AGI:CC - Alamos Gold: Another Blowout Quarter

2023-10-27 12:26:54 ET

Summary

- Alamos Gold trounced quarterly guidance yet again with near-record production, prompting the company to raise its FY2023 guidance.

- Meanwhile, it is one of the few producers enjoying lower operating costs year-over-year, though it is getting some help from the weaker Canadian Dollar.

- In this update, we'll look at the Q3 results and why AGI remains a premier name in the sector and one of the best ways to get exposure to gold.

The Q3 Earnings Season for the Gold Miners Index ( GDX ) began this week, and it's been a mixed start to Earnings Season. This is because two companies came in slightly below estimates because of lower processing rates at their larger operations, while OceanaGold ( OCANF ) saw lower production at its flagship Haile Mine because of weaker than planned grades at the lower benches of the Mill Zone. However, true to form, Alamos Gold ( AGI ) over-delivered on its promises again in Q3, beating its guidance midpoint by over 8% after just coming off a 9% beat vs. its guidance midpoint in Q2. These consecutive beats have prompted the company to raise annual guidance by ~5% and Alamos is even more unique in that it's reporting lower operating costs on a year-over-year basis. Let's take a closer look at the quarter below.

{kind=link}

P3+ Construction - Company Website

Q3 Production & Sales

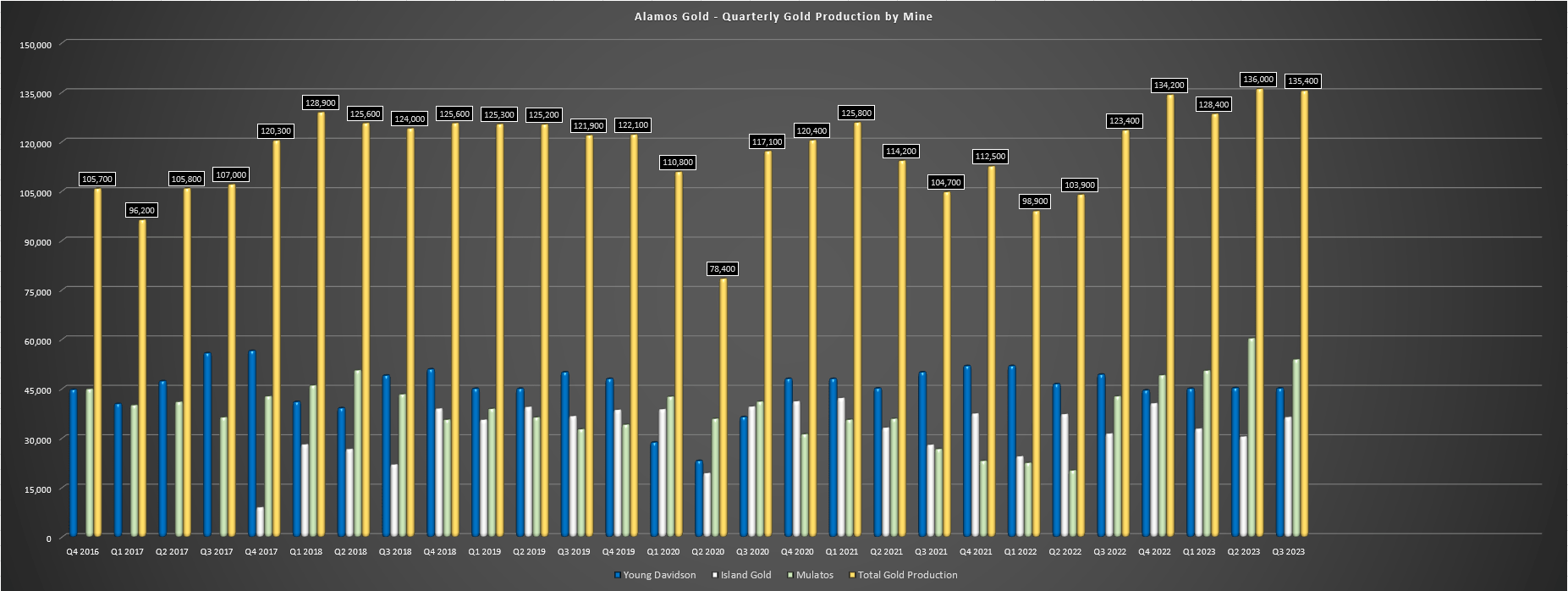

Alamos Gold released its Q3 results this week, reporting quarterly production of ~135,400 ounces of gold, an 8% beat vs. its quarterly guidance mid-point of 125,000 ounces. Notably, this was the second consecutive beat, with strength in the quarter being broad-based with solid quarters from all three of its producing assets. The