AGI:CC - Alamos Gold: Q3 Not A Blowout But Certainly Good Enough

2023-10-28 08:28:25 ET

Summary

- Alamos Gold has posted a solid third quarter.

- High expectations were met, and growth projects are progressing well.

- The market is rewarding the ongoing strong operational and financial performance.

Alamos Gold (AGI) reported Q3 results on October 25. We have listened to the earnings call , studied the MD&A and financial statements , and updated our charts. Here is a condensed tour of the latest data points, followed by our updated investment thesis for this gold miner.

Operations

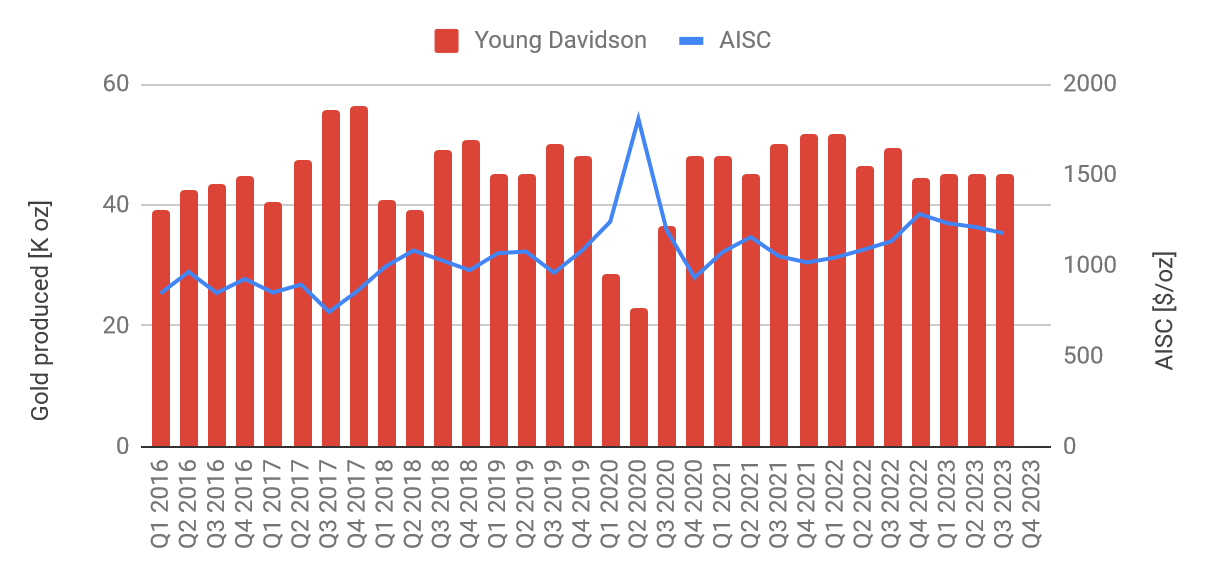

The Young Davidson mine posted another quarter of steady production. A slight drop in grade was compensated by a record amount of ore processed through the mill. Costs are bucking the trend at Young Davidson and have been trending down from a slight spike at the end of last year. All done and dusted, this was another solid quarter at this mine site.

Young Davidson gold production (company filings, author's work)

