PPG - Akzo Nobel: Underdiscussed And With Great Potential

2023-09-20 17:03:51 ET

Summary

- Akzo Nobel is positioned for solid long-term growth after a financial decline due to a cyclical downturn in the paint and coating industry.

- The company is the third-largest player globally in its respective industry, with a strong portfolio of brands and products and exposure to faster-growing industry verticals.

- Akzo Nobel has promising growth prospects, especially in the Chinese market, and is well-positioned to capitalize on the steady growth trajectory of the industry.

- Its attractiveness to investors is boosted by significant share buybacks and a 3% dividend yield.

- Financially, the company exhibited resilience in H1, with revenue growth impacted by exchange rates but offset by price increases. Margin improvements were particularly noteworthy.

Investment thesis

I initiate my coverage of Akzo Nobel N.V. ( AKZOY ) with a Buy rating following my in-depth research of the company and the underlying paint and coating industry. The company looks exceptionally well positioned for solid long-term growth after a significant financial decline following a cyclical downturn in the industry.

Akzo Nobel emerges as a compelling investment opportunity in the world of paints and coatings. This industry giant stands tall as the third-largest player globally, boasting a robust portfolio of brands and products that cater to a wide range of markets and applications. With 2022 revenues nearing €11 billion and a presence in over 150 countries, Akzo Nobel's global reach and diverse revenue streams fortify its position and mitigate risks associated with regional dependencies.

The outlook for Akzo Nobel remains promising, thanks to several key factors. First and foremost, the paints and coatings industry, although often overlooked, plays a pivotal role in various sectors, with a market value exceeding €140 billion. Projections indicate a steady growth trajectory, with a forecasted CAGR of 5% through 2030. Crucially, Akzo Nobel is excellently positioned to capitalize on this growth as one of the industry leaders, holding top positions in multiple product categories.

Furthermore, the Chinese market emerges as a significant growth opportunity for Akzo Nobel, with strategic investments and the leverage of its premium Dulux brand in the region. As a result, long-term sales growth averaging 3-7% annually seems attainable, albeit with cyclical fluctuations.

Financially, the company exhibited resilience in H1, with revenue growth impacted by exchange rates but offset by price increases. Margin improvements were particularly noteworthy, as evidenced by higher gross and operating margins. The company's capital allocation strategy, focusing on Capex, dividends, and share buybacks, reflects its commitment to rewarding shareholders. However, the relatively high net debt/EBITDA ratio and cyclicality in results warrant cautious consideration.

In this article, I will take you through my analysis of the company and the underlying industry, as well as the latest developments and financial projections.

Akzo Nobel – An introduction

Akzo Nobel is a global leader in the field of paints and coatings, operating multiple leading brands in these areas. The company is the third largest in its respective industries, only behind peers Sherwin-Williams ( SHW ) and PPG ( PPG ) in terms of sales, with 2022 revenue of close to €11 billion. Akzo Nobel operates in two main business segments:

Decorative Paints: Offering a wide range of paints and coatings for homes and buildings, Akzo Nobel's Decorative Paints segment focuses on providing aesthetically pleasing and durable solutions for interior and exterior surfaces.

Performance Coatings: This segment caters to various industries, including automotive, aerospace, marine, and industrial, with high-performance coatings that protect and enhance the performance of a wide range of products and surfaces.

The company operates in over 150 countries around the world, employing over 30,000 people in a total of 120 manufacturing facilities located across every continent. This strong global presence and extensive network of research and manufacturing facilities ensures that it can provide tailored solutions to meet customers' unique needs worldwide.

As a result, Akzo Nobel’s revenue diversification is looking solid as it is not overly dependent on any particular region, lowering its risk profile. In addition, the majority of the company’s revenues come from developed economies, again lowering sales volatility and risks. Looking into more detail, the largest and most important one for Akzo Nobel is the EMEA, which accounts for 50% of the company’s revenue, followed by Northeast Asia (mostly China) with just 18%. The Americas and South Asia Pacific account for the remaining 32%.

A strong sales outlook thanks to a solid underlying industry and strong competitive positioning

The paint and coating industry might sound like a minor industry as it creates little headlines and is a little discussed subject. However, meanwhile, the industry is worth over €140 billion and is of incredible importance globally. While the paint and coating industry is not a massively exciting or fast-growing one, it should still be able to support steady growth for Akzo Nobel, as Fortune Business Insights predicts the industry will grow at a CAGR of 5% through 2030.

