AKZOF - Akzo Nobel: Expect A 20% EBITDA Increase After A Tough 2022

Summary

- Akzo Nobel is one of the largest producers of paint and coatings in the world.

- 2022 was tough due to higher operating costs, raw materials price increases and higher transportation expenses.

- The company guided for an EBITDA of 1.2-1.5B EUR this year. The midpoint could result in an EPS of 3.75 EUR and an FCFPS of around 4 EUR.

- Don't expect a share buyback program this year: the company will focus on debt reduction.

Introduction

Akzo Nobel (AKZOF) (AKZOY) is one of the largest producers of paint and paint-related products in the world (Sherwin-Williams ( SHW ) and PPG Industries ( PPG ) are larger) and continues its growth by pursuing smaller bolt-on M&A transactions. In 2022, the company entered into an agreement to acquire the African division of Kansai Paint , which generates about 280M EUR of revenue and is active in 12 countries. This acquisition will close later this year after dealing with antitrust concerns in South Africa.

{kind=link}

Akzo Nobel's primary listing is on Euronext Amsterdam where the company is trading with AKZA as its ticker symbol . As it clearly is the most liquid listing with an average daily volume of approximately half a million shares, I'd strongly recommend to use the Amsterdam listing to trade in Akzo's shares. There also are options available. There are currently 170M shares outstanding, resulting in a market capitalization of just under 12B EUR.

2022: a lower EBITDA but 2023 should show growth again

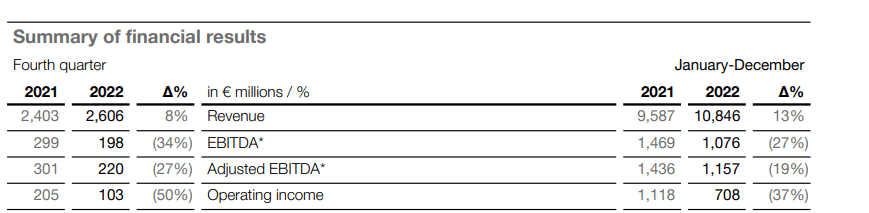

It's clear 2022 wasn't a great year for Akzo Nobel. The company had to deal with higher raw materials expenses, a higher transportation cost and just the impact of inflation in general. Despite reporting a 13% revenue increase, the EBITDA shrank by 27% and the adjusted EBITDA fell by 19% which clearly indicated severe pressure on the margins as the adjusted EBITDA margin decreased from 15% to less than 11%.

{kind=link}

The expectations weren't high for Akzo Nobel and fortunately the results did not miss those expectations. Looking at the full-year results, the company obviously remained profitable but it's clear the net income didn't come even close to the 2021 results.

