AGI - Alamos Gold Q2 Earnings: Firing On All Cylinders

2023-07-30 08:39:59 ET

Summary

- Alamos Gold reported record quarterly gold production of ~136,000 ounces, with a strong performance from its Mulatos Complex.

- The company achieved industry-leading all-in sustaining costs of $894/oz at Mulatos and was one of the few companies to report lower cash costs and AISC year-over-year despite inflationary pressures.

- Given Alamos' strong track record of per share growth and recent exploration success combined with its ability to consistent over-deliver on promises, I would view sharp pullbacks as buying opportunities.

The Q2 Earnings Season for the Gold Miners Index ( GDX ) began last week and while it's been a rocky start, Alamos Gold ( AGI ) was certainly one exception. Not only did the mid-tier producer post multiple records, but it's heading into H2 well positioned to deliver at or above its guidance midpoint helped by a massive start to the year at its Mulatos Complex, and despite a slow start to 2023 at Island Gold. Even more impressively, Alamos reported the highest sector-wide among producers that have already reported at $866/oz, and it managed this despite moderate headwinds, and all-in sustaining costs [AISC] would have been even lower if it had not sold ~3% fewer ounces than it produced. These results are nothing short of exceptional, and with assays pending from a promising drill hit at Pine Breccia (Island Gold) and a gold price that has logged a record 20 consecutive weeks above $1,900/oz, it should be an exciting (and very profitable) finish to the year for the company.