stand out in the period was Mulatos, which produced ~53,900 ounces at $1,045/oz all-in sustaining costs [AISC] and has now generated upwards of $114 million in free cash flow year-to-date with the benefit of higher grades from La Yaqui Grande. However, the company's other two operations put up impressive performance as well, with Island Gold seeing higher production of ~36,400 ounces at industry-leading AISC of $916/oz and Young-Davidson remaining consistent, with production of ~45,100 ounces at $1,178/oz, with the mine on track for its third year generating over $100 million in mine-site free cash flow.

{kind=link}

Alamos Quarterly Production by Mine - Company Filings, Author's Chart

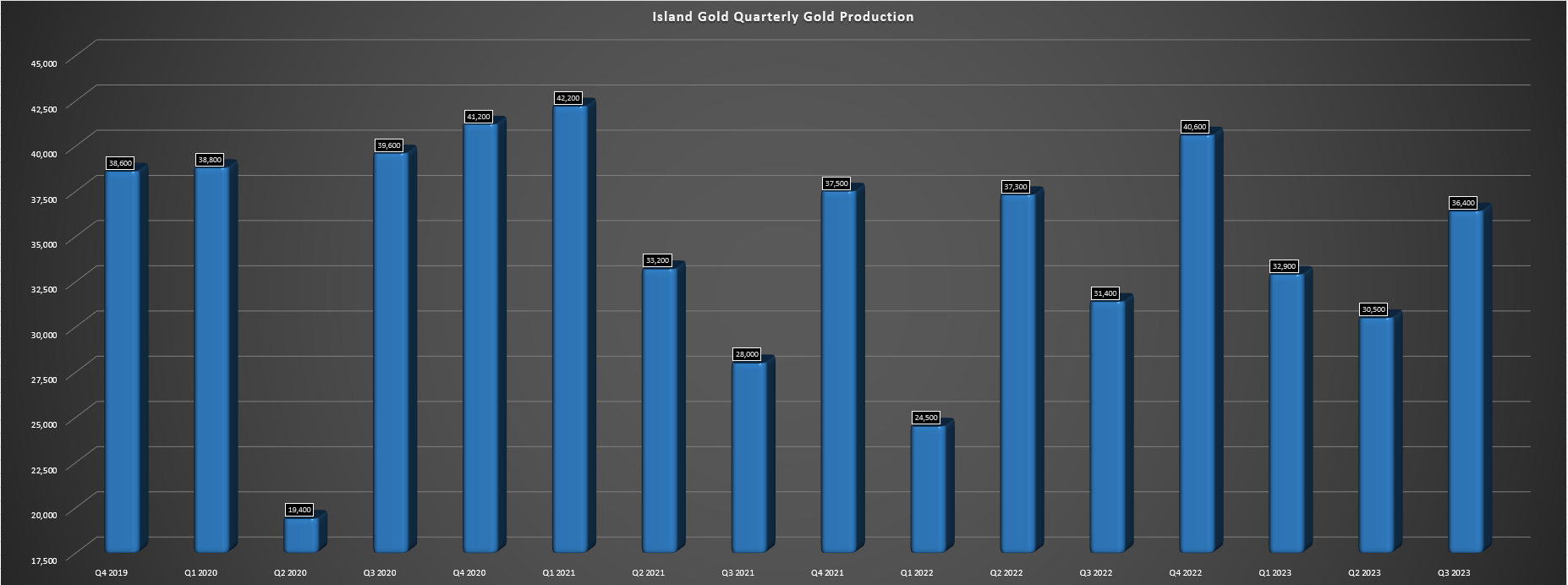

Digging into the operations a little closer, Island Gold's output increased year-over-year on the back of higher grades that offset slightly lower throughput and a higher recovery rate of 97%, with ~113,100 tonnes processed at 10.11 grams per tonne of gold (Q3 2022: 9.38 grams per tonne of gold). And it's worth noting that the mine's costs were down year-over-year despite sector-wide inflationary pressures and despite higher sustaining capital in the period. Meanwhile, the company continues to make solid progress on its P3+ Expansion at Island with $34.5 million spent on growth capital (~$118 million year-to-date), construction of the hoist house complete, and shaft sinking set to begin by year-end. And for those unfamiliar with the Island Gold Mine, given that it certainly isn't obvious from the below production chart, the asset will become one of Canada's larger mines and the lowest-cost mine in Canada post-2026, with ~300,000+ ounces on average (2027-2031) at sub $650/oz AISC even adjusting for inflationary pressures.

