AKCCF - Aker Carbon Capture Counts Easily On EU Support For Carbon Capture

Summary

- Aker Carbon Capture is easily the most prominent carbon capture business running with actual sales in Europe.

- They have a concrete value chain in connection with Northern Lights through a JV to provide both construction and maintenance services as well as logistics and carbon injection services.

- Carbon injection involves terminalling, transporting and then injecting the carbon back into depleted reserves offshore.

- They have several projects, and these will be running facilities by 2024. They have meaningful revenues but are way below profitability.

- This 'Carbon Capture-as-a-service' model is entirely new, and not yet reflected in the business results, but turns them into a real infrastructure play relying critically on continued carbon taxation.

Published on the Value Lab 1/22/23

Aker Carbon Capture ( OTCPK:AKCCF ) is a more mature, later-stage bet on the opportunity of carbon capture systems, with currently two projects in the works and close to the completion, making revenue on the construction services all the while. Carbon capture has the makings of an interesting set of infrastructure plays, and the economics could be theoretically strong. It depends primarily on the taxation of carbon emissions, which increases the value of carbon capture to emitting clients, with the regulatory framework for taxation of carbon emissions already established in major European states. With COP26 and a host of other initiatives aimed at reducing emissions as a major political milestone, and the need for carbon capture to improve the green economics of things like hydrogen production which features heavily in European energy plans, the secular outlook for CCS demand looks great. ACC is a loss-making company for now, but with this scale the economics should improve substantially, and the higher value services will come after the CCS plants at emitter locations are completed in 2024 to start.

Aker Carbon Capture's Model

ACC makes money in two ways - at least currently . They make money on construction, as any engineering company would, and then they make revenue on the maintenance of their constructed CC facilities that they've made for polluting clients. We expect the increasing share of maintenance revenue to contribute positively to margins. The value of the CC facilities is to draw carbon from the air to offset carbon emissions by polluters, and therefore reduce costs related to carbon emission allowances. Tightening on emission standards is a secular tailwind, and while artificial, higher costs of carbon emission will be an important long-term tailwind for ACC. Development of projects like blue hydrogen production, for which CCS solutions can reduce the carbon footprint, are also a tailwind and supported thoroughly by EU commitments around reducing emissions.

Revenue Mix (H1 2022 HY Report)

The next thing that they are expecting to make money off of is the terminalling, logistics and eventually the injection of the carbon definitively back into emptied deposits from previous oil pumping - this is Project Longship. They are doing this by working with a company called Northern Lights through a JV where full service offerings are going to be delivered on specific projects. This would cement them further as not just an engineering company but also an infrastructure company that could make money off CO2 infrastructure. This is a non-exclusive deal so they can still be engaged independently when contracted.

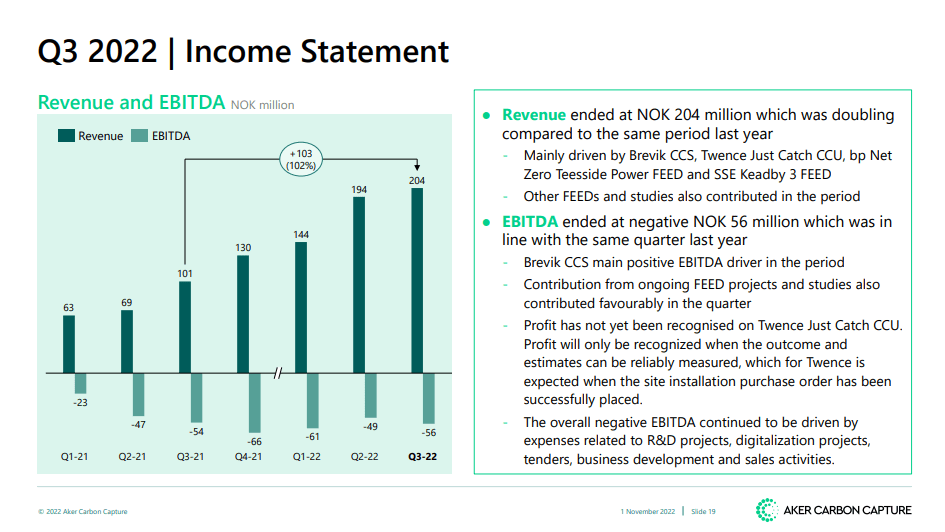

Looking at the Q3 2022 presentation, we can see the status of the model. Revenues are growing as their projects scale. The Brevik project which will be completed in Q3 2024 according to forecasts operates at a cement plant. Continued engineering there is creating revenue and economies of scale, with loss margins falling. Operating leverage may even get the company over the large fixed costs in R&D, but those costs can also be expected to decline eventually as learnings become solidified on this relatively emerging technology. Once the full services are also being delivered we expect further favourable mix effects to improve profitability.

