AGI - Alamos Gold: A Robust Updated FS From Lynn Lake

2023-09-18 03:18:28 ET

Summary

- Alamos Gold released an updated Feasibility Study for its Lynn Lake Project, showing significant increases in gold reserves and the production profile (first 10 years).

- The upfront capital expenditure estimate for the project increased materially, but this isn't that far out of line with sector-wide inflation at other assets and incorporates scope changes.

- In this update, we'll look at the project's economics, how it stacks up vs. other undeveloped gold projects, and why there looks to be an upside to the NPV (5%)/production profile.

It's been a tough year for the precious metals sector, with many producers seeing costs come in above estimates, some seeing disruptions to operations (weather-related, wildfires, strikes/blockades) and continued worries about capex blowouts after three major projects in North America came in miles ahead of initial estimates. Worse, many producers have continued to dilute despite the gold price inching higher to a record 3-year average price of $1,840/oz, like Coeur Mining ( CDE ), Guanajuato Silver ( GSVRF ), First Majestic ( AG ), Endeavour Silver ( EXK ), Eldorado Gold ( EGO ) and Argonaut Gold ( ARNGF ). This has certainly not inspired much confidence, and while margins have improved on the back of higher gold prices, the tailwind from lower energy prices has ceased, an additional headwind for the sector when coupled with several producers continuing to call out sticky labor/contractor inflation.

Fortunately, there have been exceptions from an execution standpoint, and some companies like Alamos Gold ( AGI ) have continued to grow NAV per share, helped by continued exploration success, opportunistic share buybacks, and maintaining a healthy balance sheet to ensure they don't get caught with their backs against the wall and have to sell equity or assets. And while the company was already on a path to becoming one of the lowest cost producers sector-wide, that path has been reinforced with its updated Feasibility Study [FS] on Lynn Lake, an asset with robust economics that will push its percentage of production from Tier-1 jurisdictions above 80%. Let's take dig into the recent study below, why it is great news for the company and why Alamos continues to be a premier way to gain exposure to gold.

All figures are in United States Dollars unless otherwise noted.

Island Gold P3+ Construction - Company Website

{kind=link}

Lynn Lake Updated Feasibility Study

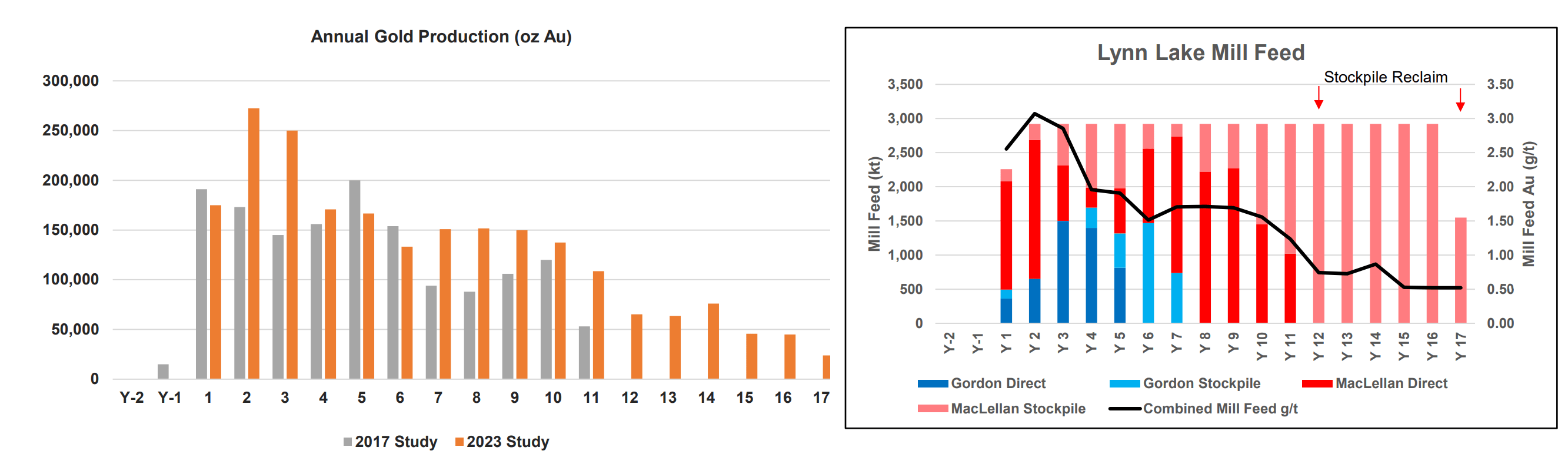

Alamos Gold ("Alamos") released an updated FS for its Lynn Lake Project in Manitoba last month, reporting a significant increase in total gold reserves, its expected first 10-year production profile, and its After-Tax NPV (5%). This was evidenced by its total reserve base growing to ~2.33 million ounces of gold (~47.6 million tonnes at 1.60 grams per tonne of gold vs. ~26.8 million tonnes at 1.89 grams per tonne of gold previously), and life of mine gold production increasing to ~2.19 million ounces of gold, a nearly 50% increase from 1.50 million ounces previously. Finally, from a scale standpoint, annual production in the first five years now sits at ~207,000 ounces (~170,000 ounces in first six years previously), while first-10 year production has soared to 176,000 ounces, up from 143,000 ounces previously. And while the nearly 6% decline in life of mine average annual output might disappoint some investors, it's important to note that there are opportunities to remedy this, with Lynn Lake reliant on primarily stockpiles following Year 9, as highlighted by the below chart.