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q2 Production & Sales

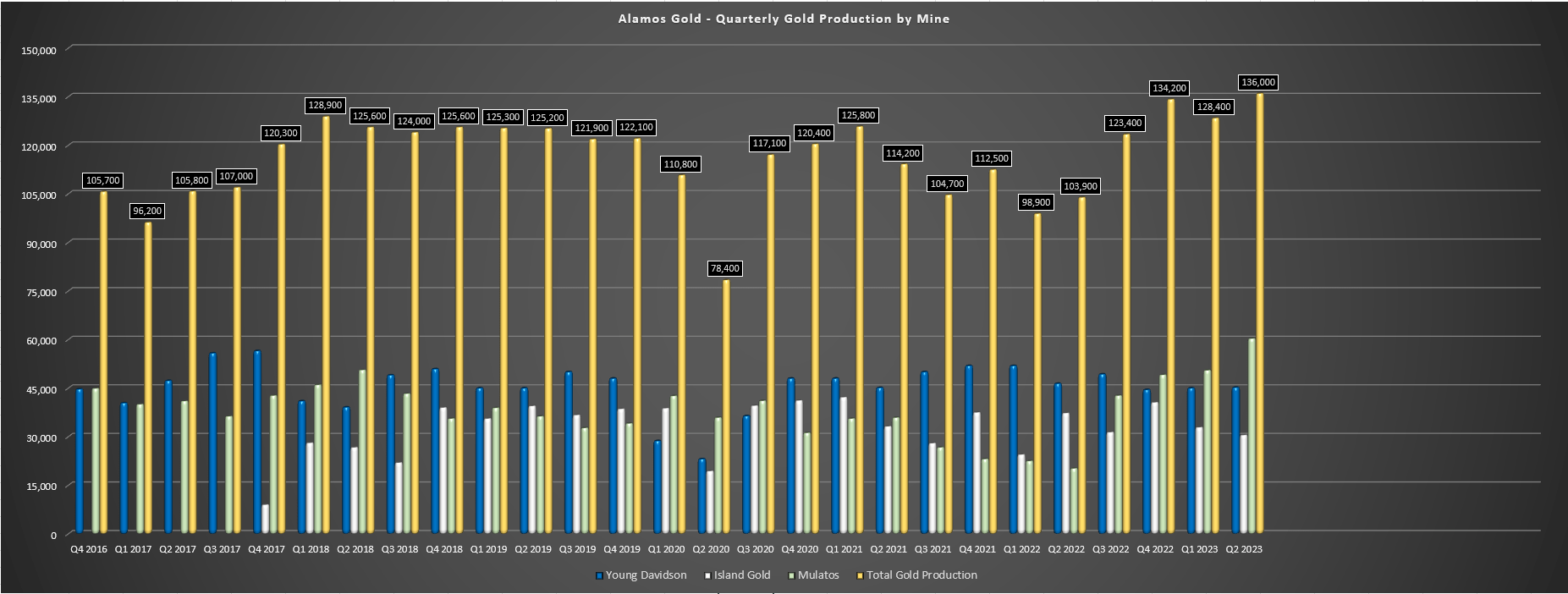

Alamos Gold released its Q2 results last week, maintaining its momentum after a solid Q1 with a record quarter for the company across several metrics. This included record quarterly gold production of ~136,000 ounces, aided by a monster quarter from Mulatos with ~60,300 ounces of gold produced, the best quarter for the asset since Q2 2018. This more than offset a softer quarter from Young-Davidson and Island Gold year-over-year with lower throughput and grades, with both assets affected by weather-related power outages and wildfires in Northern Ontario. And given this impressive production in H1 (~264,400 ounces), Alamos Gold is on pace to meet (and potentially beat) its FY2023 guidance midpoint of 500,000 ounces despite what will be a softer H2 from Mulatos with the cessation of mining at El Salto and a dip in grades at its new La Yaqui Grande Mine.

Alamos Gold - Quarterly Gold Production by Mine (Company Filings, Author's Chart)

{kind=link}

Digging into the results at Mulatos a little closer, the Mexican Mining Complex reported industry-leading all-in sustaining costs of $894/oz in the period, a significant improvement from $1,636/oz in Q2 2022 during a softer quarter for production. The significantly higher production was related to an increase in tonnes stacked at La Yaqui Grande, with ~1.01 million tonnes stacked at 1.52 grams per tonne of gold, up from ~333,200 tonnes at similar grades in the year-ago period, with stacking rates were above design capacity at ~11,000 tonnes per day. Meanwhile, at the Mulatos Pit, Alamos stacked ~1.42 million tonnes at 1.10 grams per tonne of gold, a slight drop in tonnes stacked but at significantly higher grades year-over-year. The result of this phenomenal quarter was the best performance in a decade for output and free cash flow for the asset, with $47.0 million in Q2 mine-site free cash flow and $83.8 million year-to-date.

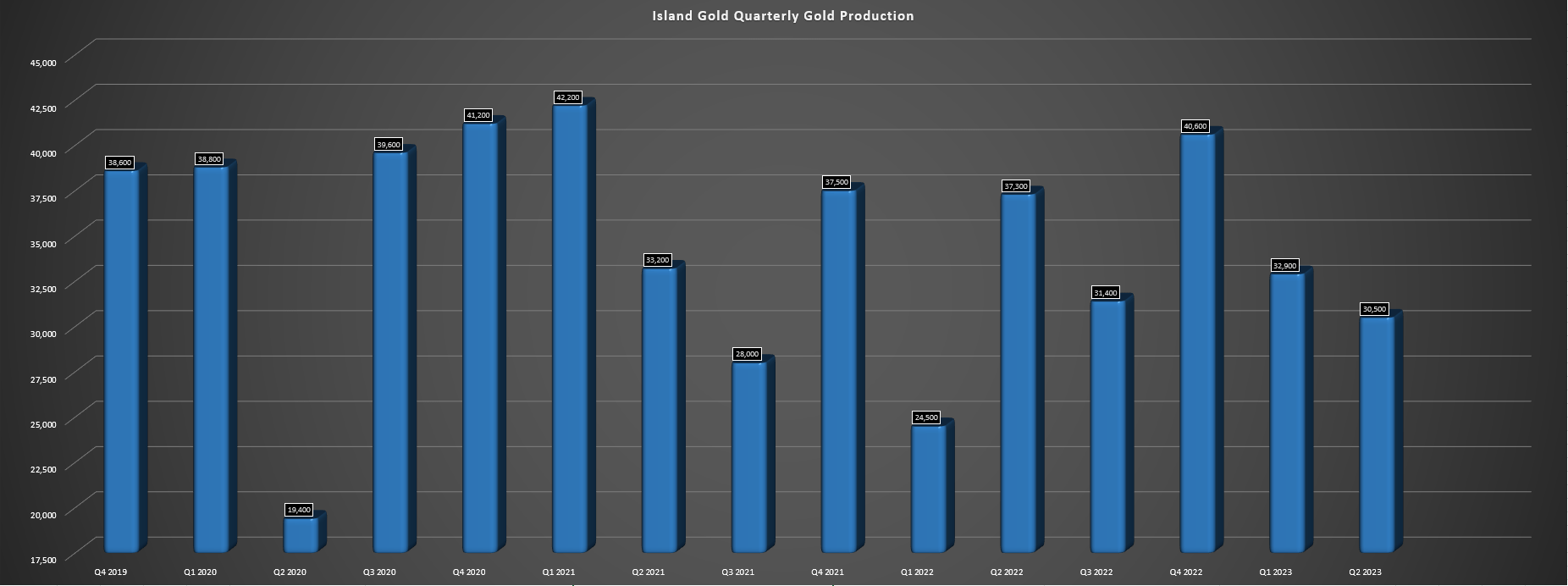

Island Gold - Quarterly Production (Company Filings, Author's Chart)