{kind=link}

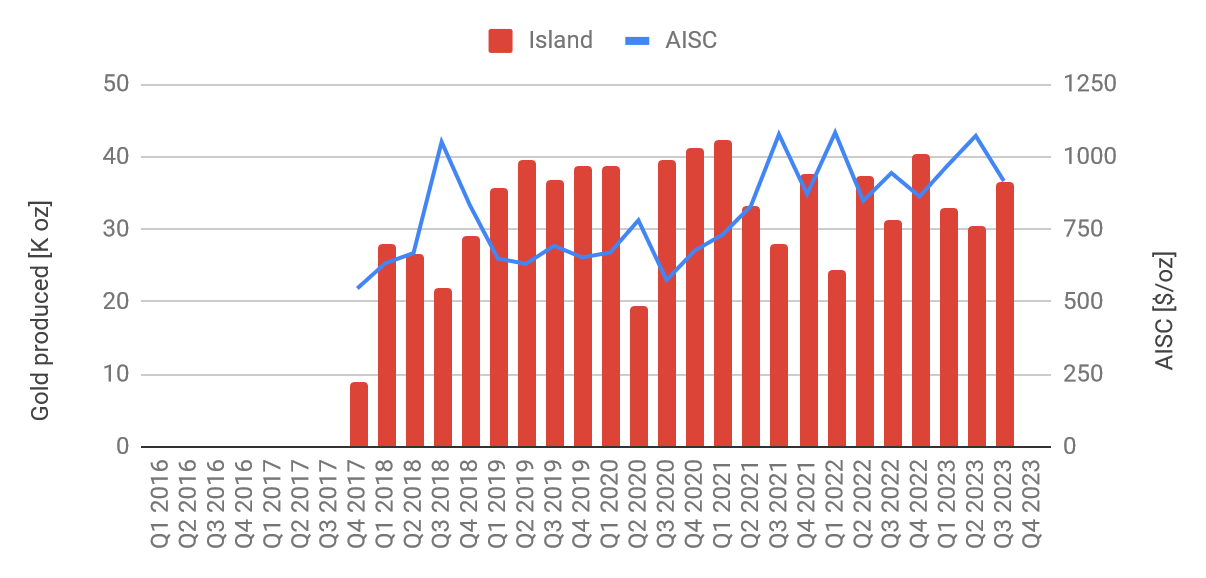

It was a similar story over at the Island gold mine. Gold production as well as costs were reported as guided. All this while the Phase III expansion project is taking shape with surface infrastructure well advanced, setting the scene for shaft sinking to commence before the end of the year.

Island gold production (company filings, author's work)

{kind=link}

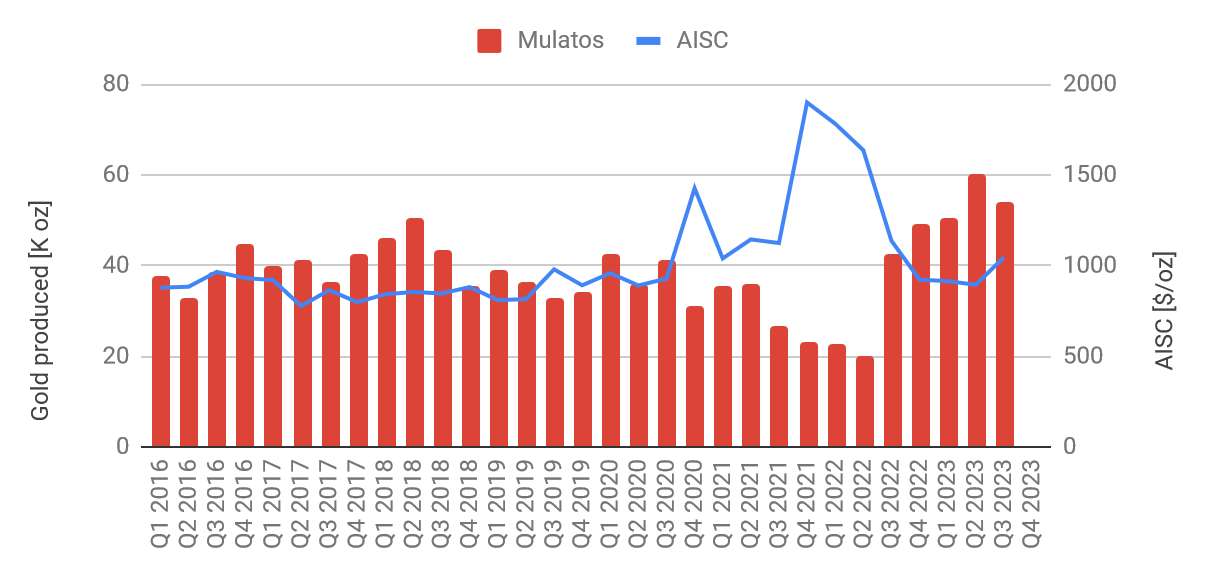

Operations at the Mexican Mulatos district took centerstage again in Q3. Production numbers did not quite match the record set in Q2, but gold output certainly remained strong. We also noted a small uptick in costs, associated with finalizing the transition of mining operations from the main pit to the La Yaqui Grande pit. Alamos processed plenty of stockpiled ore during Q3, which explains the comparatively low metallurgical recovery. Residual leaching from the Mulatos heap leach will continue to contribute for a few more quarters, but the bulk of gold production will come from La Yaqui Grande going forward.

Thanks to the highly successful transition to La Yaqui Grande Alamos increased its consolidated production guidance by 5%, aiming for the new range of 515,000 to 530,000 ounces in 2023.

