AGI:CC - Alamos Gold: A Solid Start To The Year

2023-04-28 01:27:24 ET

Summary

- Alamos Gold continues to be one of the best-performing stocks sector-wide, up ~100% from its Q3 2022 lows and 30% year-to-date.

- Its outperformance can be attributed to Alamos being one of the few miners to meet cost guidance and not report cost blowouts at growth projects, combined with continued capital discipline.

- As for the Q1 results, AGI continues to fire on all cylinders, tracking at 26% of annual guidance with improving costs helped by higher-grade La Yaqui Grande ore.

- Given Alamos' continued track record of growing reserves, production growth per share, and consistently increasing shareholder value, I would view any sharp pullbacks in the stock as buying opportunities.

The Q1 Earnings Season for the Gold Miners Index ( GDX ) has finally begun and one of the first companies to report its results is Alamos Gold ( AGI ). Unlike some of its peers that reported rising operating costs, Alamos came out of the gate strong from an output and margin standpoint, producing ~128,400 ounces of gold at cash costs of $821/oz. This was a material improvement from the year-ago period, though it helped to up against easy year-over-year comps, and this translated to record revenue, positive free cash flow despite increased spending on the Island P3+ Expansion and helped Alamos exit Q1 with one of the strongest balance sheets sector-wide. Let's take a look below:

Q1 Production & Sales

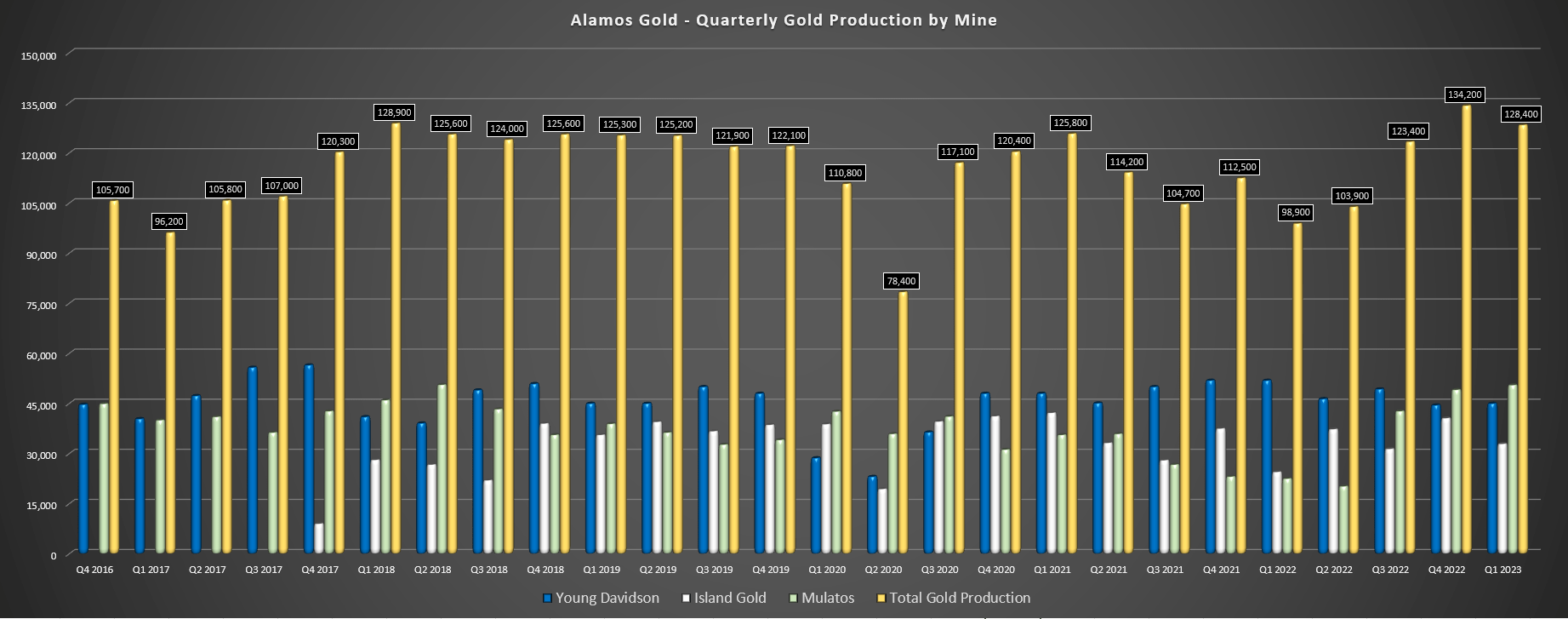

Alamos Gold released its Q1 results this week, reporting quarterly production of ~128,400 ounces of gold, a 30% increase from the year-ago period. The significant increase in costs was partially due to being up against easy year-over-year comps with lower grades in Q1 2022 at Island (~8.1 grams per tonne of gold) and the fact that Mulatos barely contributed in the period as the company worked to put its new La Yaqui Grande Mine (part of the Mulatos District) into production. The company is now realizing the fruits of this labor, with La Yaqui Grande producing ~38,400 ounces in the period, pushing Mulatos District production to ~50,500 ounces with this being Alamos' largest contributor in the quarter.

Alamos Gold - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

As shown in the chart below, this was Alamos' third best quarter to date from a production standpoint and production came up just shy of the previous Q1 record (Q1 2018: ~128,900 ounces) when the company had four mines in operation (El Chanate moved into reclamation in 2019) and Alamos was benefiting from higher grades (11.1 grams per tonne of gold). Hence, the near-record performance despite working with three mines is quite impressive. As noted above, the primary contributor to the increased production was La Yaqui Grande, where Alamos stacked ~1.02 million tonnes and saw an average processed grade of 1.55 grams per tonne of gold, nearly 70% higher than the average processed grade of 0.92 grams per tonne of gold at Mulatos.

Moving over to Canada, where the company generates the bulk of its revenue, Alamos' two assets combined for ~77,900 ounces, with Island's production up year-over-year on the back of higher grades and increased throughput (~107,500 tonnes processed vs. ~100,600 tonnes in Q1 2022). Meanwhile, at Young-Davidson, production declined year-over-year to ~45,000 ounces, but the company was lapping tough comps with production of ~51,900 ounces in the year-ago period. The near-record performance in Q1 2022 was due to higher grades and throughput (~737,700 tonnes processed at 2.38 grams per tonne of gold), but grades should improve in H2 and the mine will finish the year much stronger.