Lynn Lake - Annual Production vs. 2017 Study & Mill Feed Profile - Company Website, 2023 TR

{kind=link}

Moving over to upfront costs, this is one area where we saw significant changes, which might also be a little disappointing to some investors given that not much has changed from a plan of operations standpoint from the 2017 FS. This is based on Alamos still looking at a two-pit open-pit project processing ~2.9 million tonnes per annum (~2.56 million tonnes per annum previously), with a CIP Plant and the project benefiting from low-cost grid power. That said, there were some minor changes, including a larger mobile fleet to aid in accessing high grade ore earlier, and a larger mill with the new plan envisioning 8,000 tonnes per day vs. 7,000 tonnes per day previously. As for the fleet, this will comprise larger hydraulic shovels at the MacLellan Pit, sixteen 140 tonne truck up from thirteen trucks previously, and a larger fleet of twelve 70 tonne trucks at the Gordon Pit to allow for more selective mining vs. the seven 144 tonne trucks in the 2017 Study.

Outside of the more significant changes, the fine ore storage area will now comprise steel bins with apron feeders vs. a covered stockpile and the plant layout was optimized to boost overall recoveries with two extra tanks added to the leach circuit.

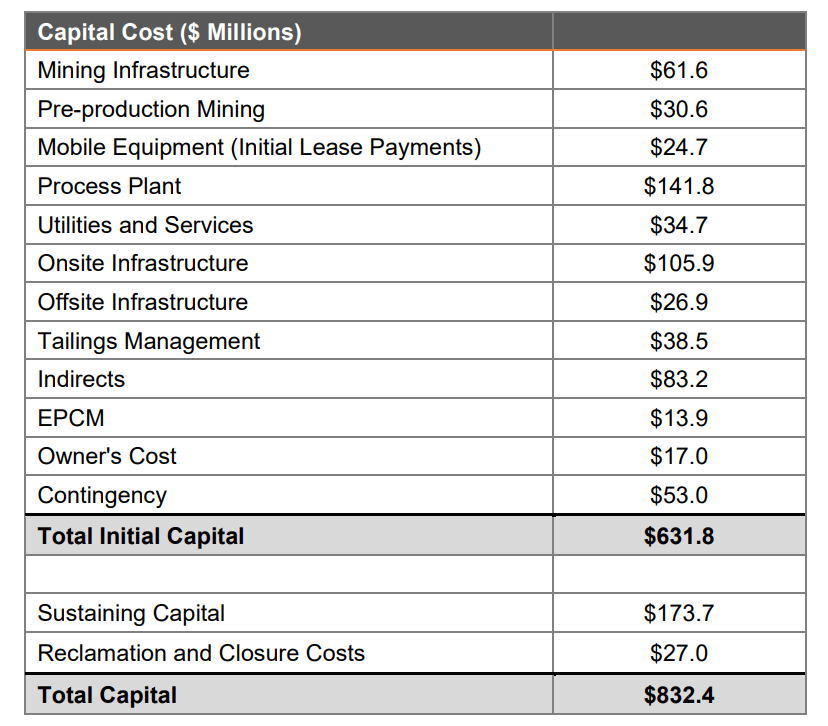

That said, while the upfront capex estimate of ~$630 million (2017: ~$340 million) is up significantly, this isn't that far out of line with what we've seen from other projects with over 60% inflation in undeveloped projects since 2019 and some projects going over 80% above budget relative to 2019/2020 estimates (Magino, Cote, Rochester POA 11). Plus, Alamos' basic engineering is at 100% completion while detailed engineering is at 55% completion with Q4 2022 cost estimates, suggesting a relatively high level of confidence in the capex estimates provided in the more current study. And while costs came in slightly above my estimates (ex-scope changes) of $550 million, the gold price has more than made up for the higher costs. Plus, as we'll detail below, operating costs beat my estimates and remain well below the sector average even if we assume ~7% inflation ($870/oz vs. ~$814/oz life-of-mine all-in sustaining cost estimates).

