ALB - Albemarle And SQM: These Amazing Stocks Entered High Quality And Bad Momentum Screener

2023-07-31 08:18:37 ET

Summary

- Albemarle Corporation and Sociedad Quimica y Minera de Chile are robust companies experiencing growth and downward price pressure while trading in an area of extremely low valuation.

- Both companies are in the lithium industry and are benefiting from the global trend towards electric vehicles.

- The long-term outlook for the industry is positive, but there are risks such as nationalization threats and short-term demand drivers.

- Both companies showed up on my high quality screener, which was designed to find bad momentum stocks with high quality - a perfect storm.

- Even a further decrease in the price of lithium should be offset by increasing production. It will still be insufficient to meet long-term demand.

The main reason I'm trying to manage more research on Albemarle Corporation ( ALB ) and Sociedad Quimica y Minera de Chile ( SQM ) is because both companies showed up in my Top Quality Stock Screener on Seeking Alpha. The high growth businesses targeted by that screener are those that are currently experiencing downward price pressure. The risks, potential, and future growth prospects of these picks will be discussed in this analysis. We will discuss seasonality as well as other trends, starting with industry outlook, the current macro environment, regulatory obstacles, but what is more crucial - the deep breakdown of companies' financials and fair value. There is no guarantee that the company will generate strong returns in the future, as the lithium price is also reflected in the company's stock price. As is well known, the companies experienced some price pressure as a result of the sharp decline in the price of lithium futures, but it still enjoys strong margins, and the global EV trend will result in sharply rising volumes in the coming years, driving up the fair value of the company even further.

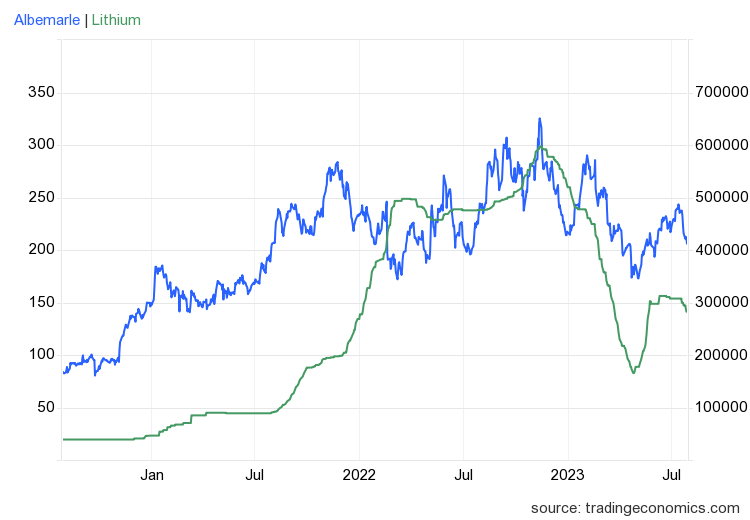

Lithium price and Albemarle price (Tradingeconomics.com)

{kind=link}

High Quality Screener

If you are wondering which screener I am referring to, it is the one I created using the Seeking Alpha tool. Such a screener provided many great picks in 2023, which helped to identify many excellent opportunities, such as Axcelis Technologies, Inc. (ACLS), Perion Network Ltd. (PERI), and Tecnoglass, Inc. (TGLS), which are up substantially in 2023 YTD.

Here are the results of my high quality screener's most successful examples; however, these companies are incredible, but you cannot find them there anymore. Due to the objective of the screener: locating high-quality companies despite price pressures. While these businesses are no longer experiencing price pressures, they could not be located there. However, it should be on a watchlist. However, not all companies are performing as well as these examples, but they serve as an illustration.

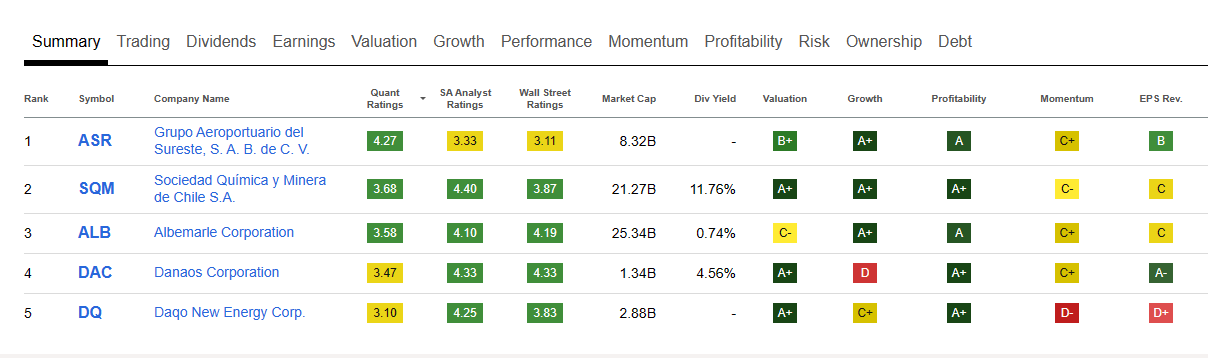

In the screener, there are typically only 5 to 10 companies that I recommend analysing further, but at the beginning of 2023, there were 10 to 20 picks. There are currently only five companies visible, and two of them are ALB and SQM:

Personal High Quality Screener (Author via Seeking Alpha)

{kind=link}

Final words to my personal screener, here are strict and simple criteria that apply to all - profitability, balance sheet, and valuation perspective:

- All sectors,

- Quant rating: Hold to Strong Buy (due to great ability of the quant rating),

- PE GAAP ((TTM)): 0.0 to 25.0,

- PE Non-GAAP ((FWD)): 0.0 to 15.0 (these conditions help me to ensure a cheap selection and promising companies due to expecting of EPS growth)

- Revenue (3Y): 15.0% to >40.0% (I want to look for companies with great growth in the latest three years, but not too high due to possibility of further risks associated with big growth),

- Revenue ((FWD)): 15.0% to >40.0%,

- Net income (3Y): 10.0% to >60% (I want to see solid track record of growth in Net income),

- Net income margin ((TTM)): to range from 5.0% to >50.0%.

- In terms of balance sheet criteria, I consider the quick ratio, which should be between 0.8 and 8.0, and the debt-to-equity ratio, which should be as low as possible, i.e. between 0% and 60%, to be the most crucial. These ratios are, in my opinion, safe from both a liquidity and leverage perspective.

- The last and one of the most important points is the Momentum Grade, which should be from F to C+ (we want high quality companies with bad momentum due to temporary issues).

Even though no one can guarantee these companies' long-term success, the majority of them are historically excellent investments. Before investing in them, additional research must be conducted because some industries are more vulnerable and cyclical than others, and each industry possesses its own risks.

Returning to the thesis - Similarities and Differences

Although I mentioned one of my high-quality screeners, additional research is required to comprehend the industry and companies in general. While both companies operate in the lithium industry primarily as producers, there are significant similarities and differences between them that must be considered.