Crucially, Akzo Nobel is one of the industry leaders and, therefore, well-positioned to benefit from this growth. Moreover, management aims to keep its growth rate above the industry as it seeks to take more market share and is exposed to several positive trends.

That the company has indeed a strong brand and product portfolio with which it is able to capture a strong share of this relatively large industry is highlighted by the fact that the company, apart from being the third largest in terms of revenue globally, also holds a #1, #2, or #3 position in each of its product categories. For example, the company is the leader in powder coatings and the EMEA and LATAM paint industry, with a total market value of €28 billion.

Looking deeper into the growth expectations, we can see that the coating industry is seeing tailwinds from multiple secular and global trends like the growth in electric vehicles, the shift from plastic to metal across industries like beverages, high demand for sustainable products, growing demand for electronics, and growing marine and airline industries. All of these factors and trends above drive a solid outlook for the coating industry in one way or another.

The growth in EVs, in particular, is of massive benefit to Akzo as the leader in powder coatings, which are most often used in battery packs. Crucially, the company already has approvals of its products by the seven largest automotive OEMs and battery manufacturers, which together account for 70% of global shipped automotive battery packs, benefitting Akzo.

Also, in the packaging coatings market, Akzo is winning market share, and again, this is a highly attractive industry due to the shift from plastic to metal. The company already is a key supplier to all leading beverage brands and is seeing fast growth in emerging markets. The company’s success in the beverage industry is highlighted by a 1% market share gain. With this transition expected to push on, this, in particular, should remain a growth market for Akzo, boosting its growth to above the industry average.

Moving on, just like the coating market, the paint market is also seeing structural tailwinds, including a growing DIY market following COVID-19 and the boost the industry is getting from e-commerce. Furthermore, factors like an expanding distribution network, brand investments, market share gains, and acquisitions should allow Akzo to boost growth in its already largest EMEA market. The company still sees plenty of growth opportunities, even in this mature market.

However, the Chinese market might be the largest opportunity for Akzo in terms of growth in paint revenues. The company is rapidly expanding its operations in the country and is successfully leveraging its premium Dulux brand to take market share. With China also being one of the largest paint markets, these are crucial moves by Akzo. Management has long ago acknowledged these opportunities as it has been shifting Capex toward this region to fully benefit from this market's opportunities.

As a result of the above-discussed growth expectations, secular drivers, and Akzo’s favorable industry positioning, I believe the company should be able to report long-term sales growth at an average of 3-7% annually. We should add that the industry has proven to be quite cyclical as it is heavily exposed to economic growth and the DIY and home improvement industry. This cyclicality led to Akzo Nobel volumes taking a hit in recent years and quarters and is something to consider when investing in this company.

The H1 performance was respectable and the company has room for margin improvements

Akzo Nobel released its H1 results on July 25 and reported revenue that was flat YoY at €5.4 billion as the company’s results were negatively impacted by exchange rates (excluding this, revenue was up 5% YoY). Furthermore, as seen in previous quarters, volumes were down in the first half of the year by 2% as the company continues to see lower demand for its products due to decreased consumer spending power as a result of high inflation, similar to what is seen in the home improvement market. Luckily, management was able to offset this volume decline by increasing prices by 6%.

Looking at the bottom line, we can see that despite a flat top line, Akzo was able to improve margins and drive growth in operating cash flows. The gross margin of 38.7% was up 120 basis points YoY, which led to a 5% increase in operating income to €461 million, or 8.5% of revenue, up 40 basis points YoY. The EBITDA result improved even more as this was up 7% YoY to €702 million, highlighting an improved EBITDA margin of 13% versus 12.1% in the previous year.

