AIN - Albany International Is Highly Profitable And The Balance Sheet Is Very Strong

2023-05-30 04:10:59 ET

Summary

- Albany International is well-prepared to face inflationary pressures and potential recession due to its strong balance sheet and leading market position.

- The company's recent decline in share price presents a good opportunity for conservative dividend growth investors, but averaging down is recommended due to high operational volatility.

- The dividend is safe as the cash payout ratio is very low.

- Risks include prolonged inflationary pressures, a potential recession impacting demand, and the management's use of the company's significant cash reserves.

Investment thesis

Albany International ( AIN ) is a company whose shares can be held for decades due to its leading position in the markets it operates, as well as its conservative use of cash and shareholder-friendly management. The company is starting to feel the impact of current inflationary pressures on its profit margins, which has lowered investor expectations in the short and medium term. Consequently, AIN stock price has declined by almost 25% from all-time highs, partly also due to growing concerns about a potential recession as a consequence of recent interest rate hikes.

Still, the company remains highly profitable and both inflationary pressures and an eventual recession represent temporary headwinds for which the company is well prepared thanks to a very strong balance sheet, so I consider the current decline in the share price as a good opportunity for conservative dividend growth investors, but given the current high operating volatility and potential risks, especially in terms of a potential recession materializing, I strongly believe that investors should slowly average down from current prices as volatility is currently too high.

A brief overview of the company

Albany International is the global largest manufacturer of paper machine clothing products and a manufacturer of advanced materials-based engineered components for a wide range of industries. The company was founded in 1895 and its market cap currently stands at $2.71 billion, employing around 3,900 workers worldwide.

Albany International logo (2022 Annual Report)

The company operates under two business segments: Machine Clothing and Engineered Composites. Under the Machine Clothing segment, which provided 59% of net sales in 2022, the company supplies consumable permeable and impermeable belts used in the manufacture of paper, paperboard, tissue and towel, pulp, nonwovens, fiber cement, and several other industrial applications. And under the Engineered Composites segment, which provided 41% of the company's net sales in 2022, the company provides highly engineered, advanced composite structures to customers in the commercial and defense aerospace industries, including Boeing ( BA ), Airbus ( EADSF ), and Comac.

Currently, shares are trading at $86.88, which represents a 24.71% decline from all-time highs of $115.39 on February 2, 2023. Inflationary pressures and supply chain challenges are having a significant impact on profit margins, and there are growing concerns about a potential global recession as a consequence of ongoing interest rate hikes to alleviate high inflation rates. This is why investors remain cautious. But despite these headwinds, the company has increased its sales over the years boosted by acquisitions, and successfully strengthened its balance sheet, which should allow for further growth in the coming years.

Recent acquisitions

In the last few years, the company has been strengthening its balance sheet after a major acquisition that took place in April 2016 when it completed the acquisition of the Composite Aerostructures division of Harris Corporation for $210 million. Later, in November 2019, the company acquired CirComp GmbH, a German developer and manufacturer of high-performance composite components for aerospace and other demanding industrial applications, for $36.3 million.

After these two acquisitions, the company raised almost $200 million in cash and equivalents and increased its inventories while maintaining a sustainable debt level, which means that it is possible that the company will soon carry out a new major acquisition as its balance sheet is strong enough.