Lynn Lake - Initial Capex Estimates & Sustaining Capital - Company Website

{kind=link}

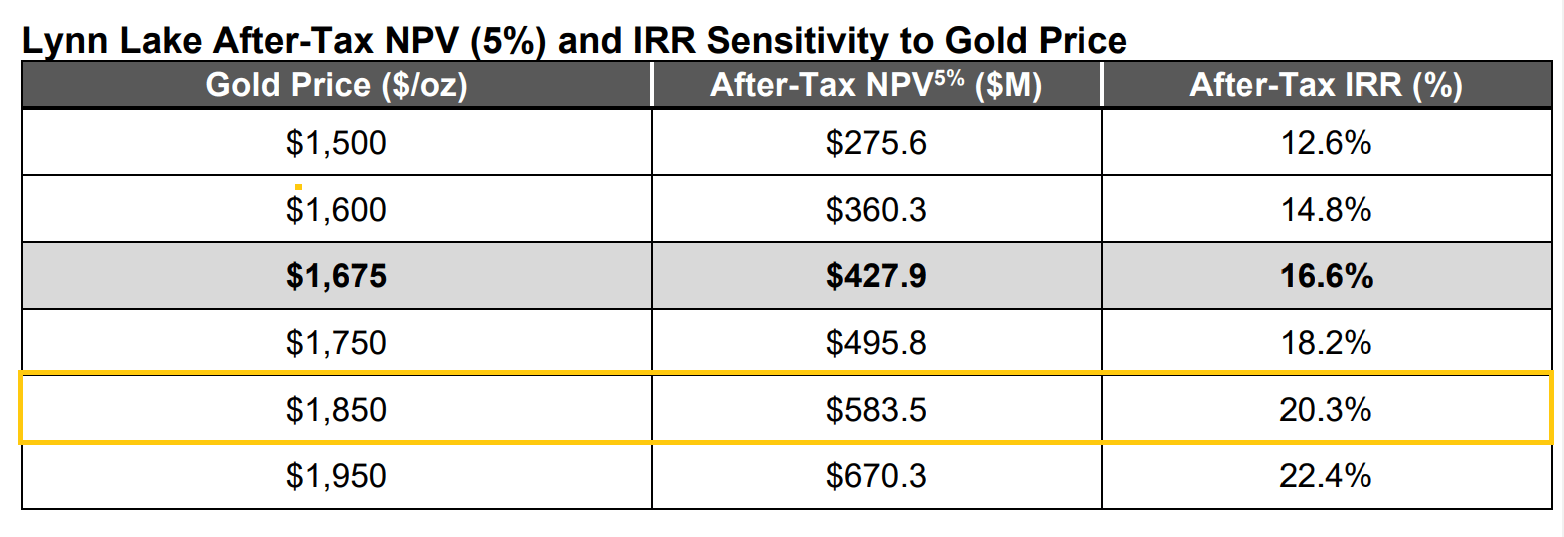

Looking at the below table below, we can see how Lynn Lake looks at different gold price sensitivities, and while upfront capex did increase ~86% from the 2017 Study, the After-Tax NPV (5%) nearly quadrupled to ~$428 million at $1,675/oz gold vs. the previous base case of $123 million at $1,250/oz gold. And using what I would argue to be a conservative price of $1,850/oz gold for a project that is likely to operate from 2028 to 2044, Lynn Lake's After-Tax NPV (5%) comes in at ~$584 million, translating to a 20.3% IRR, well above the 15% hurdle for most producers. Finally, Lynn Lake will have some of the lowest AISC sector-wide in its first 10 years at ~$700/oz if cost estimates are correct, well below industry average estimates for the entire gold producer universe (30,000+ ounce producers) of $1,380/oz in FY2024. And the mine will benefit from no royalties after its third year, with the $10 million cap expected to be extinguished by Year 4.

Lynn Lake - After Tax NPV (5%) and IRR - Sensitivity Table - Company Website

{kind=link}

So, how does the project stack up vs. other precious metals projects in the development stage?