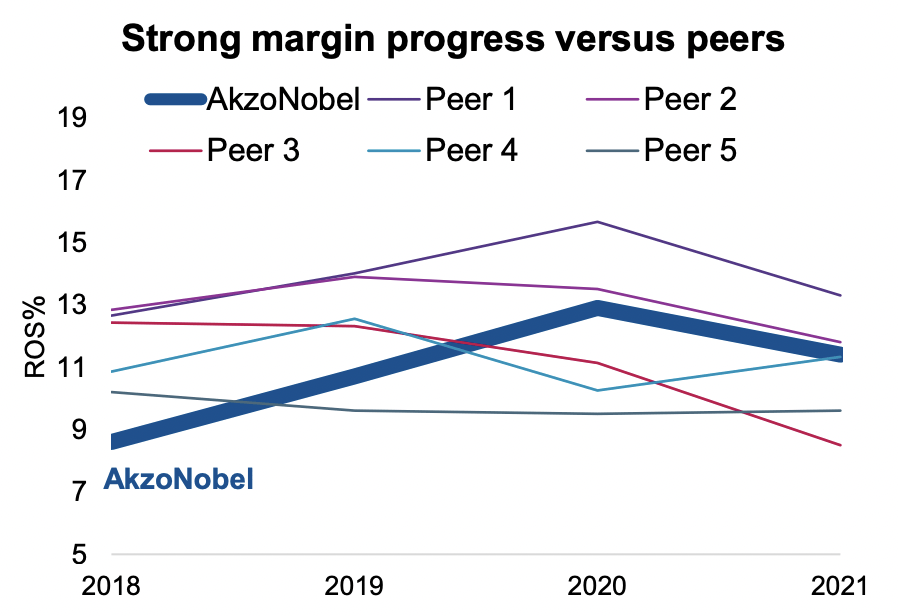

Free cash flow also turned positive from a negative €119 million last year to a significant €249 million in H1 of this year. However, EPS of €1.65 was still down 3% YoY. Still, when compared to peers, Akzo Nobel has shown a much stronger margin development in recent years and its decline from the last couple of years is an industry-wide phenomenon.

