AGI - Alamos Gold: Another Year Of Successful Reserve Replacement

2023-07-23 07:13:36 ET

Summary

- Alamos Gold reported another year of successful reserve replacement in 2022, ending the year with reserves of ~10.5 million ounces at an average grade of 1.63 grams per tonne gold.

- Notably, the company's strong reserve and resource growth has continued at Island, with multiple high-grade intercepts reported since year-end, pointing to further reserve growth at this key asset.

- Given AGI's disciplined approach to M&A and ability to grow NAV and reserves per share at a rate far exceeding its peers, I see it as a top-3 gold producer.

It's been a two-year rollercoaster ride for investors in the Gold Miners Index (GDX), with the index seeing zero progress since January 2021 despite a higher gold price and the multiple rallies have brought out chants of $50+ price targets only to fizzle out shortly after. The lack of staying power when it comes to rallies has been partially attributed to margin compression from inflationary pressures, but other reasons for underperformance include multiple poorly timed or lower-quality acquisitions near cyclical peaks and an inability to successfully replace reserves on balance. In fact, less than 25% of larger gold producers fully replaced reserves last year, and this was despite many gold producers raising their gold price assumptions which should have provided a lower hurdle for replacing mined depletion.

Portfolio Returns - January 2021 to July 2023 (Author's Portfolio Returns)

{kind=link}

It's for these reasons that the Gold Miners Index and most miners have been a better trading vehicle than an investment over the past three years. Unfortunately, some investors have remained married to their positions with an unwillingness to book any profits in the hope that we'd see a steady trend of higher highs and lows despite the index up against a mountain of near unprecedented headwinds (inflationary pressures, steeply rising shares count due to non counter-cyclical M&A and government policies/political shifts which have made some jurisdictions less appealing than they were three years ago). Fortunately, I've managed to outperform the index's [-] 19% return since January 2021 by being rigid and sticking to the highest-quality miners. And while I have made some poor calls along the way, Alamos Gold ( AGI ) is an example of one high-quality name that has contributed to outperformance and that continues to execute successfully with AGI having one of the brightest futures sector-wide. In this update, we'll look at its 2022 Reserve/Resource statement and why it's a name worth buying on any 25%+ pullbacks.

2022 Reserves & Resources

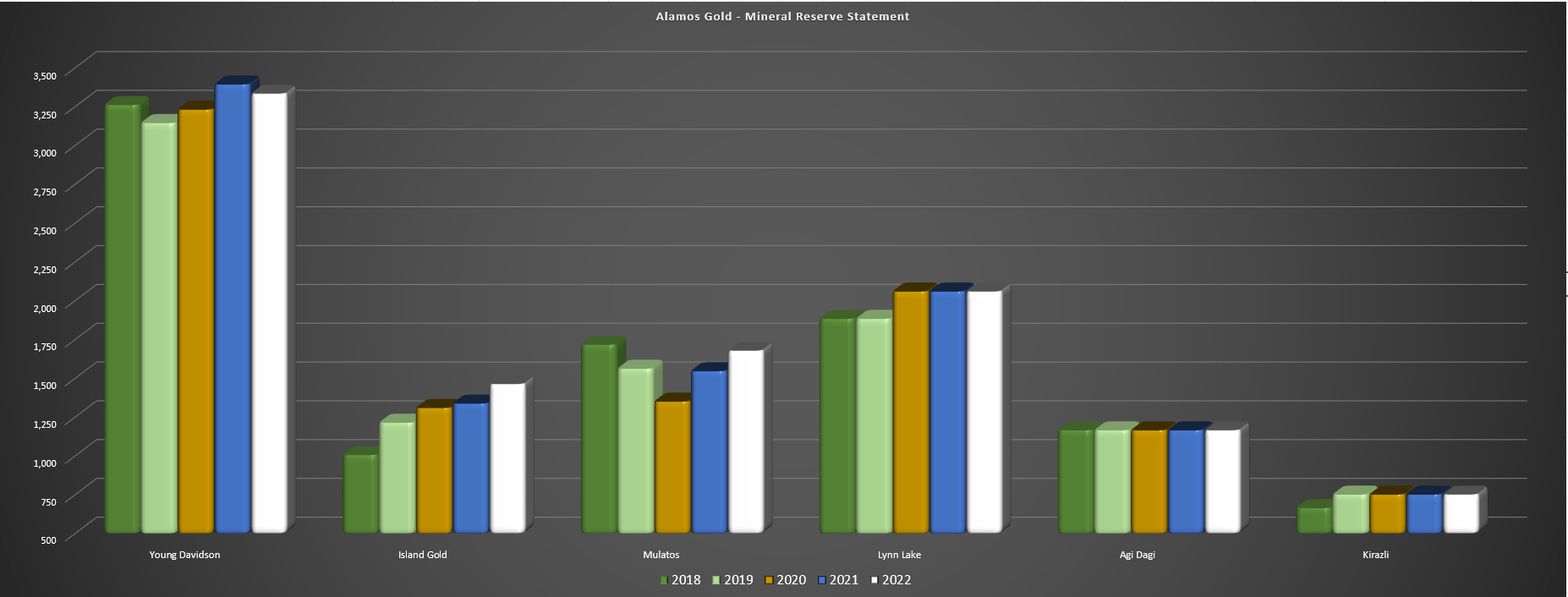

Alamos Gold released its year-end Reserve & Resource statement earlier this year, reporting a 2% increase in gold reserves to 10.46 million ounces of gold at an average grade of 1.63 grams per tonne of gold. This translated to a 2% increase year-over-year (2021: 10.26 million ounces), and a 3% increase in grade, helped by reserve additions at Mulatos (which included a material increase in grades), and reserve growth at Island Gold, where the company's reserves now sit at ~1.46 million ounces, up 45% from 2018 levels following its acquisition of Richmont Mines, despite mined depletion of ~800,000 ounces. At Island Gold, the growth came from the addition of 267,000 ounces vs. 142,000 ounces of depletion, and reserve grades increased 7% year-over-year, translating to a higher-quality reserve base (10.78 grams per tonne of gold vs. 10.12 grams per tonne of gold). At Mulatos, the new Puerta Del Aire ["PDA"] discovery led to meaningful growth, with the maiden reserve of ~428,000 ounces expanded to ~728,000 ounces at higher grads.

