ALRM - Alarm.com: A SaaS Story To Keep On The Radar

Summary

- Alarm.com is, relative to the global smart home market, a minor player with its 2.0% share.

- I believe that the company is slightly overvalued right now, but a SaaS model is historically associated with investors willing to pay more.

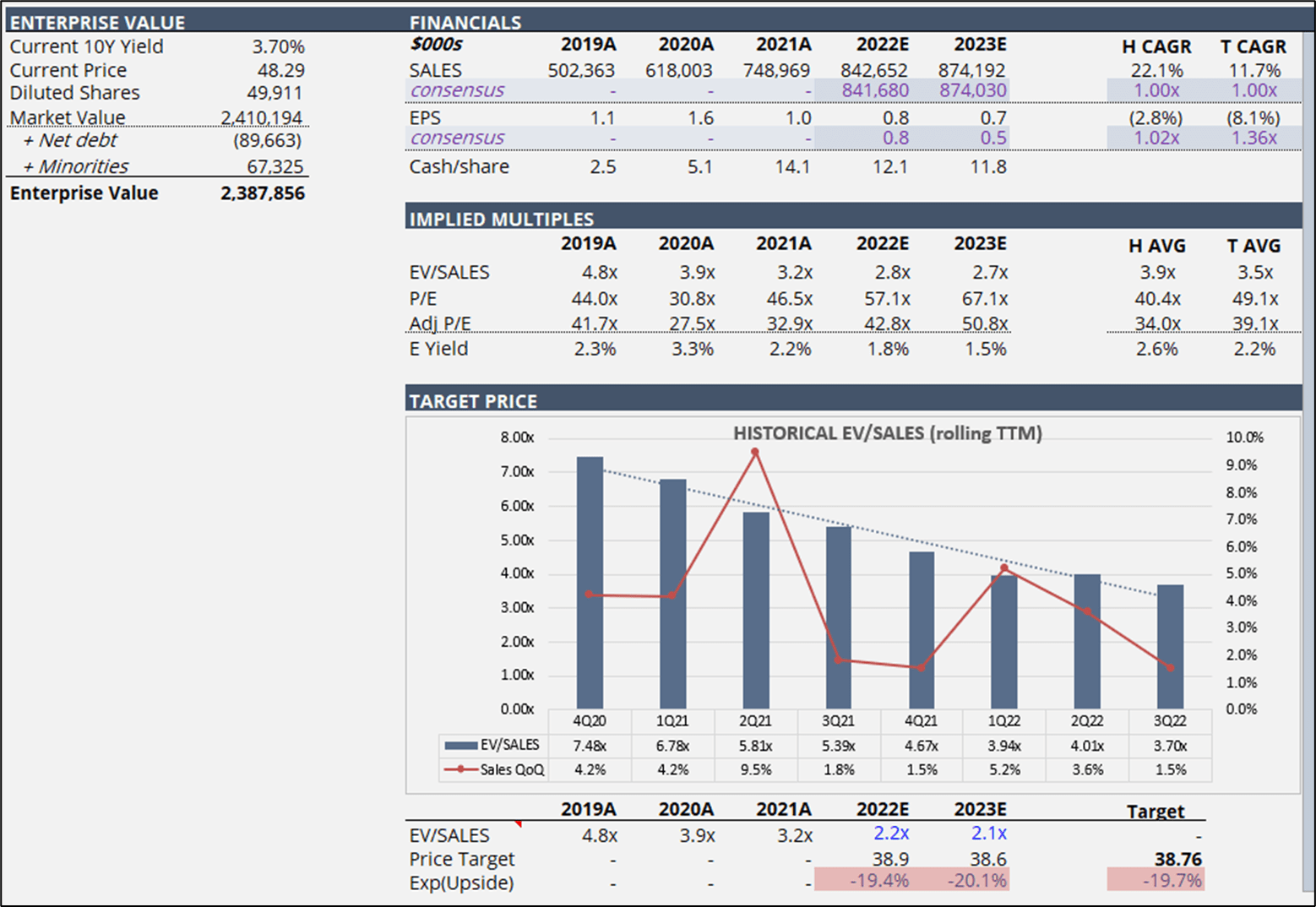

- I rate shares as HOLD with an estimated fair value of $38.76/share, which would represent a 19.7% downside from the current price of $48.29.

Description

Alarm.com (ALRM) (“the company”) is a middle-sized company providing, under a B2B2C business model, a platform that allows end-users an interactive way the management of an intelligently connected property. The company offers a portfolio of cloud-based solutions for smart residential and commercial properties, including interactive security, video monitoring, intelligent automation, access control, energy management, and wellness solutions.

