AKRO - Akero Therapeutics: Deceptively Promising

2023-11-22 04:24:01 ET

Summary

- Akero Therapeutics is a deceptively promising long at these levels.

- EFX still has to jump through clinical trials and has a long way to go until approval.

- The NASH landscape has become increasingly complex since the approval of GLP-1s and Resmetirom's successful phase three trial, and it is unclear if EFX can differentiate itself.

Introduction

Shares of Akero Therapeutics ( AKRO ) fell to 52-week lows earlier in October after reporting poor early results from a critical phase two NASH cirrhosis study; efruxifermin ((EFX)) failed to hit the fibrosis primary endpoint in that trial. Since then, the stock has rallied by approximately 40%, rising from ~$11.30 a share at the low to about $15.50 a share today. Investors seem to be betting that HARMONY - another phase two trial but for F2-F3 NASH patients - will report positive results in Q1'24.

Moreover, it seems that the market is starting to gain confidence that EFX can still become an FDA approved and commercially successful drug to treat NASH. Based on the existing data, I would agree with the former point. On the latter point, it is harder to say. Although EFX appears to work at face value, it is much less apparent that EFX has the necessary qualities to distinguish itself amid a complex treatment landscape.

Thesis

Due to future uncertainty and the competitive advantage that Madrigal's ( MDGL ) Resmetirom enjoys, I would assign Akero Therapeutics a sell rating. The challenge for Akero is to prove that EFX is differentiated. And the current data does not support this differentiation.

The Data Does Not Seem Bad

The reason for the precipitous drop in the stock price earlier in late October was that 36-week data from SYMMETRY - a phase two trial evaluating EFX as a treatment for F4 NASH patients with compensated cirrhosis - was unveiled. No statistical significance was achieved on either the 28 or 50-milligram dose for the primary endpoint of at least a one-stage improvement in liver fibrosis without the worsening of NASH vs placebo; the key secondary endpoint of NASH resolution was statistically significant for both dosages. It should be noted that a favorable dose-dependent trend towards fibrotic reduction was shown by EFX, even though this was not statistically significant. Treatment was well-tolerated with no major safety flags being reported. (Other than mild to moderate gastrointestinal events leading to a few discontinuations.)

At face value, the data does not seem so bad. At the very least, you would think that it would not warrant a ~60% drop in market capitalization. Bear in mind that this data is coming from a NASH population that has a very late stage of the disease (F4 patients with compensated cirrhosis.) At this stage, patients are on the verge of decompensated cirrhosis, where patients have an average survival of ~2 years without a liver transplant; the hurdle is quite high to begin with.

Moreover, this is a 36-week analysis of a 96-week long study. It could be true that it simply takes more time for fibrotic reduction to show separation from placebo. For the analysis to already show statistically significant reductions in NASH resolution (p<0.01 for both dosages) is impressive. The resolution rates of 63% and 60% for the low and high dosage respectively in this patient population is unprecedented.

The study met its primary endpoint for both the 50mg and 28mg EFX dose groups, with 41% and 39% of EFX-treated patients, respectively, experiencing at least a one-stage improvement in liver fibrosis with no worsening of NASH by week 24, compared with 20% for the placebo arm... In addition, 41% and 29% of patients treated with 50mg and 28mg, respectively, achieved both endpoints (NASH resolution and fibrosis improvement ?1 stage), compared with 5% for placebo.

Source: HARMONY Press Release , 9/13/22

Consider too that EFX achieved statistical significance in both NASH resolution and fibrosis reduction in another phase two trial, HARMONY: The key difference between HARMONY and SYMMETRY is that the former evaluated EFX as a treatment for the F2-F3 disease population. (This is the typical approach to evaluate a NASH therapy.) MAESTRO-NASH, the successful phase three trial Madrigal conducted to assess Resmetirom as a NASH treatment, enrolled no F4 patients . When you consider this context, SYMMETRY's failure is not as bad as it seems.

