ALC - Alcon: Buy An Eyecare Leader With $2 Billion In Quarterly Sales

2023-10-10 13:03:27 ET

Summary

- Alcon gets a Buy Rating today, in line with Wall Street consensus.

- Strengths include earnings growth, share price crossover below 200-day average, outperformance vs. the S&P500 index, and the company's strong cash position.

- Offsetting factors include a high valuation and poor dividend yield.

- The downside risk of debt levels was also addressed.

Analysis Summary

Today I'll be covering Alcon (ALC) , in the healthcare sector, subsector of healthcare supplies.

According to its Seeking Alpha profile, it trades on the NYSE, is based in Switzerland, and is a company that researches, develops, manufactures, distributes, and sells eye care products for eye care professionals and their patients worldwide.

One of its listed peers is Bausch + Lomb (BLCO).

My personal experience with this company has been in using their eye drops many years ago, and often seeing the brand as a common fixture in the eyecare aisle of the store. After all, writing articles online can sometimes lead to dry eyes!

But seriously, today I am taking the angle not of a customer but that of a potential investor, so I call this analysis something like "360 degree vision" of multiple aspects of this stock.

In today's article, I gave this stock a buy rating, due to having more strengths in my review than offsetting factors.

Its strengths include revenue growth, net income growth, capital/liquidity strength, current share price crossover below the moving average, and outperformance vs S&P500.

Its offsetting factors include a paltry dividend yield and overvaluation vs its sector.

A downside risk to my bullish outlook is increasing debt loads, which will be discussed.

Methodology

My updated rating methodology is to analyze the stock holistically across the following 7 categories of equal weight, and if it has more strengths than offsetting factors it gets a buy rating, otherwise will get a hold or sell rating:

dividends, valuation, revenue growth, net income and EPS, capital and liquidity, share price vs moving average, performance vs S&P 500.

All data sources come from publicly available info such as the most recent quarterly report on Aug. 15th for FY23 Q2 and company presentations, Seeking Alpha data, and media reports. The next anticipated quarterly earnings release is expected on Nov. 15 for FY23, Q3.

Dividends

Here I discuss the dividend yield , 10-year dividend growth, and dividend stability over the last few years. As a dividend-focused analyst and investor, I believe these are vital metrics to look at.

Though not all investors are dividend-oriented, including many of my readers, I do think generally speaking it can be a way to generate cashflow while holding equity longer-term.

Unlike some of my recent articles, I do not have great praise for this stock's dividend offering, and will show you why.

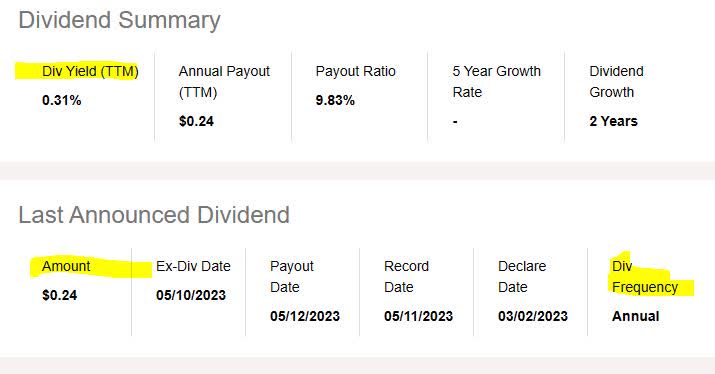

First, let's look at the dividend yield , which is 0.31% as of the writing of this article, along with a dividend payout of $0.24 per share, on an annual basis.

{kind=link}

Though a yield below 0.50% seems miniscule, whether or not I think it is a good yield depends on how it compares to the industry it is in.

In comparison to its sector average, this yield is 81% below the average, both on a trailing and forward basis. I consider this a negative point as I am looking for a yield between 1.5% and 3% when considering the sector/industry, so this stock has a yield that is much lower than my goal.

I consider yield important because it tells me a story: how much of a return I am getting on the capital invested, in terms of dividend income. A sudden drop in share price, as you may know, can result in a higher yield if the dividend amount remains the same.

Alcon - dividend yield vs sector average (Seeking Alpha)

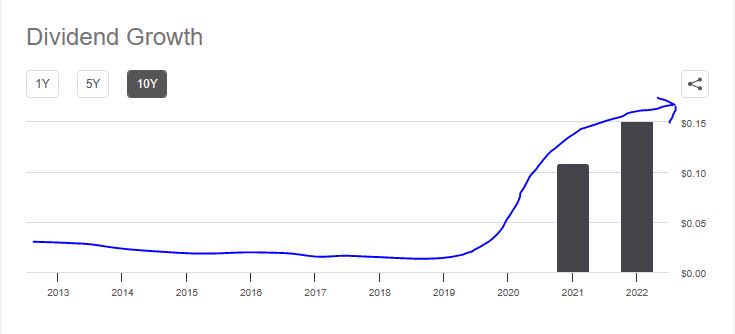

Next, I am looking at the 10-year dividend growth rate, shown in the chart below, which shows a long period with little to no dividend payouts followed by a growth spurt. I think that is a moderately negative point as it does not provide enough historical data on this stock's dividend growth. The dividend story here is one of late growth it seems.

