AKCCF - Aker ASA: NAV Discount Means You Get Industrial AI Leader Cognite Almost For Free

2023-07-20 17:01:43 ET

Summary

- Aker ASA is not an AI company at first glance, but it has Norway's first unicorn, Cognite, in its portfolio that can be bought essentially for free.

- Cognite is around 10% of the company's NAV, but if you short the publicly-listed components of Aker ASA, it can be more than 50% of the exposure.

- Its sales are growing rapidly with healthy and strategic end-markets, it has advantaged ways to make use of LLMs, and its losses are narrowing.

- Most importantly, Aker ASA trades at a discount from NAV that almost exceeds the value of the non-public holdings, including Cognite, so you get them almost for free.

- Aker ASA is the value investor's way to get AI exposure and may be the only value and bargain play on AI in developed public markets.

If you take a look at Aker ASA (AKAAF), you may think you're looking at an oil and related industrials company. You wouldn't be wrong, but at about 10% of Aker's NAV, otherwise driven by listed industrial/oil companies like Aker BP (AKRBF), is Cognite , which is Norway's first ever unicorn as an industrial DataOps and AI player. Its sales are growing rapidly and it is narrowing its losses, becoming a leading and ML-powered data player for oil rigs with scope to also make use of fine tuning LLMs with its industrial schematics to eliminate hallucination . Most importantly, Aker ASA, which is a holding company, trades far below its NAV, and therefore Cognite (and the other non-public assets) come for free even with pretty conservative valuation assumptions, and we can say that with confidence since the rest of the portfolio is publicly listed with plentiful liquidity.

While we have a lot of confidence in the oil assets, which have been booming thanks to a mix of Norwegian strategic positioning vis-a-vis Europe's oil needs and structurally higher oil prices, investors who aren't willing to take on that exposure can isolate the non-public exposures including Cognite by going short Aker BP (and most of the other listed holdings), which can be shorted at very low annual borrowing costs of around 0.5% (according to our broker). As time passes and Cognite continues to gain steam and traction as it ramps up in preparation one day for a public, separate listing like the rest of the Aker ASA portfolio, you can cheaply hedge any potentially unwanted oil risk and wait for what will likely be a high visibility holding that you would be paying nothing for today.

We think the oil exposures are also great, and would like the dividend from this NAV-discounted holding as we wait for the Cognite holding to be a more needle-moving part of the Aker ASA NAV story once IPO and M&A markets start to recover. But we understand that investors may want to simplify the bet or avoid oil exposure.

Therefore, Aker ASA can be made into a very compelling, high margin of safety bet that delivers at book value a couple of non-public exposures dominated by Cognite as well as some non-shortable illiquid public positions plus pure value from the NAV discount through a cheap-to-maintain long-short position. With the NAV discount almost exceeding the value of the non-public holdings ($750 million vs $817 million), the implication is that the market implied value for the non-public holdings is essentially zero, which is a phenomenal opportunity around Cognite when AI is all the rage and would otherwise come at a pricey multiple. Otherwise as a straight buy, Aker ASA is a great NAV discount story with quality assets and an emerging AI component with catalysts from a capital market recovery and the continuing progress of AI. High conviction buy.