{kind=link}

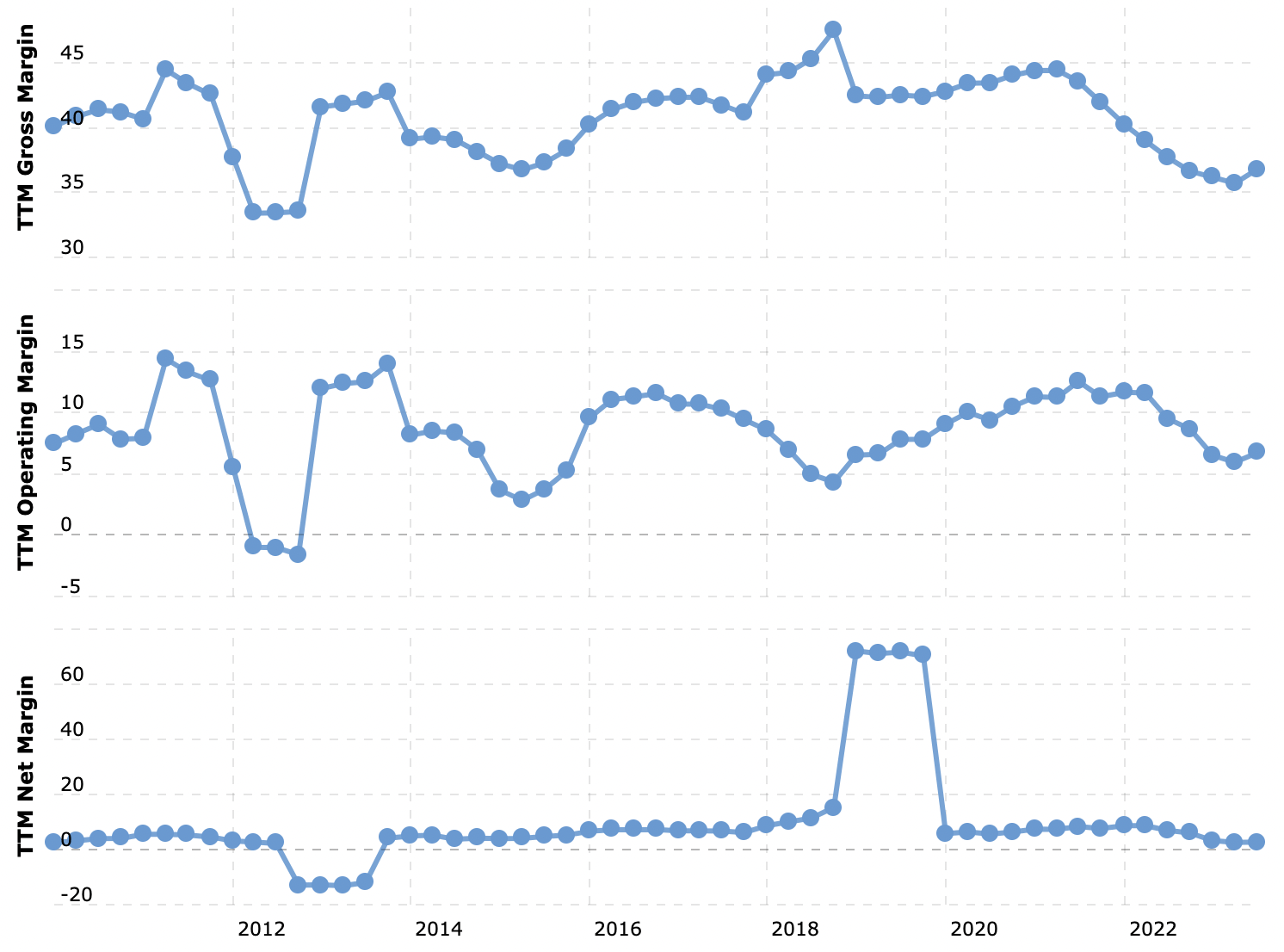

Looking at the margin development over the years, we can see the sales cycles reflected and very limited margin improvement. Whether it’s the gross margin, operating margin, or net income margin, all show little improvement overall, with margins sitting around the same level as they were in 2015, which makes me somewhat wary of whether management will be able to meaningfully improve margins going forward.