Lynn Lake Vs. Other Undeveloped Precious Metals Projects

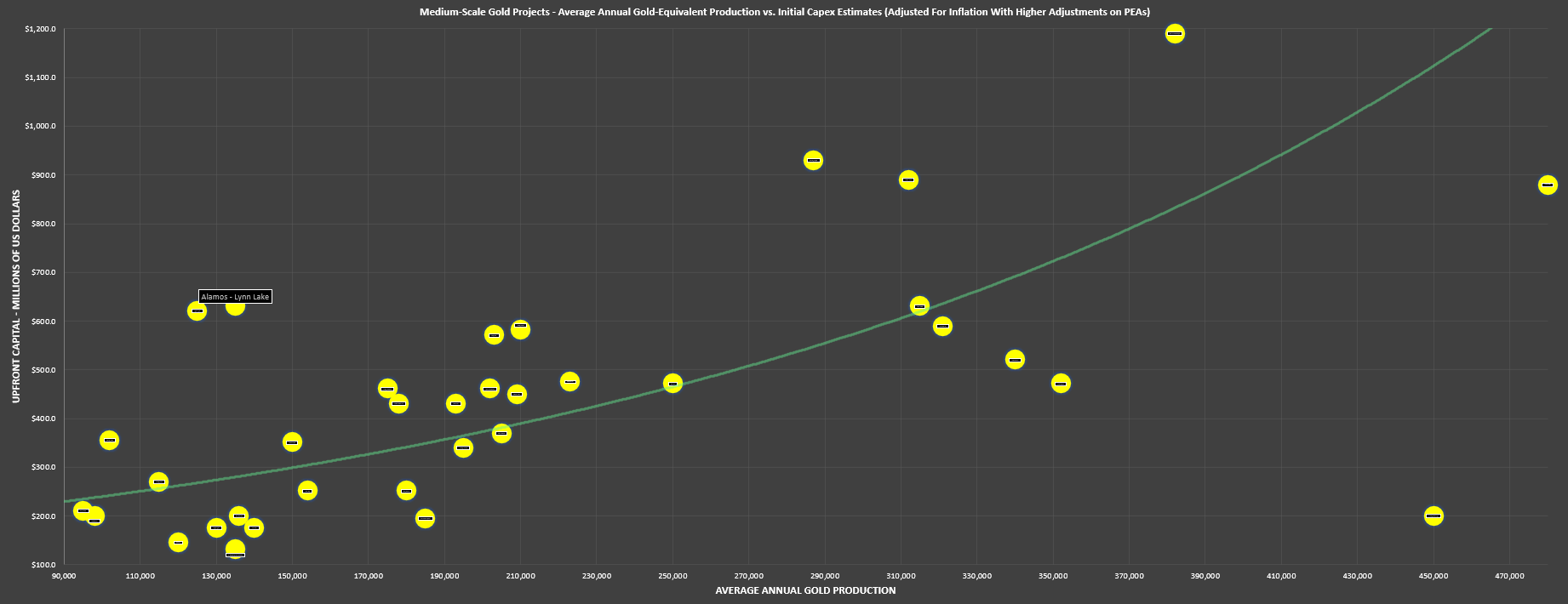

Looking at the charts below, we can see a sample of 35+ undeveloped projects or those completed this year from an average gold-equivalent production (life-of-mine) and upfront capex estimate standpoint (adjusted for inflation where necessary because of stale cost estimates and PEAs). At first glance, Lynn Lake may appear less robust than some other projects, with projects in the upper left quadrant being the least attractive on an average production vs. initial capex ratio. However, it's important to note that it's being measured against over twelve incredible projects that are of world class caliber by any standards. Second, the production profile looks far worse on a life-of-mine basis because of the average grade of ~0.74 grams per tonne of gold from Year 11 through 17 (reliance on processing stockpiles) with this being more pronounced than some other projects.

Medium & Large Scale Gold Projects - Average Annual GEO Production vs. Initial Capex Estimates (Adjusted For Inflation Where Appropriate) - Company Filings, Author's Chart & Estimates

{kind=link}

However, if we adjust for this and focus on the first 12 years, Lynn Lake comes in near other projects in the ~170,000 to ~200,000 ounce range with $500+ million in upfront capex estimates like Fenelon, Kone, and Magino (assuming higher throughput rates at Magino). Second, it's possible I haven't been conservative enough on other studies, and Lynn Lake is in the unfavorable position of having the most conservative (current) study of its peer group, capturing all the inflationary pressures from 2020 to year-end 2022. Third, while some might argue that adjusting because of reliance on low-grade stockpiles post Year 10 is biased, I would argue that the current mine life is quite conservative and could look considerably better given the exploration upside at other targets and continued exploration success at the higher-grade Gordon Pit. In fact, Alamos has extended mineralization in the northeastern portion of the proposed Gordon Pit (an area previously defined as waste), suggesting an upside to Gordon mined ounces.