{kind=link}

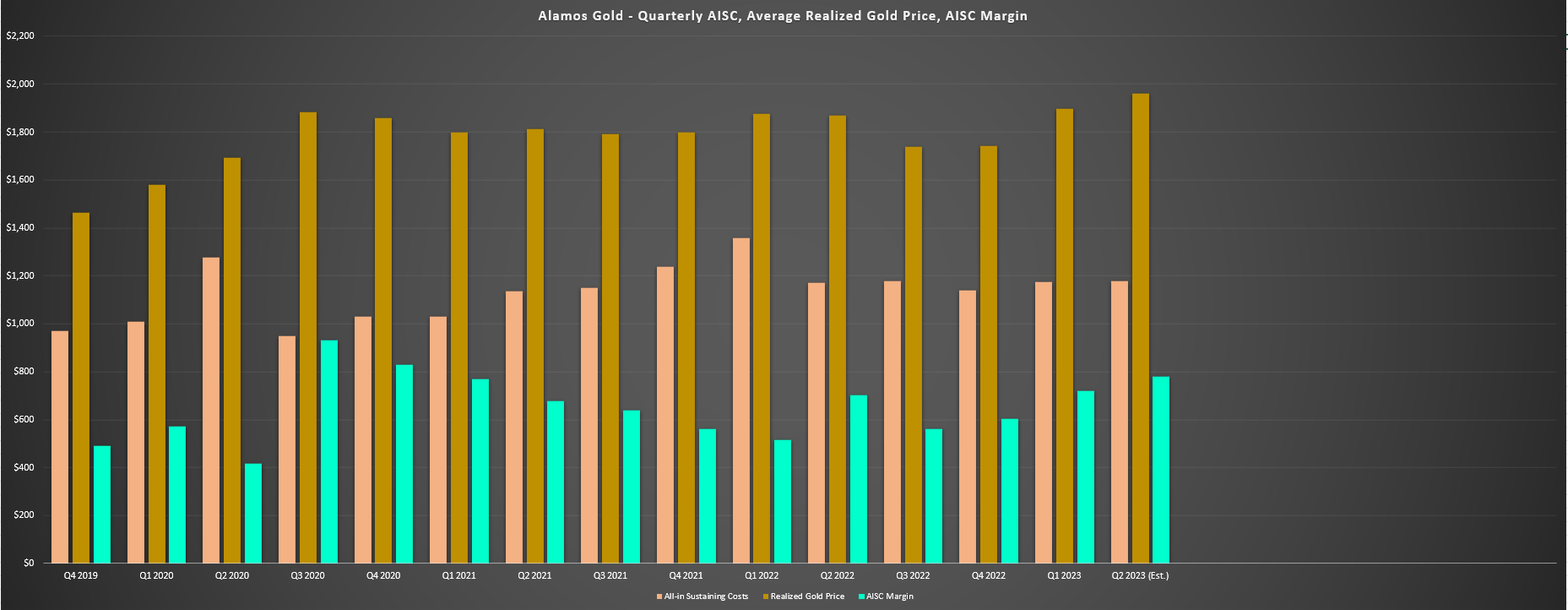

Finally, from a cost standpoint, Alamos reported cash costs of $821/oz (down 17% year-over-year) and all-in sustaining costs of $1,176/oz, which were down 14% vs. Q1 2022 levels. The significant improvement in costs was related to much lower operating costs at its Mulatos District operations as it benefited from higher-grade ore and increased sales volumes from La Yaqui Grande, plus lower costs at Island with a more normal quarter from a production standpoint. Notably, the lower all-in sustaining costs across the board was despite 19% higher sustaining capital in the period, a minor headwind, with some help from a weaker Canadian Dollar.

