Consistent Growth