Assuming a 1,500 per day mining rate with plans to mine PDA underground by ramp and development drifts from the main Mulatos Pit, the ~4.7 million tonne reserve base would support a 8.5+ year mine life, and given continued exploration success, there looks to upside to this figure.

Alamos Gold - Mineral Reserves by Mine/Project (Company Filings, Author's Chart)

{kind=link}

Unfortunately, the company's bulk underground Young-Davidson Mine west of Kirkland Lake was unsuccessful replacing reserves at year-end 2022, with reserves declining marginally year-over-year to ~3.34 million ounces of gold at slightly lower grades (2.35 grams per tonne of gold). However, it's important to note that this was partially due to contractor personnel challenges which impacted the amount of drilling completed last year. Plus, the decline isn't anything to be worried about, with this asset having a strong track record of reserve replacement since 2018 and reserves actually up 2% despite significant mined depletion in the period. And while some mines that reported reserve depletion like Yaramoko and San Jose are coming up against a wall as their mine lives sit below four years, Young-Davidson boasts a 15-year reserve life based on 8,000 tonne per day mining rates and an expanded drill program in 2023 should help pick up some slack from 2022.

Young-Davidson Mine (Company Website)

{kind=link}

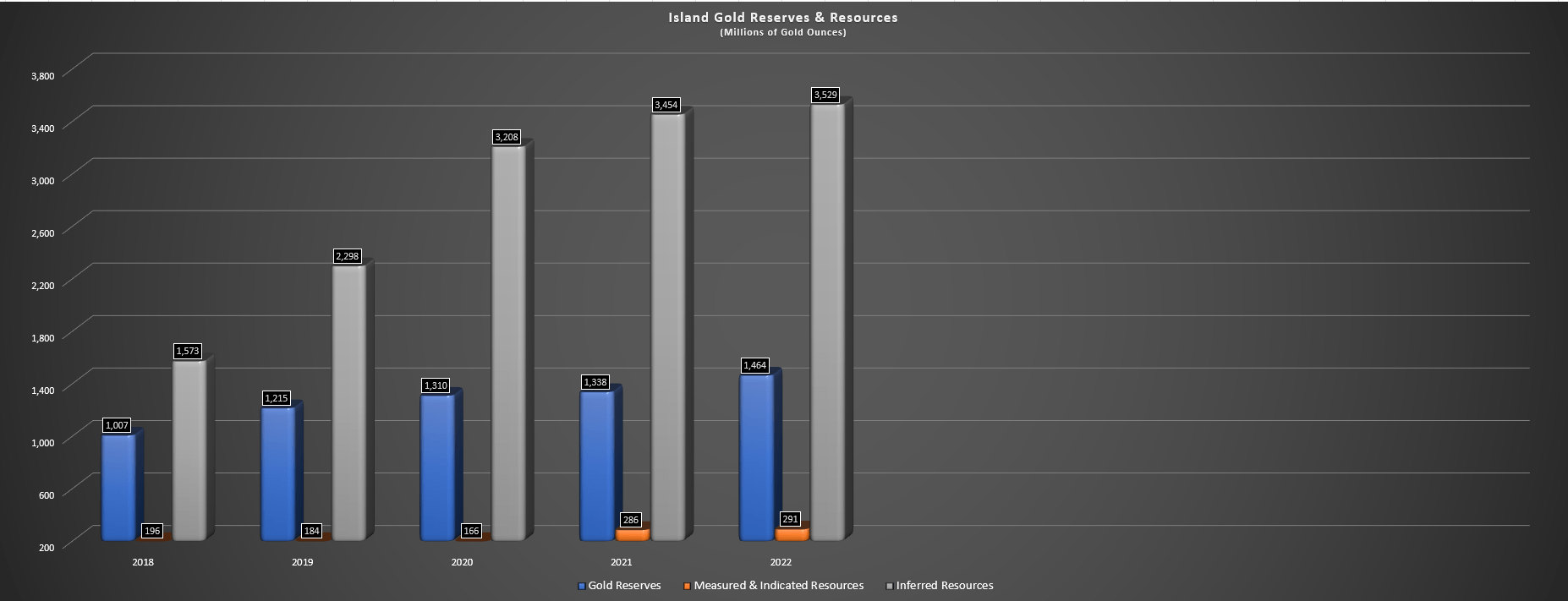

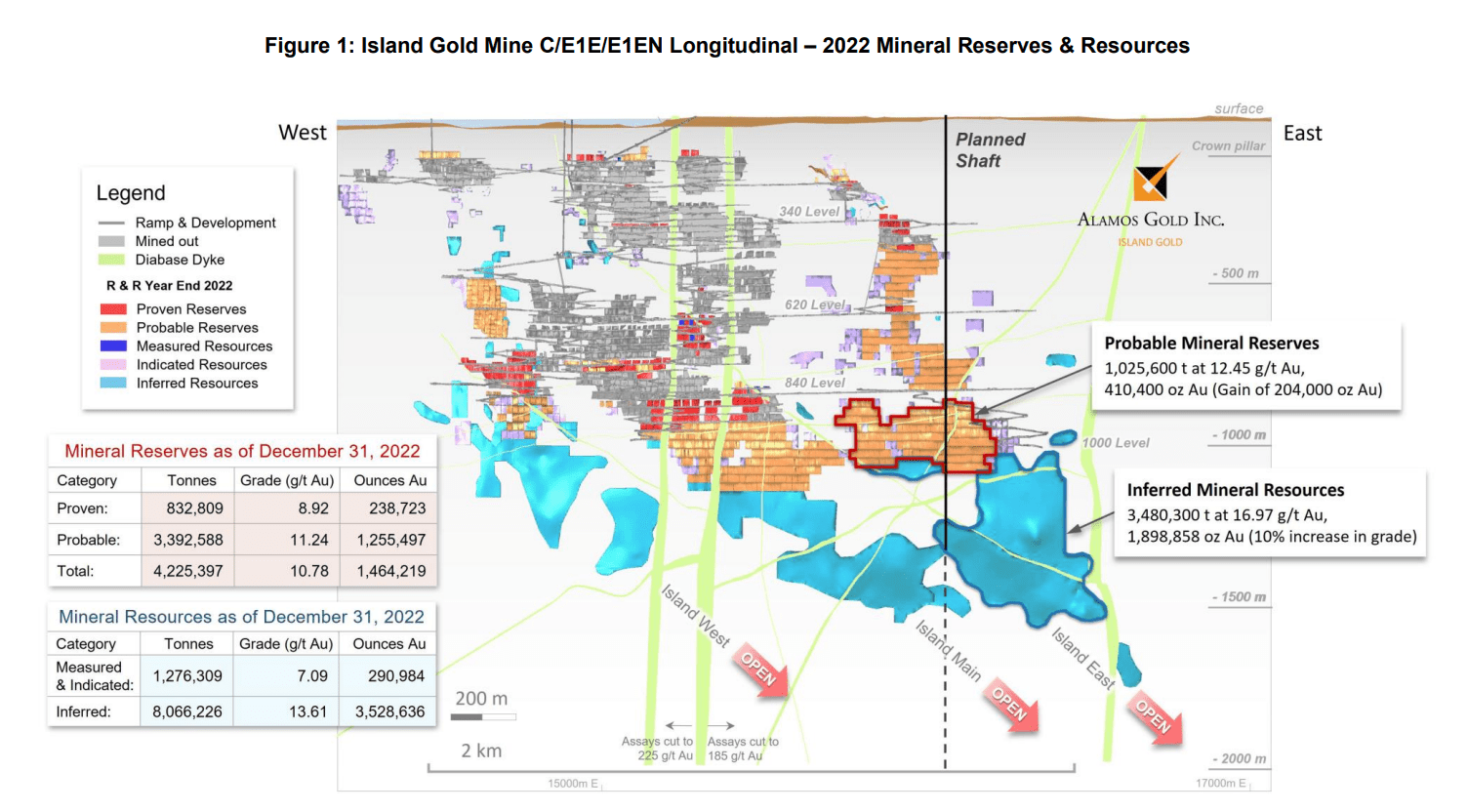

Digging into the company's most important asset given its growth profile (P3+ Expansion to increase production to ~300,000 ounces at sub $700/oz all-in sustaining costs), Alamos continues to knock it out of the park in regards to exploration success. In fact, Island's total resource base (reserves + M&I ounces + inferred ounces) has grown to ~5.28 million