ALRM - Alarm.com's Q4: Going In The Right Direction

2023-03-23 09:36:00 ET

Summary

- The hardware segment keeps decelerating, however, the management seems to have everything under control and a clear strategy to continue executing well.

- The price increase put in place in early 2022 was the real tailwind of the improved gross margins in the hardware segment.

- I maintain a Neutral rating with a new fair value of $45.51/share.

4Q22 Results Overview

After Alarm.com ( ALRM ) ("the company") reported the Q4 2022 fiscal results the market reacted with shares falling ~ 3% in response to such developments.

For Q4, revenues came in at $208M, up ~ 6.6% over the prior year, and slightly above the consensus of $207M. However, the top-line positive result also has a dark side represented by a deceleration in hardware (up ~ 0.1% YoY, mainly driven by sales of cameras) as well as SaaS and license revenue (up ~ 10.5% YoY).

Author's Estimates

Now, let's take a closer look at the 4Q22 number. We can find out that SaaS and license revenue remains resilient with a revenue renewal rate of 94% (which is at the high end of the historical range of 92% - 94%). We can also notice a significant improvement in gross margins, driven by the hardware segment where the gross margin grew from ~ 11.1% in 4Q21 to ~ 18.9% in 4Q22 (driven primarily by price increases). SaaS and license gross margins remained solid at ~ 85.2%.

On the other side, the bottom line result was well above the market consensus, with the 4Q22 GAAP EPS of $0.36 (4Q22 net margin is at ~ 8.7%), and a huge beat on street estimates of $0.12 (and also better than what I personally expected). However, a patent infringement lawsuit against Vivint keeps representing a headwind to the bottom line due to additional legal fees.

Author's Estimates

For FY23 the company expects to generate from $851.5 million to $877.5 million with non-GAAP EPS to be between $1.44 and $1.57 per share. In my opinion, I believe that the FY23 outlook is in line with the current macro-trends and it accounts for the overall slowdown on the hardware side. Having said that, I do expect an acceleration in FY24 supported by the 4 key drivers outlined by the company during the 4Q22 earnings call:

1. Commercial markets, by further improving Alarm.com's platform capabilities, the company expects to further target ~ 6M properties in the U.S. and Canada. In my opinion, the company's ability to expand further its platform capabilities as well as investments in innovation will be a big tailwind to capture a significant market share in this segment.

Commercial is now about 8% of our SaaS revenue and it grew over 25% year-over-year in the fourth quarter. And we have over 500,000 commercial accounts now.

2. Innovation in the video, with the wireless battery-powered version of the company's flagship video doorbell representing the latest one. Moreover, when this kind of innovation is coupled with OpenEye capabilities (one of the company's subsidiaries that offers cloud-managed solutions for video security), this represents an additional tailwind for the customers to choose Alarm.com

3. International growth. As of December 31, 2022, the company generates ~ 4% of its total revenue outside of North America. I do believe through strategic partnerships the company will be able to grow its market share outside the U.S. and this will represent a long-term tailwind for growth.

Our base of global accounts surpassed $0.5 million in 2022.

4. Development of its subsidiary businesses (e.g., EnergyHub, Noonlight, PointCentral, Shooter Detection Systems, and Building 36). The subsidiaries' businesses are a key part of the long-term growth and allow the company to offer a broad range of solutions. For example, EnergyHub's ecosystem enables utilities to access greater electricity load capacity as they do manage the sources of stress on the grid.