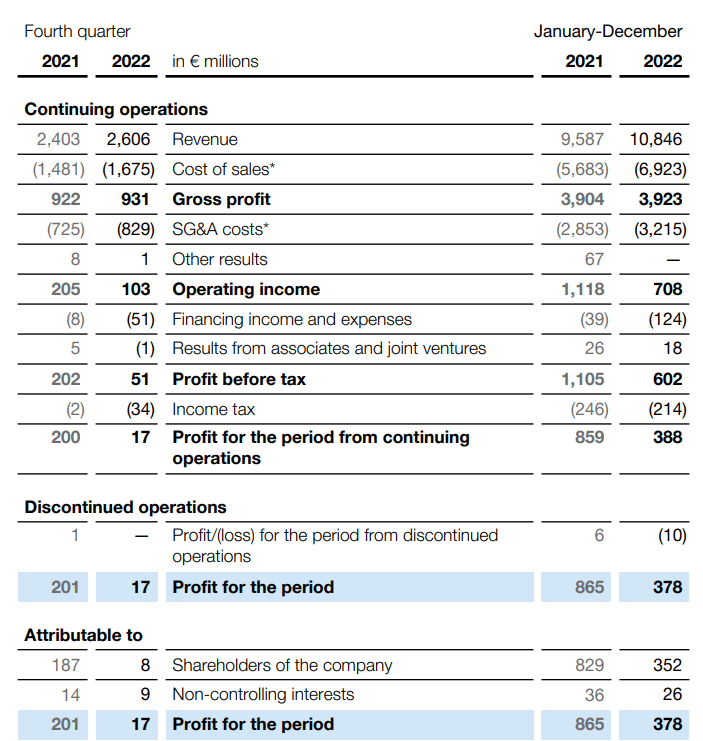

As you can see below, the operating income fell to just 708M EUR while the finance expenses increased as well resulting in a decrease of the pre-tax income of almost 50%. Unfortunately the tax pressure increased with an average tax rate of approximately 35% (compared to just around 22% in FY 2021), resulting in a net income of 388M EUR.

{kind=link}

From that net income, we still have to deduct the 10M EUR loss attributable to discontinued operations and the 26M EUR attributable to non-controlling interests. This means the net income attributable to the common shareholders of Akzo was approximately 352M EUR. Divided over 170M shares (I'm not using the weighted average share count but the current share count), the EPS was 2.07 EUR.

As no one should pay 33 times earnings for a paints and coating company, I think some additional clarification is needed. First of all, the increase of the finance expenses is mainly related to FX changes: Those increased by 64M EUR compared to FY 2021. Additionally, the financing income was just 10M EUR compared to the 28M EUR in 2021 (both interest incomes are non-recurring items). So this means the finance expenses in FY 2022 came in substantially higher either due to non-recurring items or FX changes. The net interest payments did increase but by just 25M EUR which is obviously much more manageable.

Secondly, the high tax rate was related to a 13M EUR UK tax charge and the non-deductible charges resulting from hyperinflation accounting. Additionally, the 2021 tax rate was lower than average so that also skews the comparison a little bit. Akzo Nobel is guiding for an effective tax rate of 27% in 2023.

So if I would add back 70M EUR in non-recurring or non-cash finance expenses and apply a normalized 27% tax rate, Akzo Nobel's net income in 2022 would have come in around 450M EUR or 2.65 EUR per share.

The cash flow result of Akzo Nobel was very decent as well. As you can see below, the reported operating cash flow was 263M EUR, but this includes 509M EUR in working capital investments as well as 64M EUR in cash deposits for post-retirement benefit obligations and other cash provisions. It also looks like the company paid about 10M EUR in cash taxes it didn't owe based on the FY 2022 income statement (about 224M EUR was paid although only 214M EUR was owed).

Akzo Nobel Investor Relations

On the other hand we should probably also deduct about 85M EUR in lease payments. This is not specified but considering the balance sheet contains about 85M EUR in short-term lease liabilities, I think using that number as lease payments is fair. This means the adjusted operating cash flow was approximately 670M EUR (after also taking the interest of minority owners into account).

The total capex was 292M EUR, resulting in a free cash flow result of 378M EUR or 2.22 EUR per share.