Financial Results

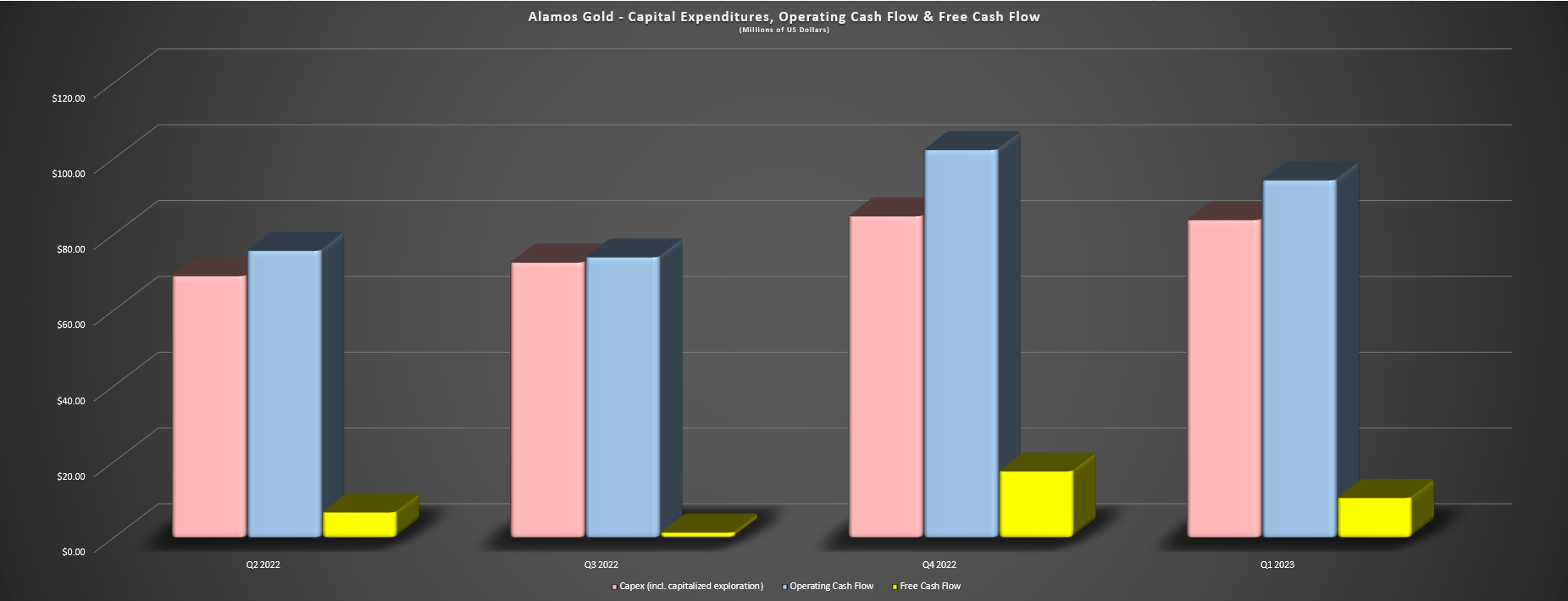

As for Alamos' financial results, the company reported record revenue of $251.5 million (+36% year-over-year), driven by higher sales volumes and a higher average realized gold price of $1,896/oz. Meanwhile, operating cash flow improved to $94.3 million (+103% year-over-year), helped by significant margin improvement and the higher gold sales in the period. The result was that Alamos generated positive free cash flow of $10.5 million despite relatively high capex with Island Gold P3+ construction ramping up (Q1: ~$43.2 million in growth capital spent at Island alone), and Alamos finished the quarter with ~$134.0 million in cash and no debt.

Alamos - AISC, Gold Price, AISC Margins (Company Filings, Author's Chart) Alamos Gold - Operating Cash Flow, Capital Expenditures, Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Looking at the margin performance, Alamos saw its AISC margins improve to $720/oz (Q1 2022: $517/oz), helped by a higher average realized gold price and lower costs because of the start of production at La Yaqui Grande, increased production at Island, and a weaker Canadian Dollar. And looking ahead to Q2 2023, we could see AISC margins improve further to ~$770/oz, assuming a similar AISC of $1,190/oz and an average realized gold price of $1,960/oz (quarter-to-date gold price of $1,940/oz). Finally, from a capital expenditures standpoint, Alamos is tracking right in line with planned spending of ~$337 million this year with ~$83.8 million spent in Q1.

{kind=link}

Lastly, while Alamos will incur significantly higher capital spending from 2023 through 2025 (total growth capital of $750 million for P3+ Expansion) as it works to more than double Island's production, the higher gold price and the shift from an investment period (YD Lower Mine Expansion) to a period of strong cash flow generation plus higher grades at La Yaqui Grande is allowing it to execute this growth while maintaining a strong balance sheet and without share dilution. This is a rarity in the sector among sub 500,000-ounce producers and even some million-ounce producers, with growth often being accompanied by material share dilution like Argonaut ( ARNGF ) and First Majestic ( AG ) or a stressed balance sheet like Kinross ( KGC ) and Evolution Mining ( CAHPF ).

To summarize, investors don't have to worry about any share dilution or balance sheet stress as Alamos works on its next phase of growth and the company could generate upwards of $140 million in free cash flow this year despite the significant increase in growth capital if gold prices continue to cooperate.