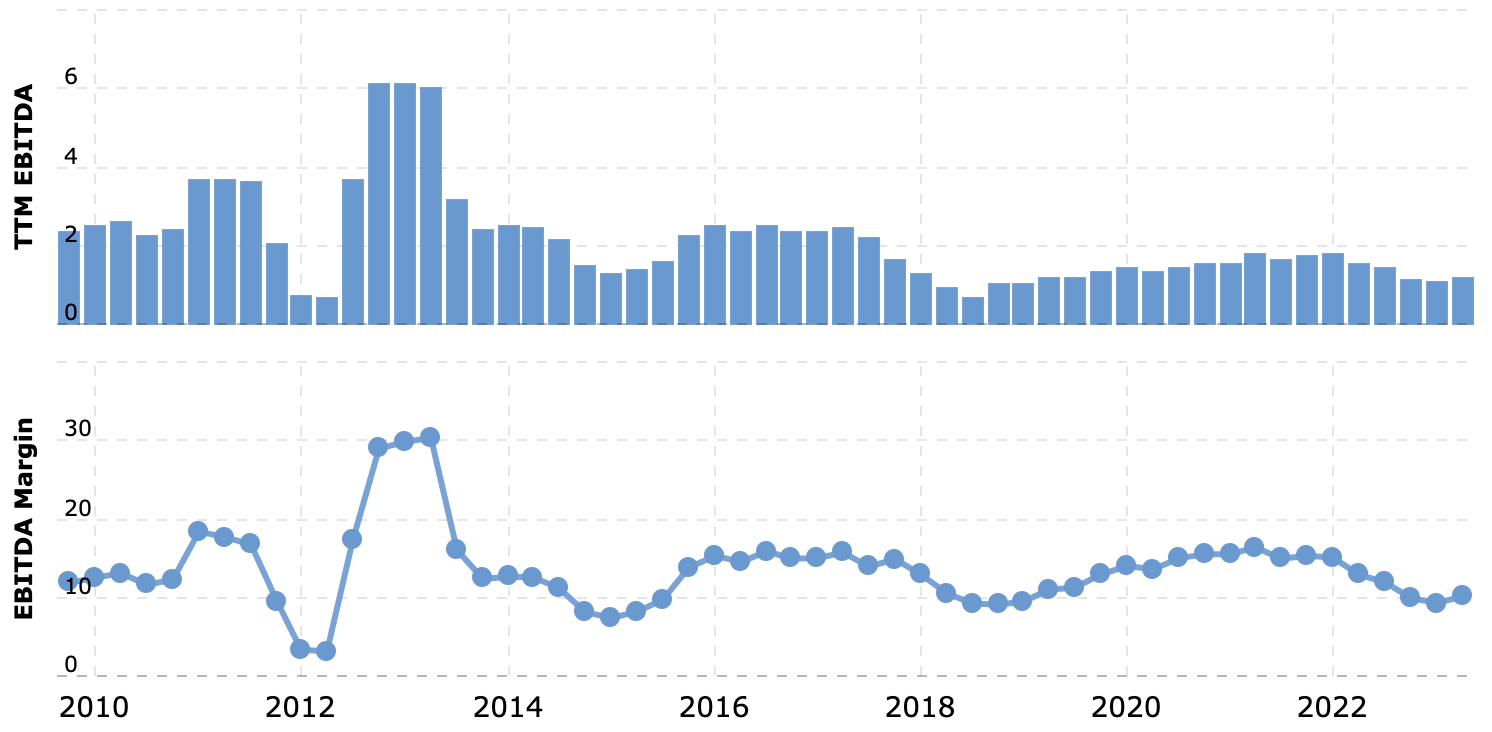

Management targets significant EBITDA growth over the next couple of years. I believe there is plenty of room for improved efficiency and cost-saving potential, but whether management can realize this remains a question with little positive data to go on. For now, I believe it is safe to assume some margin improvement (say 50 to 100 basis points of EBITDA margin expansion annually) over the longer term to drive slightly faster EPS growth in the 6-9% range. Do note that this excludes the next couple of years as margins will continue to improve rapidly from cyclical lows, as highlighted below. Therefore, EPS growth in the next couple of years will sit much higher.

Akzo Nobel EBITDA margin development (Macrotrends)

{kind=link}

{kind=link}

The company’s capital allocation strategy is also looking strong, with it aiming to invest around 3% of revenue in Capex consistently, steadily grow the dividend, and keep looking for strategically aligned and value-creating acquisitions. The 3% Capex target is already up from an average of 2% over the last decade and it also plans to boost growth in the next couple of years as it shifts its Capex investments toward growth from maintenance, with around 60% of Capex meant to drive growth going forward. I expect this to positively impact reported growth compared to previous years.