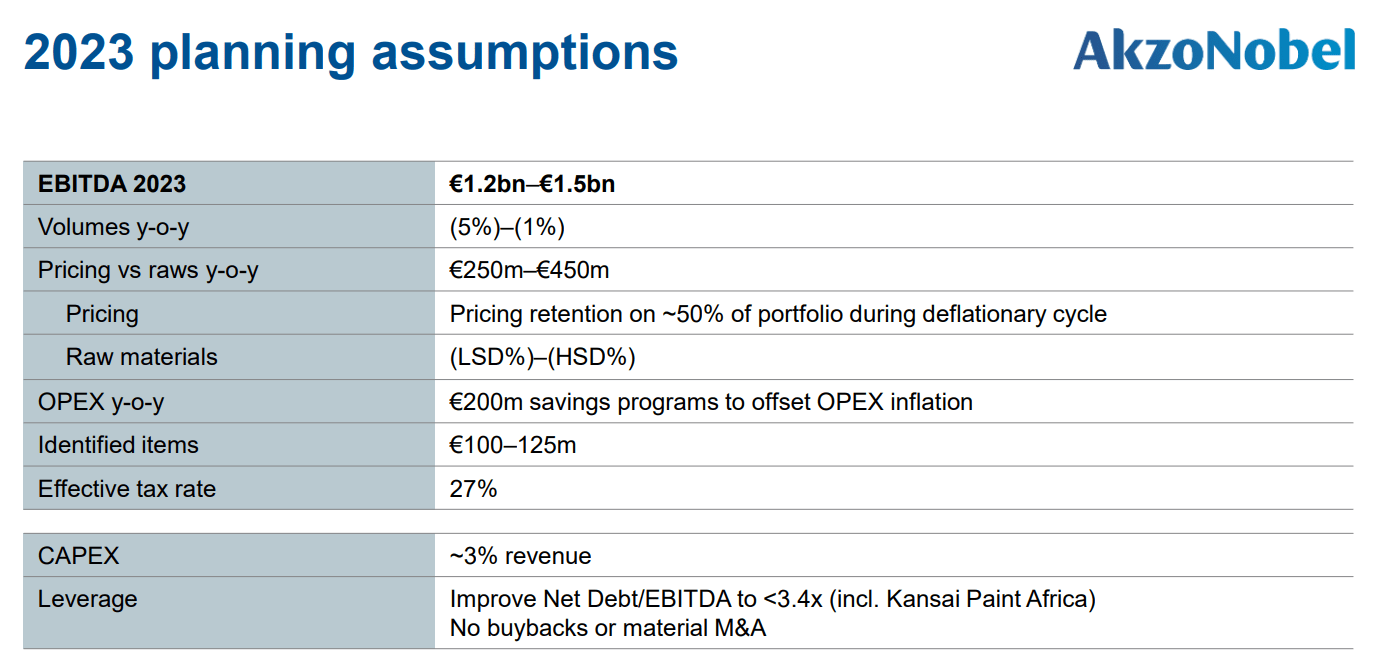

While that's still not great, we should keep an eye on the future as Akzo Nobel expects a potentially substantial EBITDA increase. Although the adjusted EBITDA came in at just 1.16B EUR in FY 2022, Akzo is guiding for a 1.2-1.5B EUR EBITDA result in 2023 (which is substantially lower than the 2B EUR it expected just one year ago ). That still is a wide margin and I expect the company to narrow it down as the year advances, but keep in mind that even using the midpoint of the guidance, 1.35B EUR, would increase the cash flow by about 200M EUR.

But let's take this step by step.

We know the depreciation charges are about 400M EUR per year, and we know the normalized finance expenses will likely be somewhere around 75M EUR (excluding FX changes which you can't really predict anyway). This means the pre-tax income will come in around 875M EUR, resulting in a net income of 640M EUR using the 27% tax rate provided by Akzo. That's approximately 3.75 EUR per share and this will likely be higher in the future (no buybacks are planned for this year) as Akzo will continue to buy back its own shares, thereby reducing the share count.

{kind=link}

We also know capex will likely continue to hover around 300M EUR per year (including growth initiatives), and assuming the sustaining capex is approximately 50M EUR lower, the FCFPS will be roughly 30 cents per share higher and come in at around 4 EUR per share.