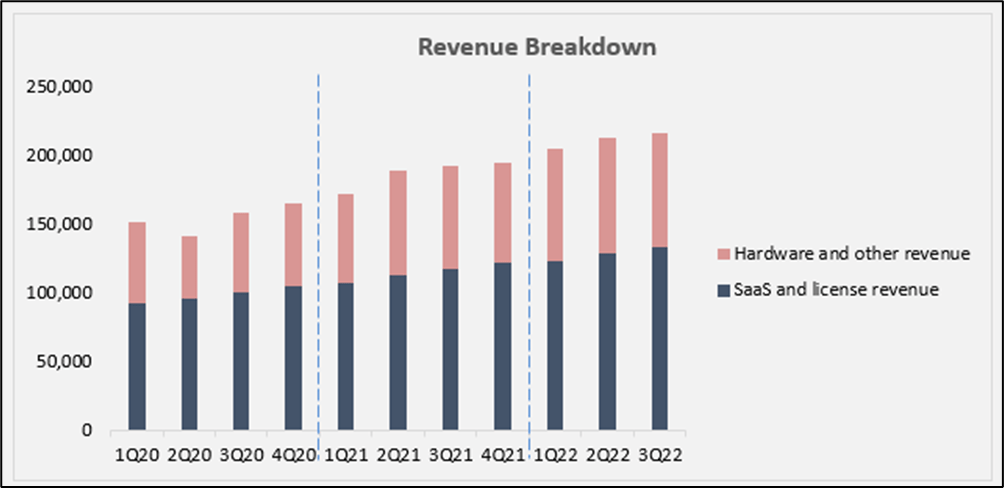

The company primarily generates SaaS and license revenue through its service provider partners, who resell these services and pay the company monthly fees, but also through hardware sales (e.g., video cameras, and gunshot detection sensors). Below, you can see how the company did recently.

{kind=link}

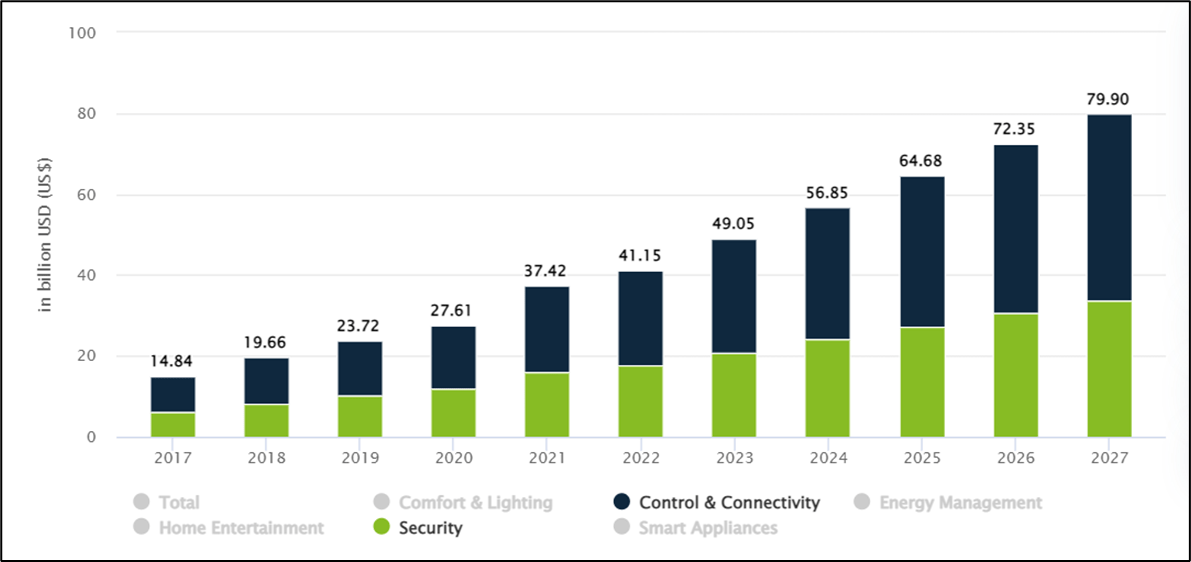

The Company is, relative to the global smart home market, a minor player with its 2.0% share. However, from 2017A to 2021A it expanded its market share from 1.59% to 2.0%.