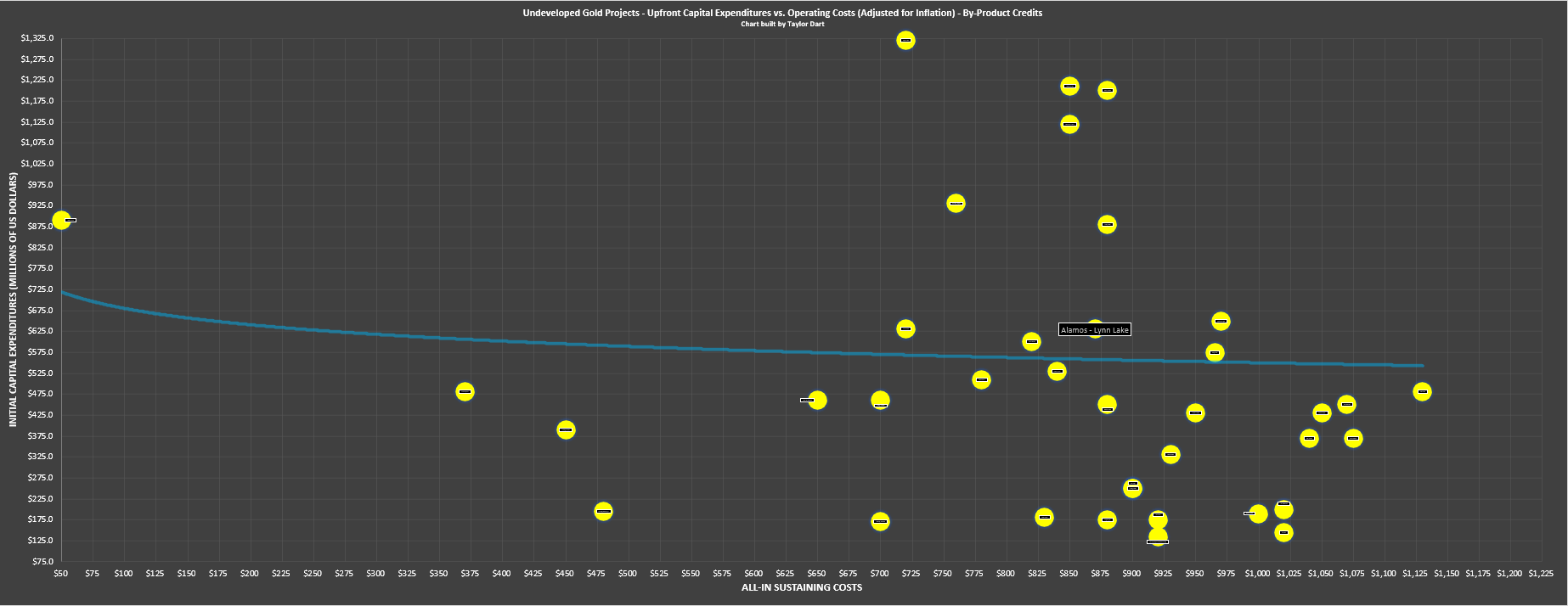

Undeveloped Gold Projects - Upfront Capex vs. AISC (Adjusted for Inflation) - Company Filings, Author's Chart & Estimates

{kind=link}

If we look at the Lynn Lake Project from another angle (upfront capex vs. estimated AISC), we can see a different story, with Alamos' costs only marginally above the trend line to define the average undeveloped or recently completed project (Seguela, Magino, Abujar). Meanwhile, although capex is high, its upfront capex and cost profile are actually quite similar to Windfall, a project where Gold Fields ( GFI ) recently scooped up a 50% stake. Lynn Lake also stacks up quite well relative to Back River which was just acquired, with upfront capex at Back River similar (~$6000 million vs. ~$630 million), and Lynn Lake's AISC potentially lower, benefiting from low-cost grid power and being less remote in northern Manitoba vs. Nunavut). So, with Lynn Lake owning 100% of this project and there being room to optimize this asset, I see this as a very attractive project, especially on a first 10-year basis with AISC expected to be over 48% below the current industry average (~$700/oz vs. ~$1,360/oz).

Plus, as pointed out in the last chart, it's possible my estimates aren't conservative enough for other projects, and Lynn Lake once again suffers from being the most current project with the highest inflation baked in vs. dated studies.

