AGI - Alamos Gold: After An 80% Run I'm Downgrading To A Neutral Rating

2023-05-09 17:06:06 ET

Summary

- One of my top gold mining stock picks at this time last year was AGI, and there were many reasons why.

- The Alamos story has played out as anticipated and shares of AGI have responded, as over the last 12 months, the stock has posted a total return of 84%.

- It's difficult to justify the risk/reward with AGI when so many other gold miners are at such steep discounts, and I don't believe the stock will continue to outperform.

- There are other aspects we need to take into account when analyzing Alamos's valuation.

A year ago, I released an article on Alamos Gold ( AGI ) that discussed that while physical gold was a great asset to own at the time, mining stocks represented an even better way to survive and thrive in the high-inflation environment.

One of my top gold mining stock picks was AGI, and I listed the following six reasons why:

1) Growth + Leverage To Rising Gold Prices

Gold stocks typically offer 2-3x leverage to rising gold prices, on average, and that leverage is amplified if a company is growing production rapidly.

For Alamos, output was increasing after many years of stagnation, as it expected production to increase from 440,000-480,000 ounces of gold in 2022 to 460,000-500,000 ounces in 2023 and then climb to just below 600,000 ounces in 2025 when the Island Gold expansion was complete.

There was also ~75,000 ounces per year of additional upside potential for the Island Gold mine plan, development opportunities at Mulatos that could increase production even more, and the Lynn Lake project in Canada represented another step-change in production if Alamos developed the asset.

2) Better Insulated From Inflation

The multi-year AISC guidance from Alamos was also a major advantage, as it was able to control costs - which is critical in this environment - thanks to its high-grade, high-margin growth.

All-in sustaining cost (or AISC) was expected to trend lower by ~$100 per ounce in both 2023 and 2024 as higher-grade ore at Mulatos came online, and then AISC would plummet to just $800 per ounce in 2025 as the expansion at the high-grade Island Gold mine would increase annual production at the operation to over 200,000 ounces of gold. AGI would be able to offset inflationary pressures and, at worst, maintain margins. Most of its peers didn't have this advantage.

The company had also hedged the majority of its Canadian dollar and diesel exposure at rates that were 45% below spot prices at the time and was less exposed to rising input costs - as Island Gold and Young Davidson are underground mines and connected to grid power.

3) A Balance Sheet Built For Growth And Inflation

With US$124.2 million of cash and no debt at the end of Q1 2022 and healthy cash flow, Alamos could fund all of its growth initiatives via operating cash flow and its treasury and wouldn't need to take on high-interest rate debt.

4) Near-Term Bullish Catalysts Will Reverse Recent Underperformance

AGI was underperforming the sector for the first four months of 2022 as its Mulatos mine was experiencing lower-than-expected production and higher costs over the short term, while Island Gold was also in a lower grade sequence in Q1 2022. As a result, the first half of the year was challenging.

However, the high-grade La Yaqui Grande satellite operation at Mulatos was coming online in Q3 2022, and AGI estimated that AISC at Mulatos would drop by $500 per ounce in the second half of last year.

The grade at Island Gold was also expected to increase for the remainder of the year.

These events would act as bullish catalysts and likely lead to outperformance.

5) Clear Value

AGI was trading at only 3.5x revenue and 8.5x operating cash flow, which was a massive discount compared to where it traded on a historical basis and much cheaper than most companies in the S&P 500.

At the time, the NPV of Island Gold and Young Davidson exceeded the company's $2.95 billion enterprise value, implying zero value for Mulatos, Lynn Lake, the assets in Turkey, and the tremendous exploration upside at Island Gold.

6) AGI Had Experienced A Deep Correction, Was Oversold, And Technicals Indicated A Reversal

AGI had declined ~20% over the few weeks prior, plunging to the low $7.00s on the back of the weak Q1 2022 earnings results, but it was extremely oversold and back above key support at the 200-day.

StockCharts.com

In summary, there were many clear bullish aspects about AGI at this time last May that warranted owning the stock, especially with inflation increasing.

The Story Has Played Out As Expected

Over the last year, the Alamos story has played out as anticipated.