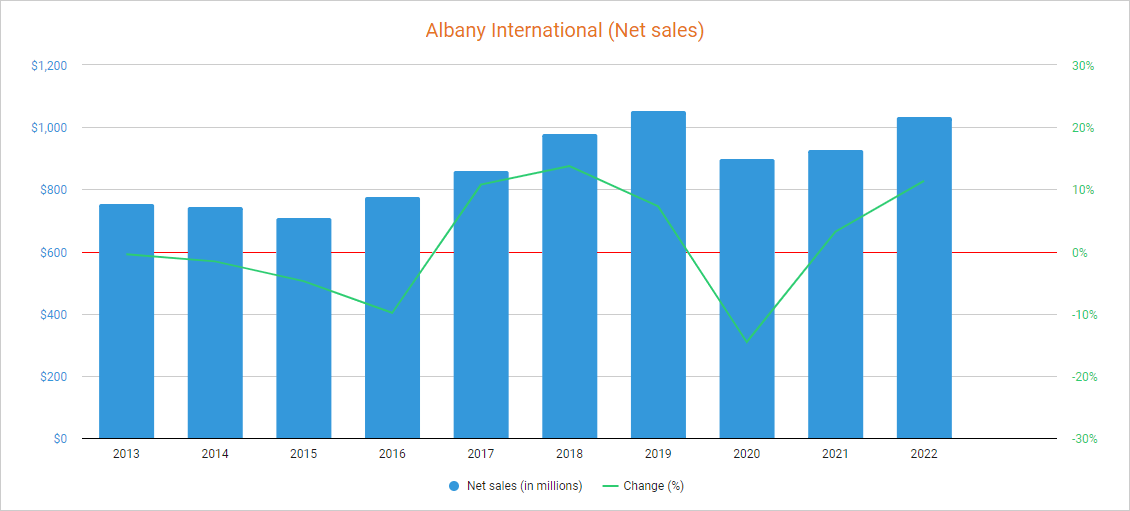

Net sales are ready to take off again

The company managed to increase its net sales over the last few years thanks to recent acquisitions and growth in the Engineered Composites segment, and although the coronavirus pandemic crisis caused a 14.56% decline, sales increased by 3.18% in 2021 and by 11.37% in 2022.

{kind=link}

Furthermore, net sales increased by 10.21% year over year during the first quarter of 2023 despite negative foreign exchange impacts, boosted by organic growth in the Engineered Composites segment as the Sikorsky CH-53K helicopter program boosted the segment's net sales by around 30% compared to the same quarter of 2022. In this regard, net sales are expected to increase by 1.94% for the full 2023 and by a further 5.71% in 2024. In the foreseeable future, the management plans to invest in the Engineered Composites segment in order to drive growth. Meanwhile, the management needs to innovate in the Machine Clothing segment to maintain its leading position in the market as it represents a very mature segment where growth is, in my opinion, not likely to happen, at least in a meaningful way. Still, the strengthening of the balance sheet in recent years characterized by high cash and equivalents and inventories suggests that the company will soon have to look for potential acquisitions to make use of that cash, which is why I strongly believe net sales are poised for future growth.

Using 2022 as a reference, 57% of the company's net sales take place within the United States, whereas 12% are generated in Switzerland, 7% in France, 6% in Brazil, 6% in China, 6% in Mexico, 2% in Italy, and 4% in the rest of the world, which means the company has wide geographical diversification.

The recent decline in the share price coupled with increased sales has caused a decline in the P/S ratio to 2.563, which means the company currently generates net sales of $0.39 for each dollar held in shares by investors annually.

This ratio is 25.86% lower than the peak of 3.457 reached early this year but is still 15.53% higher than the average of the past 10 years of 2.165 as EBITDA margins have improved over the years despite recent contraction, a fact for which I recommend averaging down as a strategy due to high operational volatility.

Margins are temporarily depressed

Due to the leading position of the Machine Clothing segment and the high added value of the products manufactured in the Engineered Composites segment, the company enjoys exceptional profit margins year after year. Still, inflationary pressures and supply chain headwinds have recently caused a deterioration of said margins as the trailing twelve months' gross profit margin declined to 37.51% and the EBITDA margin to 20.45%.

Nevertheless, these profit margins are still typical of a highly profitable company, so Albany International should not have problems in the short and medium term in generating strong cash from operations and continue strengthening its balance sheet. Nevertheless, gross profit margins during the first quarter of 2023 were 36.91%, whereas the EBITDA margin improved to 21.69% as inflationary pressures are showing early signs of improvement. In this regard, margins are expected to remain slightly depressed for as long as inflationary pressures and supply chain challenges continue putting pressure on the current macroeconomic landscape, although this should not be a significant issue for the company in the long term as the current debt level is highly manageable thanks to strong cash from operations and high cash and equivalents and inventories.

The company's debt is highly manageable

The company has been strengthening its balance sheet since the acquisition of the Composite Aerostructures division of Harris Corporation in 2016 by raising cash and equivalents of $304 million while maintaining a sustainable long-term debt, which currently stands at $491 million.

This high cash and equivalents greatly reduce the risk that debt poses to the company as it has enough resources to pay down a significant portion of its debt with available cash. But also, inventories have increased significantly in recent years to $154 million, which should allow for strong cash from operations in the coming quarters.