NAV Breakdown, Commentary on Everything Other than Cognite

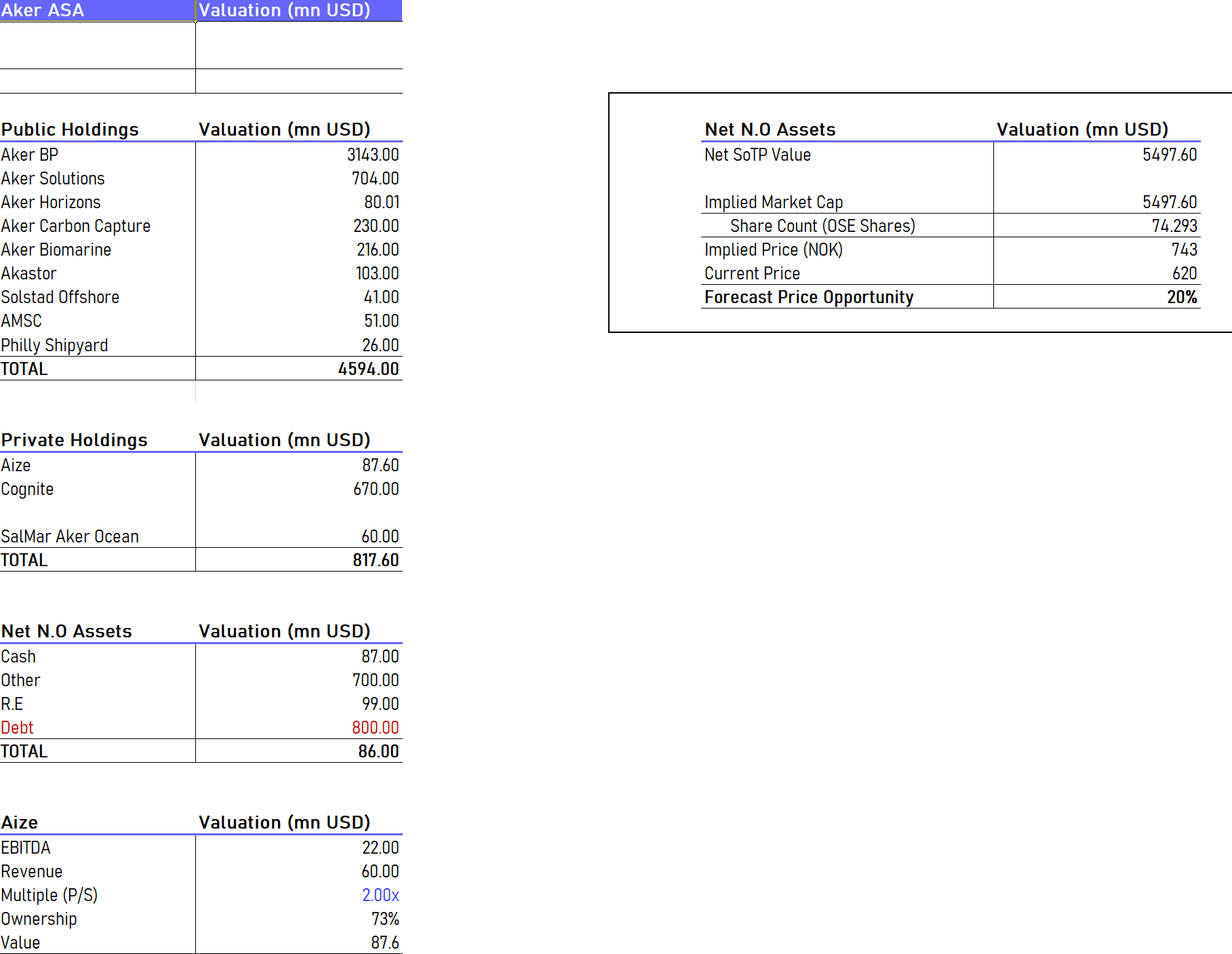

Let's begin with the NAV breakdown and an explanation of some of the other assets in Aker ASA for those who don't intend to go long-short to isolate Cognite as much as possible. Less than 10% of the public holdings are not shortable, which means it is possible to get a pretty accurate long-short balance to isolate the non-public stuff so that ultimately Cognite represents almost 60% of the exposure.

{kind=link}

The public holdings are all listed with their current market values, and when in doubt we use book values for the non-public holdings which are dominated by Cognite's book value so that we can demonstrate clearly the NAV discount.

Public Holdings

Aker BP

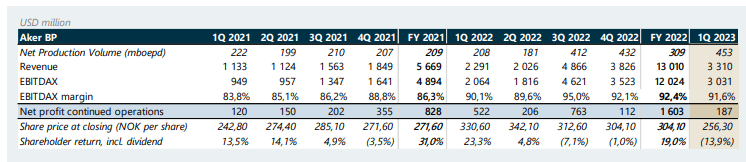

Aker BP owns interests in oil fields and produces oil from the low-breakeven point rigs on the Norwegian Continental Shelf. Besides the Saudi and other Gulf producers, the NCS assets are some of the lowest cost in the world, a major competitive advantage. Aker BP just completed some major capacity increases in the Phase II part of the plan on a major oil field called Johan Svedrup in the NCS, and production volumes are rising across its fields with utilisations at very high rates. They are also continuing to make new discoveries in fields where their interests are relatively larger. Production volumes are up massively at still great oil prices. Naturally, Norway is not following in any supply cuts from the Saudis as they are not aligned with OPEC.