Higher Production And Lower Costs At Mulatos And Island Gold

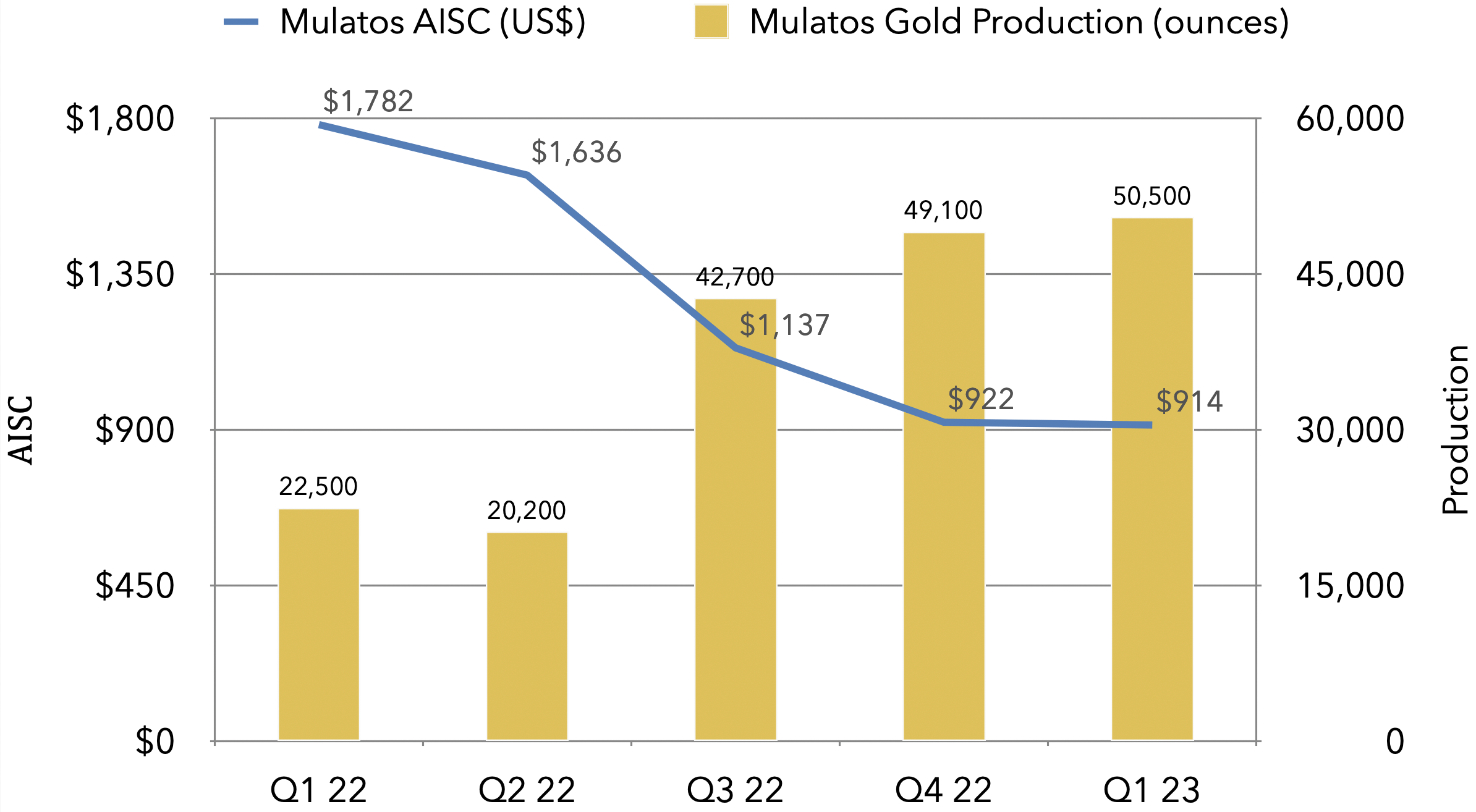

The Mulatos mine saw a considerable increase in production and a commensurate decrease in AISC in Q3 2022 as the high-grade La Yaqui Grande operation ramped up. Output in the third quarter of last year more than doubled QoQ to 42,700 ounces, while AISC declined ~$400 per ounce to $1,137. Further improvements since then have resulted in production reaching 50,000+ ounces of gold at sub-$1,000 per ounce AISC in Q1 2023.

{kind=link}

The increase in grade at Island Gold drove down AISC as well, as production surged at the mine.

By Q4 2022, Alamos's total gold production was 35% higher than in the first quarter of that year, while AISC dropped 16%, from $1,360 per ounce in Q1 2022 to $1,138 per ounce. Most companies in the sector were experiencing rising costs of 10-15% (some even higher) as the year progressed. The best-positioned saw flat to slightly increasing AISC, and that was considered a victory. Few gold miners were able to reduce costs, let alone to the degree that Alamos has since the end of Q1 2022 (when inflation began to noticeably take off).

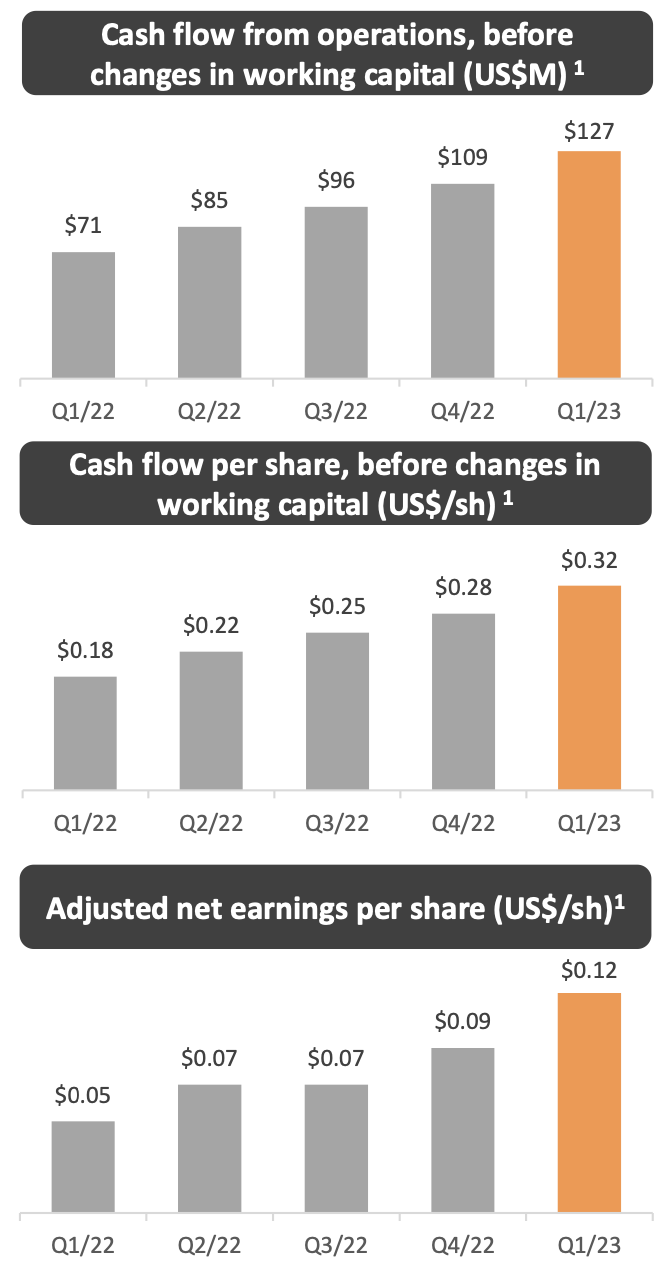

To show the strength of AGI's results, the gold price was plunging in the second and third quarters of last year, yet despite the headwind, the company posted consecutive increases in operating cash flow and net earnings per share during those periods. The gold price has acted as a tailwind since October 2022, and coupled with continued increases in production and declining costs, the positive trend in operating cash flow and net earnings per share has now stretched to four consecutive quarters.