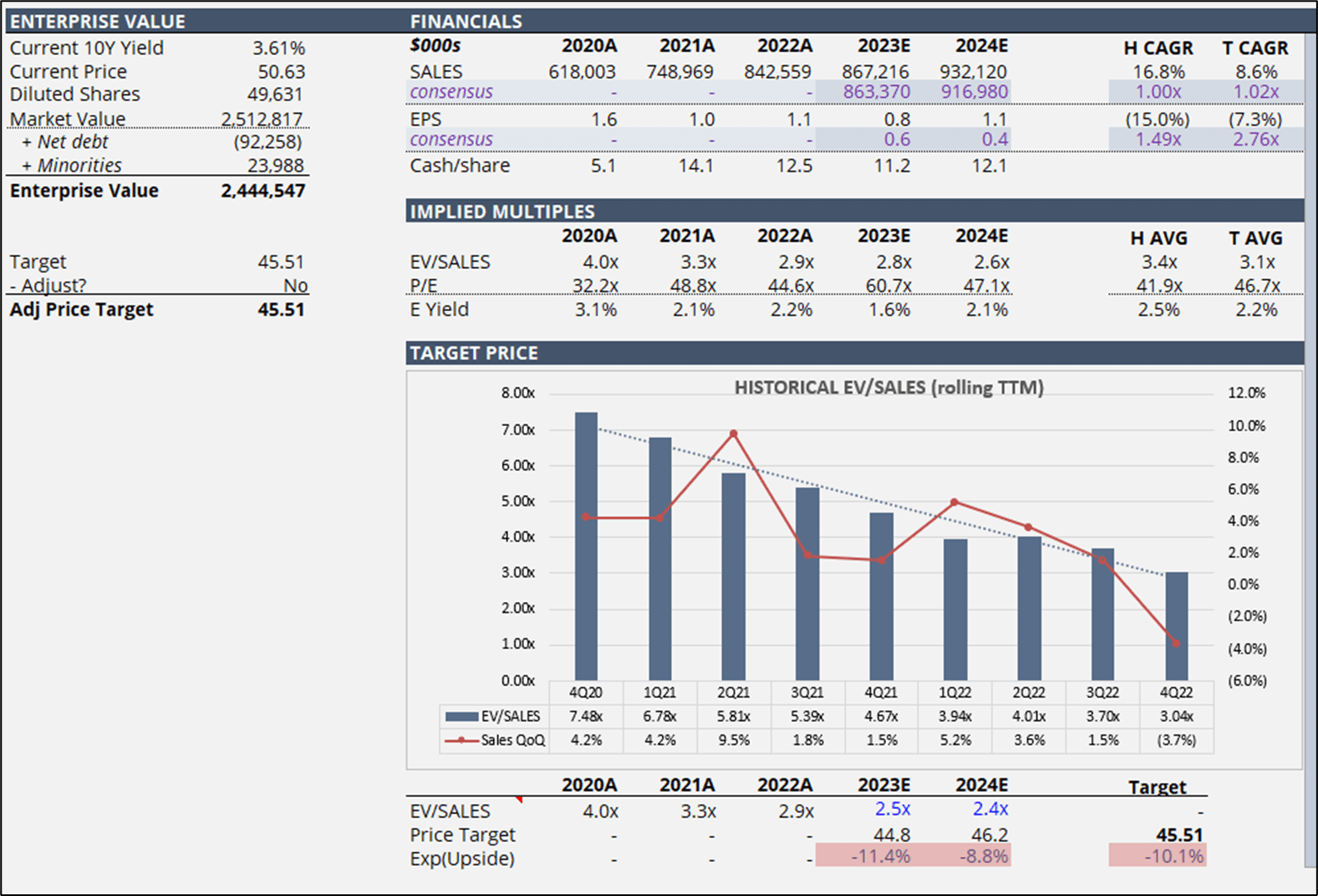

Valuation Update & Final Remarks

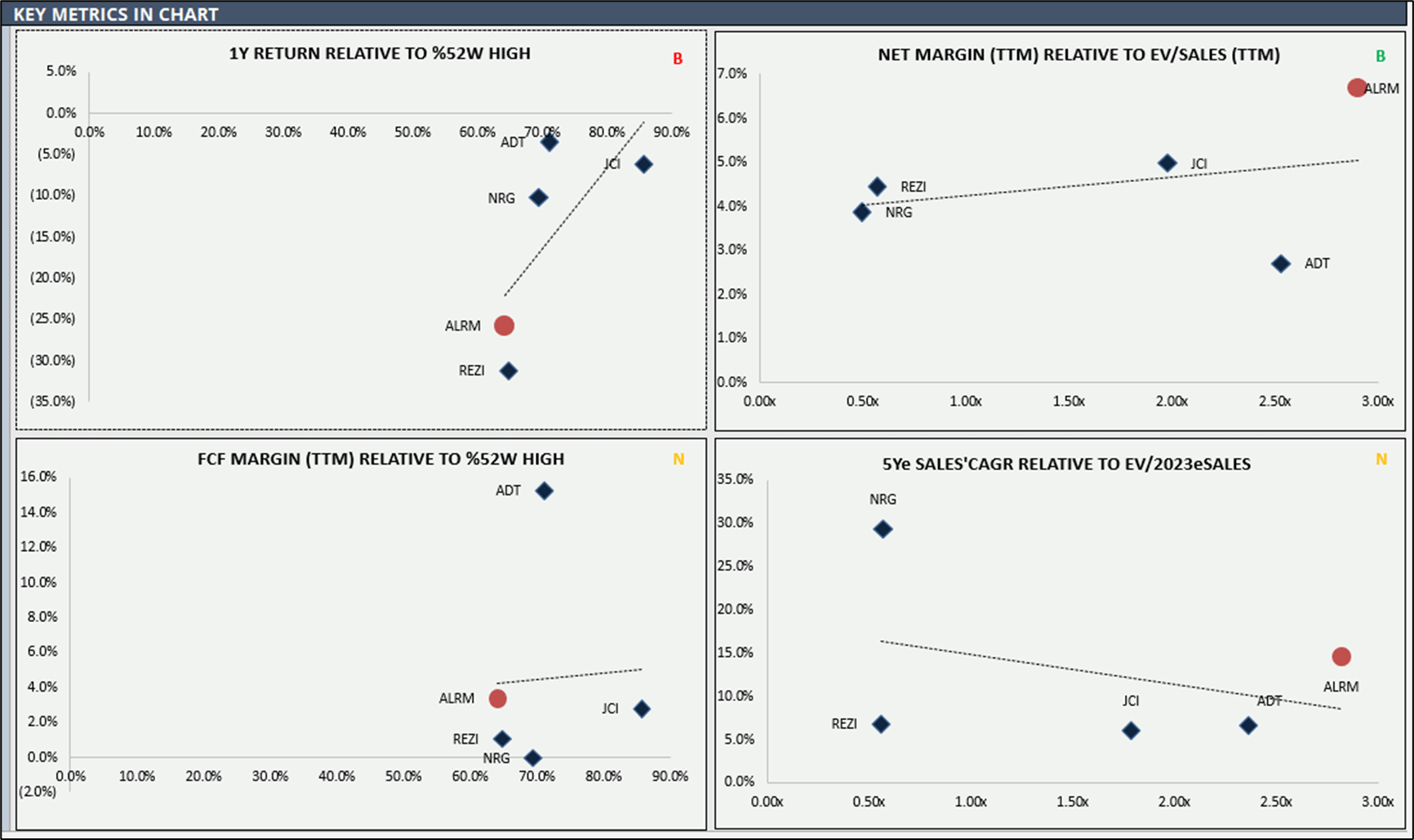

Currently, the company is trading at an EV/SALES of ~2.78x TTM, which represents a premium relative to the peer's median EV/SALES of ~1.96x TTM. Following the 4Q22 results, and the FY23 outlook, I revisited my expectations for the year ahead.

Author's Estimates Author's Estimates

{kind=link}

{kind=link}

As you can see from the above chart, I raised the target from the previously provided fair value of $38.76/share to the new fair value of $45.51/share driven mainly by multiple expansions and to a less extent by fundamentals. On the fundamentals side, I revised downward my top-line expectations with FY23, for instance, moving from ~ $874M to $867M, and I revised upward my bottom-line expectations driven by improved gross margin trends. On the multiples side, I revised it upward since I believe that the SaaS business model will allow the company to trade at higher multiples even in a recessionary scenario.

Overall, I maintain the NEUTRAL rating with the new fair value of $45.51/share , which would represent a 10.1% downside from the current price of $50.63. Having said that, for a risk-tolerant investor, the company may represent a good investment since it is profitable on a GAAP basis, with stable free cash flows, and with most of the company's revenues deriving from SaaS and licenses.

For further details see:

Alarm.com's Q4: Going In The Right Direction