ALG - Alamo Group Provides Investors With An Attractive Long-Term Opportunity

2023-04-19 03:51:13 ET

Summary

- Alamo's mid-term objective is an impressive 12% operating margin, which they are well on their way to achieving.

- Strong sales performance and a sizable backlog signal an approaching era of increased gross margins for Alamo.

- Alamo's mid-term objective is an impressive 12% operating margin, which they are well on their way to achieving.

Thesis

In my article, I explore the hurdles Alamo Group Inc. (ALG) currently faces in order to maintain a satisfactory rate of revenue growth and profitability despite scarcity of resources, labor shortages, and inflationary tendencies. I examine how sound decisions on expenses, sales volumes, and prices can assist Alamo with overcoming these obstructions for their success beyond 2023.

Growth Leads to Higher Margins and Steady Sales

In my estimation, Alamo's strong sales performance and sizable backlog signal an approaching era of increased gross margins. The company has skillfully reassessed its backlog, giving prominence to the Vegetation Management sector, while reducing work in progress. This, combined with declining SG&A expenses as a proportion of sales and the progression towards equipment electrification, lays the groundwork for continued margin expansion.

Moreover, Alamo's aggressive entry into large-scale M&A activities , supported by the thriving European market, could offer a promising outlook for growth opportunities. Furthermore, although often overlooked as important, I happen to think that the company's commendable efforts in expanding apprenticeship programs, automating certain tasks, and addressing labor shortages through community engagement deserve praise.

A striking 13% annual sales growth has also captured my attention, with a steady rise projected for 2023, provided supply chain improvements materialize. Alamo's unwavering commitment to executing their make and market strategy, streamlining operations, and investing in manufacturing expertise places them firmly on the path to achieving their mid-term objective: an impressive 12% operating margin.

Strengthening Performance, Growing Profits

The dynamic Agricultural sector surrounding Alamo , demonstrated by solid bookings and high activity levels, as well as the positive reception of their comprehensive product delivery strategy in the Industrial division, should instill confidence as well as the company's adept handling of inflation through price increases and operational improvements that have successfully bolstered their profit margins.

So upon examining the fourth-quarter and annual figures for 2022 , you can see that a distinct trend of vigorous growth and profitability becomes evident whereby a 15% jump in consolidated net sales, increased net income, and a remarkable 26% backlog growth essentially lay the foundation for a bright start to 2023. Therefore, focusing on their objectives - such as improving supply chain performance, increasing internal efficiencies, speeding the hiring of qualified staff quickly and strengthening manufacturing capabilities and presence - will be vital in maintaining this upward momentum. As such, Alamo's Board's recent approval of an increase of 22% to its regular quarterly dividend for 2023 serves as further evidence of their solid financial standing and unwavering commitment to creating shareholder value.

Industry Outlook & Peer Evaluation

{kind=link}

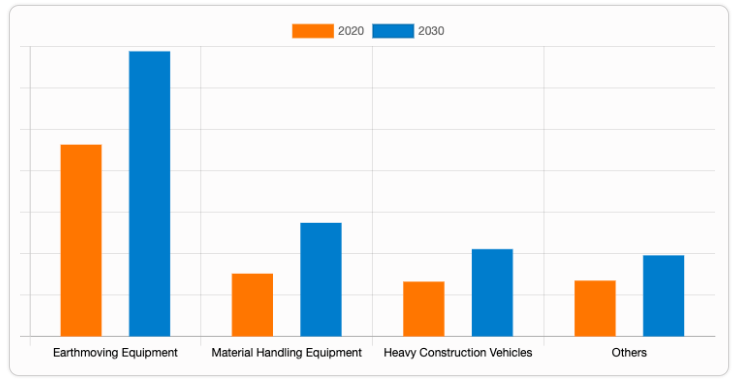

Research suggests that the global heavy construction equipment market, currently worth an astounding $176.2 billion in 2020, could experience explosive growth to reach $273.5 billion by 2030 at a compound annual growth rate of 4.4% between 2021 and 2030.

Sales can be linked to many different factors; among these is the expansion of commercial, residential, and industrial realms. Driven by rapid economic expansion and urbanization demands for large machinery is on an exponential increase - leading to infrastructure projects like highways, bridges, tunnels. Furthermore, governments have increasingly turned toward public-private partnerships to leverage private sector expertise while expanding resources further expanding this market further still.