In the mid to long term, the outlook for industry is incredibly bright

Medium and long-term outlook

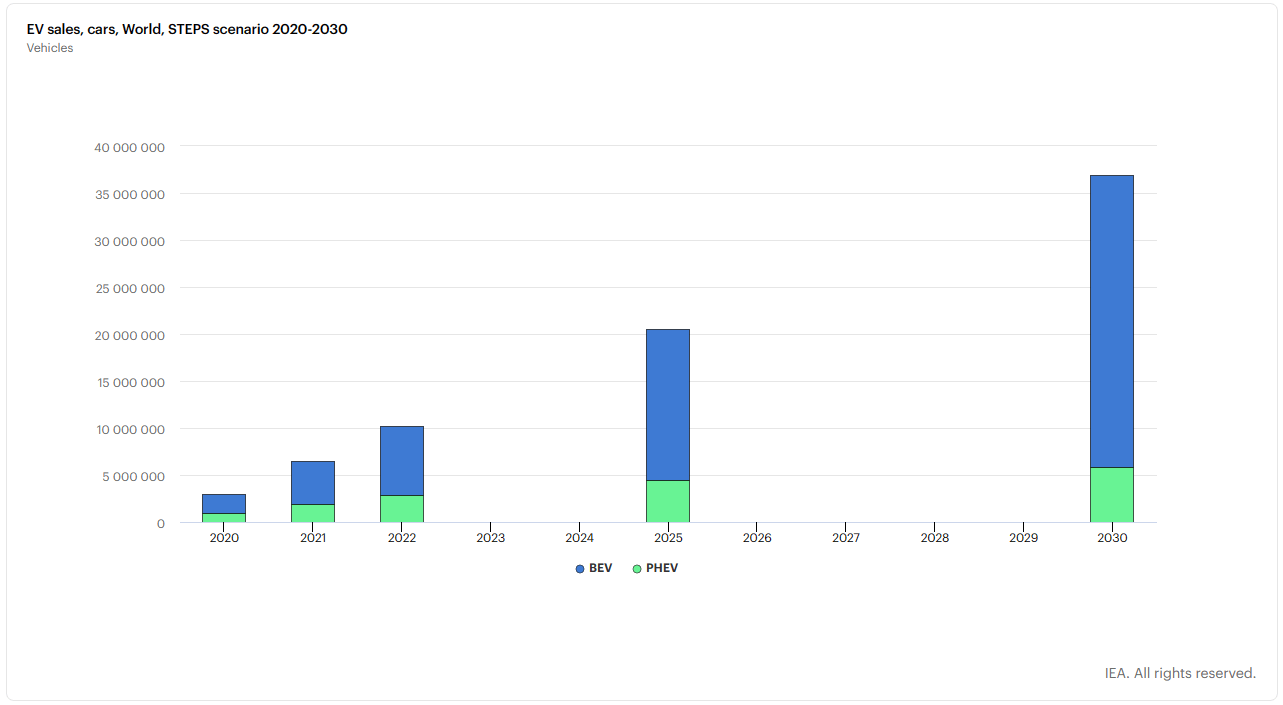

According to the International Energy Agency - IEA , total worldwide EV sales surpassed 10 million vehicles in 2022. According to STEPS ("Stated Policies Scenario" - a more conservative scenario), the institution anticipates EV sales in 2025 will reach 20 million vehicles and in 2030 will surpass 35 million vehicles. From the perspective of 2022, the industry is projected to grow at a CAGR of 26% until 2025 and nearly 17% until 2030. Simply amazing.

{kind=link}

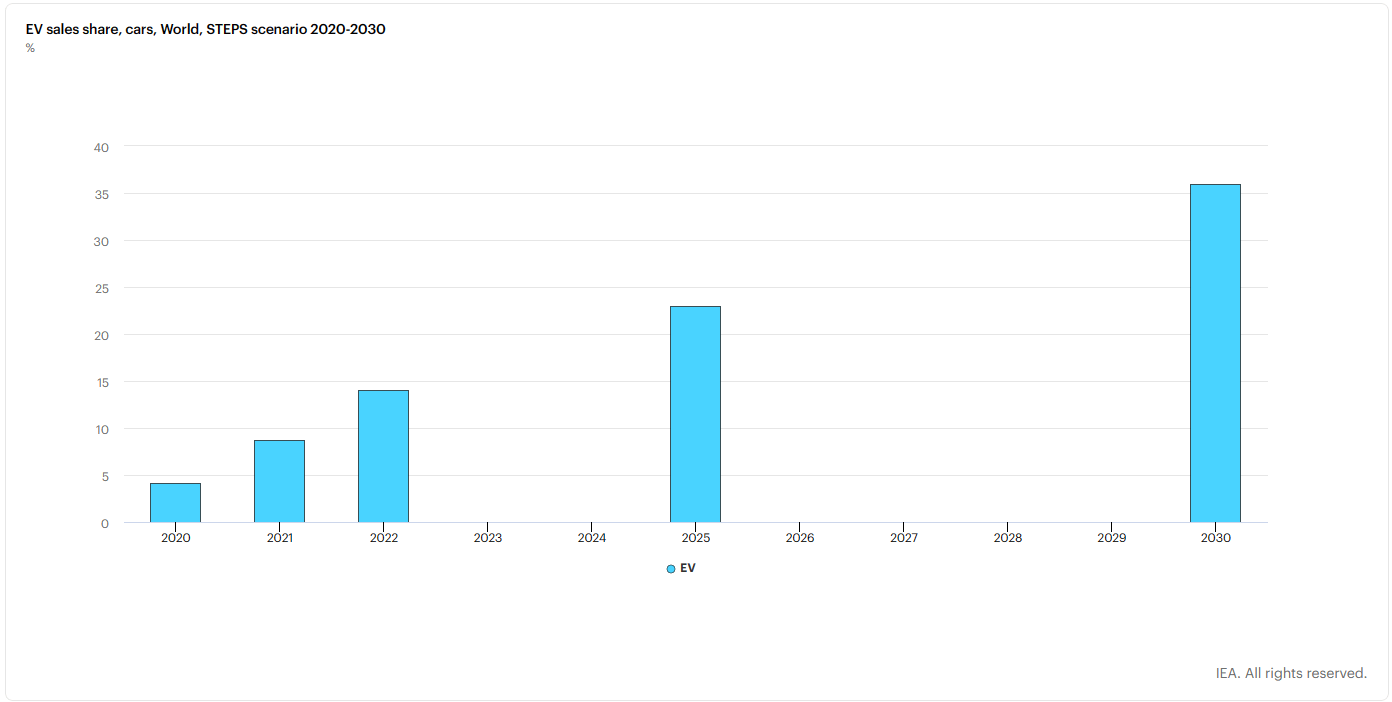

Moreover, in terms of sales, EV sales in 2022 accounted for slightly more than 14% of total vehicle sales and are projected to reach nearly 25% by 2025 and surpass 35% under the more conservative STEPS scenario.