ounces at year-end 2022, translating to just shy of 200% growth since the Richmont Mines acquisition in 2017. Just as impressively, this was the 10th consecutive year of reserve growth at Island (helped by conversion of resources in Island East, Main, and West), and the 10th consecutive year of global mineral reserve growth for Alamos, underpinned by steady additions at Island Gold (reserves up 457,000 ounces since 2018). However, it's not just ounces that have been increasing at Island, it's also grades, making this one of the highest-grade assets globally and what will likely be Canada's lowest-cost gold mine once the P3+ Expansion is complete.

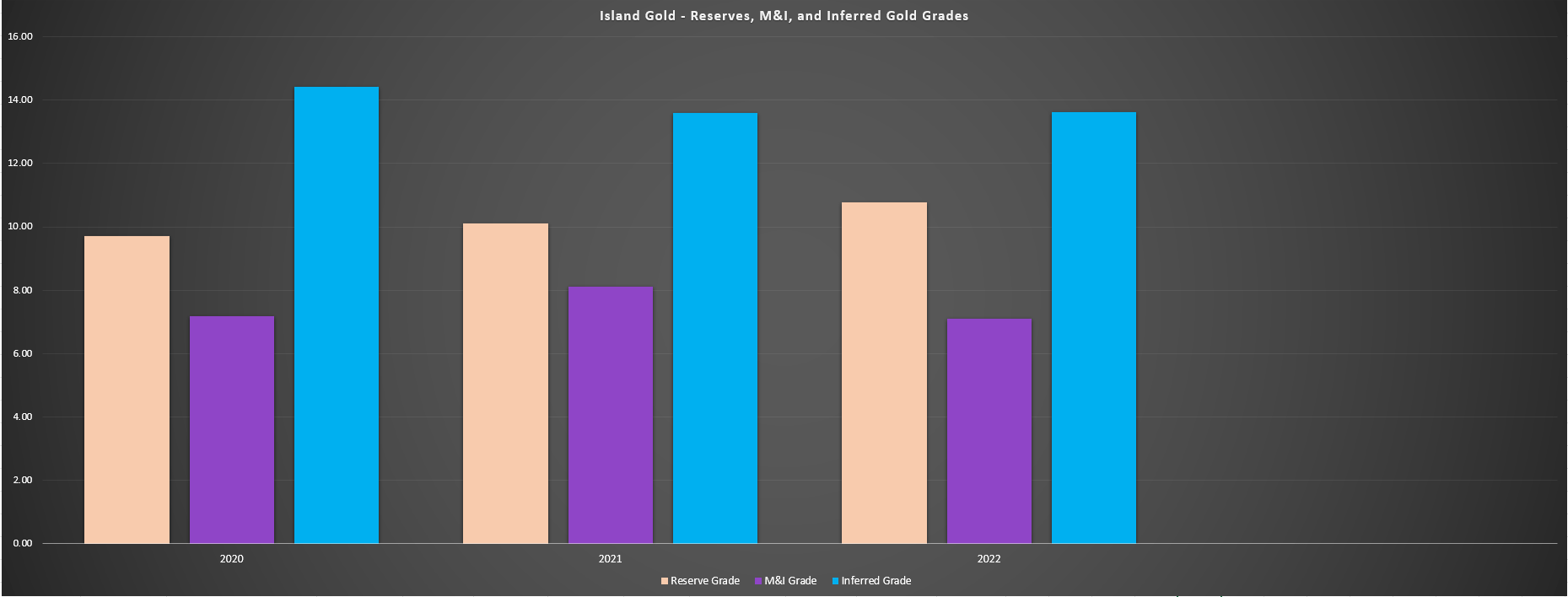

Island Gold - Reserves & Resources (Company Filings, Author's Chart)

{kind=link}

Looking at the chart below, reserve grades have improved from 9.71 grams per tonne of gold to 10.78 grams per tonne of gold since year-end 2020, and although inferred grades have dropped slightly (13.61 grams per tonne of gold vs. 14.43 grams per tonne of gold), the inferred resource base has increased 10% in the period to ~3.53 million ounces of gold, backing up an already significant ~1.76 million ounces between reserves and measured & indicated resources. And while Island Gold is one of the top-10 highest-grade gold mines globally by reserve grade, there's an argument that reserve grades could continue to improve with ~1.9 million ounces at 16.97 grams per tonne of gold of inferred resources in Island East directly below a proven & probable resource block of ~410,000 ounces at 12.45 grams per tonne of gold, and this area remains open laterally and down-plunge. Just as importantly, these resources are situated right next to the planned shaft, providing easy access to these ultra high-grade ounces once the P3+ Expansion is complete.