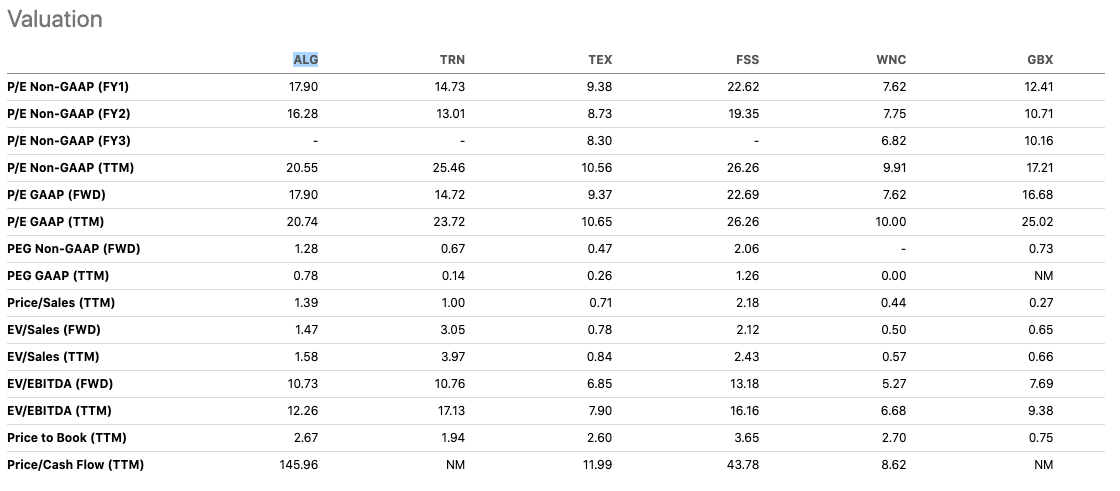

Next, moving along to valuation , Alamo Group appears to be fairly valued relative to its peers for several reasons, which include:

{kind=link}

To begin with, the forward Price-to-Earnings (P/E) ratio for ALG stands at 17.90, which, while elevated relative to peers such as TRN (14.73), TEX (9.38), WNC (7.62), and GBX (12.41), remains more moderate than FSS's 22.62. This positioning implies that ALG's valuation, though not exorbitant, is somewhat higher than several of its counterparts.

Moving on to the Price-to-Sales (P/S) ratio, ALG exhibits a figure of 1.39, surpassing the majority of its competitors save for FSS (2.18). This data suggests that the market ascribes a higher value to ALG's sales than those of most of its rivals, yet the company stops short of the lofty pricing seen with FSS.

Lastly, a glance at the Enterprise Value-to-EBITDA (EV/EBITDA) ratio reveals that ALG's forward metric of 10.73 occupies a middle ground among its peers. With a ratio higher than TRN (10.76), TEX (6.85), WNC (5.27), and GBX (7.69), but lower than FSS (13.18), ALG's valuation can be considered moderate in comparison to its competition.

{kind=link}

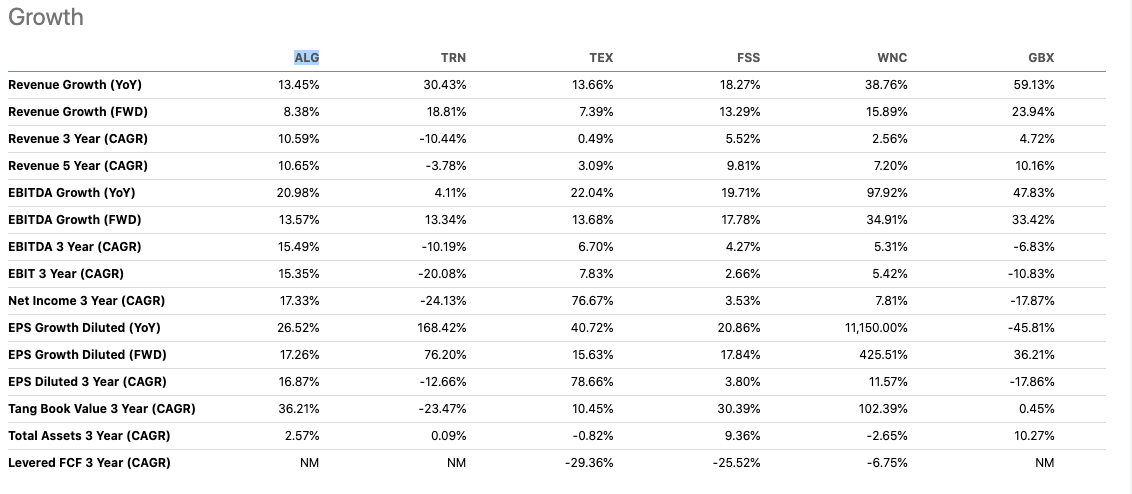

In assessing growth , it is noteworthy that ALG's performance remains steady, boasting a year-on-year revenue growth of 13.45%. This figure aligns with that of TEX at 13.66%, yet falls short when compared to the remarkable advances of TRN at 30.43%, FSS at 18.27%, WNC at 38.76%, and GBX at an astounding 59.13%. So it seems that the slower pace of growth exhibited by ALG in relation to its peers serves as a rationale for its comparatively modest valuation.