Project Upside & Bigger Picture

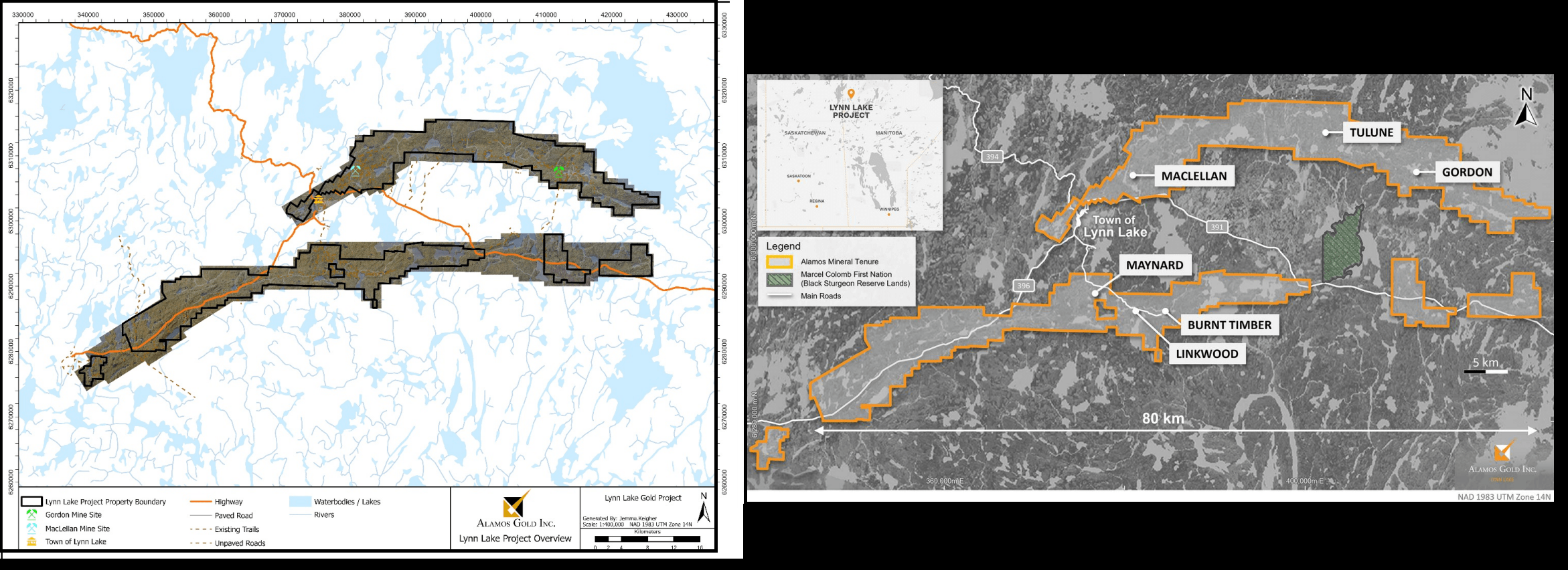

As noted previously, Lynn Lake is already an impressive project (~$670 million NPV (5%) at $1,950/oz with 200,000+ ounces of annual production in its first five years), but there is room for improvement. For starters, and for those unfamiliar, the project spans most of a massive 125 kilometer long greenstone belt and the company's land package is actually larger than Back River (~58,000 hectares vs. ~54,000 hectares), suggesting there's a lot more ounces to come if the company can make new satellite discoveries or potentially find a new mine on its land package. But, given that the company has been having the exploration success it has at its other three mines, aggressive exploration at Lynn Lake has not been a priority to date with Alamos operating a relatively lean model during periods of major growth capex and it has been a busy several years (YD Lower Mine Expansion, La Yaqui Grande construction, P3+ Construction currently) and directing exploration dollars to its flagship mine, Island Gold.

Lynn Lake Property Boundary & Infrastructure - Company Website

{kind=link}

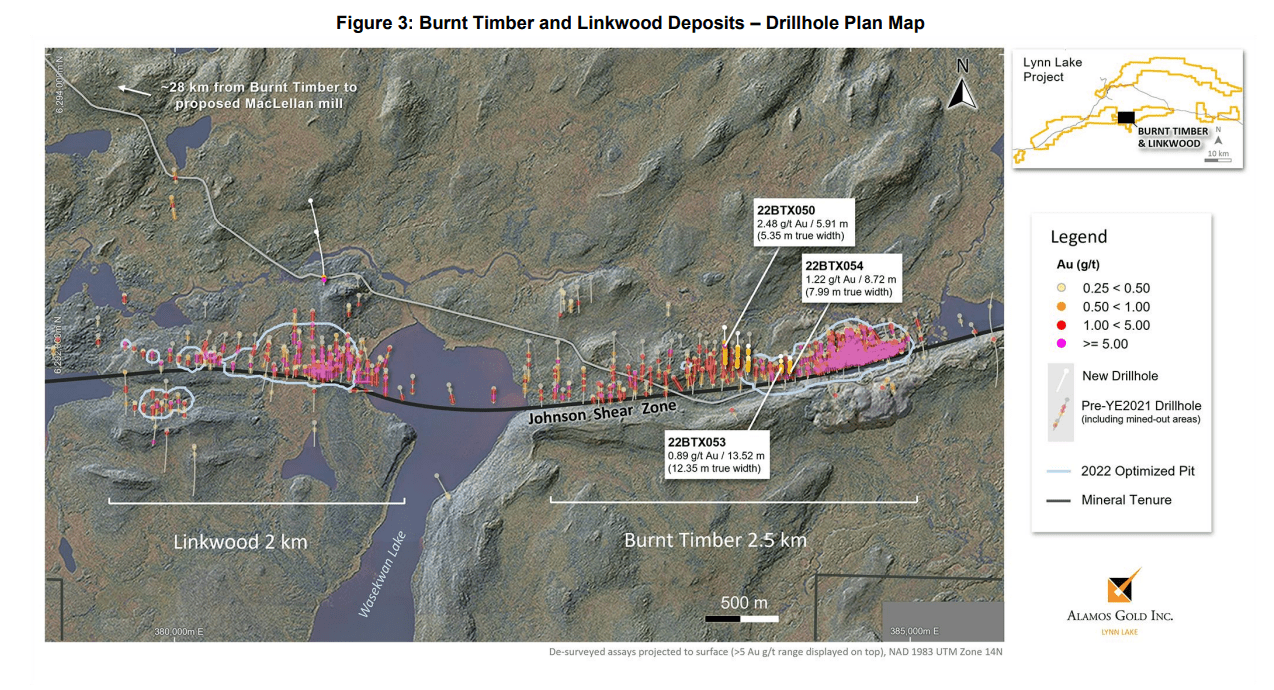

However, the company has ~1.6 million ounces in the inferred category at the Burnt Timber and Linkwood deposits, with these deposits less than 30 kilometers from the planned mill next to MacLellan. And while grades here are not as attractive as life of mine grades (~1.1 grams per tonne of gold vs. ~1.5 grams per tonne of gold), they are substantially better than the grades that the company will be processing from Year 11 to 17 (~0.74 grams per tonne of gold average). And even if we assume conservative haulage costs of ~$4.80/tonne (Gordon's estimated haulage costs of ~$7.10/tonne over 1.8x the distance), this translates to losing 0.08 grams per tonne of gold, making these ounces more attractive than stockpile ounces, which could displace these lower grade ounces and lift feed grades in the back half of the mine life, especially if the mine plan pursues a slightly higher-grade pit (~1.2 grams per tonne of gold) at Linkwood/Burnt Timber.

