AKCCF - Aker Carbon Capture: Major Orders Incoming Project Completions

2023-11-04 08:05:20 ET

Summary

- Aker Carbon Capture is nearing completion on larger projects, and its orderbook is growing, indicating it will likely hit needed volume KPIs to justify valuation.

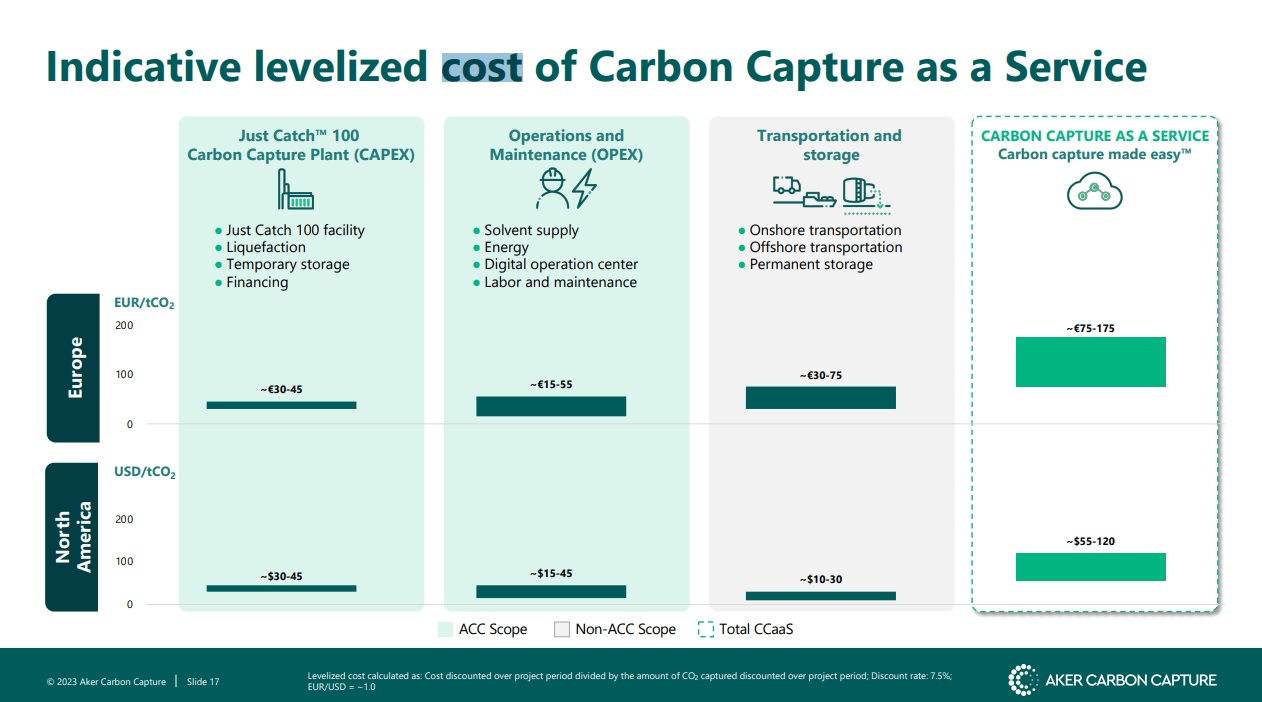

- ACC's modular carbon capture system, Just Catch, has reduced costs to around $40/tonne, making it economically viable in certain European countries with high carbon taxes.

- ACC has exploratory deals with Aramco and other companies, suggesting that the backlog could balloon, making the company's prospects more promising.

- Already negotiated backlog brings volumes to levels that justify the price, and we see the secular case as strong thanks to immense pressure behind the green agenda in Europe.

Aker Carbon Capture (AKCCF) is nearing completion in a couple of larger projects, and its orderbook keeps growing. The economics are theoretically infrastructural and interesting, and the projects ACC are pursuing could actually be profitable based on current levels of carbon taxes in target Benelux and Nordic geographies. We were less positive on the stock 25% in declines ago, but now we are more interested again and see concretely the scope for some decent economics. Speculative buy due to it still being early stage.

Quarterly Breakdown

The major projects that are in focus are the Twence project in Holland and Brevik in Norway. These are a waste to energy project and a cement factory respectively, both meaningful emitters whose profile will be offset by ACC's Just Catch modular carbon capture system.

{kind=link}

Just Catch's modular system has done a good job of bringing costs per tonne down, now at around $40/tonne, where carbon taxes are higher than that in NL and the Nordics . Admittedly, the carbon taxes in most other European countries would render the project uneconomical for emitters. Remember, the whole value of ACC's systems is to offset levies by government from pollution.

The Twence project will start producing revenues at the end of 2023, where the plant is already commissioned, while Brevik comes online in 2024.

For now, revenues have been almost exclusively in engineering and installation fees to offset upfront costs for ACC which provides the systems.

Twence and Brevik are small though compared to other projects and markets in the pipeline. Together, they deal with 500k tonnes of CO2 a year. ACC has a deal with Aramco (ARMCO) now and unsurprisingly the Saudis have ambitious plans for carbon capture in their country, already 9 million targets for 2027. They have signed pre-FEED studies going that account for 9 million in CO2 capture as of now.

Bottom Line

There is a spread between the lower carbon capture costs of the emitters that ACC is focusing on, like steel and cement production, as well as the carbon taxes in certain European geographies, mainly the Nordics and other exceptionally progressive countries. In principle, the economics should be good, and it helps that there is still scope for other nations in Europe to introduce higher carbon taxes, as the pressure is certainly there.

Moreover, the price has declined 25% since our last publication, and there hasn't been dilution. It's looking more interesting.

In theory, the economics could be really good. There are upfront costs and processes, mostly covered by the customers, but when online the service of carbon capture can be provided, it is highly recurring including maintenance and other activity. But ultimately, it is limited in value capture to what the tax is on releasing that CO2. In Benelux and Nordics though there is plenty of value to capture.

In the bag is already 500k tonnes of CO2 that will be captured in profitable regions. With Aramco and plenty of other already or bound to take interest, the carbon capture volumes are going to easily reach into the couple of millions, if not much more as most espoused plans, whether you trust them to be delivered or not, have multiple millions in targets for each country. Considering secular growth, a 2x P/S would be an alright multiple to pay, and that implies around 4.5 million in CO2 capture volumes being conservatively attainable. We don't think it's terribly far fetched considering they are already at 500k concretely, and actually already have 3 million in total in the process pipeline, with lots more millions in the exploratory and non-committed stages. The latest of the already negotiated deals within that 3 million comes online in end of 2025.

We think there is a secular case for the company, although acknowledge that it remains speculative as there are still risks around the green thesis and the company is still burning cash.

For further details see:

Aker Carbon Capture: Major Orders Incoming, Project Completions