{kind=link}

Guidance Reflects Continued Strength Of The Portfolio

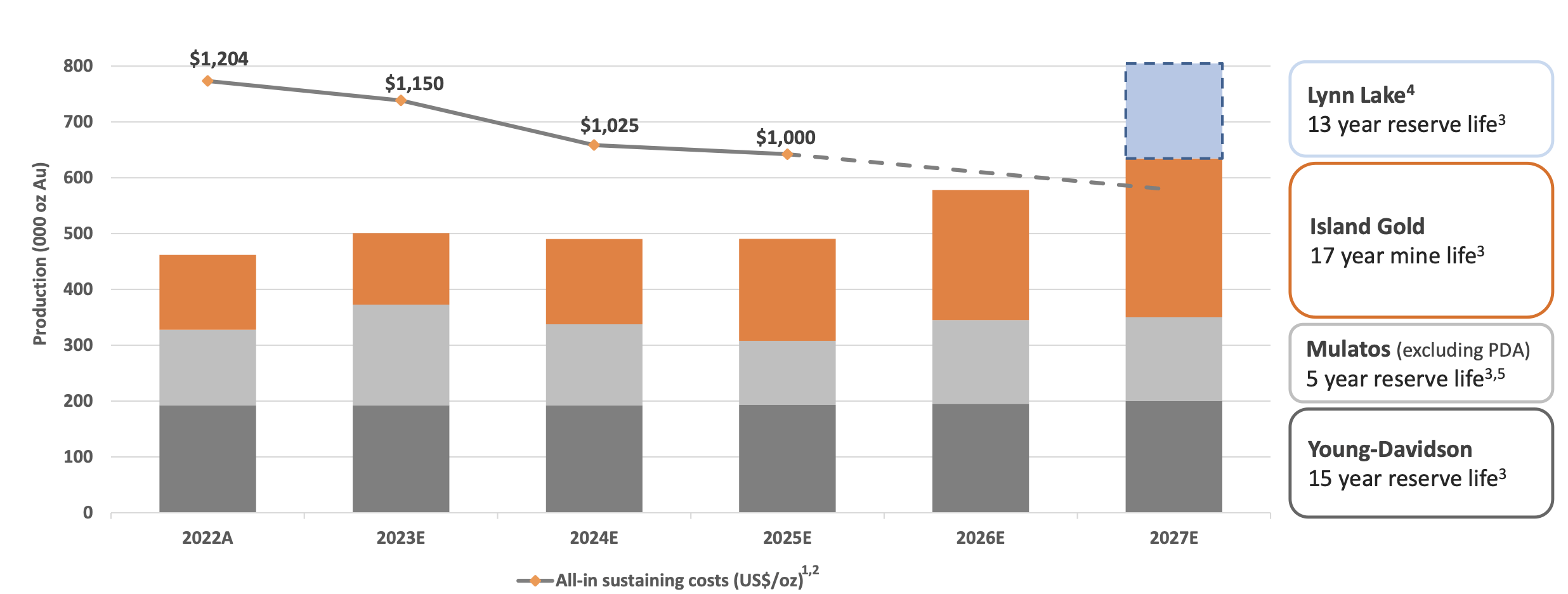

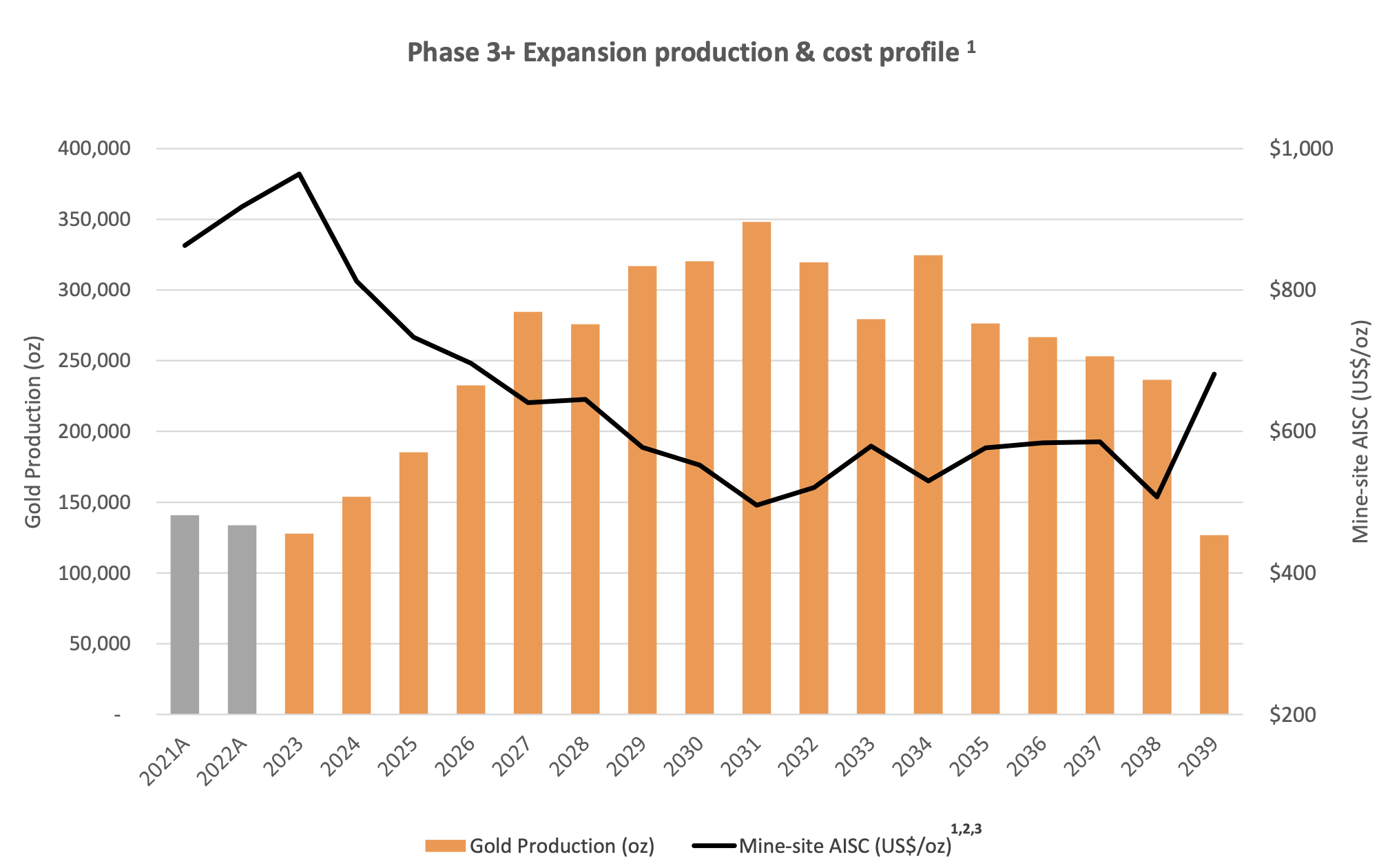

Guidance for this year calls for a 9% YoY increase in production to 500,000 ounces of gold (compared to ~460,000 ounces in 2022), while AISC is expected to drop even further to $1,150 per ounce. The positive trend of higher output and lower costs is expected to continue for the next several years, with a substantial bump in production by 2026 as the expansion at Island Gold will be complete.