Aker BP Performance (Q2 2023 Aker ASA Pres)

{kind=link}

We believe the struggle of the West in dealing with the effects of reduced oil supply and the initial fallout from the Ukraine war accentuated difficulties in shifting away from fossil fuels. Even the relatively green politics of the current labour government is Norway haven't gotten in the way of oil producers, and for those developing oil assets there are now tax breaks to incentivise NCS development. We believe the situation has reduced the urgency of the Saudis and other OPEC members to upfront their profits from their oil assets, as peak oil is further away than markets thought, therefore spurring the new supply cutting regime. We think this is a new structural element.

EBITDA is up massively and we think that together with the capacity increases, it remains a resilient holding. The only negative is that there is interest creep, as they refinanced some fixed rate debt and it meant that current rates in the US, since their debt is USD denominated, caught up with the earnings and stalled net profit. Still, the 8-9x PE more than reflects the strain on profit growth from interest creep while reserves grow and production scales as a major European provider now that Russia has been distanced. Cheap to short at 0.6% p.a. in maintenance costs.

Aker Carbon Capture (AKCCF)

We have recently updated our view on Aker Carbon Capture . They are continuing to win high profile contracts to do EPC for carbon capture facilities, based on their modular designs, and are nearing running their facilities with their carbon capture as-a-service business model as a receiver of royalties on the deployed technology as well as an aftermarket business while clients farm carbon tax benefits. The growth is substantial in revenue, and the EPC revenues represent a low-point in terms of margin contribution as far as the lifetime value of a CC customer goes. They'll actually be done with the EPC part in some places by the end of 2023, and 2024 will be a big year at the conclusion of Brevik. Their model should inflect then. It's a great company, with a fantastic ESG angle that is enshrined in the European carbon reduction plans by 2050, but it comes at a full multiple. While we are not worried about value impairment, their market cap should represent a fair value for the business as a component of the Aker ASA NAV. It is liquid and cheap to short at about 0.6% comprehensively p.a. on a premium broker.

Also note that Aker ASA owns Aker Carbon Capture through Aker Horizons. Aker ASA owns 67% of Aker Horizons which in turn owns 43% of Aker Carbon Capture. Since Aker Carbon Capture is cheaper to short than Aker Horizons, we've valued the Aker Horizons holding as its residual value after taking out the ownership of Aker Carbon Capture as it would be valued on Aker ASA's balance indirectly through Aker Horizons. This is good because then Aker Horizons no longer represents a relevant holding in the NAV calculation.

Aker Solutions (AKRTF)

Aker Solutions' backlog is skewing towards more traditional oil projects where they provide subsea engineering services and then also some life cycle management service contracts to oil players (they also do EPC for offshore renewable projects but that's reduced in the mix). They benefit meaningfully from the strategic nature of oil in the current geopolitical setup as well as government incentives for oil companies to develop on the NCS. The backlog is multiples of what it was a year ago, and its EBITDA has also doubled this quarter thanks to 36% YoY revenue growth and meaningful project delivery. As backlog gets to later milestones, mix effects will be positive as projects age. They are trading at around 10x PE, which considering the massive backlog that will take a couple of years to liquidate, sounds about fair considering oil market dynamics and strategic incentives and considerations that go beyond commodity market considerations. It's also 0.6% to short p.a.

Aker Horizons

This unit is more expensive to short, but its value is mostly determined by the publicly listed Aker Carbon Capture, and its small representation in the NAV calculation means that for investors planning a value weighted short of Aker ASA's portfolio, the 5% p.a. maintenance costs for shorting Aker Horizons will not matter much for the cost of the overall long-short play. Its residual value is also rather marginal, to the point of being ignorable in balancing the long-short.

Aker BioMarine

Aker BioMarine is the only somewhat larger component of Aker ASA that is not shortable due to limited liquidity. It represents less than 5% of the Aker ASA NAV which is not much. Still, since going long Aker ASA forces you to go long (albeit to a smaller extent) AKBM, we'll discuss it here in some detail.

Fortunes of Aker BioMarine as a producer of krill products with its specialised krill slurping vessels in Antarctica depend on the market for krill supplements, including for Omega-3, but also as a source of gym protein and in a more major example as feed for the aquaculture industry (both shrimp and salmon). Sales are growing meaningfully around 25%, and new projects like a factory to produce protein from krill, have just been completed. Price has been a major boost for the ingredients business in aquaculture in recent quarters as higher grain and substitute feed prices have gone up due to the Ukraine war, helping out krill prices. Also krill-based feed is apparently better for the salmon and actually produces better harvests. Aker BioMarine believes there is still more value to capture in that regard as krill becomes a more recognised feed.