Recent Developments

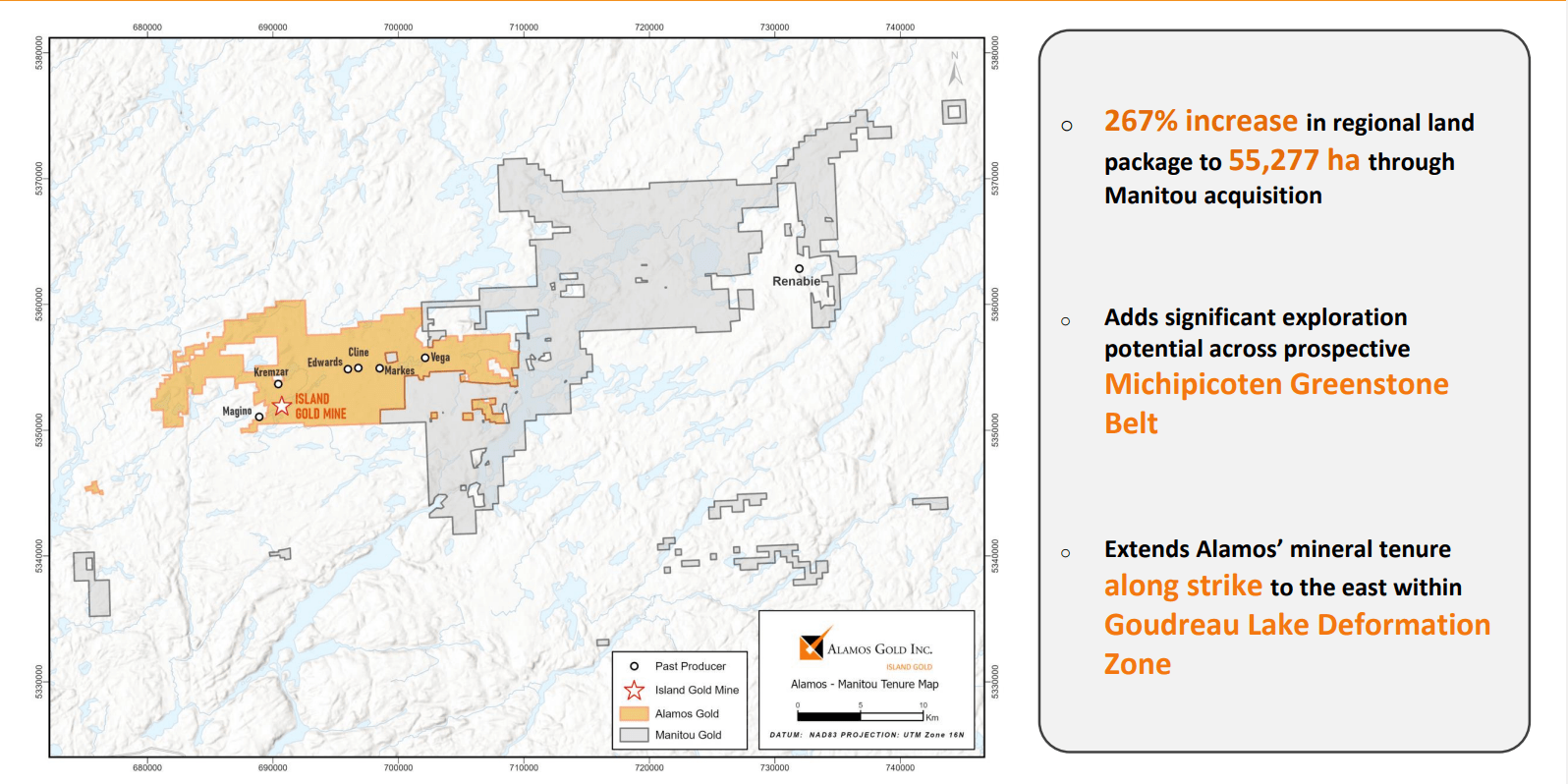

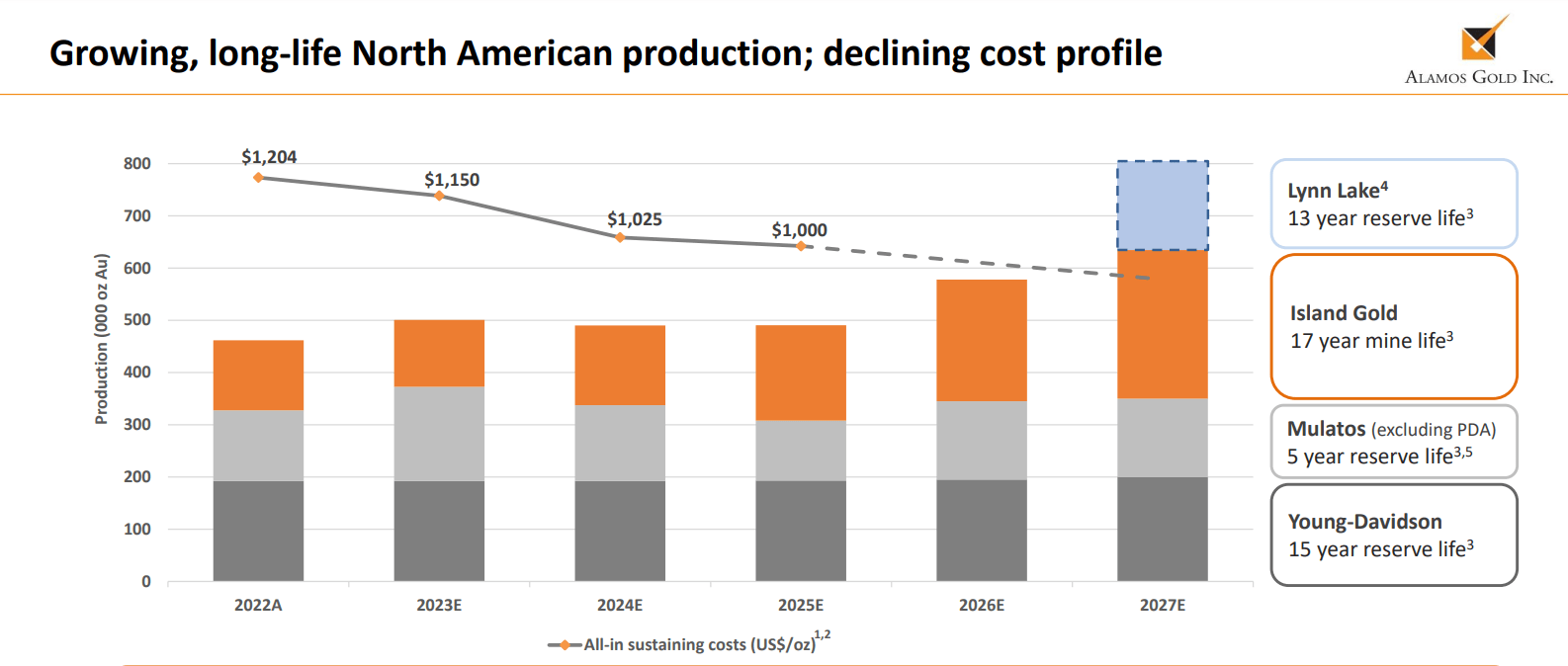

As for recent developments, Alamos noted that shaft sinking will begin later this year for its Island P3+ Expansion and that the construction of the hoist house is underway. Once the project is complete in 2026, annual production will increase to nearly 300,000 ounces per annum at industry-leading AISC of sub $650/oz, making this one of the most profitable mines in North America. In addition, Alamos announced the acquisition of Manitou Gold for a very reasonable valuation of ~$13 million. This will significantly increase Alamos' regional position to 55,000+ hectares, similar to SSR Mining's ( SSRM ) move last year to bolster its land position in Saskatchewan with the Taiga Gold acquisition, which was also welcomed by the market given that it added considerable potential future value at minimal cost to shareholders.

Alamos Gold - Manitou / Island Gold Landholdings (Company Presentation)

{kind=link}

Elsewhere, at its Mulatos District in Mexico, Alamos expects to spend over $20 million in exploration to continue to advance Puerto Del Aire [PDA], a high-grade underground opportunity at the asset which lies adjacent to the Mulatos Pit and can be processed through the Mulatos Mill. The current reserve at PDA sits at 4.7 million tonnes at 4.8 grams per tonne of gold (~730,000 ounces), and Alamos expects to release a development plan by year-end for PDA, with investors able to get a better idea of whether this will fit into medium production. As it stands, this project is not included in Alamos' 2025 guidance, suggesting upside to FY2025 guidance of ~490,000 ounces at $1,000/oz which would already give Alamos one of the most impressive production/cost profiles sector-wide.

Finally, Alamos received good news from its Lynn Lake Project in Manitoba with a positive Decision Statement issued by the Minister of Environment and Climate Change Canada and Environment Act licenses from the Province of Manitoba for the Maclellan and Gordon sites, with this expected to be a medium-grade open-pit project that will employ over 400 people if put into production. Assuming Alamos goes ahead with the project, and assuming it can extend its mine life at Mulatos which is certainly looking likely given the material ounce growth at PDA, this has paved a path for Alamos to become an ~800,000-ounce producer later this decade with some of the sector's longest mine lives in the safest jurisdictions (over 80% of production from Canada if Lynn Lake brought online).

{kind=link}

For now, the Lynn Lake numbers are quite stale (Q4 2017 report), but this still should be a very robust project with sub $1,080/oz AISC, roughly 20% below the industry average (~$1,310/oz), with an updated study expected later this year.

