ALC - Alcon: Case Of Growth Destructive To Value Reiterate Hold At 24x Earnings

Summary

- A firm creates value when its return on invested capital exceeds its cost of capital.

- If it doesn't, regardless of its expansion, growth will become destructive to shareholder value.

- This has been the case for Alcon Inc. over the past few years.

- Hence, despite a breakout above long-term resistance, we believe there's no mispricing on offer.

- Net-net, reiterate Alcon Inc. hold at 24x earnings.

Investment summary

Participating as an equity investor over the broad healthcare spectrum requires unique insights. This could come from [but is not limited to] industry experience, investing experience, managing a portfolio or basket of healthcare securities, or a combination of all three. Nevertheless, the core principles of understanding what constitutes a good equity investment remain the same.

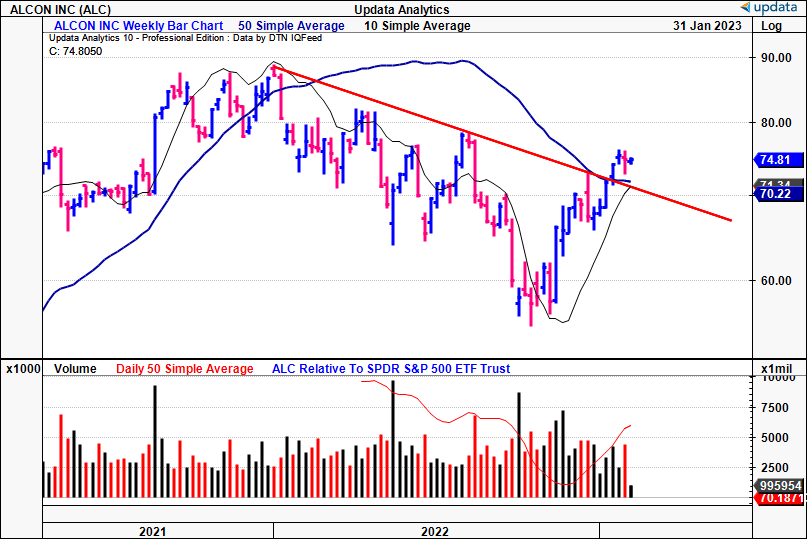

I'm going to run through the underlying framework we took with re-evaluating Alcon Inc. (ALC) after our last publication in September last year [ see it here ]. Back then, we rated Alcon Inc. a hold, asking for the stock to break its longer-term downtrend. This happened in December, and shares are up ~13%. So, it's worth sharing the deeper fundamental analysis we undertook in rating it a hold. We'd note there's scope for the stock to re-rate higher. However, net-net, we reiterate Alcon Inc. stock as a hold for long biased, long-term, fundamental healthcare investors.

Exhibit 1. ALC breakout above long-term resistance

{kind=link}

Underlying concepts in ALC analysis

Growth, free cash flow and return on capital - the tripod of success

Companies want to grow at a specified, yet non-linear growth into perpetuity. Investors want a piece of that growth, but only at a "fair" price, to maximize the upside. The questions being, what is fair, and what is the opportunity cost. For mature companies, the growth profile is harder to come by, not in the least related to sheer size. Mauboussin (2021) quotes theoretical physicist Geoffrey West, who compares the " sigmoidal growth" of companies to that of mammals - after birth, the focus is on expending energy on growth. After time, this molds to a focus on maintenance. It's no different for companies in their mature stage of their lifecycle.

Still, there are a number of ways a company can evolve and expand efficiently, from adding new products, increasing productivity, reducing capital intensity, or decompressing margins. Within this mix, there's also many subcomponents. For instance, Mckinsey & Co. (2017) illustrate that companies focusing on developing new products or services are most likely to see high top-bottom line growth. There's a caveat to this, however. Not all growth is created equally, and all growth comes at a cost.

As an investor, there's also an accounting reality, and an economic one. A firm creates economic value when it generates a return on its investments above the cost of capital, other words, an economic profit ("EP"). There's a major difference between accounting profit [that in which is presented on the periodic financial statements] and a firm's EP.

As investors, we're interested in EP over the former, as a cleaner measure of value. Why? It comes down the mechanics that drive value in the first place: a high return on invested capital ("ROIC"), that exceeds the cost of capital [positive EP], is the quintessential ingredient in the valuation recipe. It means a firm needs to reinvest lower portion of post-tax earnings to grow. It also illustrates it is investing well. Net-net, this means more residual cash [free cash flow, or FCF] is left for equity holders ("FCFE") - the cornerstone of corporate valuation. Charlie Munger, chairman of Berkshire Hathaway, say's it well :

"There are two kinds of businesses: The first earns 12%, and you can take it out at the end of the year. The second earns 12%, but all the excess cash must be reinvested - there's never any cash. It reminds me of the guy who looks at all of his equipment and says, 'There's all of my profit.' We hate that kind of business."

