ALB - Albemarle Vs. SQM: Better Lithium Investment

2023-07-25 07:30:00 ET

Summary

- The global lithium market is expected to grow more than 20% through the rest of the decade due to increasing demand from the electric vehicle (EV) industry.

- Two of the largest lithium stocks, Sociedad Química y Minera de Chile S.A. and Albemarle Corporation, are well-positioned to benefit from this market growth.

- While SQM has a stronger balance sheet and higher growth, ALB is more geographically diversified and could be seen as less risky from a political standpoint.

Article Thesis

Lithium stocks have gotten a lot of attention in the recent past, and it is pretty clear that the ongoing growth in the electric vehicle space will make for ample industry growth potential over the coming years and likely decades. Two of the largest lithium stocks are Sociedad Química y Minera de Chile S.A. ( SQM ) and Albemarle Corporation ( ALB ). In this article, we will evaluate their pros and cons for investors.

Lithium Market Overview

Lithium is a chemical element that can be described as a soft metal. It is being used in many batteries, including those used in smartphones, notebooks, tablets, and so on. Importantly, lithium is also a key commodity for the production of the batteries that are used to power electric vehicles. Since the capacity of these batteries is incredibly high relative to the capacity of a battery used to power a phone, the growth in the global electric vehicle market results in huge growth in global lithium demand. A growing EV market is the most important growth driver for lithium demand for the foreseeable future, even though the element is also used in many other products.

Some estimates see the global lithium market at around $38 billion in 2022, with projections for a market growth rate of more than 20% through the remainder of the decade, which would translate into a market size of around $90 billion in 2030. Whether these projections come true, or whether actual growth will be a little higher or a little lower remains to be seen, but it is pretty clear that lithium demand is growing rapidly, and that this already sizeable market will expand massively through the remainder of the decade, and likely way beyond, as the EV market will most likely continue to expand in the 2030s as well, while overall technological progress makes it likely that more batteries will be used in other areas as well (e.g. for AR/VR gadgets).

A fast-growing market means that companies that are well-positioned to benefit from said market growth could be attractive investments. We will thus take a look at two of the leading lithium players in the world today, Sociedad Química y Minera de Chile S.A. -- valued at $21 billion -- and Albemarle Corporation, which is valued at $25 billion right now. It is important to note that lithium prices have been very volatile in the last couple of quarters, and this could hold true in the future, too. This results in some ups and downs when it comes to the revenues and profits that major lithium players are generating, even if volumes are flat or growing.

Company Overview: SQM And ALB

Both of these companies are active in the lithium market, but that is not their sole purpose. Instead, both companies operate other business units as well, although those may be less important in the minds of some investors, as the non-lithium businesses are generally growing at a slower pace than the lithium business units. Still, taking a look at these other assets is important.

SQM is active in potassium (used for fertilizers), iodine (used in foods, tech, and medicine), and lithium, while SQM also has some smaller business units. Lithium is the major growth driver, and thanks to its position in Chile, which has vast lithium resources, SQM is well-positioned to grow its output in the future.

Albemarle is active in different industries as well, including a range of specialty chemicals. Its divisions include Bromine (with end markets such as food, industrial, and energy), Lithium, and Catalysts (with diverse end markets).

Lithium is not the sole source of revenue for these companies, but due to the expected massive growth, it will be the primary source of revenue growth in the coming years, as the other businesses can be seen as slower-growing cash cows. SQM, for example, generated around 60% of its sales growth in the lithium business during the most recent quarter. Their cash flows and profits are still highly important, as these proceeds can be used to fuel growth in the lithium business, where considerable capital expenditures are required to start up new projects that can have multi-year lead times.