In fact, while the overall market grew at a CAGR of 26.0% over the 2017A-2021A period, the company's revenue grew at a CAGR of 33.4% (1.29x the market's CAGR) over the same period. This is a positive trend that I expect to continue in the future driven by the growing consumer spending on smart home products and services.

{kind=link}

Company Valuation

Competition

The competition is represented by well-established companies like, for example, Amazon ( AMZN ) (e.g., ring products) and Google's (GOOG) ( GOOGL ) Nest which have the financial, and human resources but also a big client base to take a big bite at the company's market share.

Being of aware it, the company has invested heavily in R&D which resulted in 597 issued patents as of December 31, 2021, and numerous patent applications pending. This makes, in my opinion, the company "bulletproof" losing market share drastically and more likely of being acquired by a potential competitor.

Valuation

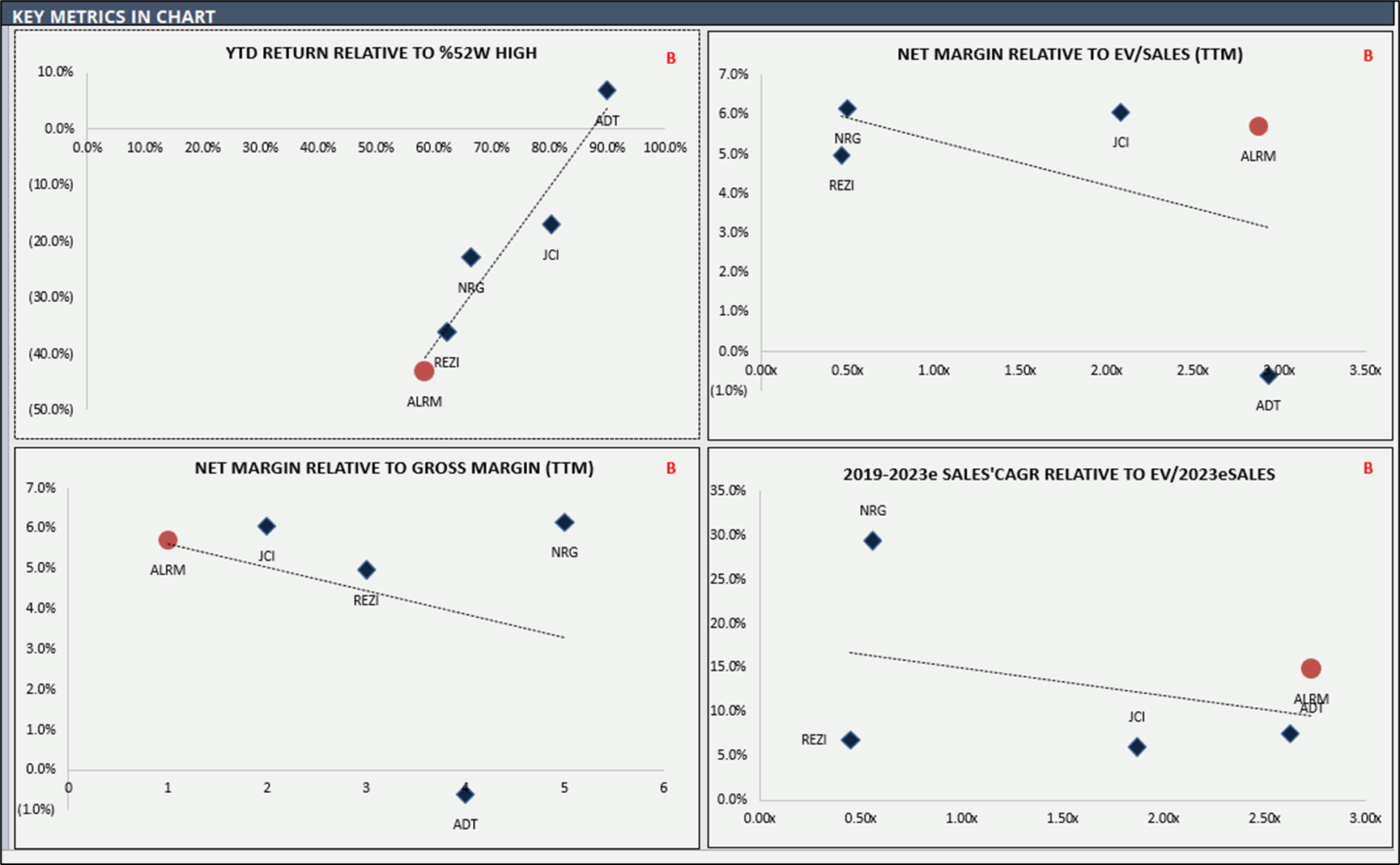

The company is trading at an EV/SALES of ~ 2.88x TTM, which represents a premium relative to the peers' median EV/SALES of ~ 2.08x TTM.