Mulatos gold production (company filings, author's work)

{kind=link}

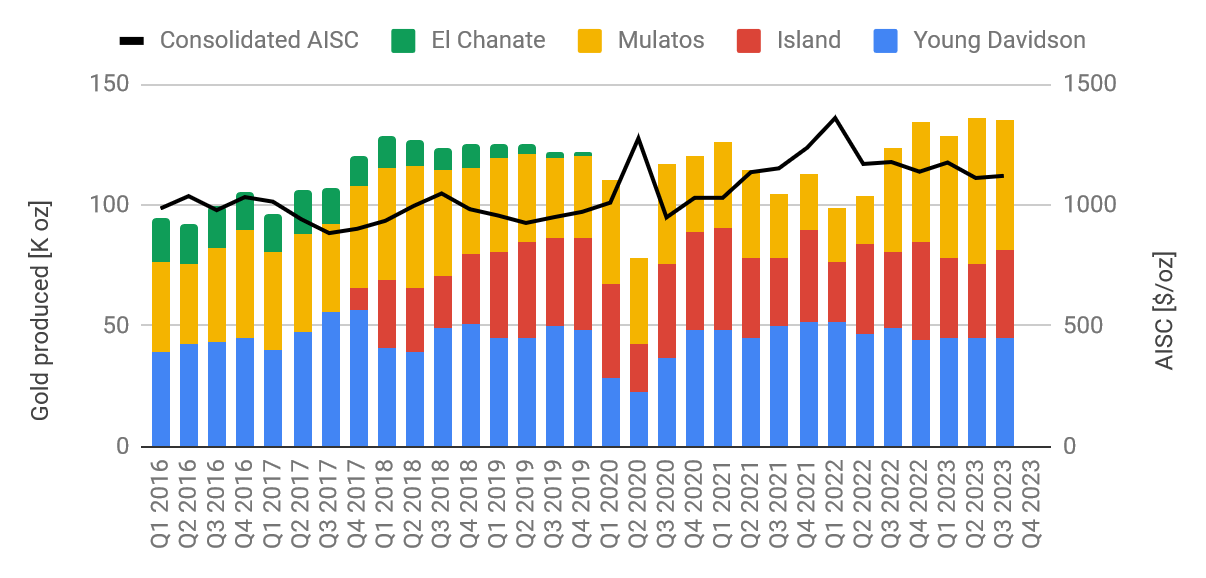

The consolidated gold production is shown in the chart below.

Consolidated gold production (company filings, author's work)

{kind=link}

Growth Projects

Alamos is pursuing three organic growth opportunities.

- We already mentioned the Phase III expansion at the Island Gold mine which has the highest priority, and will start to show its effects soon after the shaft is completed in 2025.

- At Mulatos, the company has expanded its exploration and development program thanks to ongoing success at the Puerto Del Aire discovery. This deposit will be mined from underground, accessed from a ramp and development drifts off the main Mulatos pit. A development plan for this deposit is scheduled for the ongoing Q4 and we expect a significant mine life extension for the Mulatos operations to be presented in this study.

- An updated feasibility study for the Lynn Lake development project was released in Q2. This study documented robust economics for an open pit project with a 17-year mine life. However, we don't quite see this project with a 17% IRR ranking on par with the producing assets within the company's portfolio. Hence we wonder if Alamos will indeed make a development decision for this project. For the moment, Alamos seems to be content with continuing exploration activities at this asset.