{kind=link}

In such a scenario, the lithium battery segment, which is the primary reason lithium is mined, accounts for more than 80% of total lithium consumption, indicating that the industry requires more than twice as much lithium. Simply double by 2025, then more than triple by 2030. The problem is that there are not enough companies with such high production capacities to accomplish this. As there is no room for that to occur, I have serious doubts that the total demand will be met. However, a recession could significantly impact the long-term trend and price of lithium as well as the EPS of both companies. Nevertheless, the industry trend is also strongly supported by governments around the world.

According to the U.S. Geological Survey , global identified lithium reserves amount to approximately 98 million tons, of which:

- 21 million tons belongs to Bolivia,

- 20 million tons belongs to Argentina,

- 12 million tons belongs to the US,

- 11 million tons belongs to Chile,

- 7.9 million tons belongs to Austria,

- 6.8 million tons belongs to China,

- and others.

These businesses have outstanding operations in the largest reserve bearings.

Furthermore, Seeking Alpha reports :

According to Fastmarkets, there were 45 operating lithium mines last year, with 11 expected to open this year and seven next year. This pace is, however, far from adequate when compared to the outsized global demand.

The report contains subsequent findings and CEO comments confirming that long-term supply/demand imbalances will persist. While the situation may be reversed in the very short term, as evidenced by the sharp decline in the price of lithium, the outlook for the future is much less dependent on the current cycle.

Short-term outlook

First, keep in mind that the majority of both companies' sales are driven by lithium production and prices. Thus, the company's earnings can be highly volatile due to price fluctuations in both directions. As a result of the FOMO effect, and significant demand/supply imbalances, both companies reported astounding financial results for fiscal year 2022. The massive price helped to boost both companies' financial results.

However, demand and supply imbalances can cause short-term problems for businesses. In fiscal year 2023, the global battery supply chain will experience sluggish demand and high levels of inventory, both of which are likely to be negatively impacted by significant global monetary tightening, thereby indirectly affecting purchasing and economic activity. This also helps to reduce the market price of lithium. In my opinion, there will be a global monetary easing in 2024 and 2025, even if it is a softer one, which could stimulate additional short-term demand. The subsequent factor is destocking, which may end in 2023.

So from a short-term perspective, these picks are cyclical plays, but the real potential lies in the medium and long-term. There is nothing comparable in other cyclical industries. Assuming further price pressures as a result of a decline in consumer spending or lower-than-anticipated global EV car volumes, there could be a further weakening in lithium prices, which could lead to a stock depletion that is highly desired.

Nationalization threats

In Chile, there are stories regarding the nationalization of contracts. In April, President Boric considered nationalizing the country's lithium industry. Existing agreements should remain undamaged . The suggestion indicates that, following the expiration of the contract, a new public-private partnership with a majority or controlling state stake could be formed. While Albemarle does not anticipate any major consequences on its operations, SQM refused to comment. First, the vast majority of SQM's operations are logically viewed as a threat from a regulatory and nationalization standpoint. Albemarle is better suited for this situation than SQM, whose contract is set to expire in 2030 and Albemarle's in 2043. However, the risk of operating in third countries is similar, and a similar situation may exist in China, posing additional risks associated with deteriorating relations between the United States and China. Regarding the political climate in Chile, it is only natural that the country would wish to protect its lithium reserves. However, the ultimate question is always how, because ultimately it could reduce efficiency.

Target operations

SQM

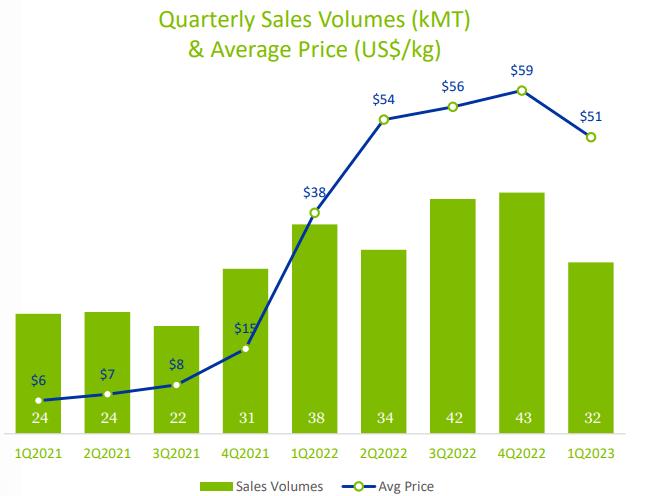

SQM is primarily located in Chile and has a substantial presence in Salar de Atacama, one of the locations with the most lithium reserves. SQM invests in mines and plants outside of Chile, primarily in Australia, thereby facilitating the "hard-rock" mining process. The predominant method of production in Chile is brine evaporation. It is typically less expensive than hard-rock mining. In fiscal year 2022, SQM earned $10,710 mil. USD, of which 76% consists of lithium revenues, totaling $8,153 mil. USD (a staggering increase from lithium segment compared to last year's 936 mil. USD). Other sales consist of industrial chemicals such as iodine, potassium, and others. This growth was primarily attributable to the increase in lithium prices :