There are two things I want to mention about the updated long-term guidance: 1) While gold production estimates for 2023 and 2024 are 20,000 ounces and 10,000 ounces higher, respectively, than the previous forecast, the benefits of Island Gold Phase III have been pushed back to 2026 (previous estimate was 2025) and lower production is expected at Mulatos in 2025 as well. 2) AISC estimates are $25 per ounce higher in 2023 and 2024 and are now expected to be $1,000 in 2025 vs. $800 per ounce previously. I don't believe the changes to 2025 production and AISC estimates are at all concerning. In fact, I was skeptical that Alamos could achieve $800 per ounce AISC in 2025, as I stated a year ago: "While continued inflation might not allow AGI to meet its $800 per ounce AISC target in 2025, if mines are hitting production expectations, the company should see margins expand and lower costs compared to today." In the current environment, investors shouldn't expect longer-term AISC forecasts to hold up. Alamos's AISC estimate is now around ~$950 per ounce when Island Gold's output increases to over 200,000 ounces per annum in 2026; I'm skeptical the company will be able to hit that target. But it's not about how much further AISC falls over the next few years, as AGI already has incredible margins at current gold prices. Rather, it's about the sizable advantage that the company still has over its peers, as even if AISC for the industry surges by $150-$200 per ounce over the next 2-3 years, Alamos has enough of a buffer to keep cost flat. Few companies in the sector are able to replicate what Alamos is doing.

{kind=link}

Updated Mine Plan For Island Gold Confirmed My Estimates

As also mentioned in my previous article on AGI, an updated mine plan on Island Gold would soon be released, and I was estimating:

- An additional ~1.1 million ounces of gold production due to the 1.4 million ounce increase in resources and assuming a resource conversion of 80%.

- A $350 million increase in CapEx due to inflation and increased scope of the project.

- A sizable jump in the after-tax NPV (5%) to US$2.0-$2.2 billion using a gold price assumption of $1,900. That NPV also accounted for 2020-2021 recognized cash flow and higher CapEx.

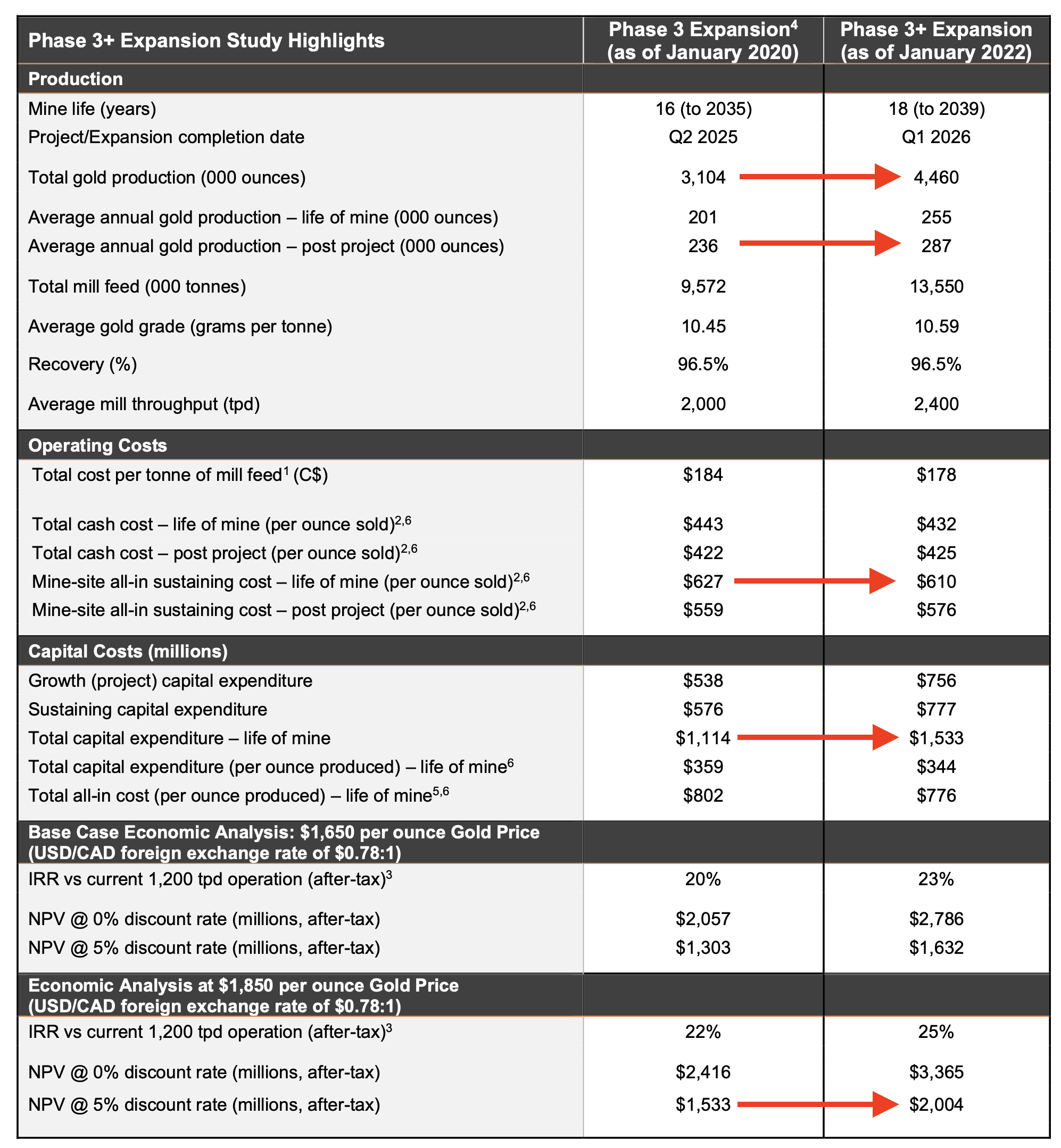

The actual results of the study are below, and I've highlighted the key metrics. Total gold production is now estimated at 4.46 million ounces, or a 1.36 million ounce increase from the 2020 study, and at a richer ore grade as well. This is higher than I estimated, as the historical conversion rate of Inferred Mineral Resources to Mineral Reserves has averaged over 100% since 2016, while I targeted a more conservative 80% conversion. As a side note, the over 100% conversion rate is due to positive grade reconciliation and more ounces than initially estimated in the block model. The average annual production after Phase III is complete has increased to 287,000 ounces per year (a gain of 51,000 ounces), while the average AISC slightly declined to $610 per ounce from an already incredibly low $627 per ounce in the 2020 life of mine. The total CapEx for the project jumped by just over US$400 million (not too far above my target). The NPV was within my range, coming in at ~US$2.1 billion at $1,900 gold ($2.0 billion at $1,850) and using similar exchange rates. That's a ~$500 million increase in the NPV.