Financial Results

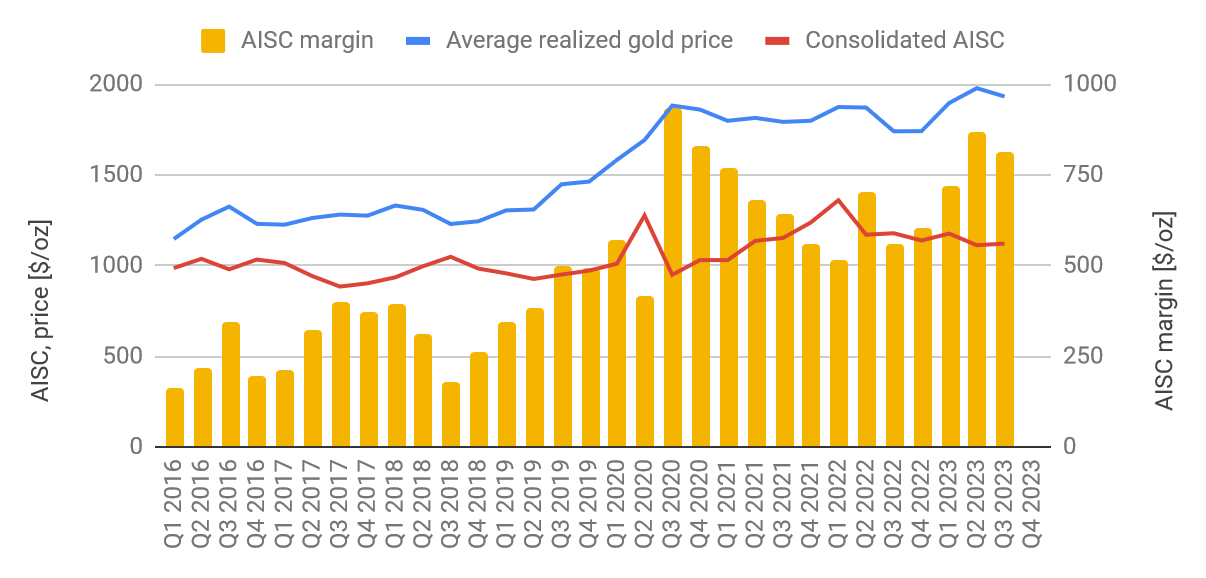

Outstanding cost control and a kind gold price environment have ensured ongoing strong margins in Q3.

Margins (company filings, author's work)

{kind=link}

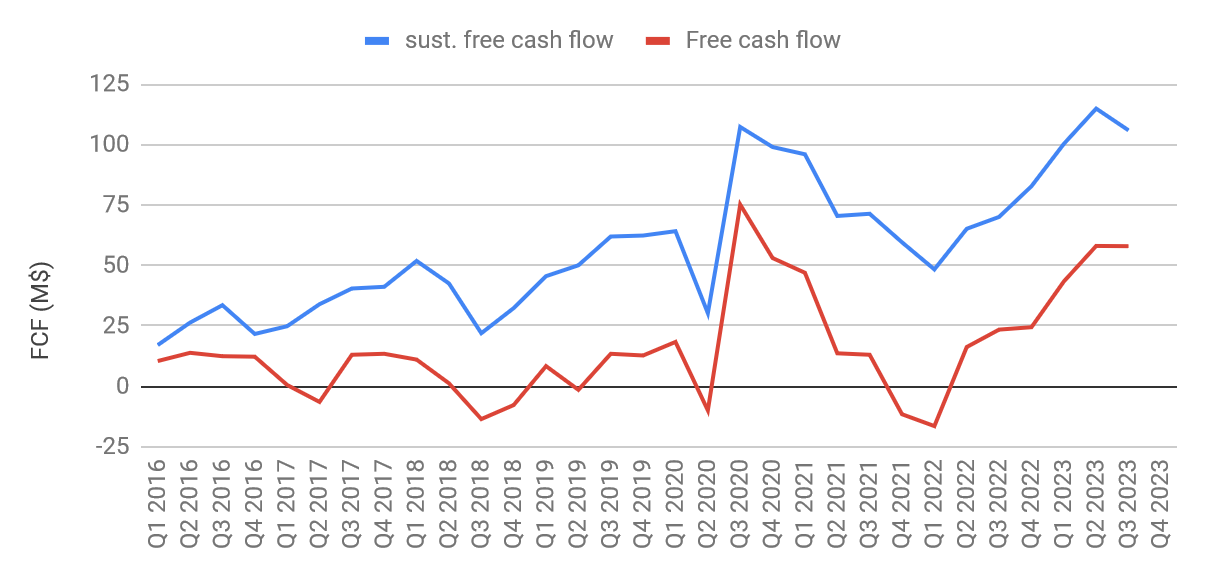

And with margins like those shown in the chart above it comes with little surprise that free cash flow generation was exceedingly strong again in Q3. The red line in the chart below shows free cash flow after paying for activities at the three growth projects discussed above; and the blue line shows free cash flow after netting out growth capital.