Island Gold - Reserve, M&I & Inferred Gold Grades (Company Filings, Author's Chart) Island Gold Reserves & Resources (Company Website)

{kind=link}

{kind=link}

Reserves Per Share

Reserve growth is important, but far more important is reserve growth per share. This is because reserve growth that comes at the expense of significant share dilution means that investors are getting exposure to fewer ounces of gold per share held. The result? One is actually seeing their exposure to precious metals diluted by owning any precious metals producer that cannot maintain reserves per share. Therefore, an investor in any producer with this criterion is not getting their desired leverage to the silver and or gold price if reserves and or production per share are declining.

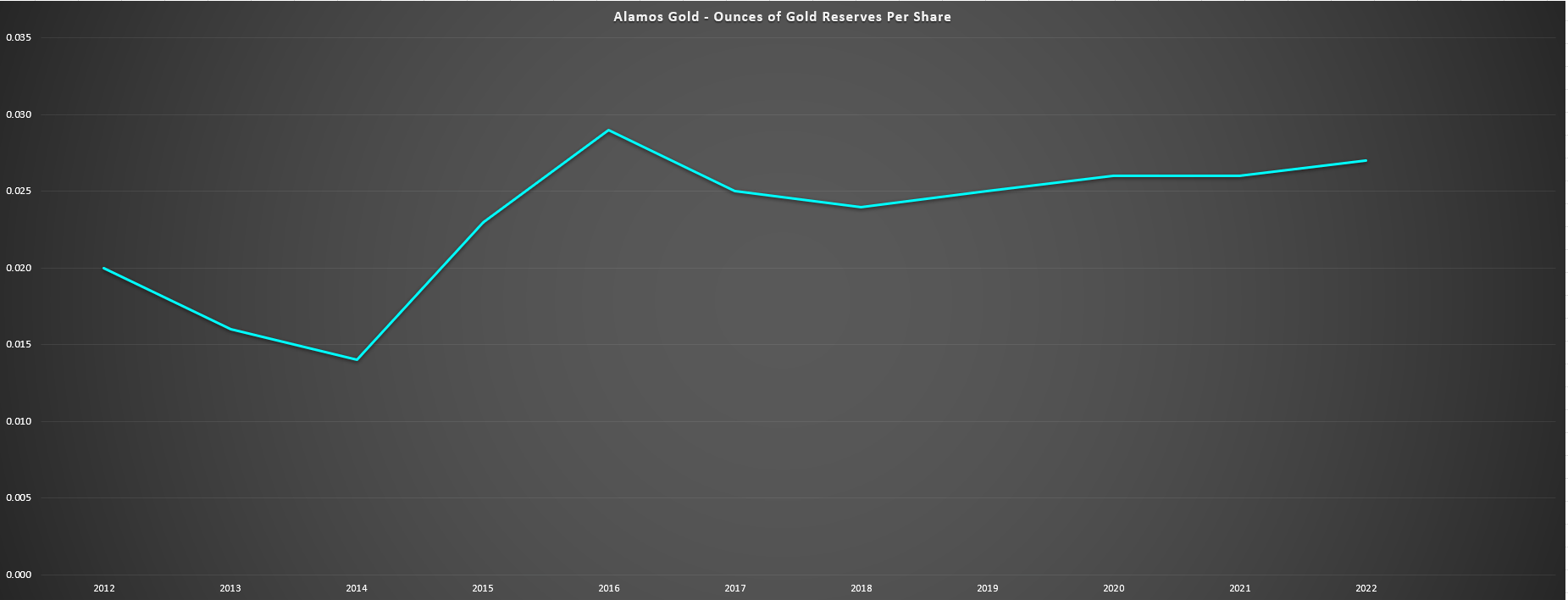

Obviously, this isn't ideal, since it makes little sense to own a producer that carries higher volatility and risk vs. a commodity (the metal itself) if it is not offering the leverage that one should get for taking on this added risk. However, there are exceptions in the sector, and Alamos Gold is one of them. In fact, as shown below, Alamos has increased reserves per share by ~40% over the past decade, which is even more impressive given that the gold price has provided no real help. Plus, with a 90% conversion rate on inferred ounces to reserves since the acquisition at Island Gold, and an inferred resource inventory of ~3.5 million ounces of gold, the current ounces of gold reserves per share chart does not do Alamos Gold justice.

Alamos Gold - Ounces of Gold Reserves Per Share (Company Filings, Author's Chart)

{kind=link}

For example, even if we were to assume that Island Gold's reserve base grows to just 2.8 million ounces vs. 1.46 million ounces today at year-end 2026 with successful resource conversion partially offset by mining depletion and assuming a share count of ~398 million shares and a combined 400,000 ounce decline in reserves across other assets from depletion, Alamos' reserves per share would hit a new high of ~11.5 million ounces. Meanwhile, reserves per share held would hit a new high of 0.029, translating to another 10% growth from current levels (45%+ growth from 2012 levels). These per share metrics are world class for a company with a depleting business model, and I would expect this trend to continue to improve over time as Island Gold is the gift that keeps on giving, and Lynn Lake has a massive land package (58,000 hectares) that's been on the back burner with the focus over the past several years being on the Lower Mine Expansion at Young-Davidson, resource growth at operating assets, and now the Island Gold P3+ Expansion.