Lithium Strategy: SQM And ALB

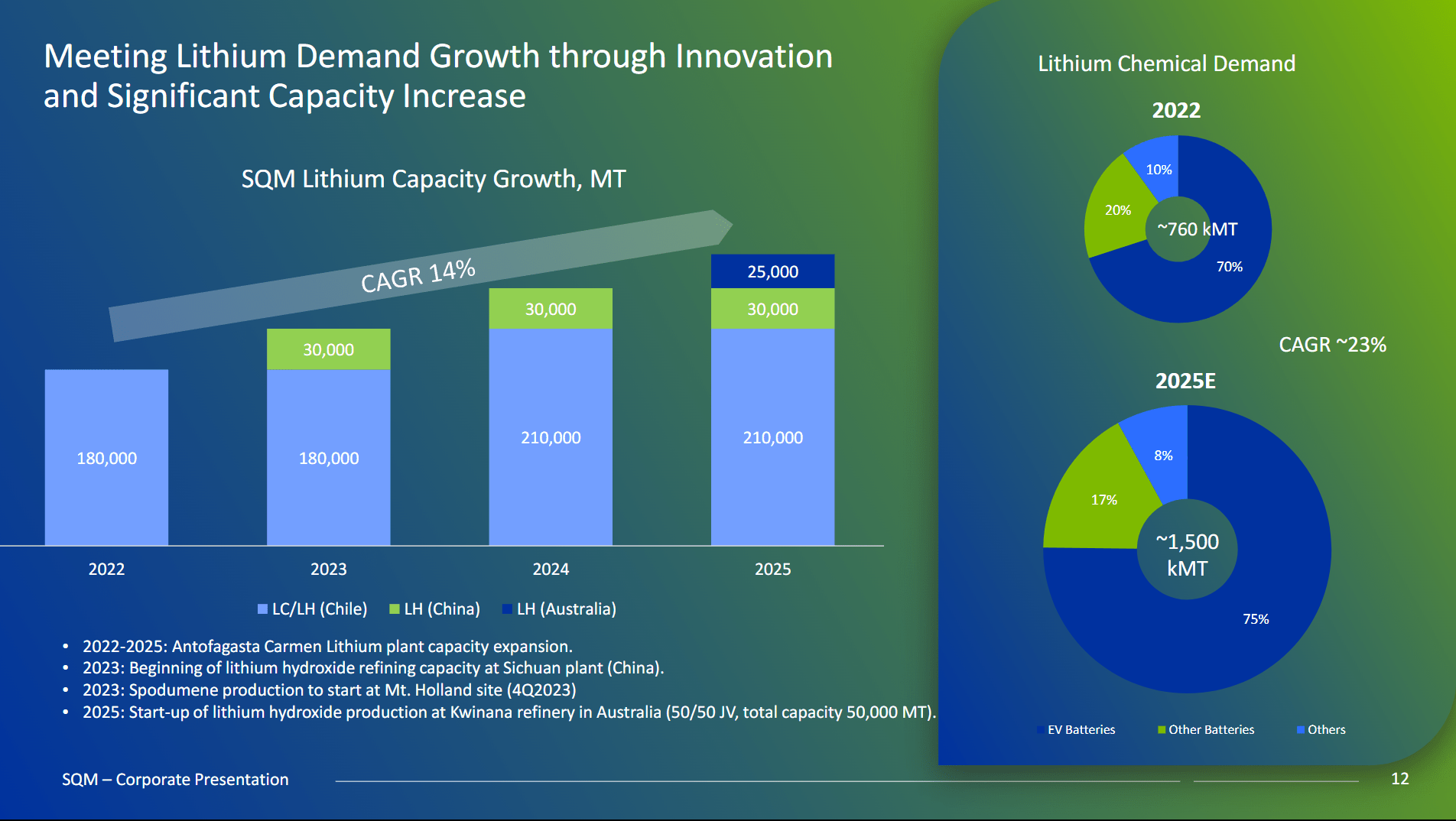

SQM's name already suggests that the company is primarily active in Chile, and that is where all of SQM's lithium is being produced for now. The company has some growth projects in China and Australia, and those will generate a rising portion of overall volumes, but even in 2025, around 80% of SQM's forecasted volumes will come from Chile.