FCF (company filings, author's work)

{kind=link}

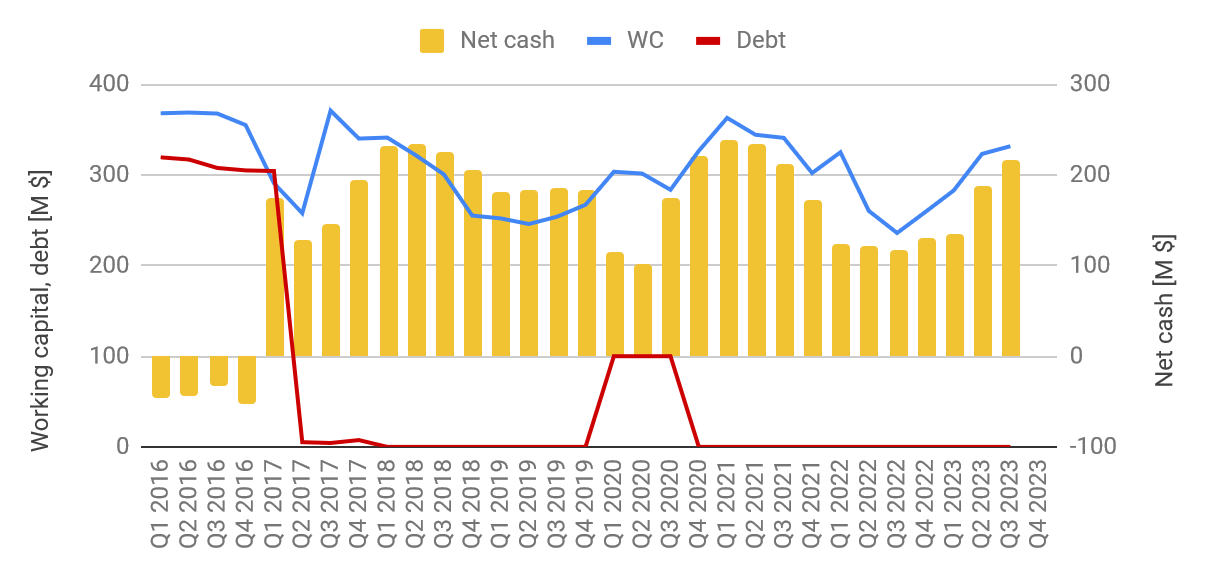

This in-flowing cash is building on the company's balance sheet. Alamos carries no debt, and the chart below illustrates the steady increase in net cash and working capital on the balance sheet. In fact, noting the $500M undrawn credit facility Alamos is building significant liquidity despite investing heavily in its growth projects and paying a dividend. And with a balance sheet like this, we wonder how long it will take until we see Alamos involved in some M&A activity.

Balance sheet (company filings, author's work)

{kind=link}

Valuation

For all the right reasons Alamos has developed into a market darling, and as a result, investors are prepared to pay a premium for the company. The company's share price has outperformed peers in all reasonable time frames.