{kind=link}

The best years are still ahead for Island Gold, as the production rate will more than double from current levels by 2027 and then will climb even further. As production surges, AISC will drop precipitously - projected to bottom out at ~$500 per ounce in 2031. When Phase III is complete, and the operation reaches the heart of the mine plan, Island Gold will be one of the best gold mines in the world. It's a tremendously valuable asset that any senior gold producer would be eager to own.

{kind=link}

Stock Price Reaction

As the bullish thesis has played out, shares of AGI have responded. Over the last 12 months, the stock has posted a total return of 84% compared to an 8% gain in gold and a 2% increase in the HUI (an index of gold mining stocks). It's been a stellar run, and it's a good time to book some profits.

Relative Valuation Has Resulted In Downgrade To A Neutral Rating

AGI was not only a top pick of mine last year; it was my #1 gold mining stock. That's been the case since I made Alamos a top pick in August 2018 when it was ~$4.50. However, given the re-rating in the shares (not just over the last 12 months, either) and how investors are no longer underpricing - or misjudging - Alamos to the same degree as they were a year ago, I've sold AGI and have moved to a neutral rating on the stock.

StockCharts.com

This is mostly a relative valuation call.

Absolute Valuation = Priced Fairly

On an absolute basis, AGI is trading around fair value at 1x NAV - slightly above if one is more conservative on the potential valuation of Island Gold that's not currently reflected in the NPV, or slightly below if more aggressive on Island's valuation and depending on if any value is assigned to the assets in Tu?rkiye and the upside at Mulatos.

Let's run some numbers and dig into the details.

The enterprise value of Alamos is US$5.3 billion.

At the current gold price of $2,050 per ounce and exchange rate of 0.75 CAD/USD, the NPV of Island Gold is ~US2.45 billion.

I would estimate the NPV of Young-Davidson and Mulatos is now ~US$1.3 billion and ~US$550 million, respectively, adjusting for the $150 per ounce higher gold price assumption and the potential value of the PDA deposit at Mulatos (which now contains over 1 million ounces of gold resources, or a 70%+ increase YoY).

It's tougher to judge the value of Lynn Lake, given the CapEx inflation since the previous study. In the 2017 Feasibility, the NPV (5%) estimate at $1,500 gold was US$290 million. Much has changed since then, as reserves have grown considerably, but inflation and the larger scope of the project might've doubled the initial CapEx. An updated FS on Lynn Lake is expected to be released this summer, and I would conservatively estimate an NPV of US$300-$500 million at current gold prices (it could be much higher, depending on where CapEx and OpEx land).

Adding it all up, there is $4.7 billion worth of assets vs. an EV of $5.3 billion, implying AGI is overvalued. However, that valuation doesn't account for any additional upside potential at Island Gold.

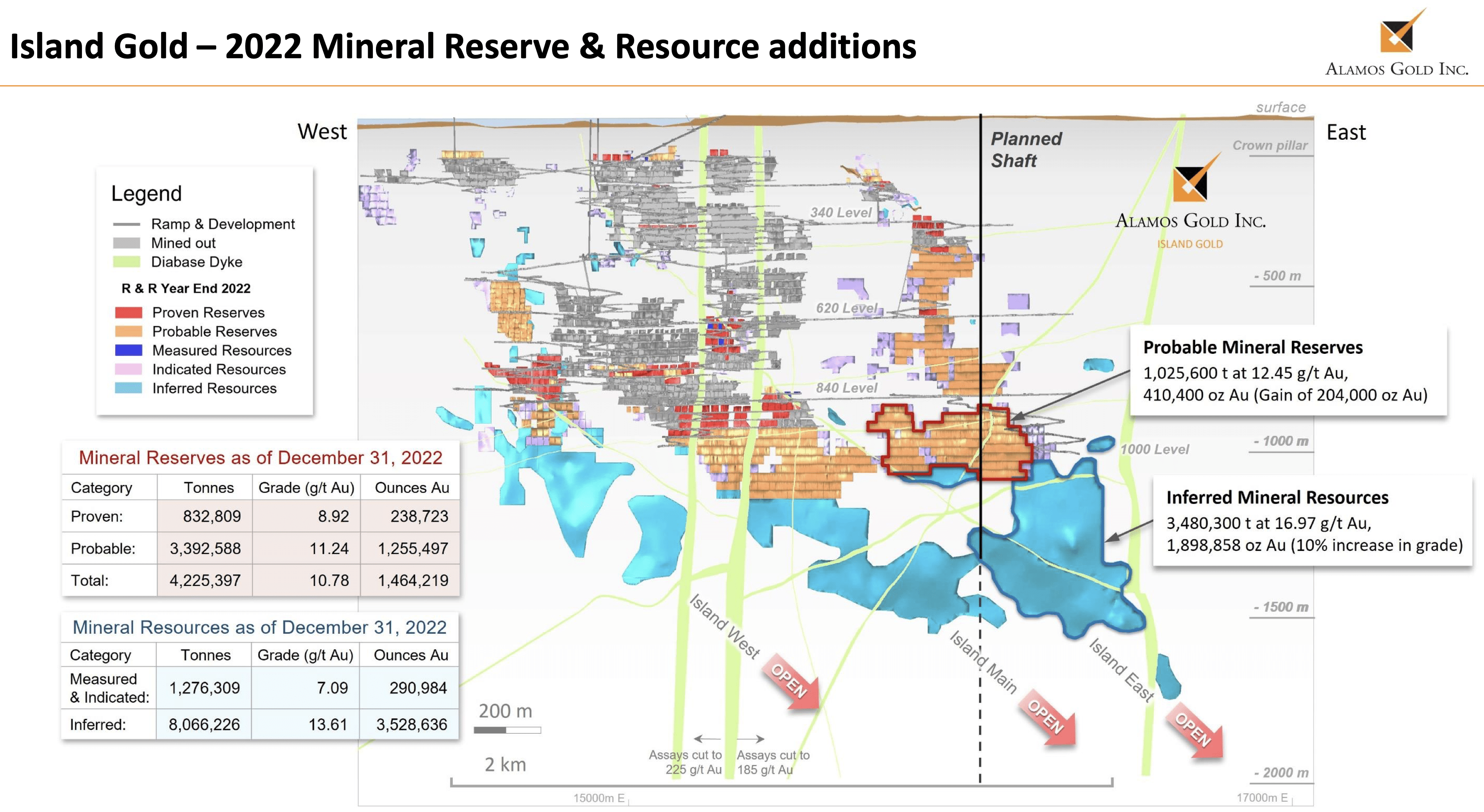

Island Gold remains open along strike and down plunge, and the grade is increasing at depth (e.g., the reserve grade at Island East is 12.45 g/t while the Inferred resources below are 16.97 g/t). Total reserves and resources keep growing year-over-year, and Island Gold now contains 5.3 million ounces of gold. Alamos has added 1-2 years of mine-life over each of the last two years, and I believe that trend will continue.