{kind=link}

Island Gold Quarterly Production - Company Filings, Author's Chart

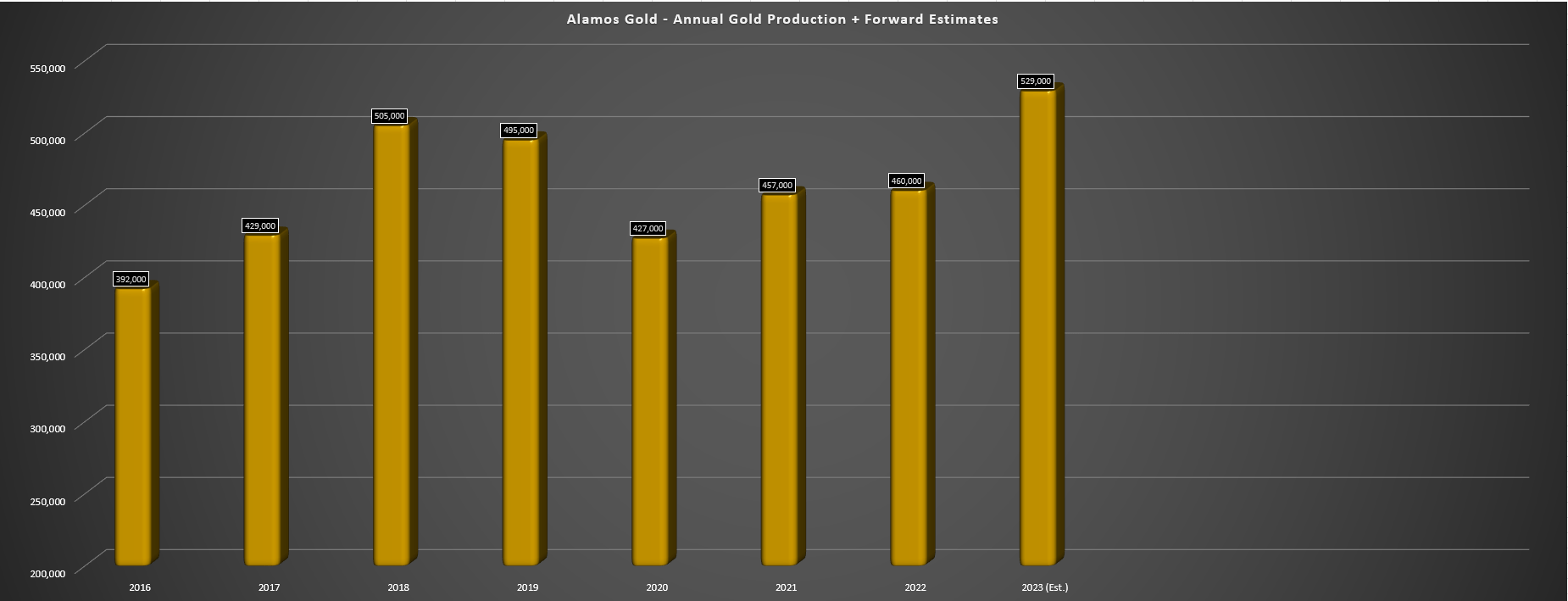

Given these impressive results from its three producing assets, Alamos is not only on track to trounce its initial guidance (480,000 to 520,000 ounces) with ~400,000 ounces produced year-to-date, but it could come in at the high end of its upwardly revised guidance of 515,000 to 530,000 ounces and within cost guidance of $1,125/oz to $1,175/oz (year-to-date AISC of $1,136/oz), placing its costs over 15% below the estimated FY2023 industry average (~$1,360/oz). And while the company has gotten some help from the weaker Canadian Dollar, it was partially offset by the ~15% increase in the Mexican Peso at its Mulatos operation, so the company did not benefit as much as producers with solely Canadian operations like New Gold ( NGD ). Finally, it's worth noting that this will mark a record year for Alamos Gold assuming no hiccups in Q4, with the potential to produce ~529,000 ounces (high-end of guidance), smashing the previous record of ~505,000 ounces and this is with major growth in the wings at Island P3+ and Lynn Lake (combined ~360,000 incremental ounces in first five years averaged across both operations).