Burnt Timber & Linkwood Deposits - Company Website

{kind=link}

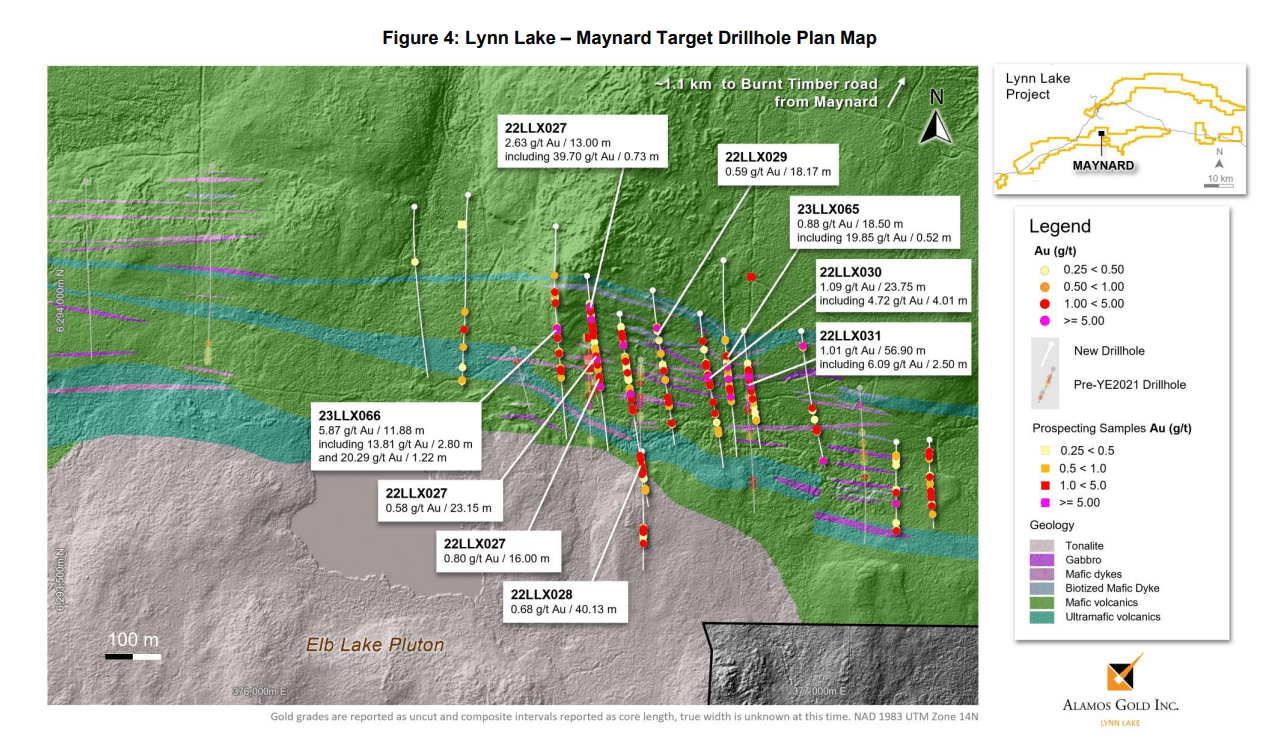

Secondly, and in addition to Linkwood/Burnt Timber, Alamos has new regional targets that it's tested in Maynard and Tulune, with Maynard being closer than Burnt Timber/Linkwood, and ~20 kilometers southwest of the proposed MacLellan Mill. Highlight intercepts from Maynard include 11.9 meters at 5.87 grams per tonne of gold, 13 meters at 2.63 grams per tonne of gold, 23.8 meters at 1.09 grams per tonne of gold, and a thick intercept of 56.9 meters at 1.01 grams per tonne of gold. Hence this could represent an even more attractive opportunity if it can grow and has similar grades to Burnt Timber/Linkwood given the slightly lower haulage costs. Elsewhere, albeit further than Maynard, Tulune is a second iron in the fire, sitting between the planned Gordon and MacLellan pits. A highlight intercept here hit 16.1 meters at 1.08 grams per tonne of gold, and given the sunk costs if Lynn Lake is developed, anything above 1.0 gram per tonne of gold with smaller satellite pits would be gravy to augment the dip in grades post Year 10. Finally, Gordon continues to deliver on grades and I wouldn't be shocked to see ounces added here as well to push stockpiles out further in the mine life, ultimately boosting NPV (5%) and helping to maintain a ~175,000 ounce production profile for the first 15 years vs. 10 currently.

Maynard Target Drill Results - Company Website

{kind=link}

So, what's the plan for development?

Alamos - Expected Production Profile with Island Expansion & Lynn Lake + Declining Cost Profile - Company Presentation