SQM forecasts considerable business growth in its lithium space, showcased by the following slide from a recent investor presentation:

{kind=link}

SQM presentation

A mid-teens annual capacity growth rate should result in compelling revenue growth. Depending on where lithium prices are headed -- some analysts forecast considerable price increases due to massively growing demand -- the revenue growth rate could be well ahead of the forecasted volume growth rate, which is attractive by itself already.

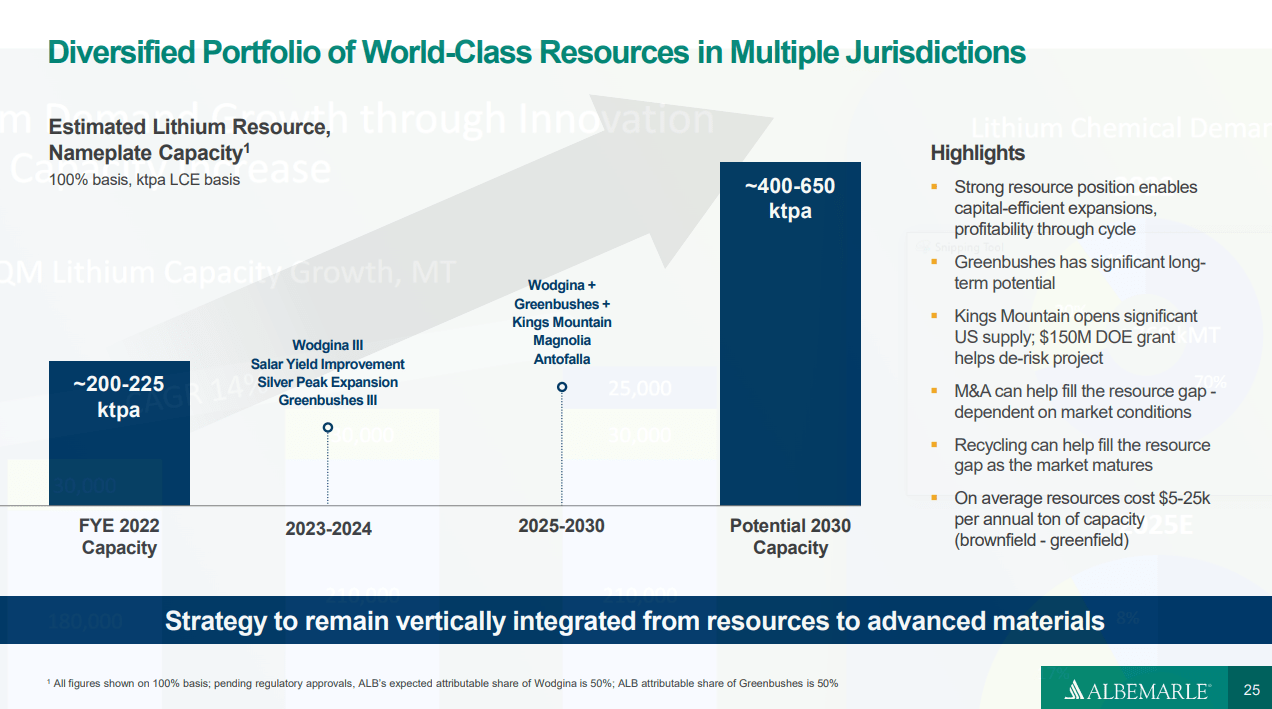

Albemarle is forecasting a marginally slower production capacity growth rate, as we can see in the following presentation slide:

{kind=link}

ALB presentation

Looking at the guidance midpoint for 2030, Albemarle is forecasting a volume growth rate of 12% through the end of the decade. That's slightly slower than the growth rate implied by SQM's forecast, although it is important to note that ALB is forecasting that this growth will be maintained for a longer period of time. If ALB's volume growth is frontloaded -- which could make sense, as a high relative growth rate is easier when the business is smaller compared to when it is larger in absolute terms -- it would not be surprising if ALB and SQM both grow at a mid-teens rate in the next couple of years.