{kind=link}

Looking at Alamos' Island Gold Mine, the asset produced ~30,500 ounces of gold in Q2, down from ~37,500 ounces in the year-ago period. The lower output was related to fewer ore tonnes mined (unplanned downtime due to smoke from wildfires), lower grades (9.51 grams per tonne of gold vs. 10.09 grams per tonne of gold) and lower processing rates related to maintenance on the fine ore bin and weather-related power outages. Combined with higher sustaining capital in the period ($11.0 million vs. $9.5 million), all-in sustaining costs crept up to $1,072/oz (Q2 2022: $848/oz). That said, even with the weaker quarter, Island Gold only saw moderately negative mine-site free cash outflows of $4.5 million despite significant growth capital spend in the period ($40.7 million vs. $15.7 million).

As of quarter-end, Alamos Gold noted that 36% of the $756 million budget had been spent or committed at Island Gold, and over 90% of buried services required to begin shaft sinking are complete. This has set the company up to begin shaft sinking in Q4 of this year, and Alamos is positioned well financially to finance this growth, with positive company-wide free cash flow, ~$190 million in cash, and ~$690 million in total liquidity ($500 million undrawn RCF). As for the second half production at Island Gold, sustaining capital should come in at similar levels and the company will benefit from increased mining rates (resulting in higher production rates), which should translate to a lower cost in H2 at the mine from a unit cost standpoint. And while Q2 all-in sustaining costs were up at $1,072/oz, these costs are still over 20% below the industry average (~$1,350/oz).

{kind=link}

Finally, the company's flagship Young-Davidson Mine was also affected by minor headwinds in the period, with unplanned downtime due to weather-related power outages, translating to lower throughput of ~696,700 ounces. Combined with a lower grade profile (2.13 grams per tonne of gold vs. 2.25 grams per tonne of gold), production came in at ~45,200 ounces, down 2% year-over-year, and all-in sustaining costs increased to $1,212/oz, up from $1,087/oz in Q2 2022. The latter resulted from inflationary pressures and increased sustaining capital and much fewer ounces sold in the period (~43,600 ounces vs. ~46,700 ounces).

Fortunately, like Island Gold, Alamos expects to see better performance at Young-Davidson with higher throughput rates and grades, resulting in lower unit costs in the period. And despite unit costs that were above my expectations in Q2 at Young-Davidson, the asset still generated over $35.0 million in mine-site free cash flow. Plus, company-wide all-in sustaining costs are sitting at $1,144/oz, below the guidance midpoint, suggesting that with improved unit costs at its two Canadian operations, the company shouldn't have any issue meeting or beating its guidance midpoint for the year. Let's take a closer look at costs and margins below:

