ALRM - Alarm.com: Tepid 2024 Outlook On Challenging Macro Overhang

2023-11-20 11:01:36 ET

Summary

- Alarm.com experienced strong growth historically, but growth slowed in 2022 due to macro headwinds and broad-based challenges in residential and commercial segment.

- Its financials have been impacted by tepid demand outlook amidst lower hardware sales, slowing SaaS revenue and declining operating margins.

- We believe there are continued downside risks and current valuation is unattractive to attribute for the slowing growth and degrading profitability.

Investment Thesis

We ascribe Alarm.com ( ALRM ) with a Neutral rating on the back of

1) persistent macro challenges significantly impacting its core residential segment and impeding growth

2) continued spend on legal costs suppressing operating margins due to several lawsuits, in particular with Vivint

3) Unattractive valuation despite slowing growth and degrading profitability

Company Background

Alarm.com offers a scalable and dependable cloud monitoring and management platform focused on residential and commercial security segments. It offers a diverse portfolio of IoT solutions including security, video analytics, energy management, electric utility grid management and other analytics to over 9 mn homes as well as commercial property owners. It relies on external service providers which markets, sells and installs Alarm's products and boasts a network of 11,000 service providers across the country. Service provider partners have an average contract typically of 3 - 5 years with residential and commercial property owners. In addition, it also sells hardware equipment and connected devices such as video cameras, gunshot detection centers and other modules.

Historical Financials

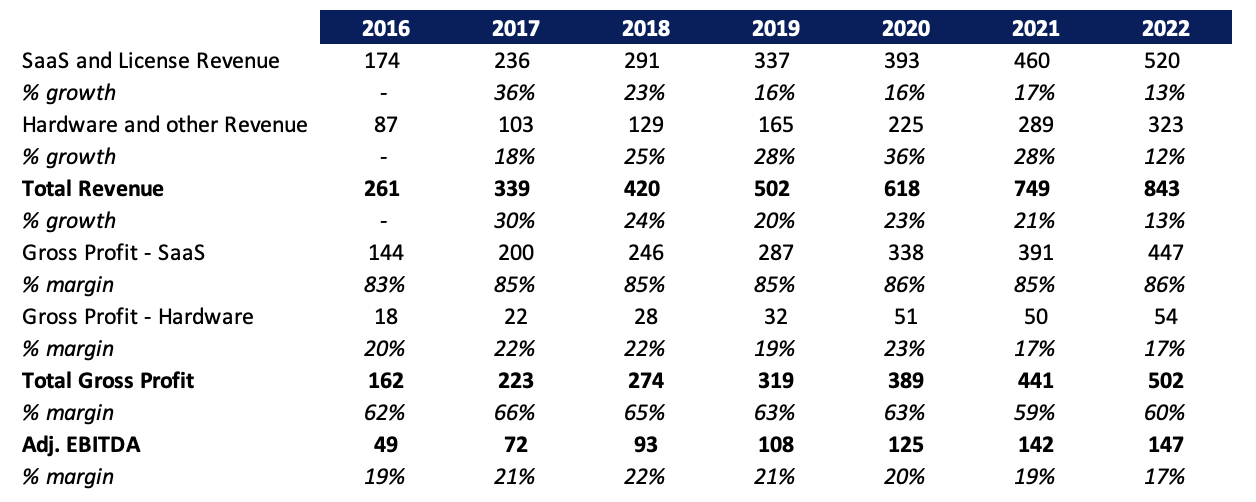

The company delivered a strong 20%+ growth historically driven by consistent growth in its SaaS and license revenue with retention rates ranging between 93-94% over the past several years along with renewed momentum within its hardware business during pandemic. Despite the pandemic, the company reported strong 20%+ growth in 2020 and 2021 driven by higher hardware sales as consumers looked to buy smart home solutions and also deploy the devices in their additional homes bought during the pandemic with record low interest rates. However, growth slowed in 2022 as macro headwinds intensified and device sales dropped along with lower renewal rates amidst inflationary headwinds.

{kind=link}

Gross profit margin for SaaS business have been stable at 85-86% historically while the gross margin within the hardware segment declined to around 17% from 20%+ during 2021-2022 as a result of higher shipment costs as well as a jump in inventory component costs. Gross margin on a consolidated basis declined to 60% primarily as a result of higher contribution from low margin hardware segment. Adj. EBITDA margin declined to 17% in 2022 from above 20% range primarily as a result of lower gross margins while maintaining stable operating leverage.