Alamos' exceptional per share growth metrics can be attributed to the team's extreme capital discipline, which is so rare in this sector, with not only a counter-cyclical approach to M&A that has helped to build a portfolio of high-quality assets in Tier-1 jurisdictions, but also opportunistic share buybacks at the right price that have helped claw back any issued shares any further. This is the complete opposite of what we've seen from some other companies, with Kinross (KGC) coming to mind, paying a combined $9.7 billion for Aurelian (Fruta Del Norte), Red Back (Chirano, Tasiast), and Great Bear (Dixie). Today, just one of these assets is producing for Kinross, it sold another for a song, and one likely won't reach commercial production until 2030. If we compare this to Alamos and its most productive future mine, Island Gold, it has paid ~$750 million in acquisition and royalty acquisition costs, and this asset has an After-Tax NPV (5%) of over $2.0 billion even after 800,000 ounces of mining depletion.

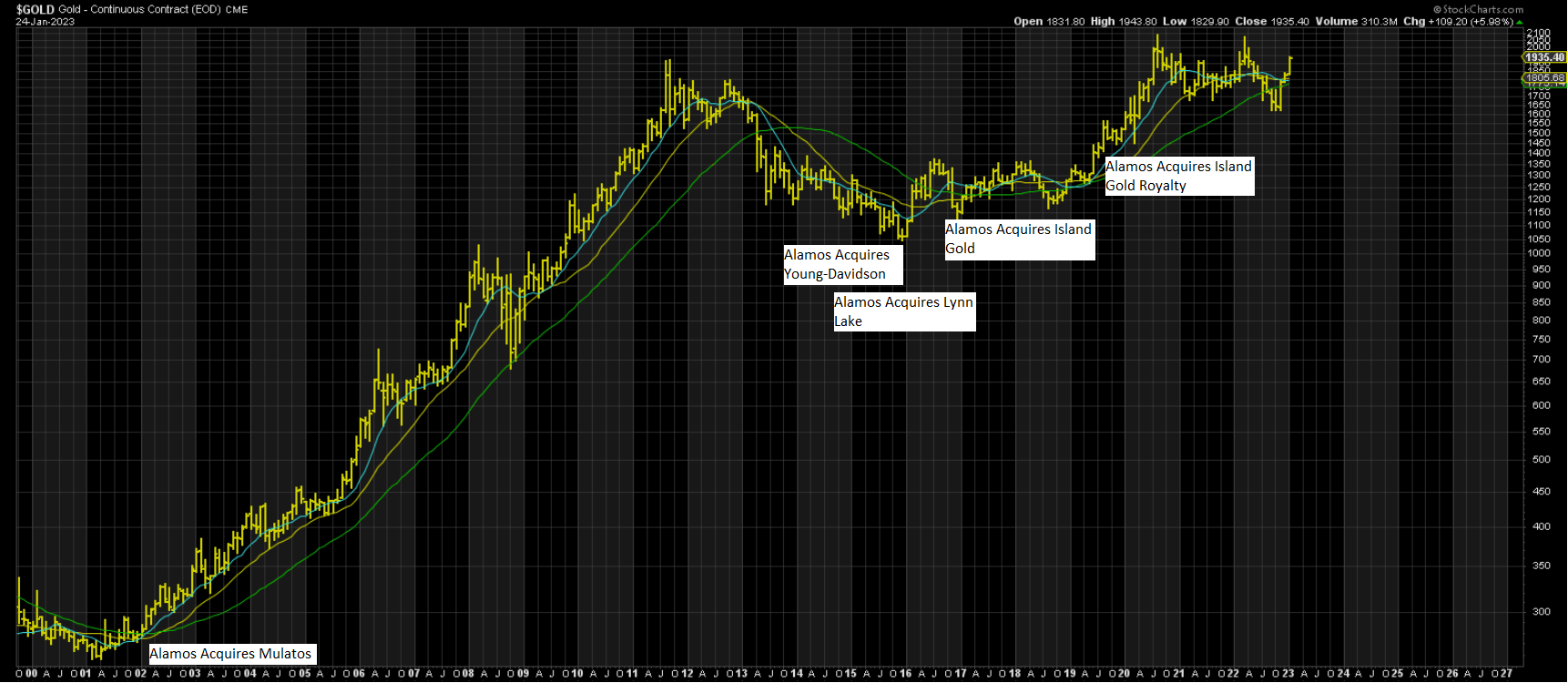

Alamos Gold Major Acquisitions vs. Gold Price (StockCharts.com, Author's Notes)

{kind=link}

And just as importantly, Alamos has been very careful with major acquisitions to ensure they were in the right jurisdictions and on high-quality assets, decreasing the probability of having to take write-downs in the future. That has been evidenced by adding Young-Davidson, Lynn Lake, and Island Gold over the past decade, all assets in Canada with above average grades, or in Young-Davidson's case, a highly profitable bulk mineable underground operation to make up for its lower underground grades. And this is arguably just as important as the price paid because it doesn't matter how great an asset is if it can't be moved into production and must be sold or takes over a decade to do so and collects dust in the time being, lowering the return on invested capital. Examples (among many others) include Fruta Del Norte (Aurelian) under Kinross and Eldorado's ~$2.5 billion deal for Stratoni, Olympias, Certej and Skouries.

The result is that investors have been conditioned after more than a decade of poorly timed and failed deals to fear any potential M&A on the horizon in miners they own (that might be suitors) and some may look to avoid some miners where M&A could be more likely due to depleting reserves at key assets. However, Alamos is one of only a handful of names that has done a phenomenal job acquiring assets at the right time to allow for material growth in production, reserves, and net asset value per share, as evidenced by the chart shared above. Hence, while some miners are proverbial hot potatoes that must be handled carefully as one never knows when a negative surprise is coming, Alamos is arguably the gold standard sector-wide for allocating capital, making it a "sleep-well-at-night miner" and a unicorn in a sector of mediocre companies on balance that can be comfortably bought on sharp pullbacks and held long-term.