It is important to realise that Aker BioMarine are creating the market for krill products. They are responsible for more than 70% of the krill harvested and sold globally, so without Aker BioMarine the product would barely exist.

There used to be a major market in South Korea which collapsed some years ago due to fraud by bad actors (not Aker BioMarine). Gross profits were flat for AKBM despite revenue increases due to a factory shutdown in the US as preparations are made for a re-entry into the Korean market later this year. Once the capacity is being utilised again things should go better as scale economics are reached again.

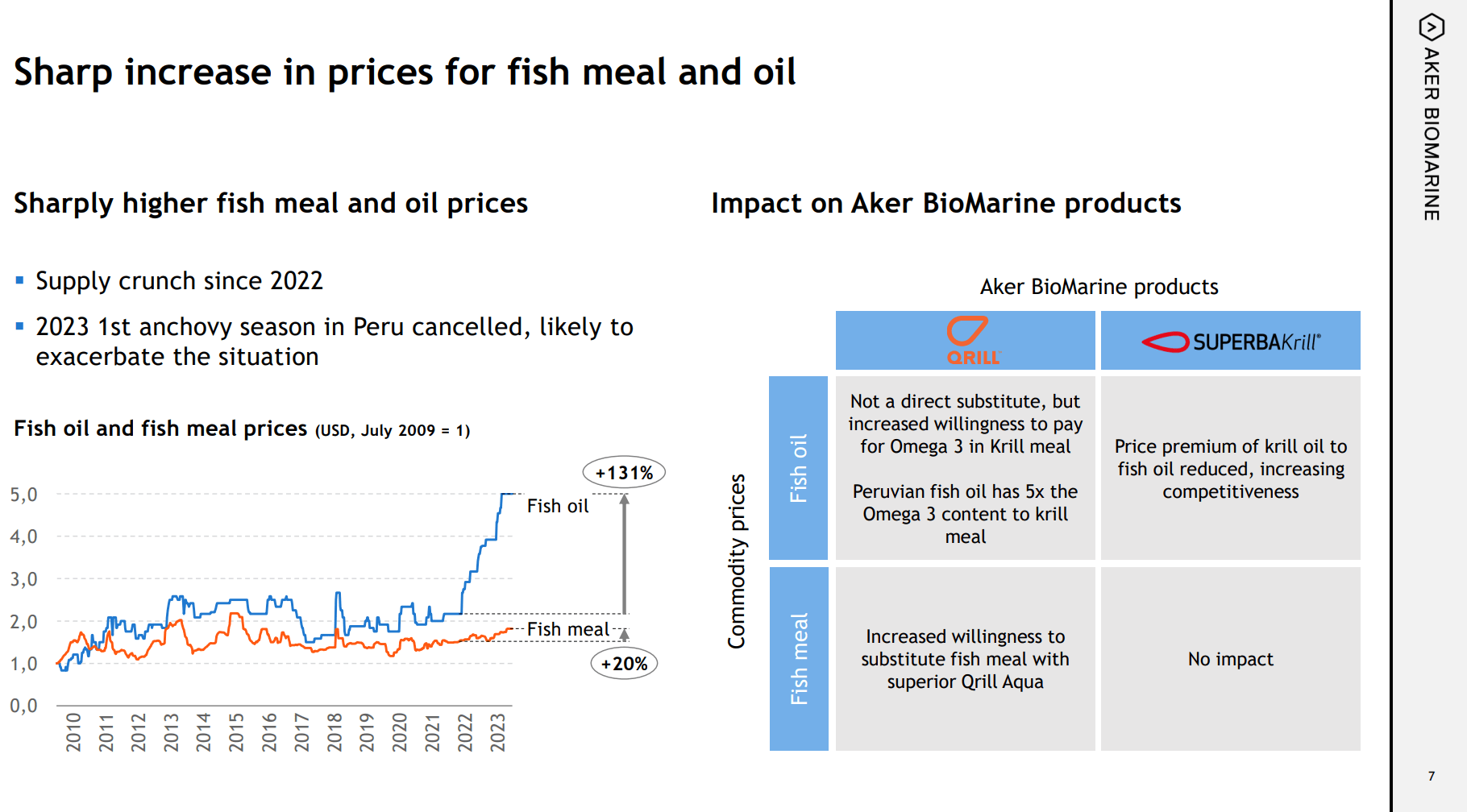

Another thing that is happening is that fish oil prices are skyrocketing, and fish meal and general feed prices are also remaining strong. The price of fish oil affects AKBM's consumer markets since krill oil is a competing supplement. With fish oil becoming more expensive, substitution effects may benefit krill oil prices and volumes.