Our revenues in 2022 were US$8,152.9 million, a 771% increase from US$936.1 million in 2021, due to higher average prices and higher sales volumes during the year. The average price for 2022 was approximately 462% higher than the average price in 2021. Our sales volumes increased approximately 55% in 2022. Our sales volumes in the lithium and derivatives business line surpassed 156,800 metric tons during 2022, an increase of approximately 55% when compared to the previous year.

SQM Quarterly Sales volumes & price (SQM - Investor presentation)

{kind=link}

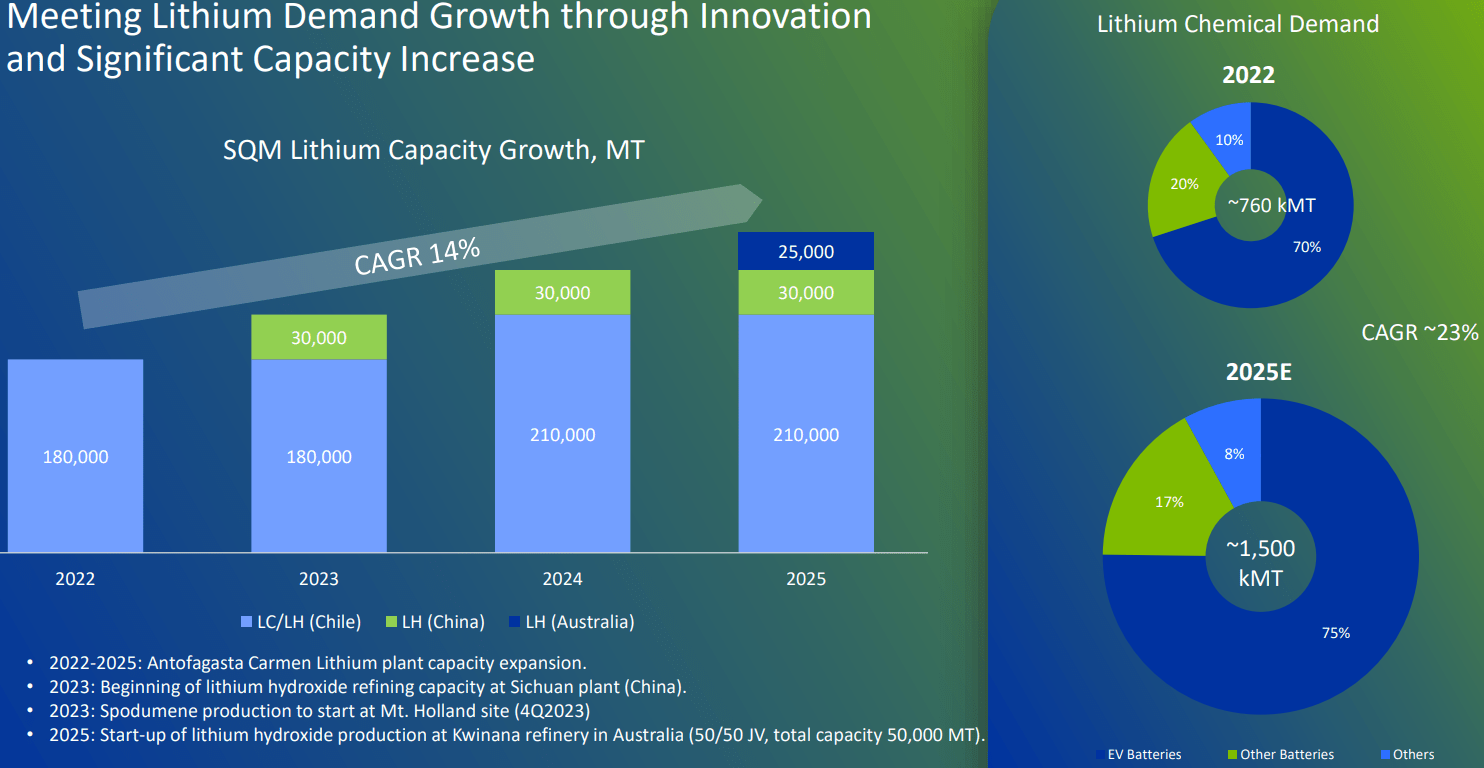

From 2022 to 2025, SQM anticipates a 14% CAGR increase in its lithium capacity, driven primarily by the additional capacity beginning in 2023 as a result of the China plant (30 000 mt in 2023 and 25 000 mt in 2025), and by new production at the Kwinana refinery in Austria. However, this CARG is insufficient to meet the trend of global demand. According to SQM, the trend will reach a CAGR of 23% by 2025, which differs slightly from the IEA's previously projected CAGR of 26%.