Technical Picture

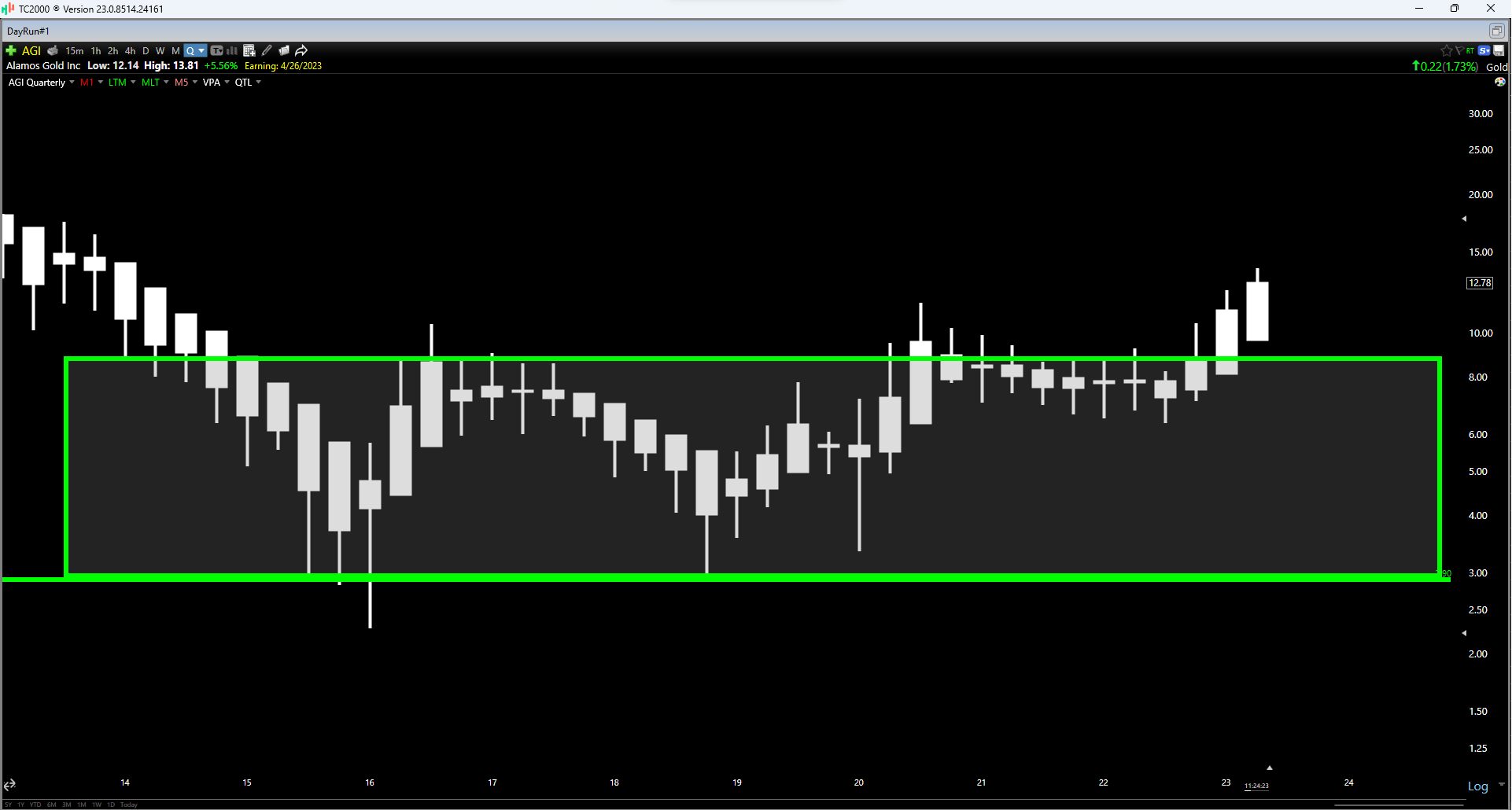

As for the technical picture, Alamos Gold continues to have one of the more constructive long-term setups in the gold space, breaking out of a multi-year base last year and continuing to see follow-through to this breakout. This is a very positive development, with this breakout ultimately targeting a move to the US$14.60 level in the future if it meets its target. Obviously, there's no guarantee that the stock gets there in a straight line, and we often see healthy pullbacks along the way. However, with Alamos being one of the few producers with a combination of strong growth, significant margin expansion, and being a name investors can trust due to strict capital discipline and ~80% of future production from attractive jurisdictions, I see it as one of the highest-quality names from an investment standpoint sector-wide.

{kind=link}

Summary

Alamos Gold continues to be one of the best-performing names in the precious metals sector, a distinction that it well deserved for its continued capital discipline, improving margin profile, ownership of what will be one of the highest-margin assets in North America post-2025. When combined with a track record of delivering on promises to investors, I continue to see Alamos Gold as a top-5 name from a quality standpoint sector-wide, and one of the best ways for investors looking for leverage to metals prices. That said, the stock's outperformance has been significant with a ~100% rally off its lows. So, if I were looking to add exposure to the stock, I see the best course of action being to take advantage of sharp pullback vs. chasing rallies.

For further details see:

Alamos Gold: A Solid Start To The Year