{kind=link}

Alamos Gold Annual Production & FY2023 Estimates - Company Filings, Author's Chart & Estimates

Costs & Margins

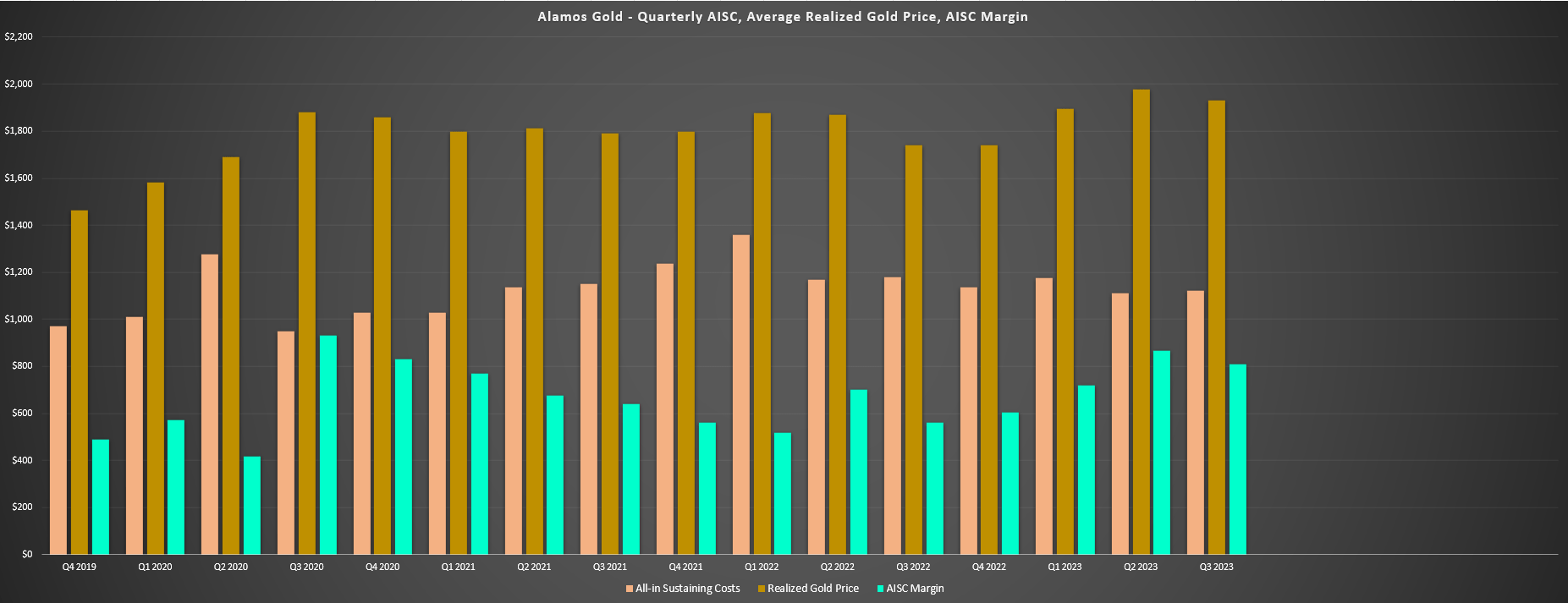

Moving over to costs and margins, Alamos reported cash costs of $835/oz (down 4% year-over-year), and all-in sustaining costs of $1,121/oz (down 5% year-over-year) despite higher sustaining capital spend in the period ($27.3 million) and fewer ounces sold vs. produced. And if the company had sold all of its produced ounces, its all-in sustaining costs would have come in closer to $1,100/oz, placing its costs even further below the industry average. Given the impressive cost control, Alamos' saw considerable margin expansion, with AISC margins soaring 44% to $811/oz, giving it some of the highest margins sector-wide among North American producers. And while we will see higher costs in Q4 as the company catches up on sustaining capital (~70% spent year-to-date), margins will still improve year-over-year, benefiting from the higher average realized gold price (Q4 2022 average realized gold price: $1,741/oz).