{kind=link}

What's Next

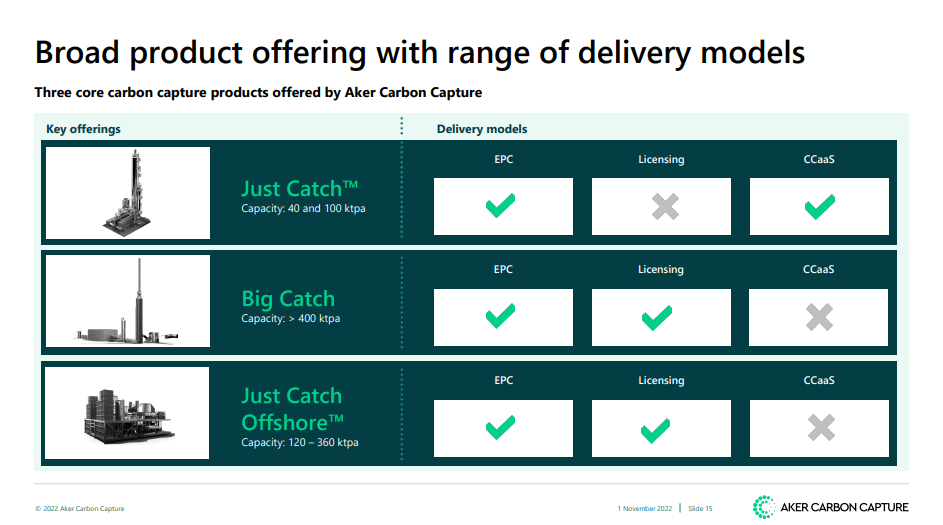

The Brevik project is one of many, and they are already partnering with major companies and emitters like Babcock ( OTCPK:BCKIF ) in the UK, Siemens ( OTCPK:SMAWF ) and BP ( BP ), and are drumming up interest from companies like Elkem ( OTC:ELKEF ) too. These are the facilities that they can build for clients, depending on their carbon emission needs, and can even be built offshore to work directly on reducing emissions from rigs.

{kind=link}

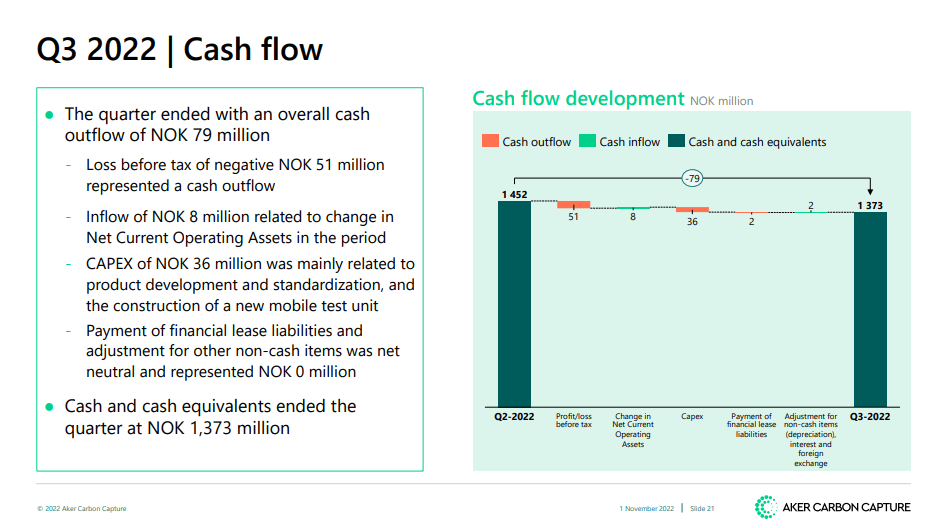

Much like subsea companies , we expect favourable mix and scale effects as the company continues to develop, and appreciate shrinking EBITDA loss margins. Cash burn is also very limited relative to how well capitalised the company is. No dilution risks here or anything like that. They have not issued shares since last year and will be unlikely to have to issue shares going forward. With the price discounted, this mitigates reflexivity effects.

{kind=link}

Another gem as far as shareholder returns goes in this company is the following from their last annual report.

The Chief Executive Officer determines the remuneration payable to key executives in accordance with board guidelines. Aker Carbon Capture has no stock option programs. The remuneration for executive management includes a fixed annual salary, standard employee pension and insurance schemes and a variable pay element.

Great to hear as it means no share based compensation expenses to sneak up on shareholders as often is the case in these emerging companies with an in Vogue , green proposition.

Finally, in terms of valuation, Aker Carbon Capture seems fairly valued. Current EV/Revenue is 8.75x. With only one projects under meaningful progress, and two more in very early stages, a tripling in revenue can be expected. There are also other contracts that have been definitively signed. As the projects there launch, we should see more than a 5x in revenue over the next 2 years. With the potential economics improving as projects go through their milestones, the EV/Revenue metric looks fair as it eventually converts into EBITDA.

Overall, while there's a strong need for government-imposed requirements to reduce emissions to support this industry (it would fail entirely without government intervention), support for reduction of carbon emissions is overwhelming among western nations. It is very unlikely to stop at this point resisting a year of very high energy costs which was the biggest danger to the green revolution in a while. Considering the possibility of great infrastructural revenues, the multiple looks fair given revenue trajectory and tight cash management and lack of major latent costs.

For further details see:

Aker Carbon Capture Counts Easily On EU Support For Carbon Capture