Costs & Margins

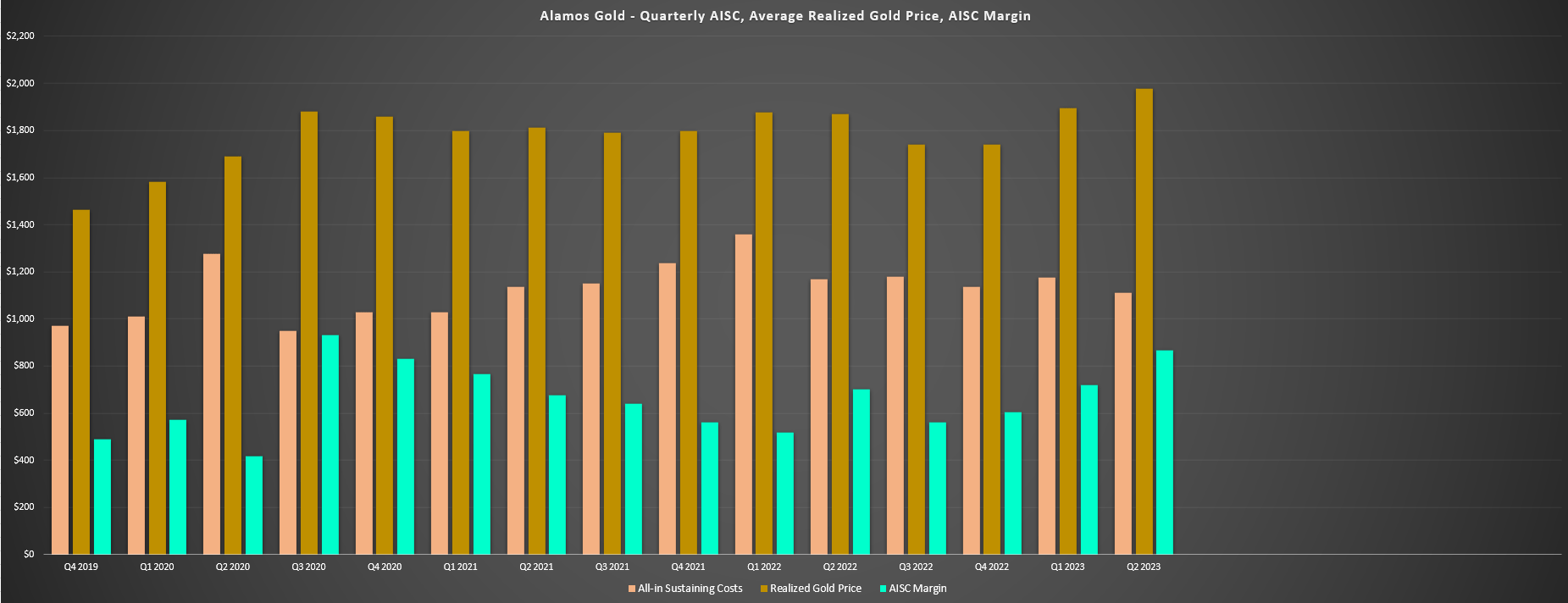

Looking at costs and margins, all-in sustaining costs came in at $1,112/oz in Q2 2023 (Q2 2022: $1,170/oz), with cash costs of $847/oz, with Alamos being one of the few producers to report lower costs on a year-over-year basis. While partially related to being up against easy year-over-year comps after a softer quarter at Mulatos in Q2 2022, this cost performance is still exceptional, with Alamos' costs ~17% below the industry average and its margins up over 20% year-over-year to $866/oz. This improvement in margins was driven by gold price strength, with Alamos reporting one of the highest average realized gold prices sector-wide at $1,978/oz, but also the lower cost profile because of the monster quarter at La Yaqui Grande and its Mulatos Complex. Also worth noting that with fewer ounces sold than produced, AISC would have come in below $1,080/oz if not for the lower sales, and the strong performance was despite higher sustaining capital year-over-year.

Alamos Gold - Quarterly AISC, Average Realized Gold Price, AISC Margin (Company Filings, Author's Chart)