SQM Lithium Capacity Growth (SQM - Investor presentation)

{kind=link}

Looking for a nationalization threat of Chile, potentially assuming that contract will expire in 2030 and further contract could be conditioned by public-private ownership, where the national authorities would own the majority - 51%, it would mean that the group's subsidy, which relates to profitability, became less efficient, but also accounts for decreased profitability. In the worst-case scenario, as the state would become the owner with the largest stake, it could replace the management, which could be influenced by politician interests, but it could also approve significant dividend hikes and stretch the pay-out ratio as far as possible to generate additional revenue for budgetary needs.

In the worst-case scenario, the Chile lithium plant's cash generation could be very low, leaving less room for additional CAPEX on other projects. I would consider some state stake to be logical, but I do not believe that the majority is appropriate. However, it is not a done deal as there is sufficient time to resolve the situation, as well as for future international projects in Australia and China, so the group's financial statements could become less reliant on Chile. So began the SQM diversification, but this may allow for a more stringent valuation of the company. Nevertheless, it is a slightly more speculative play than Albemarle, but as stated, the group results are very strong, and the group possesses high quality. Even after 2030, I believe the situation will not be as dire as it appears, but these risks should be considered. In conclusion, this threat exists and should have a significant effect on profitability, but other plants should remain intact. Alongside iodine, potassium, and other industrial chemicals, the company also operates lithium plants in Australia and China.

Albemarle Corporation

ALB has a significantly more diversified portfolio of operations, as it is headquartered in the United States (Silver Peak - production phase, Kings Mountain - development phase) and also has operations in Australia (Greenbushes with 49% ownership and Wodgina with 60% ownership) and Chile (Salar de Atacama). From this perspective, the regulatory framework is more advantageous for ALB due to the diversification of risks across multiple nations and the limited threat of nationalization or potential disruptions resulting from domestic politicians. Albemarle with SQM are currently the market leader for lithium, as they hold the largest share. The company's net sales increased by 120% YoY to 7,320 mil. USD (3,328 mil. USD as of FY 2021), with the segment contributing 68% (41% in 2021) of total revenue. In this regard, the revenue structure is also more diverse than that of SQM. SQM utilized the lithium wave more rapidly and effectively than ALB, as evidenced by its significantly greater production increase.

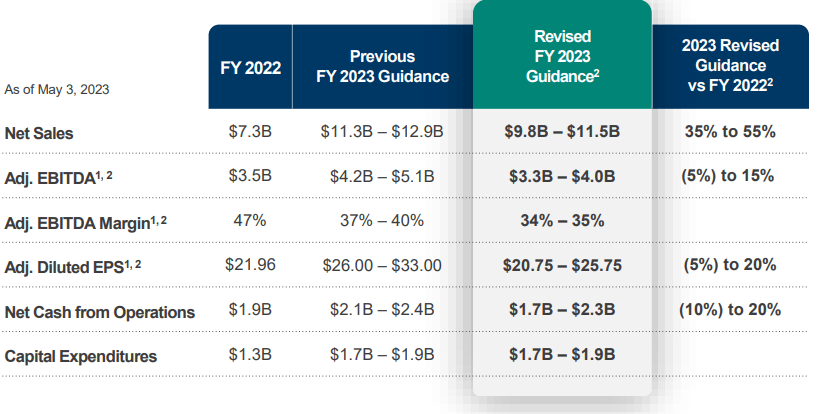

The company also provided revised guidance for the fiscal year 2023, which was significantly lower than the previous forecast due to the precipitous decline in lithium prices. However, such guidance was provided at the beginning of May, just before the bottom was spotted. As a result, based on the price, I do not anticipate a price-driven downward revision in the second quarter of fiscal year 2023, as further declines have been limited. However, the outlook for demand and supply will be most intriguing.