The fish meal prices continuing to rise also helps the relatively higher margin krill meal ingredients segment in terms of substitution effects. This price strength is being supported by structural factors related to supply side inflation, so it's a beneficial and durable situation for AKBM. It also helps that Russia just pulled out of the Ukrainian grain deal too. We think there's a lot of latent earnings growth, massive barriers to entry and other factors that makes AKBM attractive to own as part of Aker ASA, also because liquidity is better than directly owning AKBM. This fact also contributes to the argument that for a holding that you can't hedge away from, it is encouraging that it should be potentially more undervalued thanks to liquidity discounts.

Substitution Effects (Q2 2023 Aker BioMarine Pres)

{kind=link}

Akastor (AKKVF)

Akastor is a holding company of several drilling and offshore installation and aftermarket services companies that cannot be shorted. It is winning projects and maintaining a large backlog balance, and increased aftermarket intensity as well as maturing projects has meant great margin uplift. EBITDA margins are almost 20% , and revenues are growing nicely thanks again to upstream CAPEX. It is less than half the exposure of AKBM.

Private Holdings

The main private holdings to discuss besides Cognite is Aize. They are a modelling and visualisation software used for industrial assets and planning. These kinds of companies tend to be very highly valued. Aize has doubled revenues YoY and is highly profitable. Since it is growing at a venture clip we use a P/S multiple. While more valid comps trade at around 9x P/S , we take 2x just to avoid making Aize too important a part of the story. But it is actually a pretty valuable business especially considering the EBITDA margins in excess of 30%. Using the 9x would increase the NAV discount and price appreciation opportunity by 6% from 20% to 26% for Aker ASA overall. Aize would be an important part of the exposure for investors who hedged everything else possible. The ratio between AKBM, Akastor, other unshortable equities, Aize and Cognite for investors considering the long-short position would be 2:1:1:1:6 with Aize valued at 2x P/S and with Cognite at book value. Oil exposures that are unavoidable would only be around 15%. The other equities are in shipping mainly.

Aize Profit and Revenue Growth (Q2 2023 Aker ASA Pres)

{kind=link}

Discussing Cognite

Now comes the time to discuss the AI angle in Aker ASA. As just mentioned, it represents the majority of exposure for investors positioning long-short at around 54% . The remaining holdings are otherwise Aize and AKBM that move the needle, where Aize is probably also undervalued in our NAV calculation, and AKBM is not a bad proposition either. For those not hedging and just buying Aker ASA, Cognite still represents more than 12% of the overall NAV at book value.

The book value of Cognite was determined a couple of years ago by a fundraising round that provided a market value at that time which was a moment when VC markets were hot. If you assume that it doesn't accomplish sequential revenue growth, the implied P/S of Cognite using its book value and ownership is a little over 10x P/S (the funding round with Aramco in February 2022 actually implied a 800 million NOK equity value for Aker ASA's share rather than the 660 million reported as book value). Current stocks with AI tailwinds average between 7-10x P/S which means that Cognite's 2021-2022 valuation ends up looking fair in today's terms considering the demand for AI stocks in the market. We think the book value is fair.

Cognite Profit and Revenue Growth (Q2 2023 Aker ASA Pres)