{kind=link}

Alamos Gold - Quarterly AISC, Average Realized Gold Price & AISC Margins - Company Filings, Author's Chart

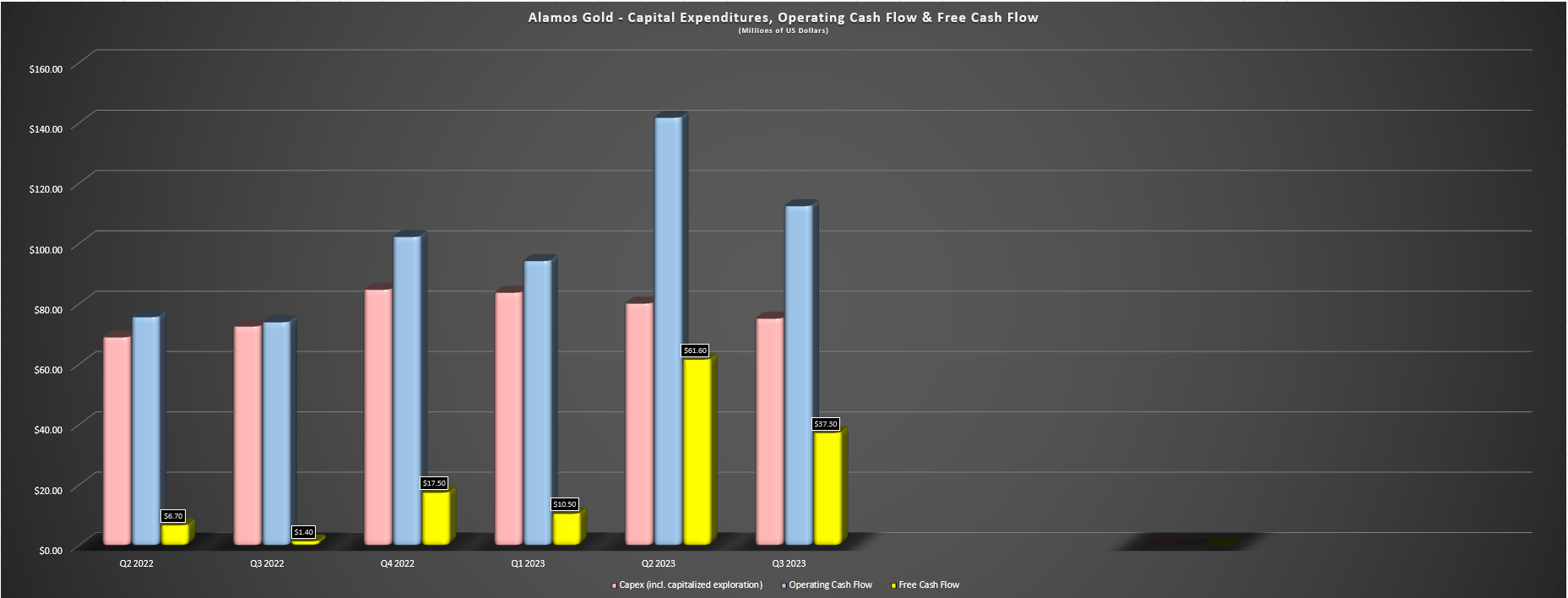

Moving to the financial results, you wouldn't know that Alamos was in the midst of a major growth project looking at its free cash flow generation, with the company reporting $37.3 million in free cash flow despite higher capex year-over-year, and ~$110 million in free cash flow year-to-date. This helped to strengthen Alamos' already strong balance sheet with ~$216 million in cash and no debt, and this solid free cash flow generation will allow the company to continue funding its growth (~55% left to spend or ~$420 million) without taking on debt and leveraging up like some of its peers. To summarize, everything is going as planned, and we should see a year of even better margins in 2024 if the gold price can cooperate with FY2024 guidance of ~$1,025/oz.

{kind=link}

Alamos Quarterly Capex, Operating Cash Flow & Free Cash Flow - Company Filings, Author's Chart