{kind=link}

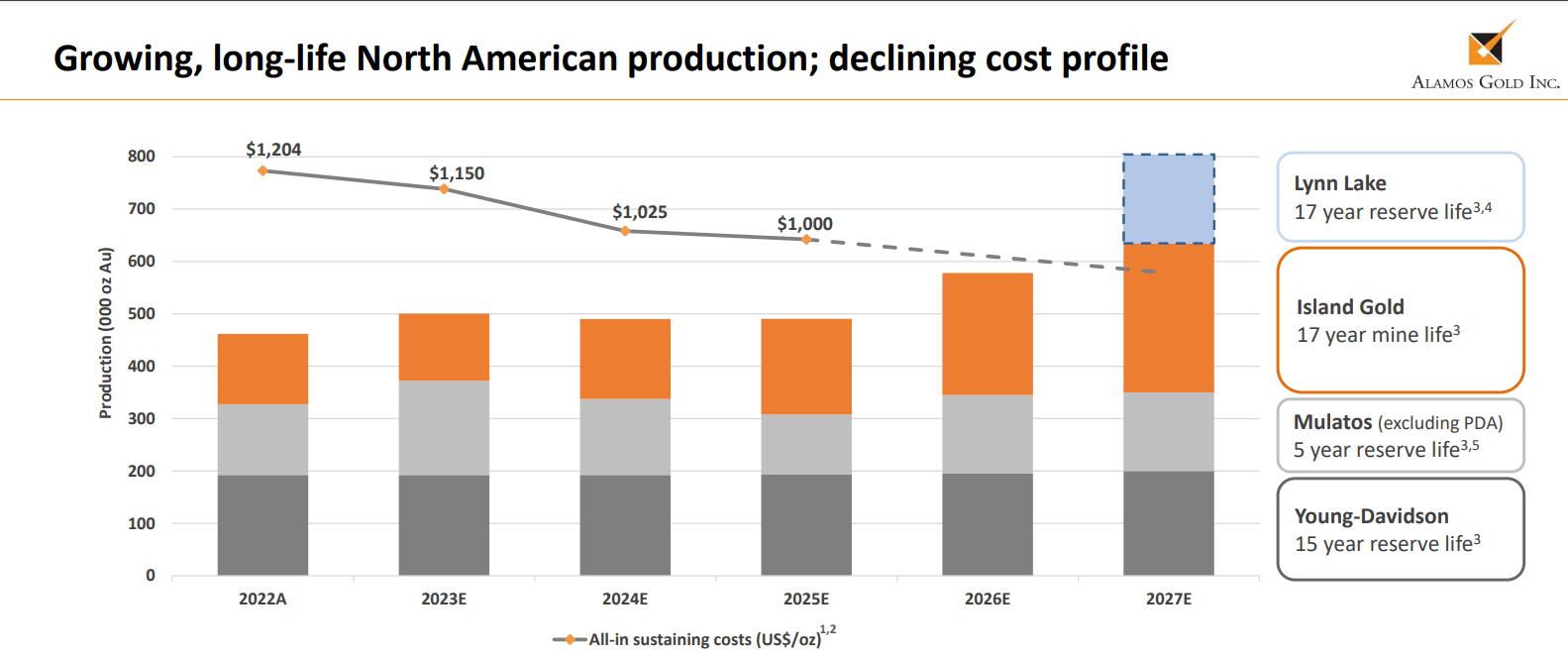

As noted by Alamos, the company does not expect to begin making any significant investment in Lynn Lake until its P3+ Project at Island is nearing the finish line, but with nearly $200 million in net cash, significant liquidity and well over $220 million in annual free cash flow post-2026, the company should have no issue funding this while maintaining its pristine balance sheet. And given that the company has signaled it doesn't expect to start major construction until major capex at P3+ has been spent, I think a Q3 2028 first gold pour is a conservative estimate (assuming it's green-lighted), which would catapult Alamos' production profile to 800,000+ ounces in 2029 at sub $900/oz costs assuming continued mine life extensions at Mulatos. Just as importantly, Lynn Lake would be margin accretive and boost its Tier-1 production if approved, potentially leading to further multiple expansion for the company.

Summary

Alamos Gold' Lynn Lake Feasibility Study exceeded my expectations regarding its expected operating cost profile with expected life-of-mine AISC below $875/oz (7% vs. study) even adjusting for continued inflationary pressures. And while initial capex increased materially, this is not surprising when few 150,000+ ounce gold projects can still be realistically built for less than $450 million (excluding lower-cost heap-leach projects or smaller projects) following three years of near unprecedented inflation. Hence, the ~$630 million estimate is not that out of line with other undeveloped projects, it's relatively modest capex for a company that will generate over $220 million in annual free cash flow post-2025. Plus, the expected margins at Lynn Lake are exceptional (~$1,200/oz first ten years at $1,925/oz gold), fitting Alamos' profile of being a mini Agnico Eagle ( AEM ), focused on top-tier jurisdictions, profitable ounces vs. absolute ounce figures, and disciplined organic growth without taking on significant leverage like some of its peers.

So, with Lynn Lake fitting this profile, investors can be comforted that Alamos does not need to pursue acquisitions to grow, with significant organic growth opportunities in its portfolio between PDA and potentially Capulin (Mulatos), Island P3+ and Lynn Lake. This is a positive development given that we often see a hangover post M&A for producers, with several examples over the past few years of suitors over-paying for assets to secure future growth, leading to significant underperformance and dragging down the overall index. Just as importantly, Alamos owns some of the longest-life assets sector-wide, and this combination of industry-leading margins, primarily Tier-1 jurisdictions and strong visibility into future production should help the stock maintain its premium multiple vs. its peer group. To summarize, I continue to see Alamos Gold as a top-5 producer sector-wide from a quality standpoint, and I would view sharp pullbacks as buying opportunities.

For further details see:

Alamos Gold: A Robust Updated FS From Lynn Lake