Recent Developments

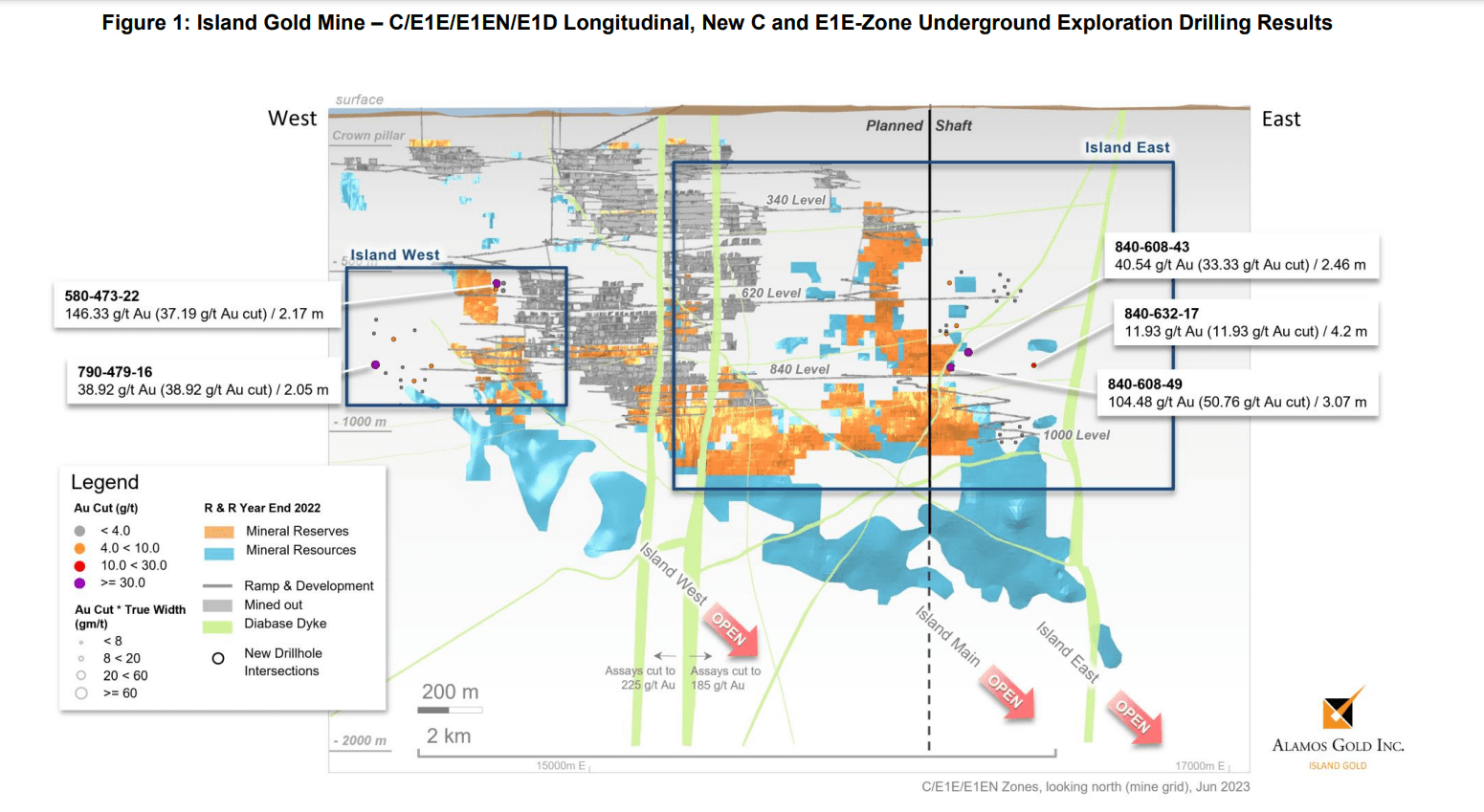

Moving over to recent developments, Alamos has continued to release high-grade results from PDA (Mulatos) and Island, where it's undergoing a major expansion with planned shaft sinking in Q4 of this year. In this update, we'll focus on the continued exploration success at Island Gold in several zones. For starters, Alamos reported two highlight intercepts which included 2.2 meters at 146.33 grams per tonne of gold and 2.1 meters at 38.92 grams per tonne of gold in Island West. The second intercept (2.05 meters at 38.92 grams per tonne of gold) was drilled over 200 meters west of the nearest reserve blocks, just outside of existing infrastructure. Meanwhile, the first intercept was drilled just east of current reserve blocks and directly beside existing infrastructure, with grades well in excess of its average reserve grade (146.33 grams per tonne of gold or 37.19 grams per tonne of gold cut). These results are quite exciting, but they're not the only highlights from Island West.

Island Gold Mine - Drilling Highlights (Company Presentation)