{kind=link}

Finally, I want to see dividend payout stability, especially if you are relying on the steady quarterly cashflow. However, this is an annual dividend and not a quarterly one, so you would have to wait for the next ex-date which is not until next May probably.

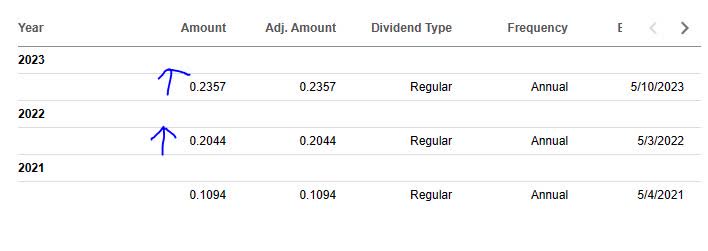

In looking at the table below, you can see stable annual payouts over the last few years, with 2 dividend increases in this time period, but also only three years' worth of history to go by.

A cashflow scenario: if I was holding 1,000 shares, for example, I could realize $235 in annual cashflow from the dividends on this stock. (1,000 shares x $0.235 per share). That comes to about $59 per quarter.

{kind=link}

Based on the evidence, I consider the category of dividends an offsetting factor for this stock, on the basis of the lack of enough dividend growth history to date, annual payouts rather than quarterly ones, and a yield far below its sector average.

Valuation

To simplify analyzing the valuation , I have chosen a single metric to focus on, and that is the price-to-earnings ratio (P/E) , both the trailing and forward P/E, as it tells me what the market is pricing this stock at in relation to its earnings.

My portfolio goal is to find a valuation lower than or close to the sector average, but not too much higher. Sometimes a stock is undervalued but otherwise has strong fundamentals, so that is a company I want to uncover.

Alcon - PE ratio (Seeking Alpha)

In the case of this stock, the trailing P/E is 103.56, which is 268.6% above the sector average, and the forward P/E of 54.03 is 108.5% above the sector average.

Hence, I would consider this stock considerably overvalued compared to its industry, both on a trailing and forward basis.

If you compare its valuation to that of its peer, Bausch and Lomb , that firm's non-GAAP forward P/E is around 27% higher than the sector, so although it is overvalued it is not as much as Alcon is.

As to what is driving such a high valuation, it could be the market is willing to pay 50 to 100x earnings for this stock because it is highly confident in its earnings potential.

According to a topic article by brokerage Charles Schwab , it has to do more with perception :

Enthusiasm on the part of investors can lead to P/E expansion—a period when investors' perceptions of a company improve , and as a result, they are willing to pay more for a dollar's worth of earnings.

Later in this article, we will go over earnings and share price.

Based on the data, I think this valuation metric is an offsetting factor for this stock, as it makes it appear too overvalued to be a value-buy opportunity.

Revenue Growth

One topic many analysts and investors look at is top-line revenue growth, as a metric tracking revenue generated before expenses, to put it simply.

Manageable growth is important, in my opinion, because companies have competition and are striving to capture market share in their sector.

For this company, we can see from the most recent quarterly results that it achieved a YoY increase in total revenue but also achieved a YoY increase in gross profit as well .

{kind=link}

At first glance, I think this is a plus for this company, which depends on sales of a physical product, such as eye drops, for example.

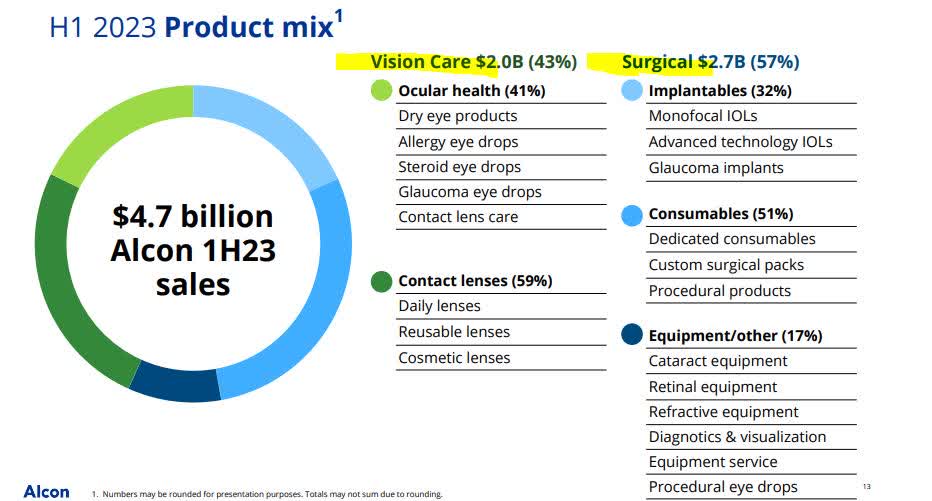

However, it turns out that this brand is highly diversified across a mix of products that have driven strong sales for the first half of the fiscal year, to the tune of $4.7B in sales in the first half of the year alone:

{kind=link}

Overall, I think the data shows that top-line revenue YoY growth is a strength for this stock's rating, and another positive is that the company has raised its full-year sales guidance, according to its Q2 earnings release .

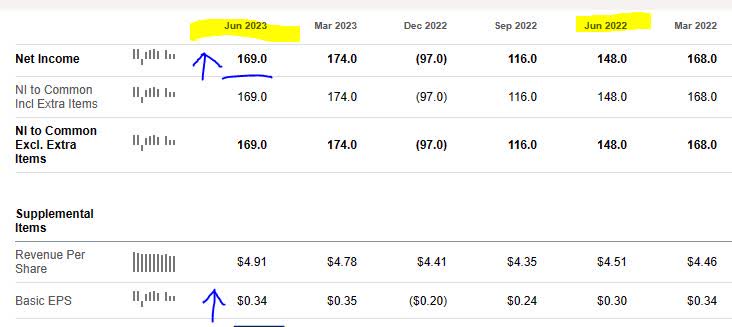

Net Income and EPS

Net income and earnings per share are getting their own section here to make the analysis easier to understand and to separate these results from top-line revenue.

Based on the most recent quarterly results available, this firm achieved a YoY growth in net income and the basic earnings per share increased on a YoY basis.

{kind=link}

On a diluted basis, the earnings per share has also shown positive results, according to the Q2 earnings commentary :

Second quarter 2023 diluted earnings per share of $0.34 increased 13%, or 34% on a constant currency basis. Core diluted earnings per share of $0.69 increased 10%, or 19% on a constant currency basis.

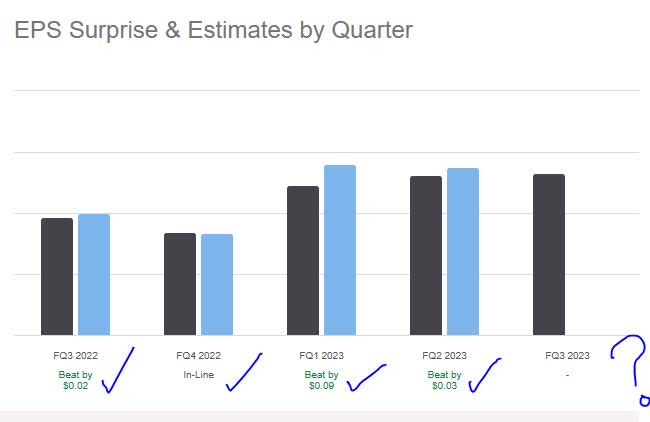

I think, therefore, that this category of net income and EPS is a strength for this stock's rating, and I look forward to a more positive outlook for the upcoming Q3 earnings result coming out in late November. Though I cannot for sure predict the Q3 result, what I can see is that this company has frequently meet or beat earnings estimates :

{kind=link}

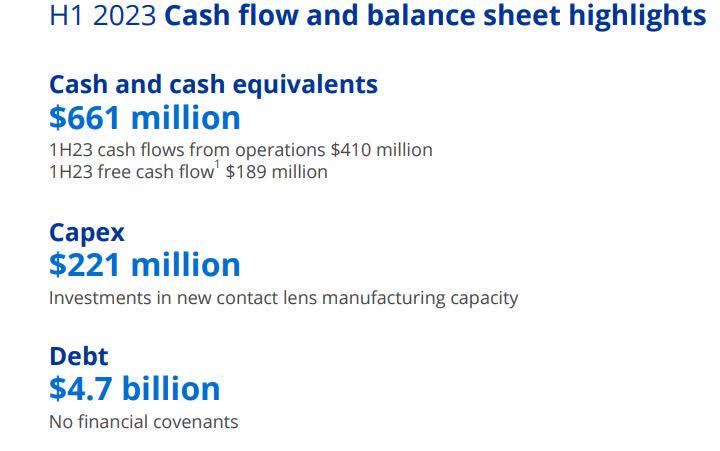

Capital and Liquidity

Here we'll focus on one or more items related to capital and liquidity strength of this stock's parent company.

The following is relevant data from the company's quarterly presentation, which shows a very strong cash position of $661MM.

