SQM - Albemarle: More Pain Short Term

2023-11-29 07:00:00 ET

Summary

- Attractive valuation faces earnings headwinds.

- Supply contracts smooth out spot price volatility for a time.

- I estimate three more quarters of declining earnings.

- The LCE sector does not know what is driving destocking.

Summary

I have updated Albemarle ( ALB ) estimates to factor in LCE price stability in the 2H24 as the company sees contracted prices decline to more closely reflected spot or market prices. In addition, I assume volume growth of 30%, as indicated by the most recent company guidance , and margins below 30% for the full year 2024. While this results in a price target of US$170 at 12x PE it is likely the next 3 quarters the company will report declining earnings, which warrants a Hold rating.

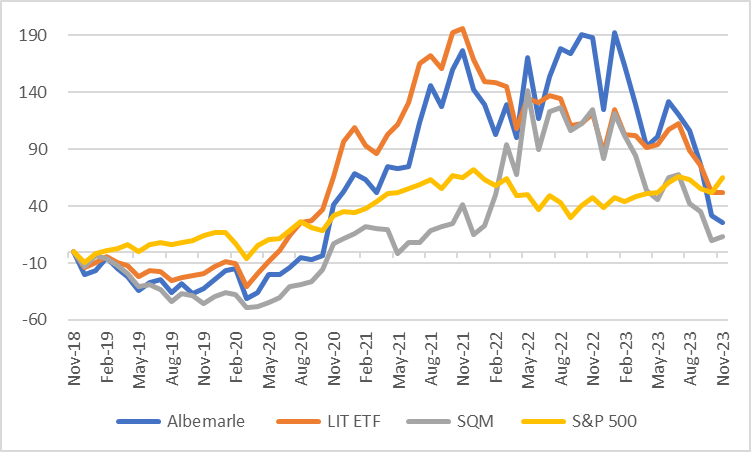

Performance

The stock has given back a large chunk of its gains. However, prices nearly peaked in 2021 before the rise and fall of LCE prices in 2022 -2023. The valuation had risen to over 60x PE when the company sold assets and settled legal suites. The decline in 2023 has been driven by LCE prices, which due to ALB contract structure takes time to fully reflect in results.

ALB Price Performance (Created by author with data from Capital IQ)

{kind=link}

Guidance is Key

Albemarle is not an easy company to model, this is due to poor disclosure of actual volumes, prices, and costs that the company cites for strategic reasons. In addition, it is not a fully integrated Lithium Carbonate producer, it acquires Spodumene or hard rock lithium concentrate from Talison Lithium, which is 49% owned and not consolidated, that is then used in its chemical processing plants for LCE production. Thus, reported revenue and operating margins are more similar to a chemical LCE converter than an integrated LCE company such as Sociedad Química y Minera de Chile S.A. ( SQM ). However, earnings include the 49% net income reported by Talison as equity income. ALB then cites its adjusted EBITDA as part operations and part net income. This means that investors cannot easily determine what actual costs and margins are and depend on company guidance for long-term forecasts.

ALB Reported EBITDA (Created by author with data from Capital IQ)

Prices and Contracts

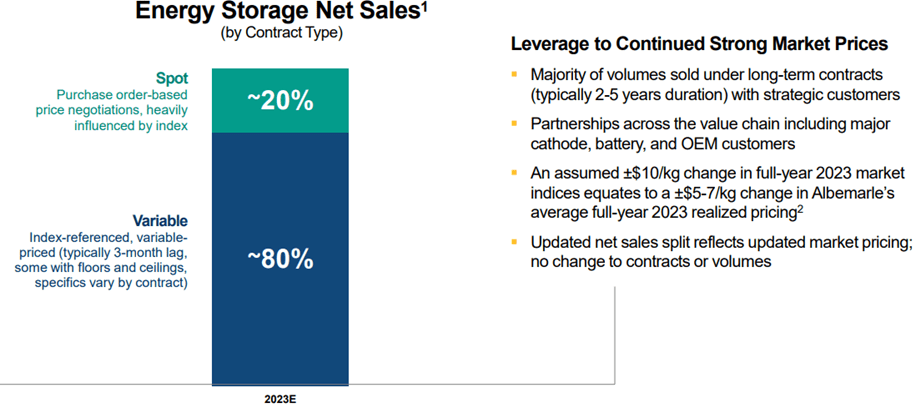

The company has seen better realized LCE price due to its customer contract terms that have 3-month lags and price floors. This has softened the impact of the LCE drop but will nonetheless reduce revenue and /or margin into 2024 even with flat spot LCE prices.

ALB Contract Terms (Image by ALB)

{kind=link}

Short-Term Pain

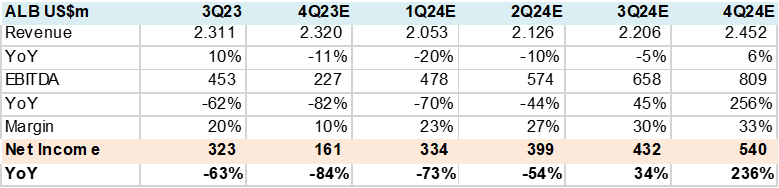

In the 3Q23 results call the company stated that it expects volumes to grow 30% and adjusted EBITDA margins to recover to 30-35% in 2H24 as the LCE inventory destocking ends and more normal supply-demand dynamics return.

However, 4Q23 and 1H24 may continue to be impacted by lower LCE prices and high Spodumene feed costs that are plaguing its chemical conversion margins. Thus, unless LCE prices rise from current levels the company may report weak results through 1H24.

ALB Quarterly Estimates (Created by author with data from Capital IQ)

{kind=link}

Valuation

Given the distortions in EBITDA due to the Talison JV I value ALB on a PE basis, this better captures growth and cash flow. I am using a 12x PE multiple that is in line with the 10-year average and before the LCE price spike and decline. My price target of US$175 to YE24 points to 46% a sharp cut from my previous target of US$235. However, given an expected weak next 3 quarters, even with flat LCE prices, the stock is a Hold.

ALB Financial Summary & Valuation (Created by author with data from Capital IQ)

Consensus

It is difficult to call market estimates a consensus given the very wide disparity of estimates from mean, high, and low. This means analysts are either behind the curve in updating models, very negative or very positive concerning the LCE demand/supply dynamics. My estimates assume LCE prices are close to the bottom and may stabilize at US$18kg.

ALB Consensus Estimates (Created by author with data from Capital IQ)

Conclusion

I rate ALB a Hold (from BUY). The company's contract terms and cost input dislocation may hurt results through 2Q24 which limits investor appetite despite expectations of a 2H24 and forward earnings recuperation. A better entry or cost average down, point may appear.

For further details see:

Albemarle: More Pain Short Term