{kind=link}

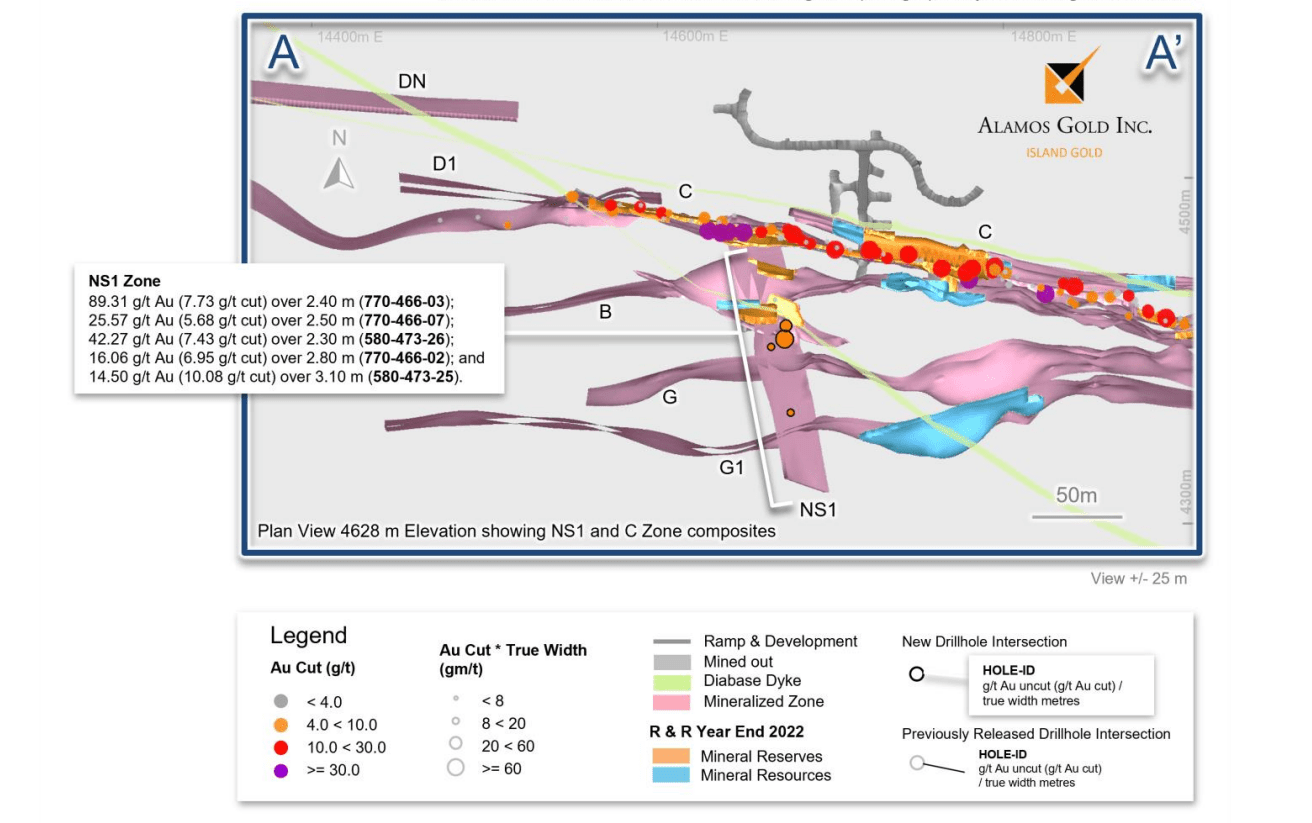

In addition to high-grade results in the main C Zone, Alamos hit multiple high-grade intercepts within sub-parallel zones in the hanging wall, and the company noted that it hit a "newly defined perpendicular structure, the NS1 Zone". Highlight intercepts in this new zone include 2.40 meters at 89.31 grams per tonne of gold, 2.50 meters at 25.57 grams per tonne of gold, 2.30 meters at 42.27 grams per tonne of gold, 2.80 meters at 16.06 grams per tonne of gold and 3.1 meters at 14.50 grams per tonne of gold. Elsewhere, Alamos also intersected high-grade mineralization in the G1 Zone (2.50 meters at 60.03 grams per tonne of gold), and in in the Island West Footwall Zones, with a newly defined sub-parallel structure, the DN Zone, yielding a hit of 2.90 meters at 22.34 grams per tonne of gold. Between extensions to existing reserves and newly defined structures, this points to further reserve growth at Island Gold in close proximity to existing infrastructure and allow for greater ounces per vertical meter.

NS1 Zone Intercepts & Minrealized Zones (Company Website)