{kind=link}

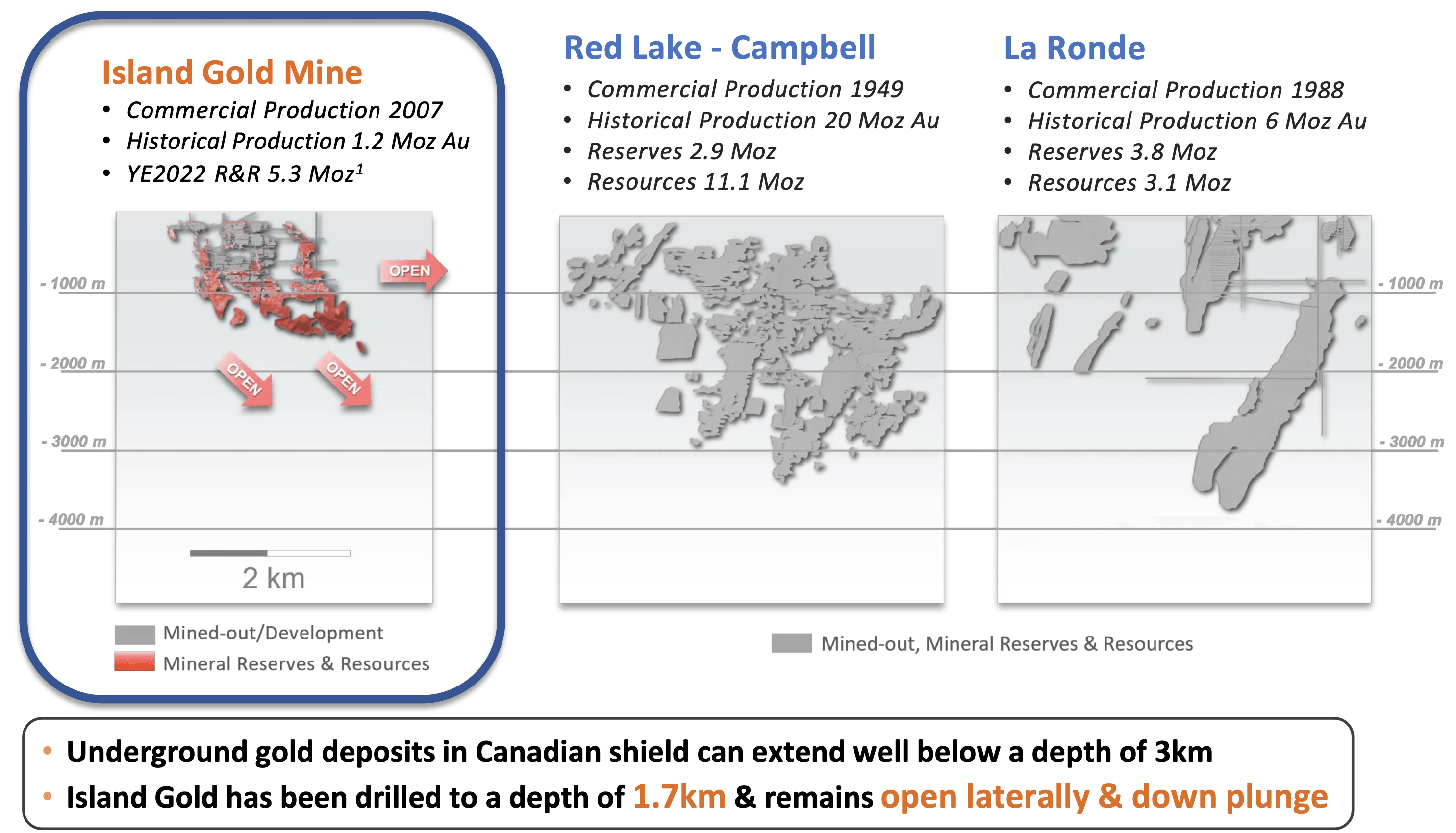

If we compare the current depth of Island Gold to other gold mines in the region, such as the Campbell mine at Red Lake and the La Ronde mine, systems like Island Gold can extend to much greater depths (2x the depth that which Island Gold has been drilled). Alamos is sinking a shaft at Island East (which is part of this Phase III expansion) and will be able to capitalize on any additional ounces down plunge.