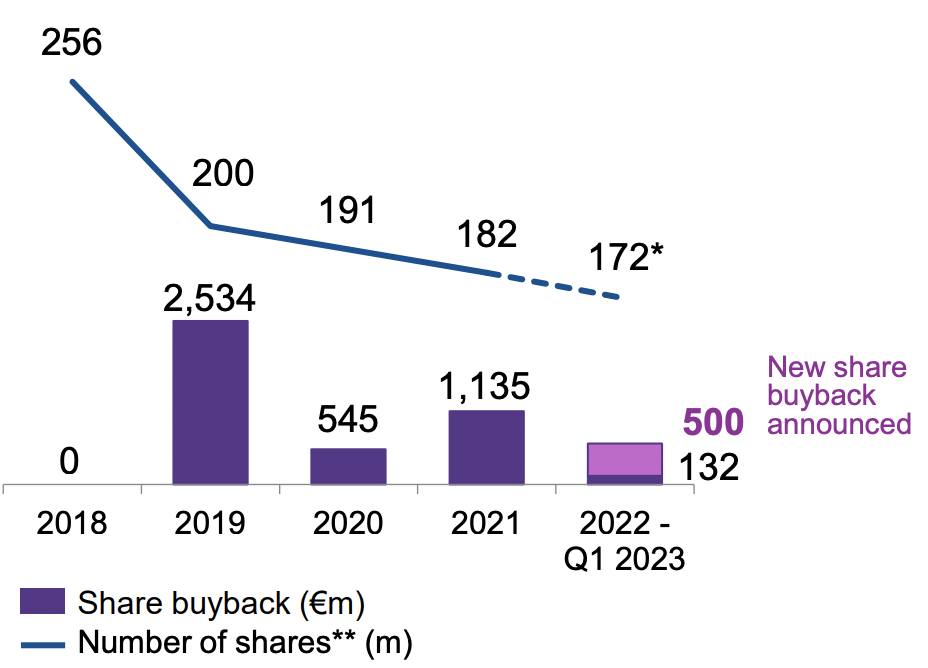

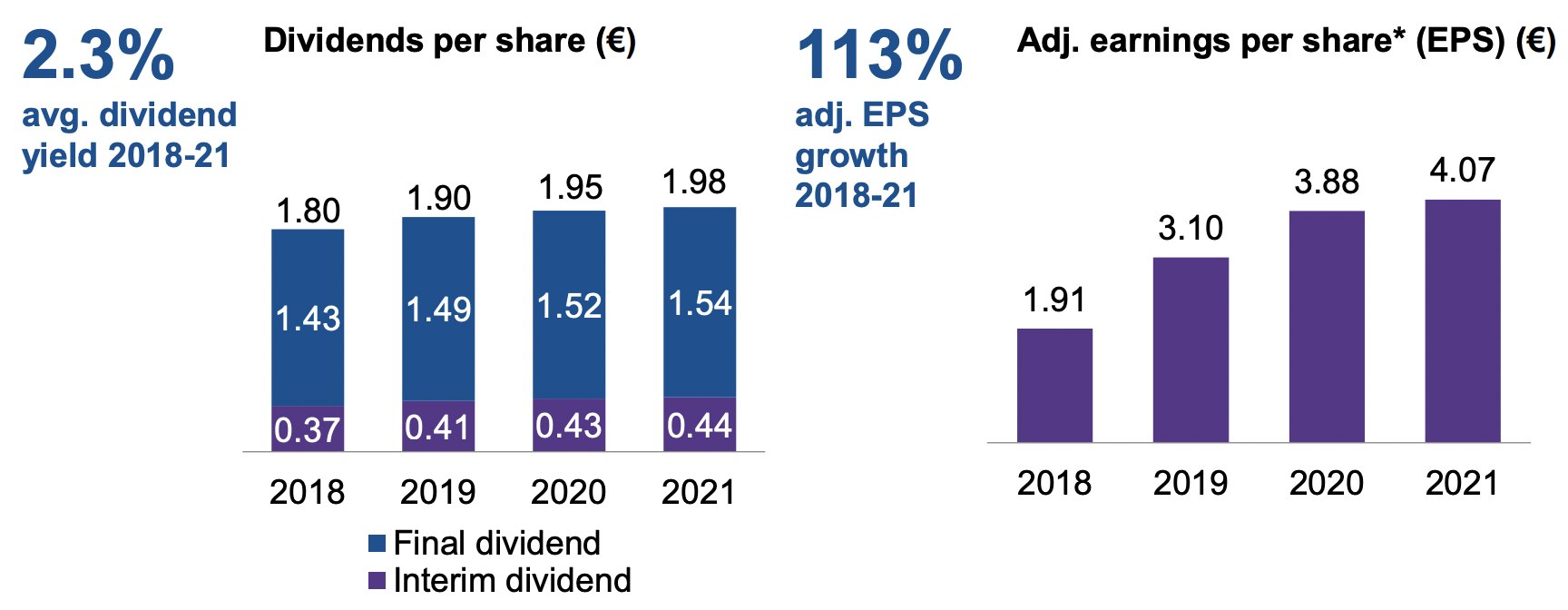

Moreover, regarding capital returns to shareholders, investors have little to complain about as shares currently yield approximately 2.9% based on a 2023 dividend of €1.98 per share, sitting above its average yield of 2.3% over the last years. Furthermore, the company has already retired 29% of outstanding shares since 2018, partly fueled by the sale of its chemicals business in 2019, but nevertheless highlighting that management is focused on rewarding its shareholders.

Akzo Nobel outstanding shares reduction (Akzo Nobel)

{kind=link}

It plans to keep returning cash to shareholders as it aims to steadily keep increasing the dividend while also continuously buying back shares with the remaining cash. However, share buybacks will likely remain subdued in the next couple of years as management will focus on bringing down its debt first, reserving the cash for this. Still, investors will see plenty of returns.

{kind=link}

On the note of its debt, the company's financial position might be one of the only negative aspects of this business. The company has a net debt/EBITDA ratio of 4x, which to me, is way too high considering the company’s results are exposed to quite some cyclicality. This negatively impacts its risk profile.

Management aims to reduce this to a far healthier level of around 1-2x. This should be well achievable as the operating environment improves further over the next few quarters and the company’s EBITDA results rapidly increase. This should be able to lower this number to 3.4x by the end of the year, showing significant progress. However, this is still up from the 3.2x reported at this time last year. Real progress is expected after 2023 as higher EBITDA should help lower the leverage to below 2x within a few years. As a result, I am not overly worried right now, especially as the underlying industry fundamentals are improving. This should give the company plenty of time to improve its financial profile.