{kind=link}

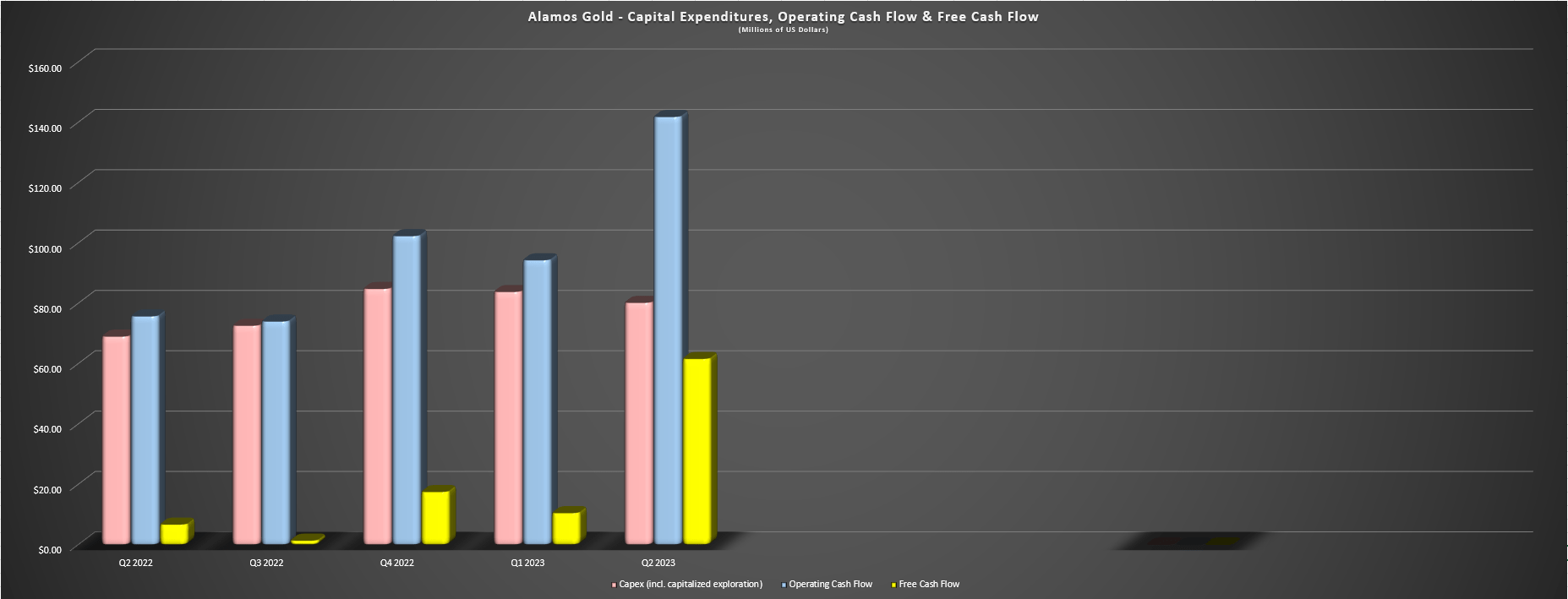

As for the company's financial results, Alamos reported operating cash flow of $141.8 million, and free cash flow of $61.6 million, with the latter representing a record for the company, though it did benefit from the collection of sales tax receivables that were delayed in Q1. This financial performance was even more impressive given that the company saw elevated capex in the period due to the start of major construction at its Island Gold P3+ Expansion Project, with capital expenditures of ~$80 million in Q2 2023. The result was that Alamos finished the quarter with a much stronger balance sheet, sitting on ~$190 million in net cash, which is a stronger financial position than many of the sector's largest gold companies, let alone mid-tier producers.

Alamos Gold - Quarterly Capex, Operating Cash Flow & Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