{kind=link}

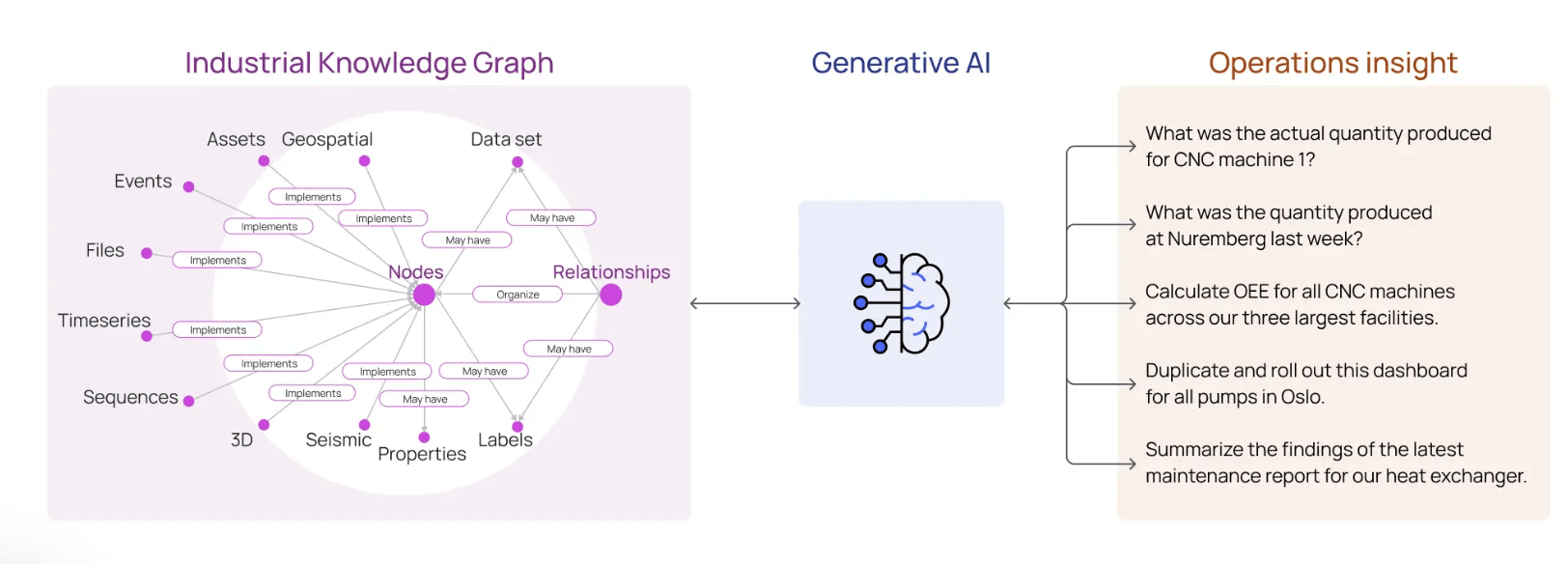

The value of Cognite is that it creates a dashboard for data that might exist across divisions that may have data siloed away. While something like Google can retrieve data from webpages when you make a search to improve the search results, like naming the owners of a business, its working hours and prices etc., Cognite uses industrial and engineering data stored in a company's database to build schema that users can use to check and search for information about a facility and its machines. In this manner it is innovative, since a platform that compiles unstructured data, including photos taken during maintenance, doesn't exist for industry. What makes Cognite technologically interesting is that it retrieves this data using ML processes. The examples often given are where it starts with P&ID (piping and instrumentation diagram), and then with all the unstructured data across the company's cloud, it uses information on the P&ID to automatically retrieve data about all the machines and instruments that are noted on the diagram. Sensory data, maintenance pictures from the field, time series data, CAD models, manuals, logs and anything else that can be linked then becomes compiled in one place where it can be interacted with through the P&ID, which may be just a picture or in .PDF form. This all depends on computer vision and to a lesser extent NLP.

Cognite provides systems to be able to deal with various references that may be made to different assets, and it connects references and can create the necessary graphs by knowing about those connections in a variety of contexts and businesses. It will be able to build flow lines, past specific tanks, valves, seals and pipes, with all the sensory information collectable along the way. Cognite works with major oil companies like Equinor ( EQNR ) and Aramco ( ARMCO ) as examples. Aramco is also an investor, in addition to Accel and TCV. Aker ASA owns 50% of Cognite currently.

The other thing Cognite is capable of is building a digital twin of your facility or machine by using manuals and all other diagrammatic and sensory data that may pertain to that facility or machine. Having an ML process create a 3D model for you can be very useful for planning and analysis, and the model contains linked references and is interactive. These can have simulated physics and can be a view of a facility or asset in real time. It is combined with collaboration features in order to schedule and push for maintenance with personnel in the field.

It can also ingest large datasets like 3D models and to reduce it in a usable way for use on the field through things like browsers and less powerful handheld technology.

It has APIs, extensive documentation for those APIs, and SDKs for developers to build their own applications on top of Cognite's platform.