Albemarle is less focused on Chile compared to SQM, which makes sense, as Albemarle is not a Chilean company. Nevertheless, Albemarle also owns extensive assets in Chile, which can be explained by the country's vast resources. Albemarle is also active in the US, China, Australia, and so on. Due to its business being more diversified from a geographical perspective, Albemarle could be seen as a company that is less at risk from a regulatory or political standpoint -- some investors are worried about potential nationalization of lithium assets in Chile, for example, and SQM would be more heavily impacted if that were to happen (I believe this is unlikely, but one never knows).

Both companies plan to grow fast, with SQM potentially growing a little quicker in relative terms, while ALB has the advantage of being more diversified across different jurisdictions.

Fundamentals: SQM And ALB

Both companies have enjoyed compelling business growth in the recent past, and investors have benefitted a lot from that:

SQM has turned a massive 520% revenue increase over the last three years into an incredible 1,550% EBITDA increase. Shares delivered a total return of 190% over that time frame -- or 43% per year. The fact that SQM's share price rose a lot less than its EBITDA can be explained by multiple contraction -- as lithium operations are ramping up, the earnings multiple declines, at least to some degree.

Albemarle delivered revenue growth of 170% over the last three years, and showcased EBITDA growth of 430% -- a lot less compared to SQM, but still a very strong result. Total returns were in the 150% range, which pencils out to around 35% per year.

In absolute terms, SQM is somewhat bigger compared to ALB, with revenues that were around 20% higher over the last year.

Looking at the two companies' debt levels, we see that SQM has net financial debt of $300 million, with Albemarle having net debt that is around 5-6x as high. But even Albemarle does not have threatening debt, considering it generated EBITDA of close to $4 billion over the last year, which makes for a net leverage ratio in the 0.5x range -- which makes for a pretty clean balance sheet. SQM's balance sheet is even stronger, however.

SQM's ultra-strong balance sheet allows it to pay out hefty dividends, as we can see in the following chart:

The trailing twelve months dividend yield of SQM is 12.2%, but it should be noted that dividends are very volatile. Annualizing the most recent payout of $0.79 gets us to a dividend yield of 4.4%, thus investors may see a substantially lower effective dividend yield over the next year compared to the last twelve months. Even a 4% yield from a fast-growing company is pretty attractive, however. Albemarle offers a way lower dividend yield, as it operates with a pretty low payout ratio of just 7%. That makes Albemarle's dividend ultra-safe, but ALB does not offer a compelling income stream for now. It has raised its dividend for a very nice 28 years in a row, making it a Dividend Aristocrat. But for those that want a sizeable income yield now, ALB, unfortunately, is not very attractive, as Albemarle reinvests the majority of its cash flow back into its business.

Looking at the two stocks' valuations, we see the following:

Based on forecasted EBITDA for the current year, Albemarle is close to two times as expensive as SQM -- even though Albemarle looks rather inexpensive in absolute terms. SQM is very inexpensive in absolute terms, however. The valuation discount can most likely at least partially be explained by some investors' worries about investing in a Chilean company and the political risks this could bring.

SQM Versus ALB: Which Is Better?

On paper, looking solely at the numbers, SQM looks like a better deal than Albemarle: Equal or faster growth, a lower valuation, a stronger balance sheet, and a substantially higher (although fluctuating) dividend yield. But I can also understand those that worry about potential political risks -- Albemarle, with its more diversified assets, seems like a lower-risk pick from that perspective. Overall, I think both companies could be attractive over the coming decade. I own Albemarle and might add a position in SQM in the future.

For further details see:

Albemarle Vs. SQM: Better Lithium Investment