{kind=link}

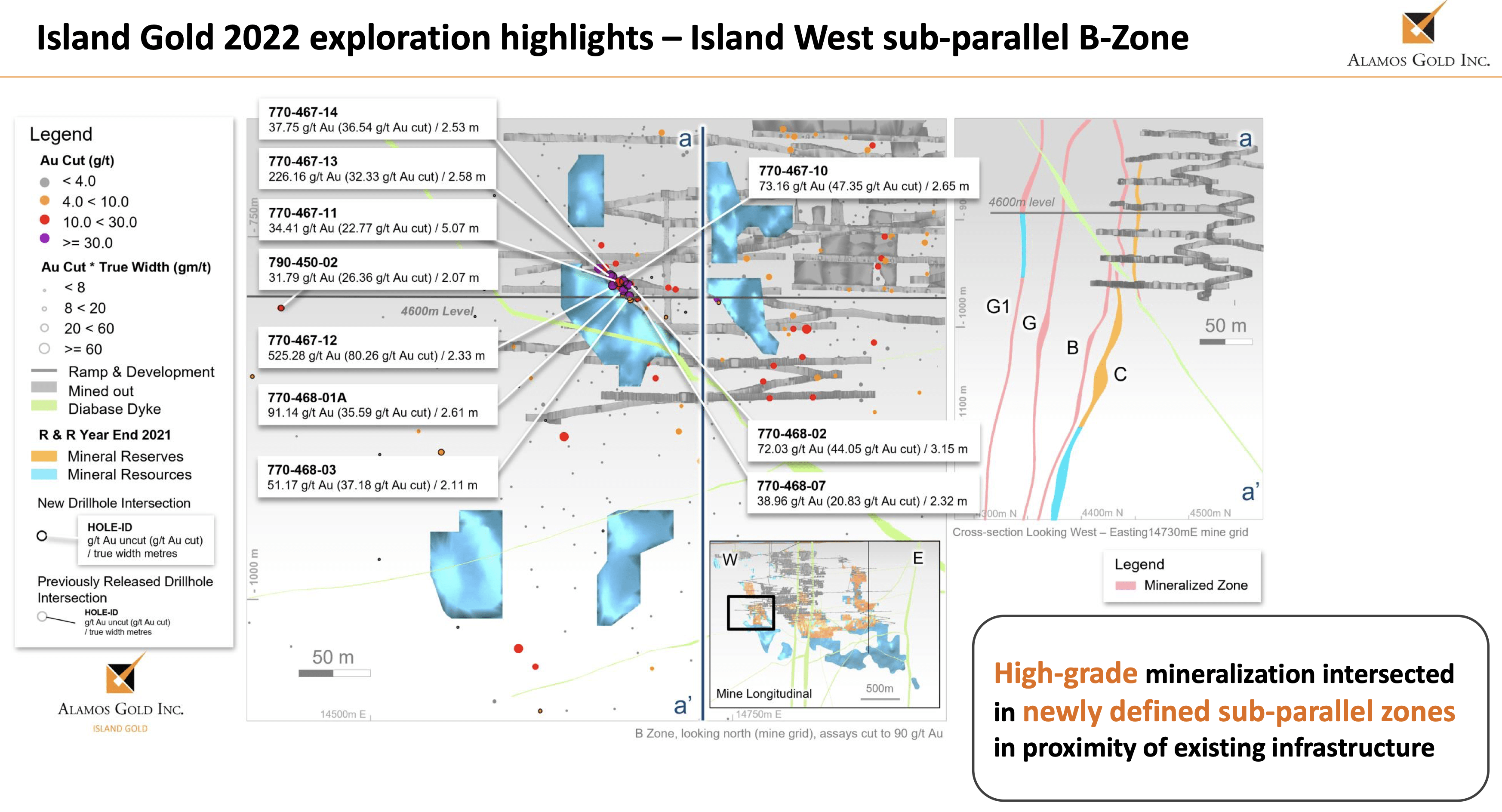

But it's not just at depth that Alamos is finding more ounces, as exploration results at about the 900-1,000 meter level at Island West have identified newly defined, high-grade sub-parallel zones near the existing infrastructure. Several holes averaged 1-2 ounces per tonne (or 3-6x the average mined grade) over 2 meters.

{kind=link}

Unless they are bonanza-grade and prioritized in future mine plans, any ounces discovered down plunge won't come online for another 20 years. Still, if we factor in another one million ounces (or four years) of production at the back-end of the current LOM and account for higher sustaining capital for the increased development cost, that's another ~$400 million of after-tax NPV.

If Island Gold continues down plunge for another 1,000-1,500 meters and the grade holds up, the mine life extension could be 10-20 years.

You can likely estimate a ~US$100 million increase in the after-tax NPV for every additional year of mine life added to the LOM, and there could be another $1-$2 billion of value depending on if exploration success continues. So, the current NPV of US$2.45 billion doesn't reflect the potential (maybe even true) value of Island Gold.

Then there are the assets in Türkiye. Kirazli, Agi Dagi, and Camyurt had a collective value of over US$1 billion, but construction at Kirazli was suspended in 2019 after the Turkish government failed to grant the routine renewal of Alamos's mining licenses. The company filed a US$1 billion investment treaty claim against Tu?rkiye "for expropriation & unfair & inequitable treatment" of its projects. I've assigned zero value to these assets, but they do represent a potential upside to the valuation should Alamos be successful with its claim.

{kind=link}

I prefer to be conservative with any valuation analysis. Assuming a modest mine life extension at Island Gold and zero value for the assets in Türkiye, I can get to a ~$5.3 billion fair value for AGI. The difference maker will be whether Island Gold will be a ~25-year, ~250,000 ounces per annum mine or a 40+ year mine at the same production level. If it's the latter, then AGI is still trading at a healthy discount to its fair value.

Relative value = Priced Aggressively

Moving up by 80% over the last 12 months while its peers remained around the flat line, AGI's relative valuation has expanded considerably. But it's not just been within the last 12 months that Alamos has seen an aggressive move in its stock, as shares are up 363% since their lows in 2018, which is more than 3x the performance of the HUI.

Many quality gold miners are trading at 0.5-0.7x NAV, and some of the best developers are at even deeper discounts to the fair value of their assets.

Few producers in the sector are trading at around 1x NAV like Alamos; only the royalty/streaming companies are commanding higher valuations on average (due to their high-margin, inflation-resistant business model).

It's difficult to justify the risk/reward with AGI when so many other gold miners are at such steep discounts, and I don't believe the stock will continue to outperform as it has over the last several years, which is why AGI now deserves a neutral rating.

AGI is the best acquisition candidate among all of the mid-tier producers and a likely target by some of the larger gold miners. But even if Alamos is bought out, I don't believe the premium would be excessive (I would estimate 15-20%). The high relative valuation could also act as an impediment for potential suitors.

Other Factors To Consider

There are other aspects we need to take into account when analyzing Alamos's valuation:

1. The management team is top-notch, as John McCluskey, CEO of Alamos, has taken the company from a single-asset, small producer with ~100,000 ounces of gold production to a multi-asset, mid-tier producer with 500,000 ounces of gold output and growing.

Alamos, under McCluskey's stewardship and vision, has followed the path of Agnico-Eagle ( AEM ) and methodically built the company to what I believe is currently the best mid-tier gold producer in the world.

A premium should be applied to AGI because of its management, which is backed by an equally strong Board of Directors.

2. Low-cost gold producers generally command a premium in the market, and AGI should trade at a higher value than other gold mining stocks.

3. The majority of Alamos's production comes from Canada and the rest from Mexico, which gives AGI a sizable jurisdictional risk advantage over other gold miners that operate in less favorable regions of the world. Producers with a heavy presence in the U.S. and Canada typically trade at a higher multiple.

But there are also current risks with Alamos that offset some of those premium aspects.