Weakening Earnings

The company had a tumultuous 2023 as a result of declining hardware sales while it tries to pivot to commercial segment as consumer segment continues to worsen. Renewal rate declined marginally to 93% on a trailing twelve month basis resulting in an HSD growth in SaaS revenues, although significantly lower than the high teens growth reported during the pandemic as well as over its long term history. ALRM reported a muted Q3 with total sales growth of 2.6% with growth further decelerating from the 5.1% YoY growth it posted in Q2 and missing estimates by a slim margin. The slower growth was primarily as a result of an ~8% decline in hardware sales as a result of broad-based decline across both residential as well as commercial market. The residential market is also impacted by lower sales of LTE modules as the conversion from 3G to LTE modules has been largely complete while macro conditions continue to worsen demand environment elongating the cycles within the commercial segment.

Consolidated gross margins improved by 290 bps to 63.3% driven by strong improvement in hardware gross margins which shot up by 350 bps YoY as a result of favorable product mix and tailwinds from lower supply chain costs. Selling and marketing expenses as % of revenues remained stable while R&D expenses deleveraged by 180 bps as a result of increased headcount. In addition, legal fees continue to squeeze bottom line as it fights several litigations with Vivint and others which lead to G&A deleverage by 120 bps. In all, Adj. EBITDA margins came in at 18.6%, down slightly by 20 bps, as a result of robust gross margin expansion offset by SG&A and R&D deleverage.

Balance sheet position continues to be strong with the company ending with total cash balance of $680 mn and total debt outstanding of $493 mn implying a net cash position providing significant flexibility to the balance sheet to invest in growth areas.

The company guided full year revenues to be ~$880 mn at midpoint with SaaS and license revenue expected to be $567 mn at midpoint and hardware revenue of $313 mn. This implies an 8% growth in Q4 for SaaS and license revenue, further decelerating from 8.9% YoY growth it recorded in Q3 and an ~6% jump in hardware revenues YoY, while flat sequentially. We believe given Q4 is seasonally a weak quarter due to weather and lower installs and the company could fail to meet its guidance amidst macro pressures that have seen no signs of abating. The company expects EBITDA margin of 16.3% for the year implying a sub-16% for Q4. In addition, the company provided a tepid initial guidance for 2024 and expect revenues of $917.5 mn implying a 4.2% revenue growth, down slightly from 4.4% expected growth in 2023. SaaS and business licence revenue is expected to further slowdown to sub-8% driven by higher churns and lower new adds while hardware revenues is expected to decline by 2% at midpoint, post the 3% decline anticipated in 2023 reflecting continued macro pressures while margins are expected to be flattish at 16%. We believe there are pronounced downside risks to the company's guidance amidst tough macro, rising competitive intensity as well as higher legal costs and ADT's shift towards its platform.