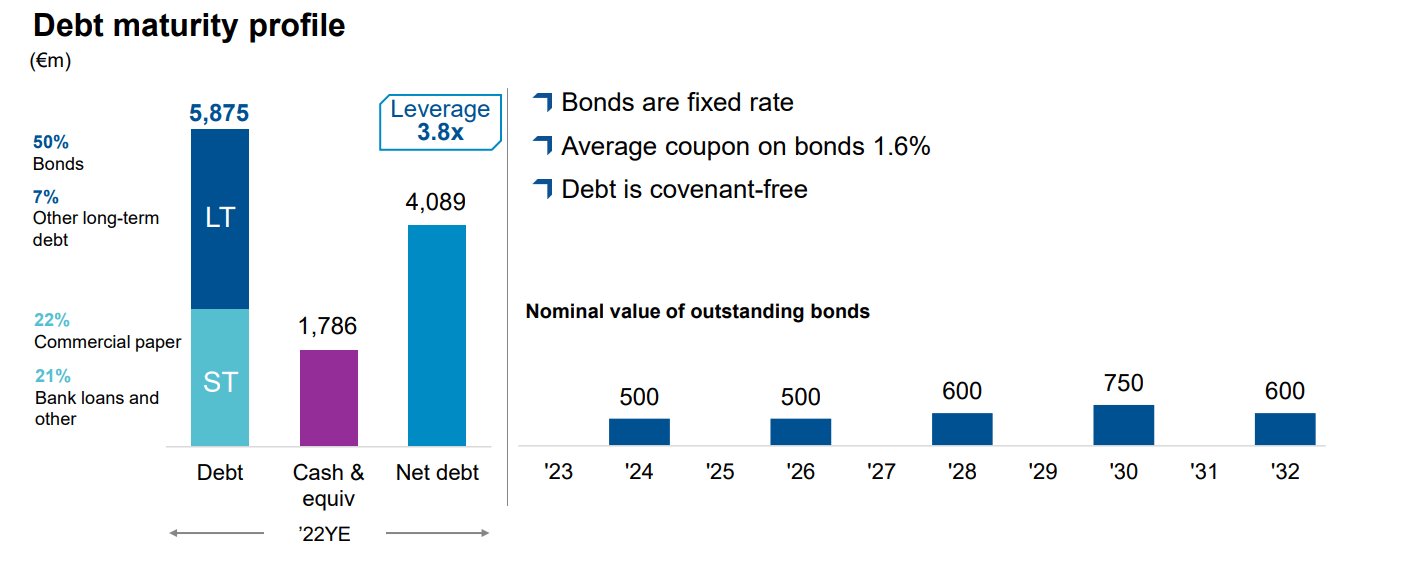

Akzo won't repurchase any shares this year as it will focus on bringing its net debt down to achieve a debt ratio of less than 2 times EBITDA. Assuming the company meets the midpoint of its EBITDA guidance, this means Akzo wants to reduce its net debt to 2.7B EUR (from 4.1B EUR as of the end of 2022). As it also still needs to pay for the Kansai Africa transaction, I'm not expecting a material reduction in the net debt (perhaps it will move down to 3.8B EUR or so) but the higher EBITDA result should have a noticeable impact on the debt ratio which will fall to 3.4 by the end of this year (including the impact of Kansai).

{kind=link}

Investment thesis

I have no position in Akzo Nobel as the company isn't exceptionally cheap (trading at about 11-12 times EBITDA using the midpoint of this year's EBITDA guidance) but I do expect the underlying free cash flow result to increase toward 7% either this year or by next year. Additionally, I like the company's focus on deleveraging as that will obviously reduce the impact of the increasing interest rates. While Akzo won't be immune, it actually has a shot at generating and retaining sufficient cash to just pay off the bonds that will mature this decade if the refinancing climate isn't optimal. That being said, the Eurobonds on the market are all trading with YTMs in the mid-3% range, so I don't anticipate any major issues on the refinancing front.

Akzo proposes to pay a final dividend of 1.54 EUR per share, which brings the full-year dividend to 1.98 EUR per share, the same level as last year. This represents a dividend yield of just under 3% (subject to the standard 15% Dutch dividend withholding tax).

I currently have no position in Akzo Nobel but I'm considering writing out of the money put options. The P58 for June, for instance, has an option premium of 1.05 EUR which would result in an effective purchase price of 57 EUR per share which would represent an EV/EBITDA multiple of 10 and a free cash flow yield of 7%. And perhaps I will go a little bit further out with a P45 or P50 for December with an option premium of respectively 0.75 EUR and 1.20 EUR. In that case, even if I don't get assigned, I'd still make some money on the option premiums.

For further details see:

Akzo Nobel: Expect A 20% EBITDA Increase After A Tough 2022