Cognite is looking at leveraging LLMs. Firstly, fine-tuning generally has many effective methodologies and it would be a useful approach in leveraging pre-trained language models like those underlying ChatGPT. Secondly, because of Cognite's existing capabilities in AI-driven data collation and collection, LLMs can be trained on conceptual schema to avoid hallucinations and to make the references made by a prompted LLM more trustworthy. Rather than probabilistic responses, the reasoning engine behind LLMs, which understand text and semantics, can be used to provide determined responses based on a definite schema that can be fed to the LLM. Cognite AI, which is the name of this new functionality offered by Cognite, has just been launched, and interest is apparently very high. We have yet to see the benefits on sales from take-up of this product at Cognite's high profile industrial customers. If their Data Fusion platform can provide the conceptual graphs necessary to avoid hallucination by an LLM if you prompt it for information from specific contextual data in industrial manuals etc., then the product could become very successful and a game changer.

LLMs in Cognite (Cognite Website)

{kind=link}

Since LLMs are excellent coding co-pilots and Cognite's documentation is extensive, it could be useful for developers in the organisation and for data analysts using Cognite's platform to perform the necessary commands to produce the outputs and generate the needed insights from the compiled data. More ambitiously, the LLMs could be used to answer prompts and produce reports itself and help with maintenance and repair activities.

Recurring SaaS revenues are growing in the mix as of the FY 2022 report, measured by ARR internally, and those will annualise into good revenue growth for Cognite which has already been more than 30% YoY for the Q2. Loss margins are beginning to narrow for the company at -15% in the Q2, although it is still in ramp-up mode and is burning cash. Still, the margins are a lot better than they were last year. They raised $150 million in 2021 when they became Norway's first unicorn, then a little more from Aramco later on, and they likely have about 1.5 years before they need to raise again. While dilution is never fantastic, the products are creating growth and there are tailwinds from industries benefiting from strategic and market support, including E&P who are seeing strategic support in developing assets, but also CleanTech and power companies. Raised cash will be reinvested well. With more assets being built in the energy and oil space, Cognite's already existing markets are growing quickly, in addition to greater penetration of digital tools in industrial companies.

Risks

The first thing to mention is that while Aker ASA is a public company, its disclosure on Cognite is somewhat limited. We don't get as much data, such as balance sheets, that can tell us exactly what is going on with the company. To the extent that net income and EBITDA can proxy for cash generation, and given public disclosure on the funding rounds, we can determine the runway of around 1.5 years, but we don't get a lot of insight into details of business strategy. The mitigating factor is that venture-profile companies usually share a strategy of just burning cash constructively and gaining as much traction as possible. Since the markets are healthy, we aren't looking for anything special in their strategy. We have every reason to believe Cognite is doing that on the basis of its revenue growth and the health of its end-markets.

Related to Cognite, the other risk is around capital market conditions. VCs and others are also invested in Cognite, and given the composition of Aker ASA's holdings, one would assume that they all want to exit with an IPO. IPO markets have not been good due to weak public markets. The exception, however, has been AI stocks, and Cognite does fit the bill there. Still, realising this value concretely could take some time and should be seen as a VC style exposure, although not an early stage one like in a typical SPAC. Also, it should be mentioned that rating upgrades are happening across advisory companies as markets are seeing greenshoots, which means that institutions believe that there might be a turning point in IPO and similar activity.

Bottom Line

Ultimately, you can get exposure to Cognite through an undervalued holding vehicle supported in its NAV by mostly liquid public holdings. Cognite's book value is reasonable, and the NAV discount almost eclipses the non-public holdings, meaning they are valued basically at zero within Aker ASA. If you take a long-short position against the independently listed public assets, you can concentrate the bet on Cognite as well as some other potentially undervalued assets like Aize and AKBM.

There is an LLM angle to Cognite, as well as the already relevant AI-powered dashboard and platform that Cognite provides. Aize is in the stable and high multiple model visualisation space, and probably also could deserve a higher multiple. But most of all, going long Aker ASA implies a zero value for them because of the NAV discount.

In a space where a bargain is essentially impossible to find, we have found one where the discount is high conviction, and the implied value of a small portfolio of assets, dominated by industrial DataOps leader Cognite, is basically zero due to a SoTP discount bolstered by market values of solid and liquid public assets. A clear buy.

Editor's Note: This article was submitted as part of Seeking Alpha's Best AI Ideas investment competition , which runs through August 15. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Aker ASA: NAV Discount Means You Get Industrial AI Leader Cognite Almost For Free