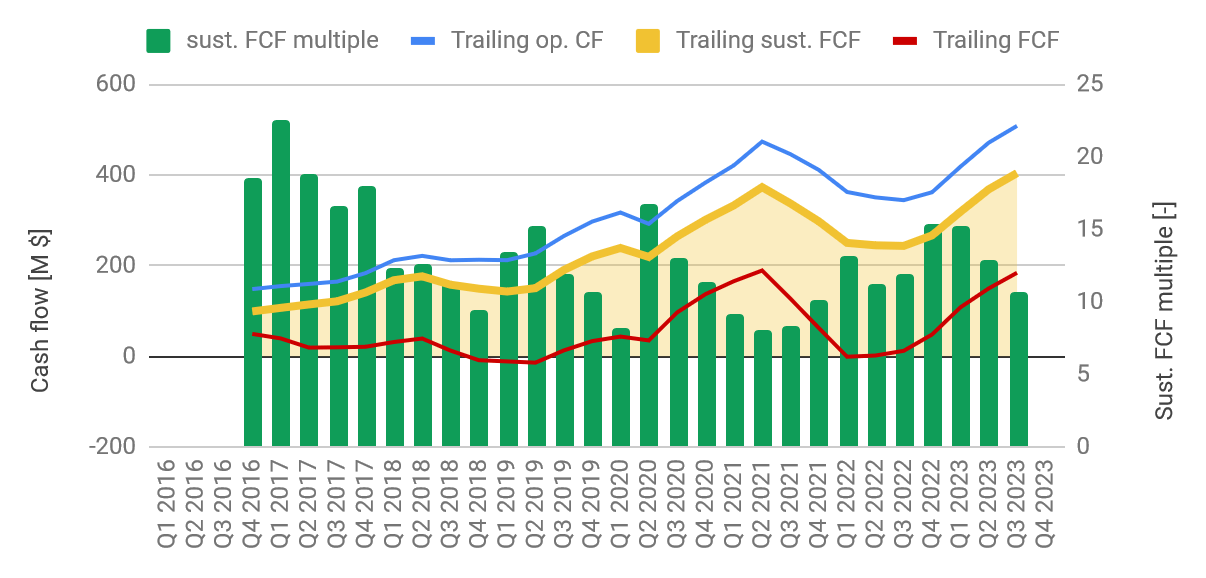

We submit that the market is gauging Alamos first and foremost based on its cash flow generation. We like to use sustaining cash flow as our measuring stick when computing cash flow multiples for companies with a strong growth profile. Traditionally, this multiple has oscillated between 10 and 15 over the past several years. At the end of Q3 it printed 10.7, but has risen to 12.5 at the time of writing, smack in the middle of the quoted range.

FCF multiple (company filings, author's work)

{kind=link}

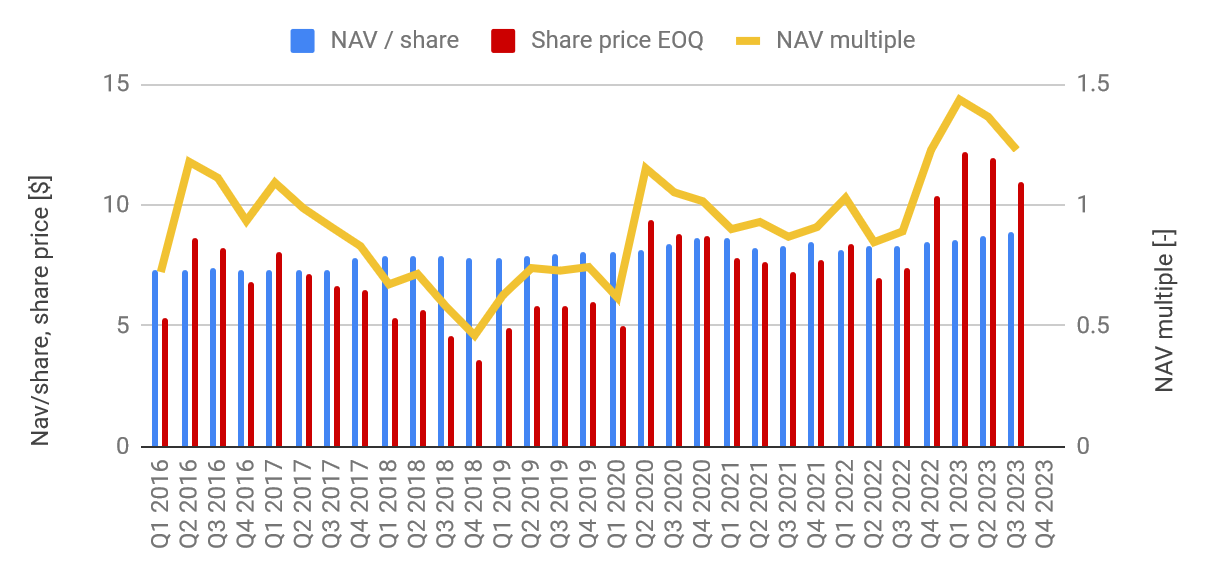

And while cash flow is king when it comes to the valuation of a producing miner, it pays to also keep an eye on the NAV multiple. The chart below illustrates how the company briefly traded at almost 1.5xNAV at the start of the year. This exuberant attitude had cooled off a bit by the end of Q3, but at the time of writing, shares were back trading at 1.44xNAV.

NAV multiple (company filings, author's work)

{kind=link}

Summary & Investment Thesis

Alamos Gold posted yet another solid quarter. Operations clearly delivered, allowing for a small production guidance increase; and the financial performance followed suit. The market recognizes the company's potential and investors seem prepared to pay a premium for the quality on display.

Shares were trading at $12.82 at the time of writing. This transfers in a cash flow multiple right in the middle of the typical range for Alamos Gold, and a NAV multiple towards the top of the typical range.

Absent a gold price rally the upside seems limited from here and we rate Alamos as a HOLD for now.

For further details see:

Alamos Gold: Q3 Not A Blowout, But Certainly Good Enough