The key thematic of this analysis: if ROIC is less than the cost of capital, then growth is actually destructive to value. Remember this for later.

Alas, accounting profit does a poor job in capturing the hidden cost to equity holders - i.e., the reinvestment of post-tax earnings required to achieve a stated growth rate. Moreover, typical calculations of FCF miss the actual free cash flows that are distributable to equity holders. As a result, 'equity earnings' are often misrepresentative, and FCF is often overstated. It's also worth noting that companies with growth rates less than their ROIC can payout cash [either hypothetical, or in dividends/buybacks] to shareholders without jeopardizing growth.

The market values Economic Profit, so it should

The above preamble in mind, you'll be able to see in the following charts why we continue to see ALC as a hold. Don't get us wrong here - it's great company, with products in the same steed. Plus, it's growing operating income and earnings at an attractive rate. It's the questions of value and fair price that has us on the sidelines.

Here's the premise of the value component:

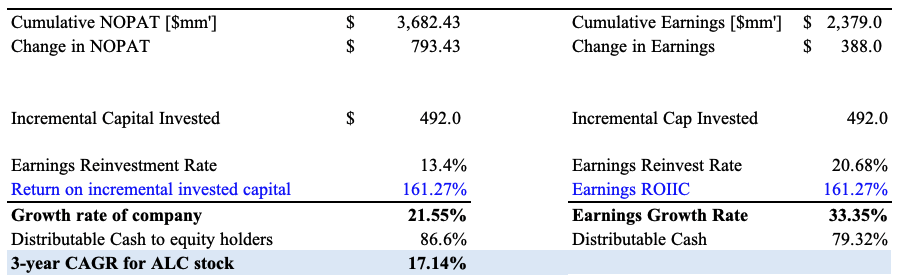

(1). First off, ALC is profitable and is steadily growing with decent operating margins above the sector median. Since listing, its stock has caught a decent bid as well. Looking at rolling TTM periods from Q1 FY20-Q3 FY22', ALC generated a cumulative $3.6Bn in net operating profit after tax ("NOPAT") and ~$2.4Bn in earnings [Exhibit 2]. This corresponded with an additional growth of $793mm and $388mm, respectively.

Exhibit 2. ALC NOPAT and Earnings growth, FY20-FY22' [rolling TTM basis].

Note: Rolling TTM basis is used to provide an 11 period lookback, where each period is 12 months. (Data: Author, using data from ALC SEC Filings)

(2). The returns on these numbers are impressive, as well. To achieve the above growth rates, it only had to invest an additional $492mm in capital, otherwise, 13.4% and 20.7% of NOPAT and earnings respectively. Consequently, it grew 21.5% over the testing period [33.35% of earnings]. As such, the return on incremental invested capital is high at >161%. The market values this kind of growth, hence, unsurprisingly, its stock price compounded at ~17% over time as well. As such, 79% of earnings has been distributable to equity holders.

Exhibit 3. Substantial ROIIC from 13.4% reinvestment rate

{kind=link}

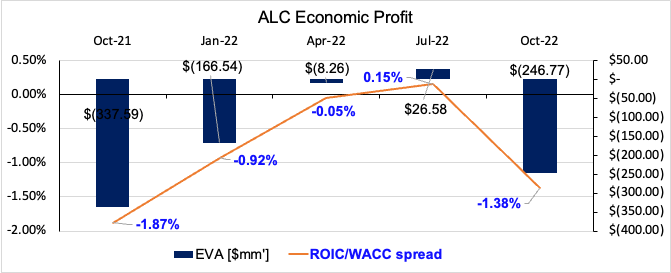

(3). As mentioned earlier, if a company sports a high ROIC, it can create value for shareholders. But remember, this only applies if the EP spread is positive, otherwise, the growth erodes the value to equity holders.