Recent Developments

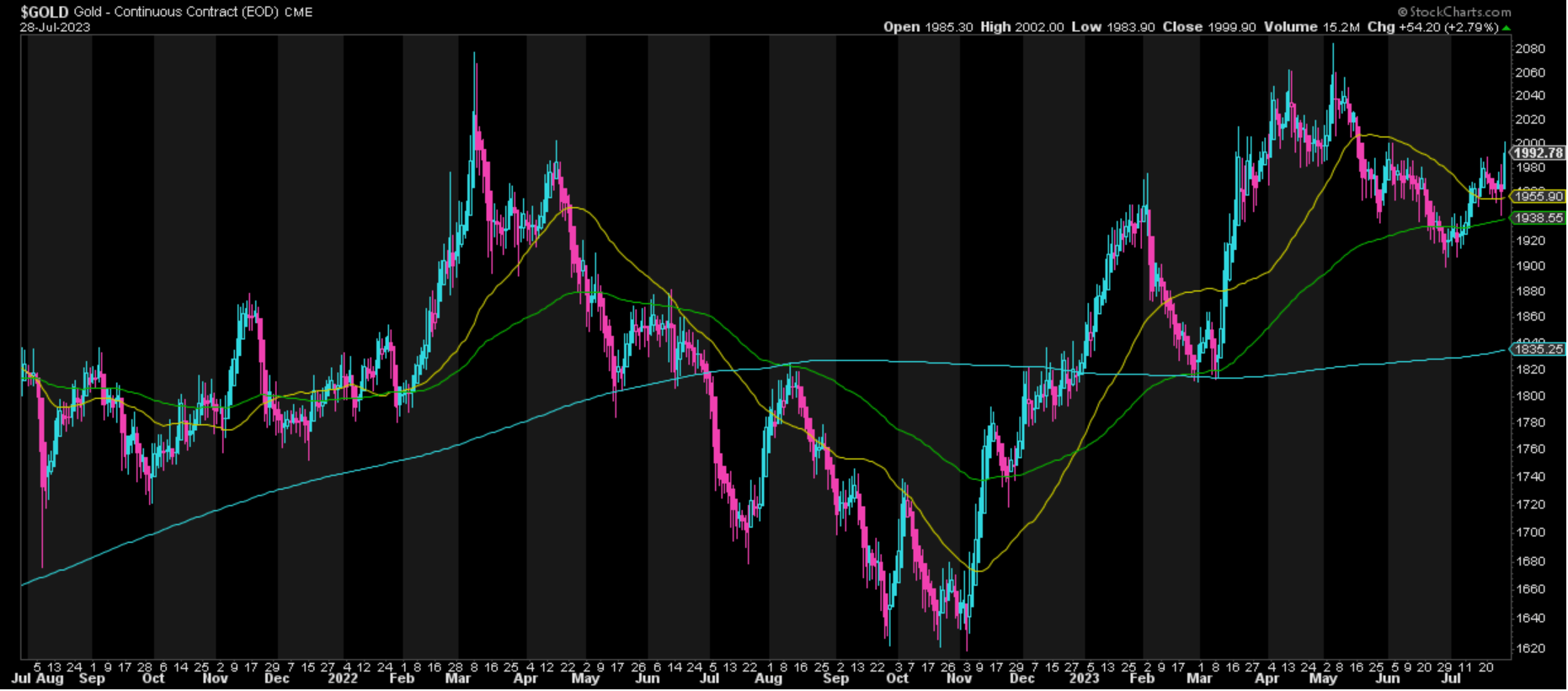

As for recent developments, the gold price has spent a record 20 weeks above the psychological $1,900/oz level and while it fell to finish Q2, it has rebounded and remains above $1,950/oz. This has set the sector and Alamos up for another strong quarter from a financial standpoint, with a quarter-to-date average realized gold price of ~$1,950/oz, assuming the gold price continues to cooperate. And while Mexican producers sector-wide will feel the pressure on costs from a rising Mexican Peso with collars in place at a minimum rate of 20.46 MXN/USD and a maximum rate of 22.66 MXN/USD. Therefore, the strength in the Peso that we've seen over the past couple of months won't spoil Alamos' profitability in H2, while other producers like Guanajuato Silver ( GSVRF ) will have a rough H2 due to 100% exposure to Mexico and all-in sustaining cost margins that are already razor-thin at ~10%.