Albemarle Corporation - FY 2023 Guidance (ALB - Presentation)

{kind=link}

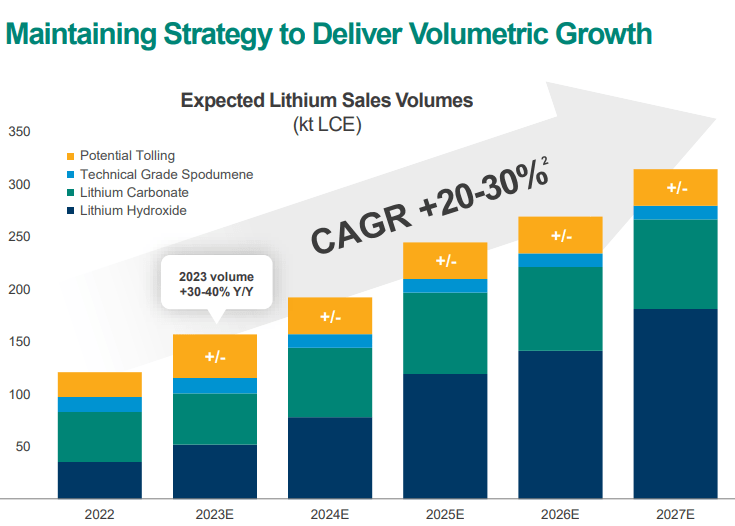

As a result of the ramping up of new capacity, however, it is anticipated that volumes will increase by 30-40% YoY. Albemarle Corporation anticipates a 20 to 30% CAGR in its lithium sale volumes (kt LCE) through 2027. This estimate takes into account the time required to ramp up a new conversion plant as well as the expansion of Silver Peak, La Negra, Kemerton, Qinzhou, and Meishan. Due to numerous uncertain variables, they estimate CAGR rates of 20-30% (for 5 years).

Expected Lithium Sales Volumes (Albemarle Corporation - Presentation)

{kind=link}

However, these volumes are absolutely astounding, and even with significantly lower lithium prices, say 20-30%, they could completely halt the market's growth. Yes, profits would decrease, but this is not the industry near B/E. In 2019 and 2020, when lithium prices were substantially lower due to other business segments, the EBITDA margins of both companies were robust. In the future, the company's earnings per share ((EPS)) should increase significantly as a result of a significant increase in volume, which the company fully benefits from.

Valuation and Balance sheet examination

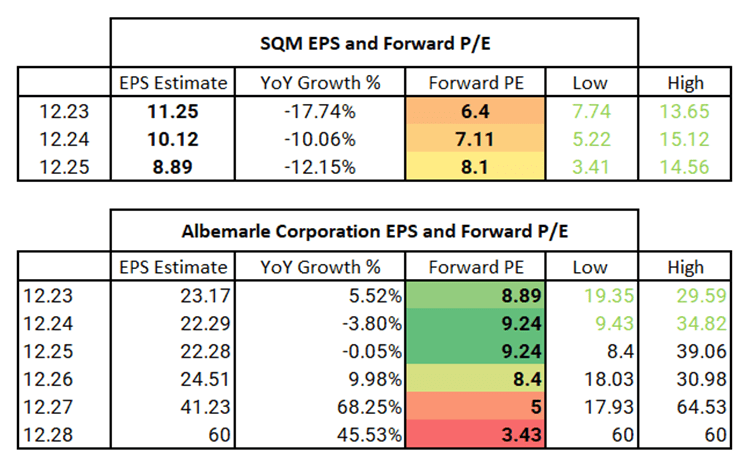

To determine whether a company's outlook is optimistic or pessimistic, I believe it is essential to examine both the trend of earnings revisions and its projected EPS for the following years. While SQM's next EPS trend until 2025 is stagnation, followed by a slight increase, and then a significant decrease after 2030, Albemarle's trend is continuously increasing. Albemarle received a 20-30% premium for forward PE (compared to SQM) pricing as a result of a less risky political environment resulting from its projects' greater diversification and higher growth. As a reminder, SQM expects its production to increase by 14% CAGR, while Albemarle anticipates an increase between 20% and 30%. However, the company's profitability is anticipated to increase significantly after 2027. In addition, other strong contributors to Albemarle's business model and other streams existed even in FY 2022. SQM is currently more "lithium-dependent" than Albemarle, despite the fact that its business model is extremely stable and its revenue streams are also extremely promising.

SQM and ALB Forward PE (Author via Seeking Alpha)

{kind=link}

I see substantial price reductions in both companies, but there is one that I prefer. Consider the Low-High EPS range for the next three years. Such ranges are exaggerated. Some analysts anticipate that the price of lithium will increase, whereas others anticipate that it will decrease significantly. In my opinion, it is unquestionably advantageous for the investor, as lower EPS risks pose a smaller threat than the market currently anticipates. Future earnings could easily exceed projections if the deviation is so significant. I am convinced that thanks to the long-term EV trend, both companies have enormous opportunities.