Risk 1

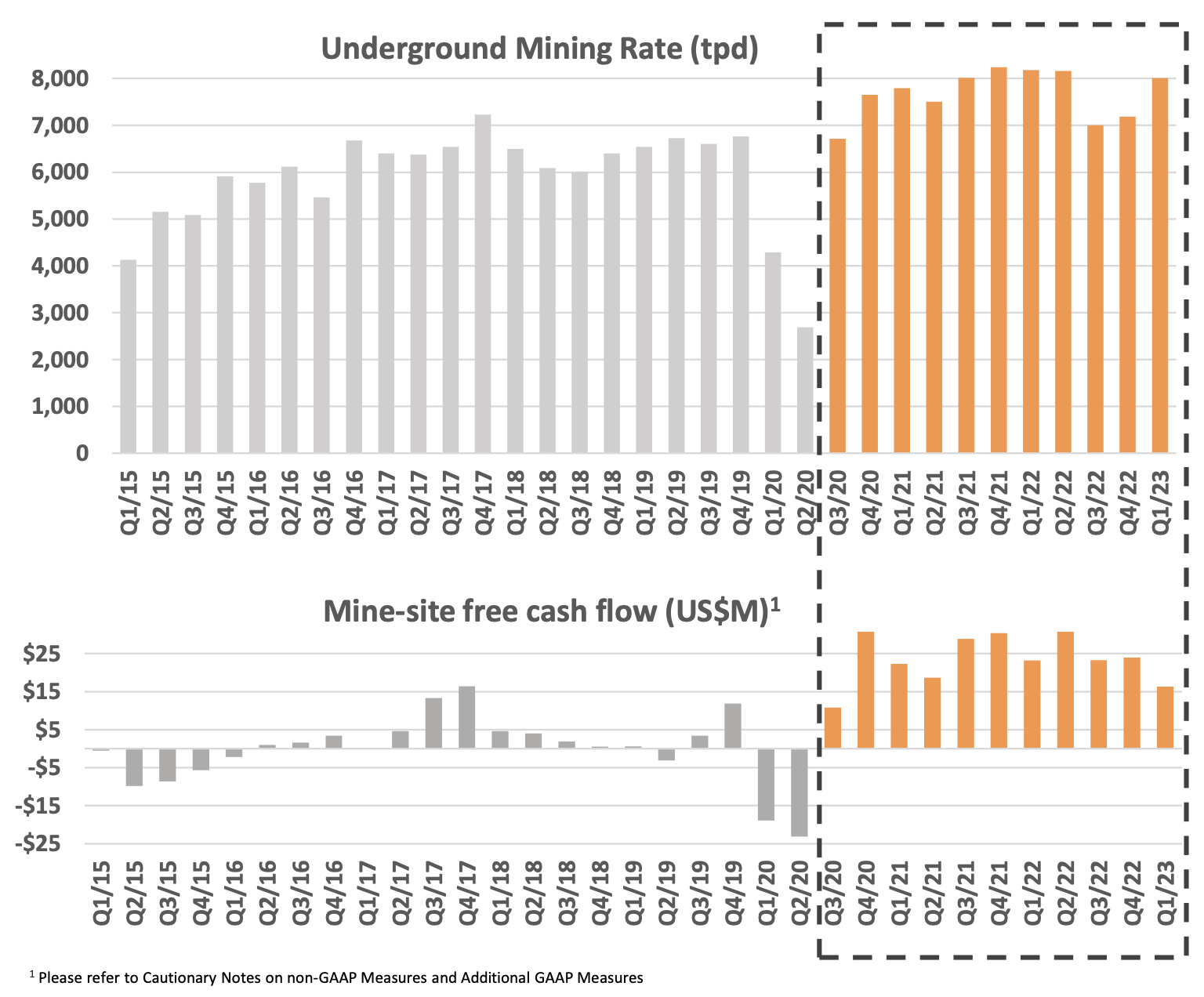

Young-Davidson is estimated to generate US$100 million of free cash flow per year at $1,750 gold. For the last several quarters, YD has struggled to reach the $25 million mark needed to achieve the annual free cash flow projections. In fairness to Alamos, the average realized gold price in Q3 and Q4 2022 was roughly $1,750, and the underground mining rate temporarily dipped to ~7,000 tonnes per day, and the mine still came close to the target. Last quarter, YD only generated $16.3 million of free cash flow, but the quarter was also negatively impacted by a temporary buildup of $8 million of sales tax receivables, which according to AGI, "were collected in April and will benefit the second quarter." Still, the gold price averaged $1,900 in Q1 2023, and I would've expected more free cash flow. With gold solidly above $2,000, YD should generate well in excess of $25 million of FCF per quarter. While AGI could still hit its goal of $100 million per year of free cash flow from this operation, if it's only generating that amount at $2,000 gold, then it's a downgrade to the original target. YD is an extremely low-grade operation, but it's economical because it's bulk mined. However, the low grade makes Young-Davidson more susceptible to inflation and cost pressures. It's something I'm keeping my eye on as my valuation for the asset adjusts higher for current gold prices.

{kind=link}

Risk 2

Mexico just passed a bill that changes the way mining concessions and water rights are determined and implements a 5% tax that will go to local communities. Some of the language in the bill is ambiguous, and many mining companies in the region are still trying to determine what (if any) impact it will have on their operations or projects.

Alamos is an established producer in the region with a solid reputation, but it's unclear if any of these changes could negatively impact Mulatos.

Risk 3

The Island Gold P3+ Expansion Study contains 87% of M&I and Inferred Mineral Resources, and the majority of those ounces are in the Inferred category. Inferred ounces haven't been drilled enough, and drill spacing is wide (over 100 meters). Confidence in these ounces is lower than M&I resources or mineral reserves, the latter of which are drilled to 30-50 meter centers.

Given the depth of these Inferred resources, drilling from underground is more cost-effective. Once the shaft is complete and the underground built out more, these ounces will be thoroughly drilled off and moved up to reserves.

I have much higher confidence in the Inferred ounces at Island Gold than I do for other projects, especially given the historical 100% conversion rate of Inferred Resources to Reserves and positive grade reconciliation. The mineralization of the resources at Island is also consistent with the style of mineralization of the reserves and part of the same structure, implying it's all one continuous orebody. Still, using Inferred resources in a mine plan carries a higher risk until those ounces are more tightly drilled.

All of these aspects (positive and negative) have been taken into account in my valuation and updated rating.

For further details see:

Alamos Gold: After An 80% Run, I'm Downgrading To A Neutral Rating