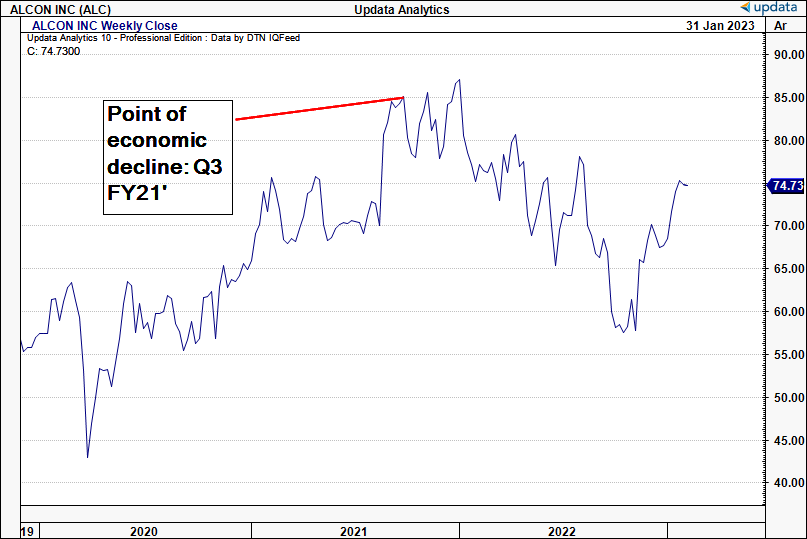

You'll see in Exhibit 4 that, since Q3 FY21 at least, ALC has generated a ROIC less than the hurdle rate. Consequently, whilst it's been able to grow at a high rate, because its periodic ROIC [shown in Exhibit 2] haven't been accretive to its corporate or equity value. In fact, we postulate it's been value-destructive. This is in contrast with the incremental ROIC stated in Exhibit 3. Since Q3 FY21', ALC stock has re-rated heavily to the downside as a reflection of this [Exhibit 5].

Exhibit 4. Negative EP since FY21'

{kind=link}

Exhibit 5.

{kind=link}

(4). It's also worth noting that, when a firm grows faster than its ROIC, it must access external capital to fill the gap - either debt or equity (Mauboussin 2014 ; 2022 ). Because this is the case for ALC, we'd note that ALC priced a $1.3Bn debt offering last November. The issue, set in two tranches, will pay $600mm at a 5.375% coupon and $600mm at 5.750%, due in 2052. Per the release:

"Net proceeds from the offering will be used for general corporate purposes and to repay all or part of the outstanding indebtedness under its term loan facility."

This wouldn't be a problem if its ROIC was above the cost of capital - but we've already demonstrated that it isn't. Hence, it hasn't created substantial shareholder value, evidenced by the market's re-rating of the stock, amid the 2022 bear market.

Negative EP erodes shareholder value

Each of the drivers discussed so far illustrate that ALC's growth has come at a cost to equity holders since FY21'. It's been great for the company, not so much for those holding its stock. We demonstrate this in the below example.

An investment is "worth it" when the present value of its future cash flows are greater than the cost of the investment. As equity investors, we measure this by the future stream of cash flows we are entitled to, discounted at an opportunity cost of capital, otherwise, the cost of equity. Richards (1991) provides we can use a derivation of the earnings yield and growth rate, totaling ~24% in ALC's case.

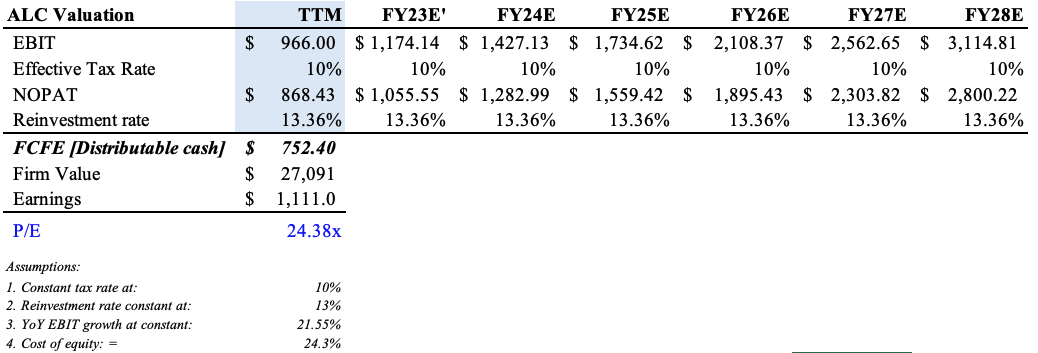

Hence, from the analysis so far, we've obtained a great deal of information about ALC's sustainable growth rate over the next few years, how much it needs to reinvest to grow, and the cash left over for investors. If we presume Alcon Inc. can at least maintain its growth and reinvestment rates over the next 5 years, discounting this back at the cost of equity, we believe it's fairly valued at 24.4x earnings, well behind its current rating of 77x/33x GAAP/non-GAAP earnings. If it pulls back or re-rates to this level, we are buyers. Hopefully, this explains the concept of why generating an EP is so essential to intrinsic value.

Exhibit 6. Fair value estimate of 24.4x

{kind=link}

In short

All growth is not created equally. Simply examining YoY growth rates of stated earnings isn't enough. A company needs to generate a return on its investments above its cost of capital. Otherwise, the growth, whilst good for the company, is value-destructive for shareholders. It also means, likely, that external financing will be required to fund the growth - again, value destructive for the equity holders. Consequently, we reiterate Alcon Inc. a hold at 24x earnings.

For further details see:

Alcon: Case Of Growth Destructive To Value, Reiterate Hold At 24x Earnings