That is why I believe that investors should see significant improvements in the company's operations in the foreseeable future, both thanks to a reduction in debt (and therefore interest expenses) and a potential acquisition if the management manages to find a good opportunity. In addition, the company continues to accumulate more cash as it remains highly profitable despite headwinds.

The dividend is safe as the cash payout ratio is low

Albany International's shareholders have enjoyed growing dividends over the years, and the latest raise was announced in December 2022 when the management decided to increase the quarterly payout by 19% to $0.25 per share.

But despite increasing its dividend over the years and the recent drop in the share price, the dividend yield currently stands at just 1.15%, which is a very low yield as a consequence of two main factors: first, the cash payout ratio is very low, which allows for significant growth investments over the years, and second, the current exceptional balance sheet situation suggests that the company is ready to make a big move.

In order to assess the sustainability of the dividend over the years, in the following table I have calculated what percentage of the cash from operations the company used each year to cover dividends paid and interest expenses. In this way, we will be able to calculate the company's ability to cover its dividend year after year through actual operations.

| Year |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| $84.20 |

| $95.94 |

| $79.52 |

| $64.22 |

| $132.49 |

| $200.35 |

| $140.25 |

| $217.48 |

| $128.21 |

| Dividends paid (in millions) |

| $19.73 |

| $21.09 |

| $21.81 |

| $21.87 |

| $21.93 |

| $23.25 |

| $24.57 |

| $25.89 |

| $26.47 |

| Net interest expenses (in millions) |

| $10.71 |

| $9.98 |

| $13.46 |

| $17.09 |

| $18.12 |

| $16.92 |

| $13.58 |

| $14.89 |

| 14.00 |

| Cash payout ratio |

| 36.16% |

| 32.39% |

| 49% |

| 60.67% |

| 30.23% |

| 20.05% |

| 27.20% |

| 18.75% |

| 31.56% |

As one can see in the table above, the management has been very conservative with the use of cash in recent years as the cash payout ratio has remained at very low levels, including 2022 despite ongoing supply chain and inflationary challenges.

As for the first quarter of 2023, cash from operations was -$16.4 million as inventories increased by $14.7 million and accounts receivable by $21.2 million while accounts payable increased by just $6.5 million. During the first quarter of each year, there's also some seasonality in receipts and incentive compensation payments for performance in the past year. In this regard, the dividend remains safe despite current macroeconomic challenges and cash from operations should be higher in the coming quarters due to higher-than-usual inventories.

Risks worth mentioning

Although I consider Albany International's risk profile to be very low thanks to its leading position, high profit margins, and very robust balance sheet, there are certain risks that I would like to highlight, especially in terms of timing.

- If inflationary pressures continue to impact the company's operations, profit margins could remain depressed for an extended period of time or even fall below current margins, which could cause further share price declines.

- If a recession does materialize as a result of recent interest rate hikes, demand for the company's products could be significantly reduced. This would cause not only a temporary drop in sales but also a deterioration in profit margins due to unabsorbed labor, which would be a problem considering that the company will soon have to start emptying its inventories.

- The company is currently sitting on a mountain of cash, so the management will soon have to decide what to do with all that cash. It depends on how well the management uses this cash so that net sales keep growing in the long term and, therefore, the share price continues the upward trend that the company experienced in recent years.

Conclusion

It is clear that Albany International's prospects have deteriorated slightly in recent quarters as a result of the recent contraction in profit margins and growing concerns about a potential recession, which could have a significant impact on the demand for its products. But even so, Albany International's operations remain highly profitable while sales are expected to continue to increase slightly in 2023 and 2024. In addition, the company has significantly strengthened its balance sheet since the acquisition of the Composite Aerostructures division of Harris Corporation in 2016, so it is strongly prepared to face not only the current inflationary and supply chain challenges but also a potential recession.

Albany International can be bought and held for decades by any conservative dividend investor, and shareholders can expect the company to continue expanding over the years thanks to its strong balance sheet and high profit margins. Even so, and although I consider that the recent fall in the price of shares represents a good opportunity to start a position, I believe that investors should pay attention to the price of shares and slowly average down from current share prices since the P/S ratio is still higher than the average of the last 10 years and we are facing times of high volatility in the markets.

For further details see:

Albany International Is Highly Profitable And The Balance Sheet Is Very Strong