{kind=link}

I believe that the company is slightly overvalued right now.

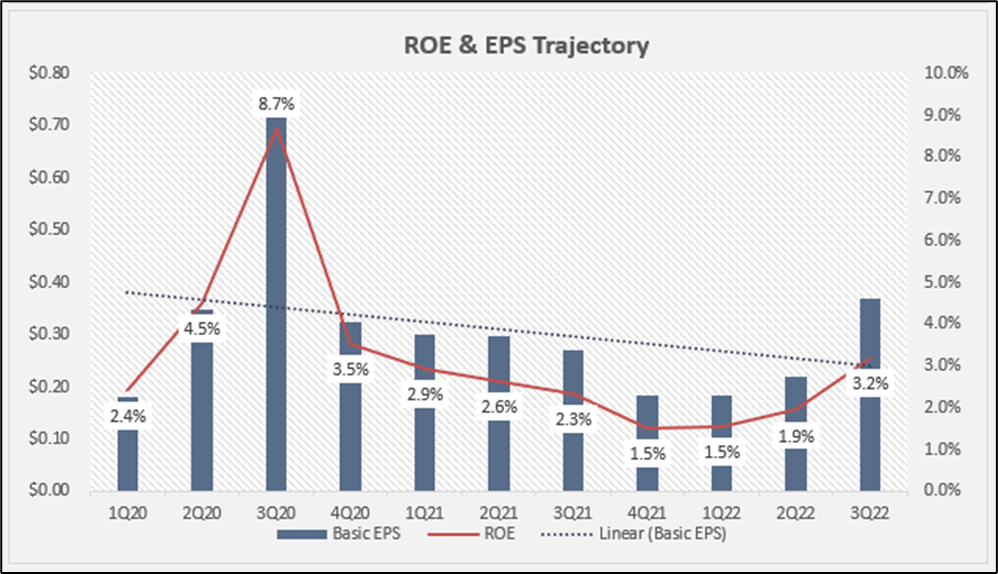

A SaaS is a nice model as it allows the generation of highly predictable and recurring revenue (in 3Q22 revenue renewal rate was 94%, which is at the high end of the company's historical range of 92% to 94%). This is the reason for the stock performance over the last years.

However, the economic slowdown poses a serious threat to the company's top-line performance and the legal spending related to Vivint’s refusal to pay licensing fees will affect both the bottom and top line. In particular, as stated during the 3Q22 earnings call :

Alarm.com believes that quarterly SaaS and license revenue and total revenue will be impacted by approximately $6 million per quarter beginning with the fourth quarter of 2022 and through 2023.

On the inflation side, the company did a second price increase this year on some of its hardware products that along with some relief in shipping costs led to an improvement in hardware gross margins from 17.7% in 2Q22 to 19.1% in 3Q22. However, this is still below the company's historical gross margins of 21%.

{kind=link}

The balance sheet is healthy and interest-bearing debt doesn't represent an issue given the company's quick ratio of ~ 4.11x.

Overall, I do see good reasons that make me willing to invest in this company. In fact, I believe that the company will be able to effectively navigate this economic slowdown through innovation and M&A. Moreover, once the legal battle with Vivint will be over, and assuming a positive outcome, this will add additional fuel to the stock performance.

Having said that, and in line with the current macro environment and company-related trends, I expect convergence to the median valuation of EV/SALES of ~ 2.08x.

{kind=link}

In terms of downside risks , here are a few:

- Competition , If the competition will be perceived as being a key driver of slower growth, it would negatively affect the company's share price.

- A legal Battle, a later termination with a negative outcome, would negatively affect the company's share price. On the other side, a sooner termination with a positive outcome is likely to generate a positive reaction which would positively affect the company's share price.

Final Remarks

I rate shares as HOLD with an estimated fair value of $38.76/share , which would represent a 19.7% downside from the current price of $48.29.

Author's Estimates

Having said that, even if I do believe in the growth potential and I do like a SaaS model (this is also the reason I am unwilling to take a short position) and I am more likely to wait on the sidelines as I do expect the overall market to go lower in the 1Q23. Below, you can see some stock statistics.

For further details see:

Alarm.com: A SaaS Story To Keep On The Radar