{kind=link}

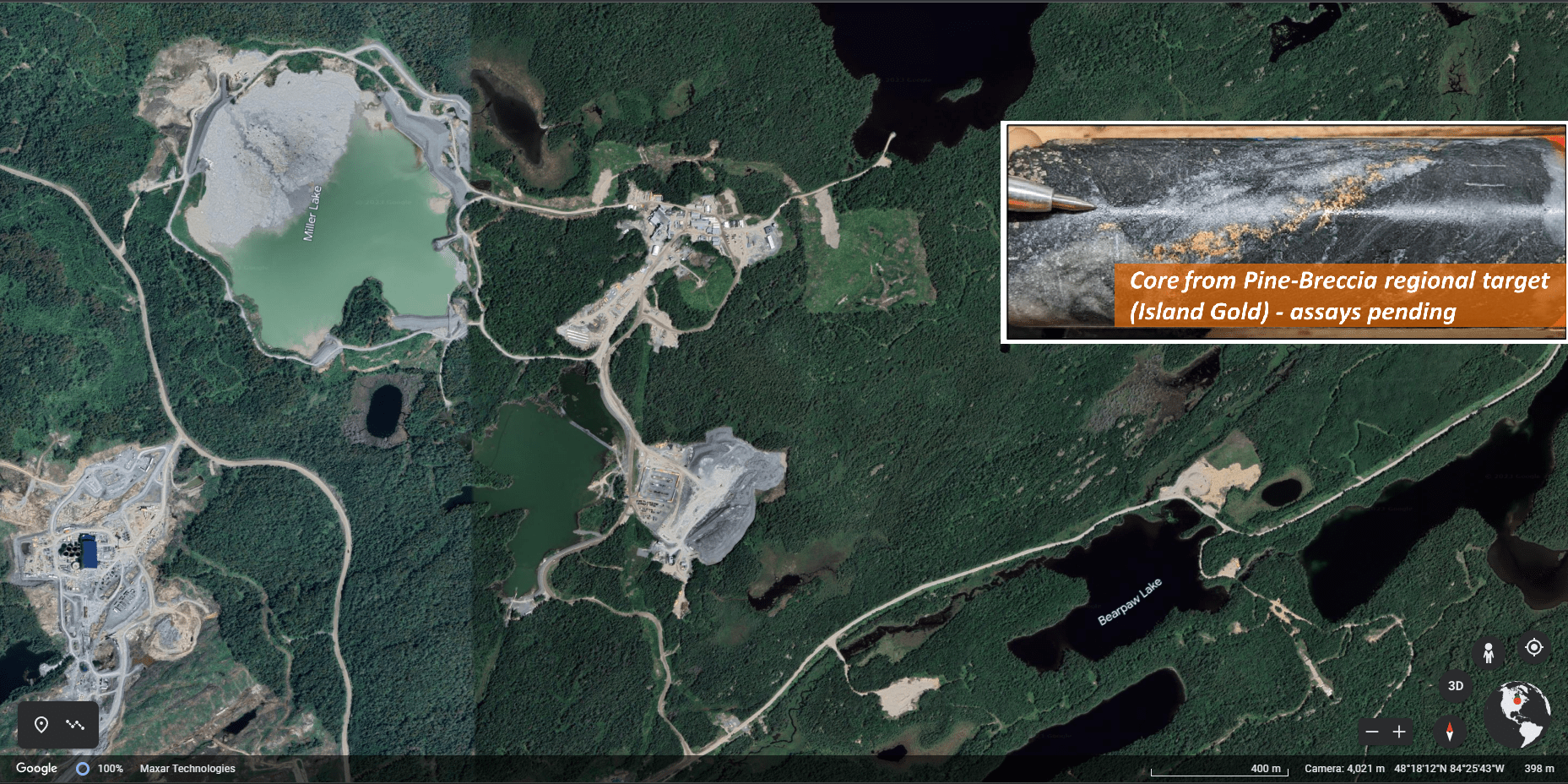

The other positive development worth noting (albeit assays are still pending) is that Alamos Gold pulled some very impressive-looking core (visible gold) out of a regional target at Pine-Breccia at its Island Gold Property, with the Pine-Breccia Target sitting 4 kilometers from the mill and northeast of Bearpaw Lake (shown below). As discussed in the 2022 TR, the Pine Zone is a folded sulphide-oxide iron formation which is part of the Goudreau Iron Range, while the Breccia Zone is a silicic fault breccia to quartz stockwork zone that can be traced several kilometers along the Maskinonge Lake Fault. Previous drilling hit 6.0 grams per tonne of gold over 1.0 meter, and while we don't know what this hole from Pine Breccia will intercept, the core is certainly encouraging and could represent a new target where Alamos could grow its already large 5.0+ million ounce resource base in close proximity to the Island Mill.

Island Gold Site Infrastructure, Bearpaw Lake & Core w/ Visible Gold from Pine-Breccia Target (Google Earth, Company Website)

{kind=link}

Summary

While we have seen a disappointing start to the Q2 Earnings Season with a few misses already reported, Alamos Gold ( AGI ) has been a clear exception, reporting record production, revenue, and free cash flow, similar to its larger Canadian peer, Agnico Eagle Mines ( AEM ). Notably, the record free cash flow was despite elevated growth capex with shaft site infrastructure (Island Gold P3+), and the record production was achieved with minimal help from Island Gold, which had a mediocre quarter in Q2 because of the impact of wildfires and slightly lower grades. And given the impressive start to the year despite minor headwinds, Alamos is on track to potentially beat its FY2023 guidance midpoint, tracking at ~52.9% of guidance and tracking slightly below on costs even with strength in the Mexican Peso.

Meanwhile, from a bigger picture standpoint, Alamos is now less than three years away (2026) from transforming into a larger producer with industry-leading costs (sub $950/oz) and a free cash flow machine, and exploration success has continued across its portfolio to provide strong visibility into production into the late 2030s. This graduation to the upper ranks of the mid-tier producer space with higher margins should allow the company to see multiple expansion, especially when combined with increased production from Tier-1 jurisdictions. And more importantly, AGI is one of the few producers consistently growing per share metrics with disciplined capital allocation to maintain a strong balance sheet. Given these rare attributes, I continue to see Alamos Gold as a top-5 gold producer and a name worthy of buying on sharp pullbacks.

For further details see:

Alamos Gold Q2 Earnings: Firing On All Cylinders