Summary

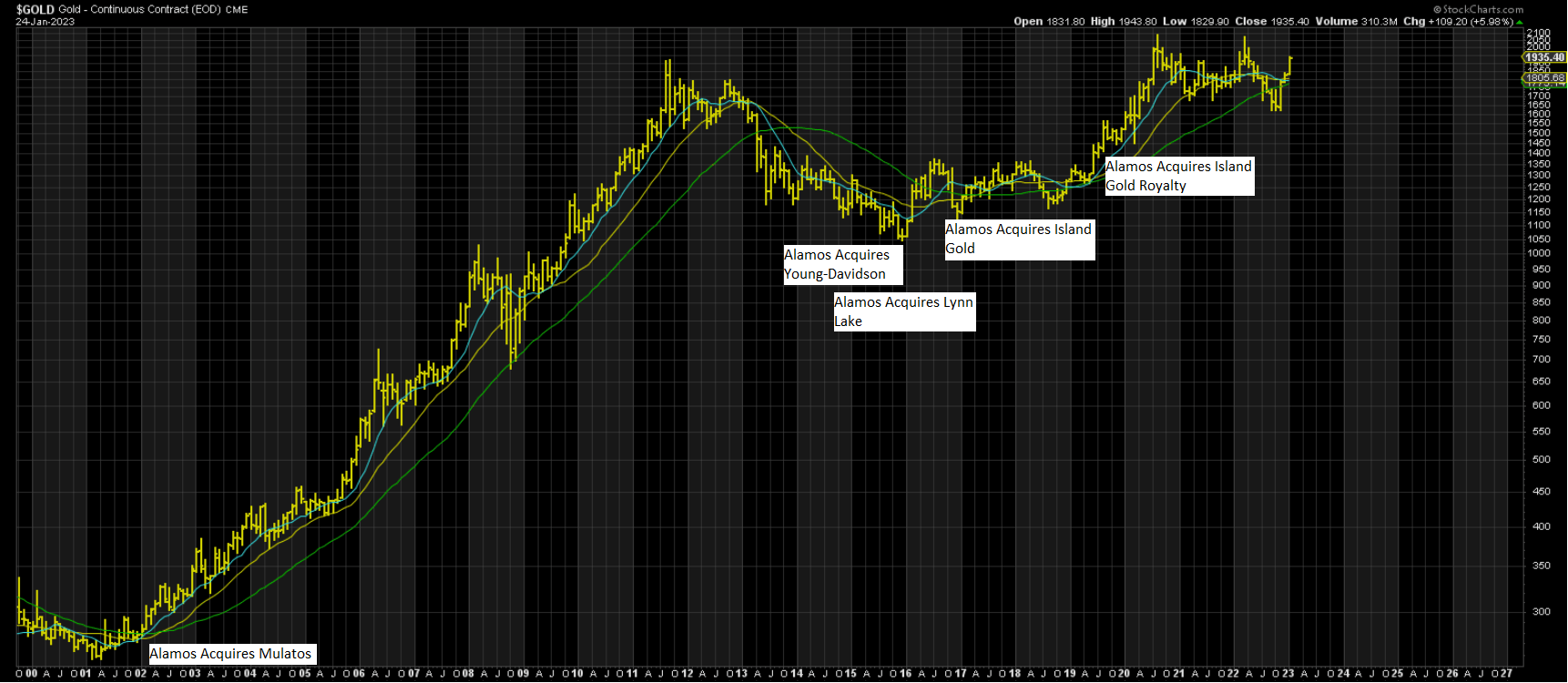

As stated by Alamos, its aim is to operate a sustainable business with growing production, expanding margins, and increasing profitability that leads to growing returns to all stakeholders (while employing a balanced approach to capital allocation). And while many precious metals producers might convey similar objectives, few follow through, and most fail miserably. This is precisely what makes Alamos so unique, which is that it has consistently grown in a disciplined manner while maintaining a strong balance sheet and occasionally stepping into the market during periods of extreme pessimism to scoop up high-quality assets at fire-sale prices, all while maintaining a focus on margins vs. absolute production. And while we saw one deal not pan out with its Turkish assets added in 2009 (Agi Dagi, Kirazli), it has more than made up for this with its other acquisitions, and will be the proud owner of the lowest-cost mine in Canada post-2026.

{kind=link}

Alamos Gold - Past Acquisitions In Counter-Cyclical Manner - StockCharts.com

This model is like the model that Agnico Eagle ( AEM ) has employed, which can be thought of as similar to two of Warren Buffett's key rules (don't lose money, and it's better to buy a wonderful company at a fair price than a fair company at a wonderful price. Extending these rules to both companies M&A approach, employing these tenets essentially means not making risky bets when it comes to acquiring assets, meaning avoid those assets with high technical complexity, lack of community support, and/or those in volatile jurisdictions, and focus on the best assets, not average assets. And looking at the acquisition of Mulatos (still producing 20+ years later with a new discovery in PDA, Young-Davidson, Lynn Lake (future 20+ year mine life) and Island Gold, the company has excelled in this department, and it's bought these exceptional assets at great prices, not fair prices, which is even more impressive.

Given this discipline, Alamos is easily a top-5 gold producer sector-wide despite its smaller scale, and this excellence has extended to the company's operations where the company is firing on all cylinders lately and trouncing guidance in a sea of misses. Hence, for investors that are looking for a way to play the gold sector without the headaches, I see AGI as a premier name and I would view any sharp pullbacks as buying opportunities.

For further details see:

Alamos Gold: Another Blowout Quarter