{kind=link}

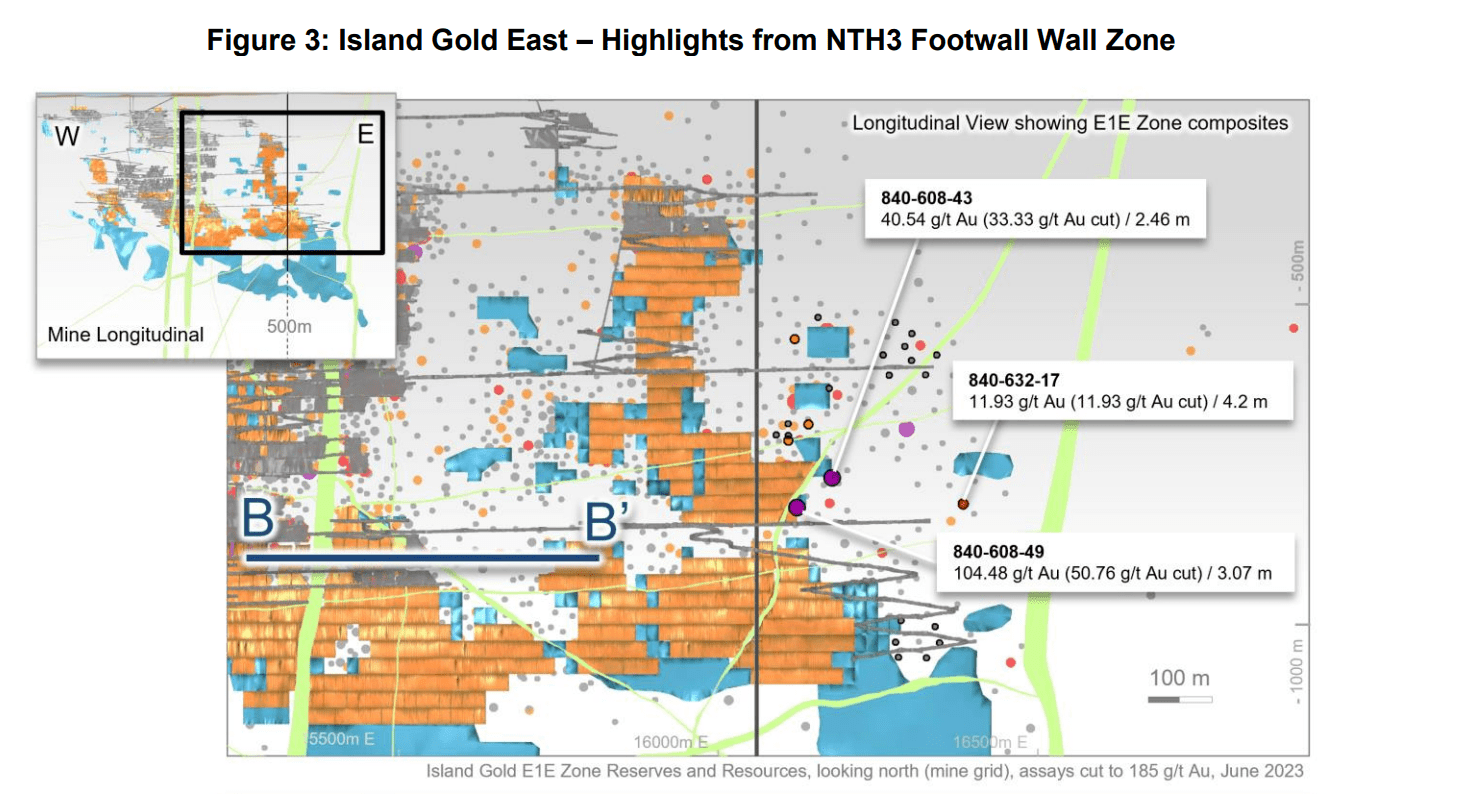

Elsewhere, in an area where Island Gold has released some monster hits in past years, including 21.33 meters of 71.21 grams per tonne of gold (MH25-08, albeit deeper in the mine), Alamos reported several solid intercepts in the E1E-Zone, with high-grade mineralization outside of existing reserves with intersections that included:

- 3.10 meters at 104.48 grams per tonne of gold

- 2.50 meters at 40.54 grams per tonne of gold

- 4.20 meters at 11.93 grams per tonne of gold

As shown below, these intercepts were east of existing reserves and came in at above average grades relative to its current reserve base. However, this wasn't the extent of drilling success in Island East, with the company also reporting high-grade intercepts from the footwall from the 620 and 840 levels in Island East, with sub-parallel structures built upon here as well. Structures identified to date include the NTH, NTH2 and NTH3 Zones (40 meters, 90 meters, and 75 meters north of the main E1E-Zone, respectively), with some of the better intercepts including 3.10 meters at 44.48 grams per tonne of gold (NTH2 Zone), 2.10 meters at 17.90 grams per tonne of gold (NTH2 Zone), and 2.70 meters at 13.21 grams per tonne of gold (NTH3 Zone). Finally, in areas where Alamos has yet to establish geometry and continuity (hanging wall and footwall), the company hit several high-grade intercepts with the best three being 4.70 meters at 137.20 grams per tonne of gold (footwall), 4.20 meters at 18.39 grams per tonne of gold (footwall), and 3.70 meters at 55.29 grams per tonne of gold (hanging wall).

Island Gold East - Drill Highlights (Company Website)

{kind=link}

Overall, I see the seemingly never-ending stream of high-grade drill results from Island Gold across multiple zones as very encouraging, with this emboldening the view of this being a mine that could remain in production into the late 2040s. And just as importantly, the growth in high-grade resources near existing infrastructure could add the company to pull forward additional high-grade ounces, augmenting an already impressive mine plan at Island. This is a major differentiator vs. most other high-grade underground assets that have lower visibility into future production past 2030 and are seeing steadily declining reserve grades, such as Yaramoko held by Fortuna ( FSM ), Seabee held by SSR Mining ( SSRM ), Deflector Underground held by Silver Lake ( SVLKF ) and Fosterville and Macassa held by Agnico Eagle ( AEM ).

And while this doesn't take away from the latter two being exceptional assets, Alamos has continued to grow Island's reserves with lots left in the tank (inferred resource base at even higher grades), with Island's reserves up from 1.31 million ounces at 9.71 grams per tonne of gold to 1.46 million ounces at 10.78 grams per tonne in the same period that we've seen Macassa's reserves decline to 1.91 million ounces at 15.11 grams per tonne of gold vs. 2.36 million ounces at 22.1 grams per tonne. Hence, while Alamos is one of a kind in its ability to grow reserves and net asset value per share consistently even in a flat gold price environment (2012-2022), its Island Gold Mine is just as incredible, with it continuing to grow its reserve base and reserve grades simultaneously net of mined depletion.

Q2 Earnings

Alamos Gold reports its earnings next week on July 26th after market close and consensus estimates are for $250 million in revenue and $0.12 in quarterly earnings per share. The company has beat earnings estimates in its last three quarters and also beat revenue estimates in its most recent quarter, helped by the stronger than expected average realized gold price and a very solid production quarter (~128,400 ounces), with Alamos tracking at ~26.2% of its annual guidance midpoint (490,000 ounces) heading into Q2 and set to benefit from another quarter of elevated gold prices, with most producers reporting an average realized gold price of $1,965/oz or higher, 4% above the $1,896/oz reported in Q1 2023.

Summary

Alamos Gold successfully replaced reserves yet again at year-end 2022, with 2% growth in gold reserves year-over-year to ~10.5 million ounces combined with a lift in overall grades to 1.63 grams per tonne of gold (+52% since 2012). However, while impressive, it was the growth outside of reserves that was just as important and the continued ability to uncover new future mines at Mulatos, with PDA now looking like the next asset that will keep Mulatos in production well into the 2030s. Elsewhere, Island Gold's resources outside of reserves now total nearly 4.0 million ounces even after resource conversion, and Lynn Lake (a project in reserves that hasn't contributed production yet) has been further de-risked for production later this decade following a positive Decision Statement by the Minister of Environment & Climate Change Canada, and Environment Act Licenses from the Province of Manitoba.

Island Gold Mineralization (Company Presentation)

{kind=link}

Putting this all together, Alamos already has one of the longest averaged weighted mine lives sector-wide with ~86% of net asset value in a Tier-1 mining jurisdiction (Canada), which justifies a premium multiple, but the pieces are in place for this to continue given continued exploration success. And with an incredible 90% conversion rate at Island and a dirt-cheap $14/oz discovery cost since acquisition, especially considering sub $700/oz all-in sustaining costs post-2025, Alamos is not reliant on M&A to grow and has a path to 75% production growth looking out to the end of this decade if Lynn Lake is brought into production, with the unique setup of having growth, margin expansion, and a higher proportion of ounces coming from Tier-1 jurisdiction assets. So, with AGI continuing to execute near flawlessly and owning of the best assets sector-wide (Island Gold), I continue to see it as a top-3 gold producer and a name worthy of scooping up on sharp pullbacks.

For further details see:

Alamos Gold: Another Year Of Successful Reserve Replacement