Outlook & valuation

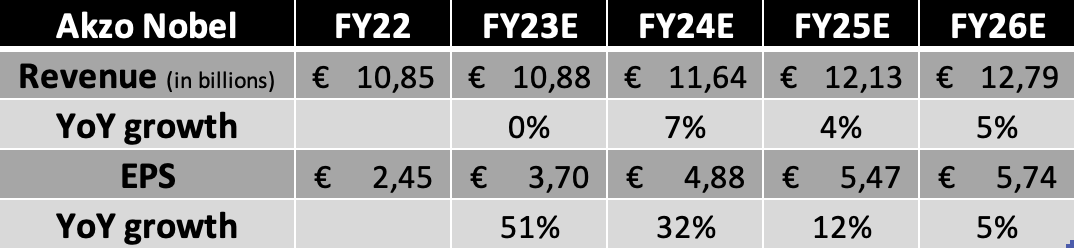

Following its Q2 results, management upgraded its FY23 outlook and now expects to deliver €1.40 to €1.55 billion in adjusted EBITDA and volumes to improve in H2 and be approximately flat YoY. Adding this guidance to my analysis of the company and the underlying industry, I arrive at the following financial projections through 2026.

Financial projections (By Author)

{kind=link}

(This includes FY23 EBITDA of €1.58 billion.)

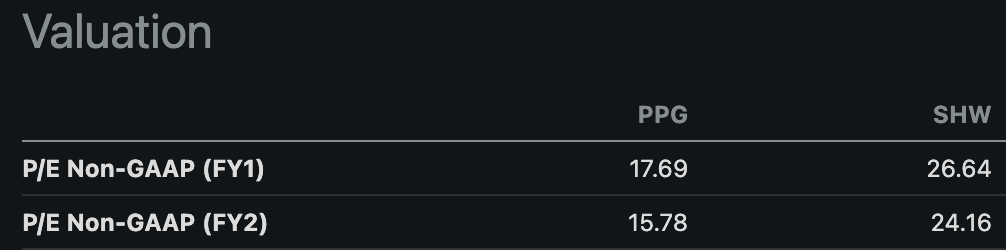

Based on these assumptions, shares are currently valued at 18.5x FY23 EPS, which is far from cheap for a cyclical stock growing at mid-single-digits. However, this is based on a depressed EPS level. If we shift to the FY24 projection, shares are currently valued at a forward P/E of 14x, which is looking much better. Also, when compared to its two larger peers, shares are looking quite attractive as these trade at a discount to peers based on FY24 EPS estimates. Meanwhile, Akzo Nobel pays a far higher dividend while having a similarly strong competitive position.

Valuation peer comparison (Seeking Alpha)

{kind=link}

As the company has a decent growth outlook, substantial market share, and operates in a respectable industry driven by several secular tailwinds while also being shareholder-focused, I believe it deserves a valuation more in line with its peers. Therefore, I believe a 16x P/E ratio is more than fair here and gives us a decent amount of downside protection. Based on this belief and my FY24 EPS estimate, I calculate a target price of €78 per share. Going with an annual return of 9% (12% including dividends), the current fair value sits around €68.60 per share, meaning shares are currently trading around fair value.

Conclusion

I went into this analysis entirely blank on the company, but I must admit I am quite impressed by it. Akzo operates in a very big and respectable industry that is highly important to many of the world’s largest industries.

Furthermore, as the industry is expected to grow at a solid rate of mid-single-digits and with Akzo Nobel being one of the three industry leaders with exposure to faster-growing industry verticals, I am quite bullish on the company’s growth outlook, which should be able to beat the industry average. Moreover, from a current depressed level, the EPS outlook for the next several years is impressive, and even beyond that, it should be able to deliver high-single-digit growth for shareholders.

With a price target of €78 and a fair share price of €68,60, I believe shares currently are fairly valued, potentially offering very solid double-digit annual returns to investors in the long term when including its 3% dividend yield.

All taken into consideration, I am enthusiastic about Akzo Nobel and as shares are fairly valued, I rate these a Buy

For further details see:

Akzo Nobel: Underdiscussed And With Great Potential