{kind=link}

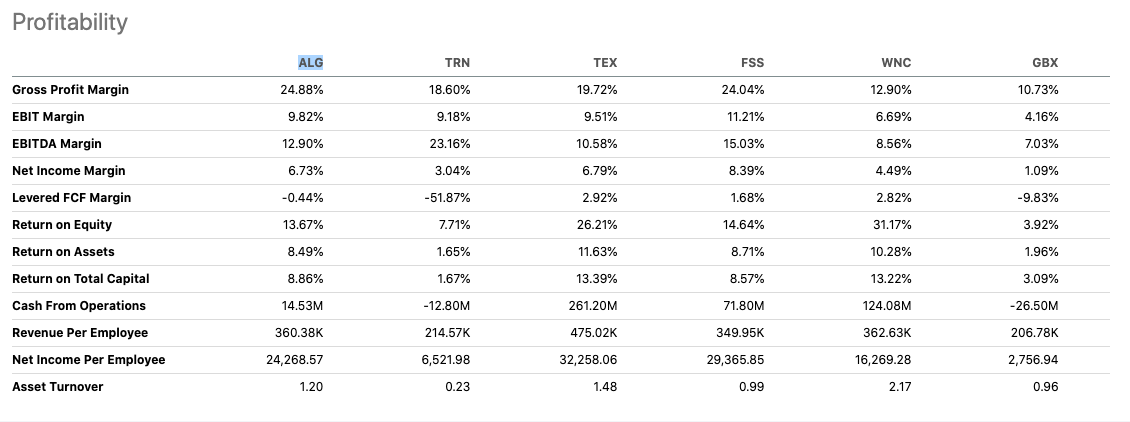

Once we turn our focus towards profitability , you'll discover that ALG's metrics such as gross profit margin, EBIT margin and net income margin fall comfortably within its industry peers' midranges when measured against them. Furthermore, its return on equity (ROE) and return on assets (ROA) also exhibit moderately with respect to competitors within its field compared with averages seen elsewhere. As such, Alamo Group Inc's valuation appears fair when measured against peers; I believe its current share price of $177.78 does not necessarily leans towards overvaluation nor undervaluation either extreme.

Risks and Headwinds

From my perspective, Alamo's survival in the 2023 revenue growth landscape largely depends on making calculated moves to address supply chain bottlenecks and workforce shortages. While its commendable efforts to overhaul manufacturing capabilities are notable, they might not be the panacea for ongoing labor scarcities. Although, streamlining work in progress and optimizing production facilities for efficiency may help Alamo curb its dependence on overtime.

Hidden behind the agriculture sector's remarkable robustness, danger patiently awaits. If supply chain disruptions continue, the Industrial division's influx of orders could be short-lived. Alamo should stay attuned to the foreboding undertones of inflationary trends that could erode business margins. The company's strategies to combat inflation-price increases and operational adjustments-may struggle in the face of unyielding inflationary forces, leaving profitability in disarray.

Rising Challenges for Alamo

Alamo's Q4 and full-year 2022 financial results showcase growth and profit, but concealed beneath are the aforementioned supply chain glitches, labor shortages, and impending inventory transportation expenses. So, it seems to me that decisive measures are necessary for the company to meet the demand for its products and overcome these challenges.

As I see it, Alamo's most pressing obstacle is fulfilling the growing appetite for its products (not such a bad problem though) while grappling with supply chain constraints and labor scarcities. A prudent approach to managing expenses and revenues, coupled with well-thought-out price modifications, could alleviate the impact of inflation. My assessment is that Alamo must also remain watchful for signs of economic downturn and proactively avert potential threats that could jeopardize future successes. Though the outlook for Alamo appears positive, from my viewpoint, prompt action is essential to traverse these perilous conditions, ensuring sustained revenue growth throughout 2023 and beyond.

Takeaway

Alamo Group provides investors with an attractive long-term opportunity. It offers moderate valuation relative to competition, strong year-on-year revenue growth rates of 13.45% and healthy profitability metrics such as gross profit margin, EBIT margin and net income margin as well as ROE/ROA figures. Though supply chain bottlenecks, labor shortages, inflationary forces are potential threats, the company appears to be taking steps toward mitigating them which makes Alamo an appealing long-term buy option for potential investors.

For further details see:

Alamo Group Provides Investors With An Attractive Long-Term Opportunity