Alcon - balance sheet highlights (company quarterly presentation)

{kind=link}

Further, here is additional data of interest from their Q2 press release when it comes to cash flow , an important metric I follow and keep mentioning in articles recently:

Cash flows from operating activities for the first half of 2023 totaled $410 million, compared to $470 million in the prior year. The current year includes cash outflows from a legal settlement, higher interest payments associated with increased financial debt outstanding and higher taxes paid due to timing of payments.

One thing that sticks out, and why I highlighted it, was the increase in the interest expense on debt.

From its balance sheet , we can see the company has positive equity of over $19B, which I think is another positive point to bring up.

Based on the evidence found, I consider this firm's capital and liquidity situation a strength to its overall rating, based on positive operating cashflow and a strong cash position as well as positive equity, although I would keep an eye on the long-term debt situation going forward and am hoping they will decrease it in Q3.

Share Price vs Moving Average

Now we've come to the part where I like to talk about the share price and whether I think it's a buying opportunity right now or not.

First, let's take a look at the share price and 200-day moving average ((SMA)) as of the writing of this article:

The share price of $75.56 is less than 1% below the 200-day SMA which stands at $76.23 . I think this moving average is a good long-term trend indicator which is why I track it as it smooths out the price trend over a longer period.

In my portfolio goal, I am looking for crossover opportunities, where the price crosses below the moving average after a period of bullishness, which I consider a buy signal as long as other fundamentals are strong. However, a buy opportunity could also exist if the price is hovering around the moving average.

This chart shows a crossover below the moving average just occurred so to test the share price against my portfolio goals I created the following simulated trade scenario: I will buy 100 shares at the current price, hold 1 year, and want to achieve at least a 10% or better (unrealized) capital gain at that time.

In addition, in anticipation of losses as well, my maximum loss tolerance is--20% (unrealized capital loss). Here is how my trading idea turned out:

{kind=link}

The above simulation shows two scenarios, one where the future share price rises +15% above the current 200-day SMA, and the other where it drops -15% below the SMA.

The outcome of both scenarios is that they are in line with my goals for gains and losses. For example, the first scenario projects a future capital gain of 16.02%, while the second scenario projects a capital loss of 14.25% (within my limit of a 20% loss).

Based on this simulation, I think the current share price is a strength.

Though your portfolio strategy may differ, I consider this section a general and simplified framework with which to think about this stock in a longer-term sense, in which time one can expect potential gains as well as losses, so establishing a maximum risk tolerance is important.

While it is nearly impossible to predict a future share price 100%, I think it is possible to establish risk tolerance "ranges".

Performance vs S&P 500

The following is a comparison of the 1-year price performance of this stock vs the S&P 500 index. I have included this metric in my updated rating methodology so as to compare this equity to a major market index that is tracked often, and whether it was able to outperform it or not.

I consider this relevant because it shows the market momentum for this stock. It may be a great company fundamentally, the market reality is that other investors influence the share price based on demand for the stock, so comparing it to this major index could add some clues as to market sentiment.

{kind=link}

The data shows the stock outperforming vs this index, which I consider a strength to my rating, as I believe it to indicate a bullish market sentiment for this stock. In fact, it has outperformed this index ever since late 2022 it seems.

I think this metric is relevant as it shows this stock's ability to outperform a major market index over a longer term.

Risk to my Outlook

A dow n side risk to my bullish outlook would be an increasing debt level from June 2022 until now, with a $4.6B long-term debt load as of the end of Q2.

{kind=link}

Unlike my recent articles covering banks and insurance companies that earn a very large amount of money from interest-earning assets, a firm like Alcon is in the opposite boat in regards to the current high rate environment, as many other companies, and I think many investors and analysts may turn bearish on its stock if debt levels get too high in Q3 and Q4, which also would impact interest expect on the income statement.

Consider that the issue was brought up in an August article by Nasdaq :

First and foremost, higher debt costs squeeze corporate profits. Firms with a lot of debt are impacted by potential higher interest expense.

Moreover, rising rates dim the economic growth prospects and can impact future returns for companies.

Secondly, rising rates decrease the present value of any business.

My counterargument to the market bears on this stock is that while the debt concerns are certainly warranted, I think that what could offset that risk for this company is the fact that it sells necessary healthcare products and does a fairly large amount of business in that space, to the tune of $2.4B in sales in Q2, so the product demand is there.

Consider the following graphic showing robust growth in sales in their vision care segment, for example:

Alcon - vision care segment (Alcon quarterly presentation)

In closing, my bullish sentiment on this stock remains and my buy rating stands. Although it is slightly more bullish than the consensus from SA analysts and the quant system, it appears to be in line with the Wall Street consensus at this time:

Alcon - rating consensus (Seeking Alpha)

For further details see:

Alcon: Buy An Eyecare Leader With $2 Billion In Quarterly Sales