There are differences between the balance sheet and cash flow of each company, which is completely logical. In my opinion, both companies have very strong financial health, but SQM's results are superior. The quick ratio is higher than average at 1.7, which is very strong, so any potential short-term headwinds should not be a major concern. Fairly, it was pre-dividend, which totaled $0.51 per share and could total up to $352 million USD, so the updated quick ratio should be below 1.50 (or lower, depending on exact formula). However, the trend is falling sharply, but the value is still very good. Albemarle's quick ratio is sufficient.

The cash flow statement is where I observe a material distinction. While both were cash cows for FY 2021 and FY 2022, I prefer the Albemarle approach. This is because the company used the cash for additional CAPEX and investments totaling 1.73 billion USD TTM, whereas SQM "only" made investments totaling 659 million USD TTM. Albemarle utilized its cash for, in my opinion, a more beneficial purpose, such as R&D, CAPEX, more projects, more new ownerships, etc. This is another reason why the company will grow significantly faster in the coming years. On the other hand, as evidenced by the cash flow from financial activities, SQM opted to lavishly reward its shareholders with dividends. Instead, Albemarle emphasized growth and other opportunities, resulting in increased CAPEX.

Considering the tangible book value of both companies, I would say that SQM operates even more efficiently. Albemarle's growth trend in tangible book value is slightly higher, but this is primarily due to cash and equity outflows caused by dividend payments in SQM (=more outflows from book value). Importantly, both book value and tangible book value will increase significantly over the next few quarters and likely years. Therefore, there will be value creation.

I consider the debt positions of both companies to be very healthy. SQM's ratio of debt to assets was 28%, whereas Albemarle's was only 19%. In other words, 28% and 19% of assets are financed through debt, while the remainder is financed through successful business model, or equity. This is absolutely ideal.

Summary and risks

To begin with, I'd like to welcome both of these companies into my high-quality screener. Both satisfy business quality conditions, but their momentum is poor. Although it is anticipated that the company's next one to two quarters will experience a decline in EPS due to the falling price of lithium, these headwinds will diminish over the coming years. Despite the risks that were described in detail, I consider both of these companies to be solid opportunities.

In conclusion, inclusion in my high quality screener is a helpful starting point. Moreover, I view the long- and medium-term industry trend as being very positive due to EV. There will be short-term headwinds throughout the entirety of 2023. However, I do not anticipate a substantial deviation from the long-term trend. The only scenario that could produce such a result is a recession, which could cause a 20–50% decline in lithium prices and a reduction in long-term volumes. In the medium term, however, the EV trend and electrification are the future, and both companies are ideal candidates for this. In the past year, there was a FOMO effect that drove the price of lithium through the roof. However, even if negative supply/demand imbalances persist, the price may normalize in the coming year. While CAGR volumes are estimated to increase by 14% for SQM and 20-30% for Albemarle, it should be sufficient to meet market demand. I am aware that there are many more companies producing lithium, but these are the largest. Due to cyclicity, I do not anticipate a significant deceleration in the price of lithium in the near future, perhaps 10 to 25%. Nonetheless, the most important factor is that production volumes will increase significantly in both companies, which should mitigate any further price reductions. Even with the knowledge that margins will decline in the upcoming quarters, margins could be still strong and lead to solid profits.

Regarding balance sheet health, both companies are in excellent shape. From this perspective, SQM is preferable because it has a higher quick ratio, and thus more working capital for liquidity needs, strong net debt results, and room for investments or dividend payments. Albemarle also has a strong balance sheet, primarily due to low debt levels and a solid liquidity position.

SQM is significantly undervalued based on forward PE ratios for the next two to three years, which range from 6 to 8x. The market has discounted the future EPS trend, which I believe is inappropriate. On the other hand, the market has fully incorporated nationalization risks into discount factors. While these threats are real, they are not the only reason for the market's poor pricing. The second reason, in my opinion, is the anticipated growth restriction due to stagnant EPS estimates for the coming years. Seeing the growth potential, (which is lower than Albemarle's) I firmly refute this belief. In the case of Albemarle, I am more confident in this selection due to its faster and safer growth, very limited nationalization risk due to the lengthy maturity of Chile's contract, and substantial investments that will pay off. As stated previously, there are substantial differences between the low and high EPS estimates of both companies, which is highly advantageous. These differences are a result of the significant estimation disparity. Due to the cyclicity of the industry, future lithium price pressures could be downward, which would make the stocks even more attractive.

If you would like to read a more focused macro article, then you can link to my previous work here , focusing on the technology sector. In the case of stock-picking, I believe there are great companies that are worth reading about, such as PayPal ( PYPL ) or an already-paying-off bank , with very strict risk criteria.

For further details see:

Albemarle And SQM: These Amazing Stocks Entered High Quality And Bad Momentum Screener