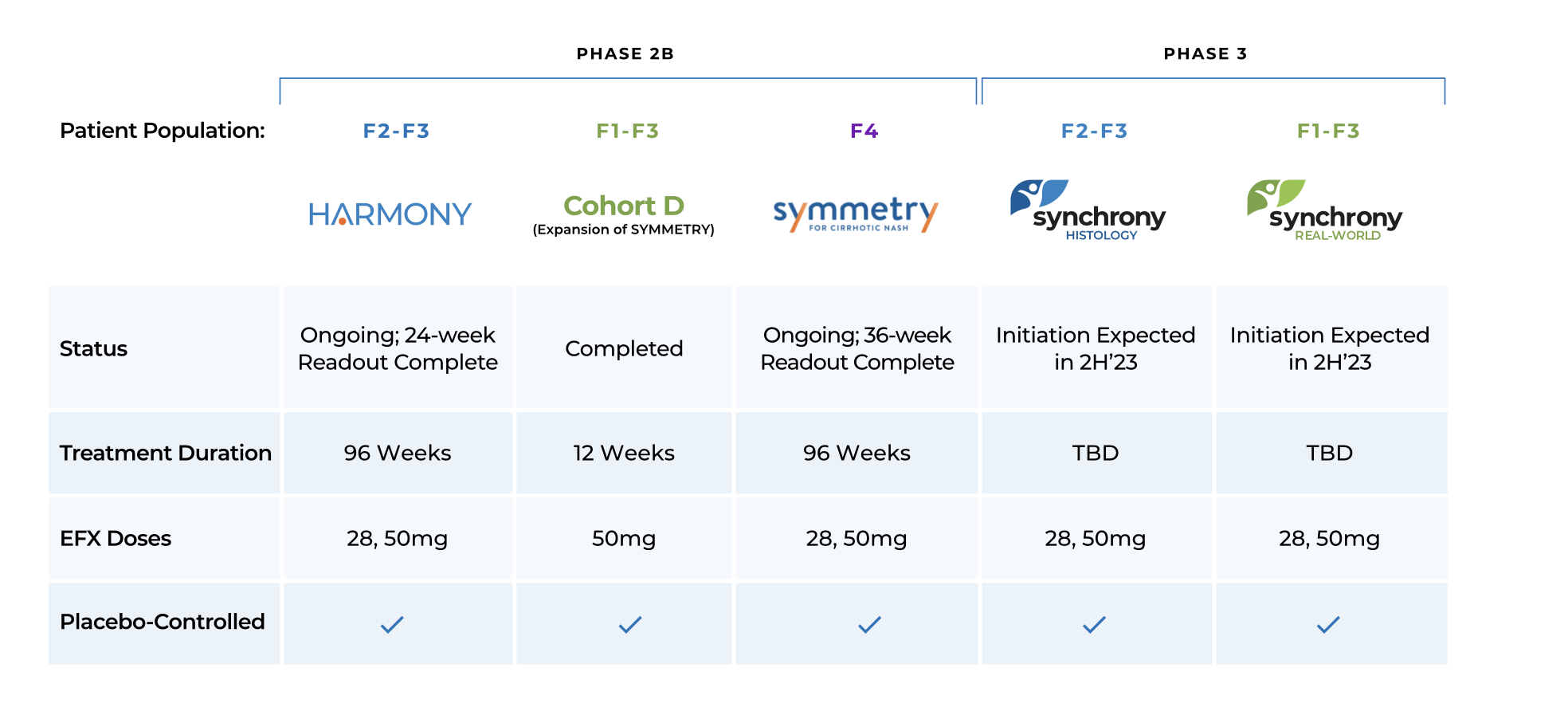

Akero Therapeutics' Clinical Trials (Akero Therapeutics' Investor Relations Material)

{kind=link}

Akero's approach of conducting multiple clinical trials for different patient subgroups makes sense when you consider the heterogeneous nature of NASH disease. A narrow miss on F4 patients does not preclude the FDA from granting accelerated approval to EFX based on the outcome of Synchrony and HARMONY.

Differentiation and Complexity

However, the challenge for Akero is that they need to not only get EFX past the finish line but also demonstrate superiority in a complicated treatment landscape. This is why the 36-week readout of SYMMETRY mattered so much; investors wanted to see if EFX could differentiate itself through anti-fibrotic effect. The primary endpoint miss at this juncture suggests that EFX will not satisfy these high expectations once SYMMETRY concludes at week 96.

Such a high bar is necessary because of Resmetirom's vast head-start. The FDA already accepted Madrigal's NDA for Resmetirom and set a priority review date of March 14, 2024. If approved, which I believe it will be, Resmetirom will have a huge head-start in defining itself as the sole treatment for NASH. If SYNCHRONY HISTOLOGY is initiated in December, and the treatment duration is the same as HARMONY and SYMMETRY, then it would take ~22 months before primary completion. Then, you have to add in the time it takes for Akero to put together an NDA package and the time for the FDA to review it. If the NDA timing for EFX matches Resmetirom's, it would add on another ~15 months. All in all, Akero is behind Madrigal by ~3 years.

Remember, Resmetirom already demonstrated its anti-fibrotic effect and NASH resolution in Maestro-NASH; the oral delivery mechanism of Resmetirom is also much more convenient than the subcutaneous injections needed for EFX. Once approved and given the opportunity to become the standard of care for NASH, it will become difficult to unseat unless a more compelling option comes forward. With the recent fibrosis endpoint miss, it becomes harder to sell EFX over Resmetirom. EFX also needs to, at the minimum, prove itself in SYNCHRONY and HARMONY. And exceeding expectations in SYNCHRONY is no guarantee, given the large graveyard of other NASH drugs that failed in phase three trials .