Valuation

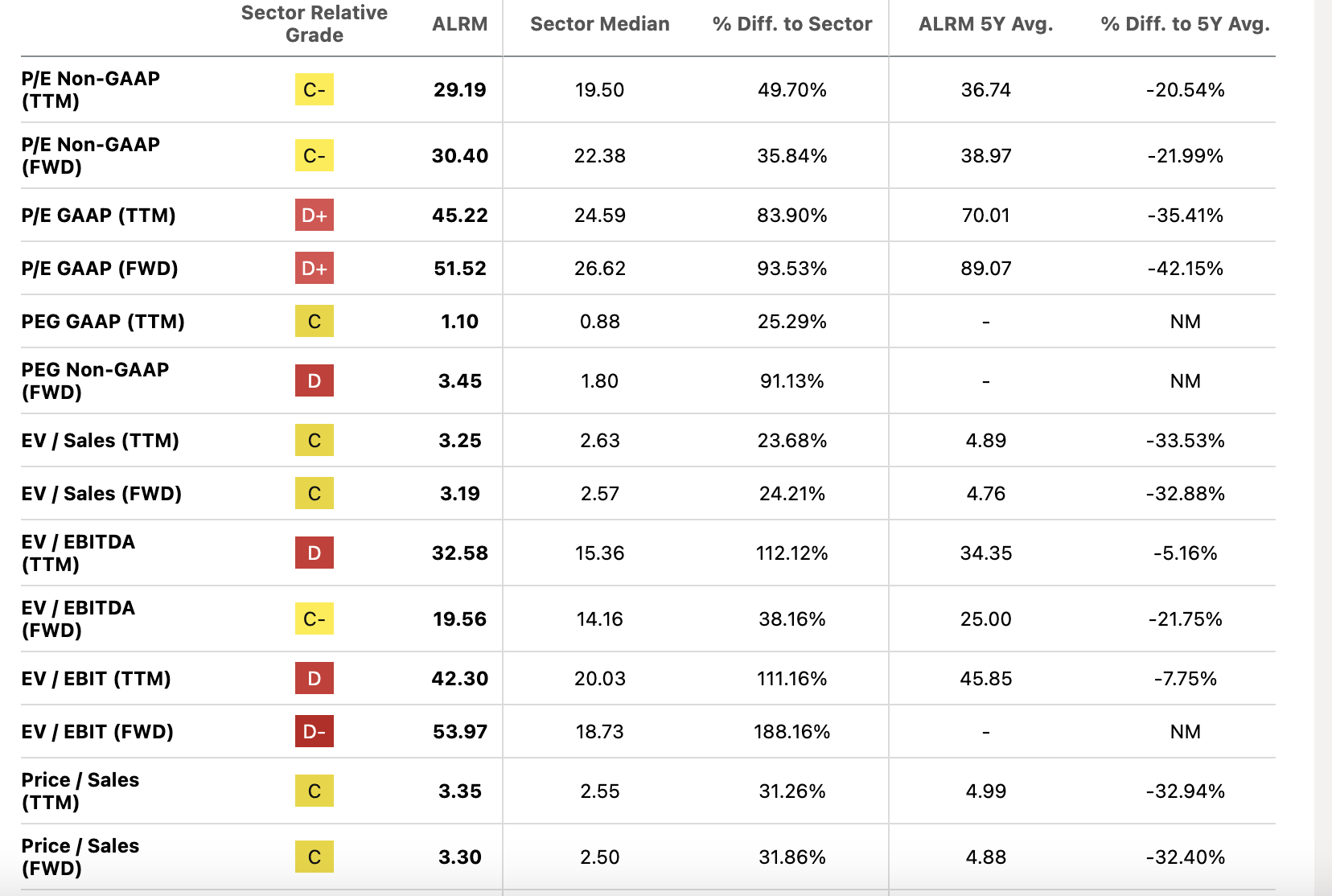

Seeking Alpha's Valuation grade ascribes a 'D-' rating primarily as a result of higher valuation compared to its peers. ALRM trades at 3.2x EV/ Fwd Sales and 19.6x EV/ Fwd EBITDA at a significant premium compared to 2.6x EV/ Fwd Sales and 14.2x EV/ Fwd EBITDA of its sector median respectively. Even factoring the valuation basis the growth characteristics, the company trades at 3.4x on a Fwd PEG basis compared to sector median of just 1.8x demonstrating the significant premium despite slowing growth. From growth perspective, revenue growth is expected to be just 7% compared to sector median of 8% while EBITDA growth is expected to be around ~1% compared to sector median of 7%.

{kind=link}

It does trade at a discount to its long term average across all parameters. We believe the discount is warranted given the slowing growth and intensifying macro headwinds, particularly within the consumer space. Initiate at Neutral.

{kind=link}

Risks to Rating

Risks to rating include

1) ADT contributes about less than a fifth of consolidated revenues historically. Google's (GOOG) (GOOGL) $450 mn investment back in 2020 along with its launch of DIY home security system in partnership with Google in March 2023 have started to move off to its own platform and can prove detrimental to its business

2) Macro conditions can worsen impacting new home sales as well as continued inflationary headwinds which can dampen consumer demand

3) Adverse impact from litigation with Vivint and in case other service providers follow a similar suit could have a detrimental impact

4) ALRM relies on service provider's capabilities to sell and market its devices and cloud solutions. The inability of the service providers to market can be detrimental to the growth

5) ALRM operates in a competitive space with several mega tech players such as Google, Amazon (AMZN) (Ring) and others have entered within the space and have been competing aggressively which can significantly impact its operations

6) Upside risks include general improvement in macro environment, commercial penetration improves substantially, growth within the international markets

Conclusion

Alarm.com has done phenomenally well historically driven by increase in DIY security solutions and IoT for new home buyers as well as buyers with second homes amidst record low rates since the pandemic. However, the current inflationary headwinds squeezing discretionary spends by consumers along with slowing pivot to commercial segment amidst slowdown in consumer reflects the current downturn within the industry as well as Alarm.com, in particular. In addition, the competitive space has been heating up with the launch of a new ADT security solution in partnership with Google, while Amazon also continues to bolster its security and home solutions segment. We believe the slowing growth and relative valuation provides limited margin of safety and we initiate with a Neutral rating.

For further details see:

Alarm.com: Tepid 2024 Outlook On Challenging Macro Overhang