The path forward for EFX is complicated by the changing treatment paradigm of NASH too. There exists a palpable possibility that GLP-1 therapies may shrink the total NASH population by reducing the upstream obese population. ( Obesity is by far the top root cause of NASH.) It is also true that GLP-1s themselves may treat NASH directly. A key readout in February from Eli Lilly ( LLY ) evaluating Tirzepatide as a NASH treatment will provide the clarity needed on this concern.

Another complexity is that NASH resolution and fibrotic reduction are surrogate endpoints, so EFX will face an uphill battle against insurers in attaining coverage. The recent ICER report NASH articulates the reasoning behind why insurers might be resistant perfectly:

Although there is a tremendous need for disease-modifying treatment for NASH, given the lack of clinical outcome data, the spontaneous improvement of histology in 25% of untreated patients, the lack of long term safety data, and that it takes an average of seven years to progress one fibrosis stage, it will be reasonable for payers to use prior authorization as a component of coverage for NASH therapies. Payers should cover intensive weight management programs that include nutritionists and drug therapy given that resolution of NASH has been observed in up to 84% of patients within one year of bariatric surgery. Lifestyle interventions with a sustained body weight reduction of at least 10% lead to NASH resolution in up to 90% and regression in fibrosis in up to 45% of patients.

Think about how complex the commercial landscape may be in 2026. EFX may be competing against Resmetirom, GLP-1s and insurers who would prefer to have step therapy prior to covering any drugs. Without demonstrating clear superiority and differentiation from the standard of care, commercialization could prove itself to be difficult. This explains why the initial reaction to SYMMETRY was so stark.

Financials And Valuation

One solid aspect of Akero is that they have no shortage of liquidity to fund their trials and operations. As of their last quarter , they have ~$554 million in cash, cash equivalents and short-term marketable securities. They also have another ~$60 million in long-term marketable securities, bringing their total liquidity to ~$610 million. In contrast, their long-term debt stands at ~$20 million.

Averaging their net loss for the past four quarters yields a quarterly cash burn rate of ~$30 million. Assuming it holds steady at that level, Akero should have no problem covering the cost of EFX's development to approval. However, it will likely need to raise more money from either a partnership or shareholder dilution if it wishes to commercialize EFX.

As of the time of writing, each share of Akero trades at ~$16.50, yielding a market capitalization of ~$920 million. With an enterprise value of ~$330 million, it is clear that the market is not assigning much value to EFX. Valuing EFX itself is difficult, as there is still a great deal of uncertainty regarding its clinical profile, let alone compared to Resmetirom. Even less certain is how GLP-1s will modify the NASH landscape by 2026 or the effect of insurers pushing back against coverage. Such a great deal of uncertainty makes it difficult to find the true value of EFX.

In any event, I am skeptical that EFX can carve out a niche or successfully compete against Madrigal's Resmetirom. The first-mover advantage is difficult to overcome, and the superior convenience offered by Resmetirom's oral delivery cannot be overcome. (Remember, most NASH and NAFLD patients are asymptomatic, so ensuring ease of use to maintain compliance will be a top concern for those prescribing treatments.) Consequently, the difficulty of assigning any value to EFX compels me to think that Akero's correct valuation would be cash value; this suggests a price per share of ~$11 and a downside of ~40 percent from the current valuation.

Conclusion

The complicated path forward for Akero is long and cloaked in uncertainty. Akero is behind by three years at the very least and still needs EFX to pass through phase three trials. And although EFX shows therapeutic promise, it is difficult to determine from the existing data if it can outshine Resmetirom. Due to the magnitude of the uncertainty, I would assign a sell rating to Akero.

Risks To Thesis

1) The bull thesis is not far-fetched. The bank-shot lies with a successful 96-week readout of SYMMETRY. If EFX manages to hit on the primary endpoint of fibrosis reduction in F4 patients with decompensated cirrhosis, then that would meaningfully differentiate it from Resmetirom. Or, if it manages to demonstrate clearly better endpoint and/or outcomes data through HARMONY/SYNCHRONY.

2) Madrigal could receive a complete response letter ((CRL)) from the FDA in response to its NDA for Resmetirom. There has been some speculation from bears that Madrigal engaged in a sleight of hand by changing its fibrosis endpoint in MAESTRO-NASH before the readout. Such a scenario would not be without precedent too, as Intercept's OCA NDA for NASH died in regulatory limbo following its CRL from the FDA. Although I find FDA rejection unlikely, it could delay Madrigal anywhere from 6 to 24 months depending on the nature of the CRL. This outcome would propel the bullish thesis behind EFX by lowering the risk from competition.

For further details see:

Akero Therapeutics: Deceptively Promising